How Much Is Car Insurance for a 16-year-old Monthly

Car insurance for a 16-year-old monthly typically ranges from $200 to $500 or more, depending on location, vehicle, and driving record. While it’s expensive, smart choices like adding your teen to your policy or choosing a safe car can help reduce costs significantly.

[FEATURED_IMAGE_PLACEOLDER]

Key Takeaways

- Monthly premiums for 16-year-olds average $200–$500: This high cost reflects the increased risk associated with young, inexperienced drivers.

- Adding your teen to your policy is cheaper than a standalone plan: Most insurers offer family discounts when multiple drivers are covered under one policy.

- Vehicle type greatly impacts insurance rates: Sports cars and luxury vehicles cost more to insure than safe, practical models like sedans or SUVs with high safety ratings.

- Good student discounts can save 10–25%: Maintaining a B average or higher often qualifies teens for significant rate reductions.

- Location plays a major role in pricing: Urban areas with high traffic and theft rates typically have higher premiums than rural regions.

- Defensive driving courses may lower rates: Completing an approved course shows responsibility and can lead to discounts with many insurers.

- Usage-based insurance programs offer savings: Telematics devices that monitor driving habits can reward safe behavior with lower monthly payments.

📑 Table of Contents

- How Much Is Car Insurance for a 16-Year-Old Monthly? A Complete Guide

- Why Is Car Insurance So Expensive for 16-Year-Olds?

- Average Monthly Costs: What to Expect

- How to Reduce Car Insurance Costs for a 16-Year-Old

- Types of Coverage You Need for a Teen Driver

- Common Mistakes to Avoid

- Long-Term Strategies to Keep Costs Down

- Conclusion

How Much Is Car Insurance for a 16-Year-Old Monthly? A Complete Guide

So your teenager just got their license—congratulations! But now comes the reality check: car insurance. If you’re wondering, “How much is car insurance for a 16-year-old monthly?” you’re not alone. It’s one of the most common questions parents ask when their child starts driving. The short answer? It’s expensive—but not impossible to manage with the right strategy.

At 16, your teen is statistically more likely to be involved in an accident than any other age group. According to the Insurance Institute for Highway Safety (IIHS), drivers aged 16–19 are nearly three times more likely to be in a fatal crash per mile driven compared to drivers over 20. Because of this elevated risk, insurers charge significantly higher premiums for young drivers. But that doesn’t mean you’re stuck paying sky-high rates forever. With smart decisions—like choosing the right car, taking advantage of discounts, and maintaining good grades—you can keep costs more manageable.

In this guide, we’ll break down exactly what goes into determining car insurance for a 16-year-old monthly, explore real-world examples, and share practical tips to help you save money without sacrificing coverage. Whether you’re adding your teen to your existing policy or shopping around for the best deal, this article will give you the tools you need to make informed choices.

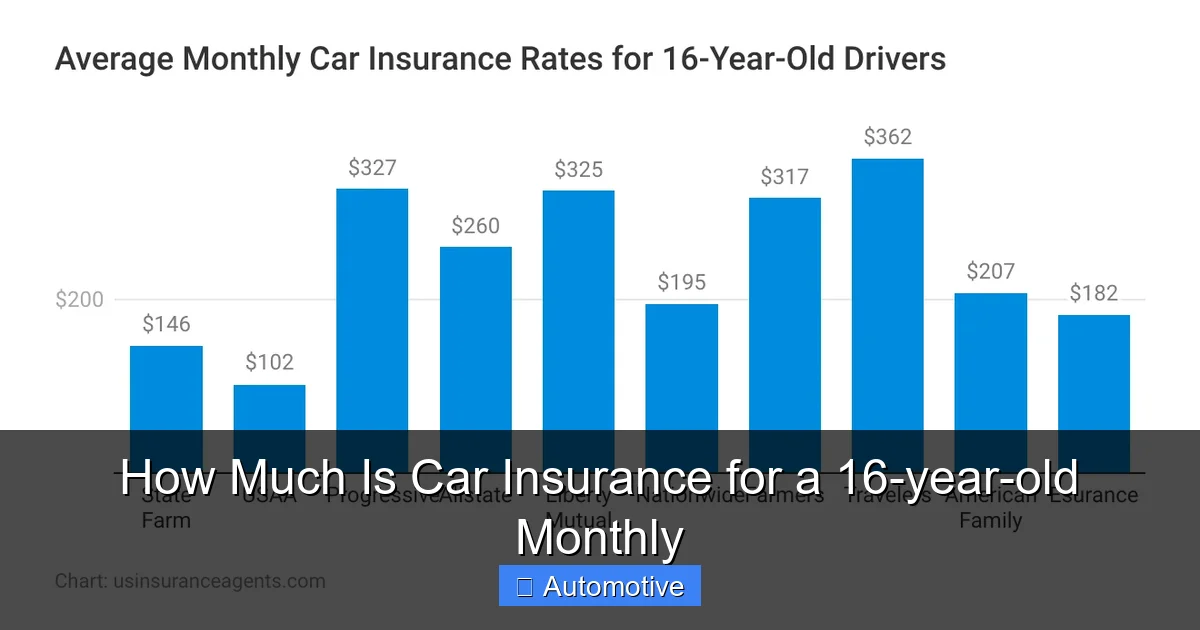

Why Is Car Insurance So Expensive for 16-Year-Olds?

Visual guide about How Much Is Car Insurance for a 16-year-old Monthly

Image source: usinsuranceagents.com

Let’s face it—insurance companies see 16-year-old drivers as high-risk. And they’re not wrong. Data from the National Highway Traffic Safety Administration (NHTSA) shows that in 2022, drivers aged 16–19 accounted for 5.5% of all motor vehicle crash fatalities, despite making up only about 4.5% of licensed drivers. That’s why premiums spike when a teen gets behind the wheel.

But it’s not just about accident rates. There are several factors that contribute to the high cost of insuring a 16-year-old:

Lack of Driving Experience

At 16, most teens have only been driving for a few months. They haven’t yet developed the judgment, reflexes, or situational awareness that come with years on the road. Insurers know that inexperience leads to mistakes—like misjudging distances, overcorrecting during emergencies, or getting distracted by passengers or phones.

Higher Likelihood of Risky Behavior

Teen drivers are more prone to speeding, distracted driving, and driving under the influence. A CDC study found that in 2021, 30% of teen drivers involved in fatal crashes were speeding at the time. Even if your teen is responsible, insurers base rates on group statistics—not individual behavior.

Increased Claims Frequency and Severity

Not only do teens get into more accidents, but those accidents tend to be more severe. This means higher repair bills, medical costs, and liability claims—all of which get passed on to policyholders in the form of higher premiums.

Gender and Age Factors

Historically, male teens have faced even higher rates than female teens due to higher accident involvement. While some states have banned gender-based pricing, it still plays a role in many areas. Additionally, 16-year-old males often pay the highest premiums of any demographic.

No Prior Insurance History

Unlike adults who may have years of continuous coverage, teens start with a blank slate. Insurers have no way to assess their risk based on past claims or payment history, so they default to the highest risk category.

All these factors combine to make car insurance for a 16-year-old monthly one of the most expensive insurance purchases a family can make. But understanding why helps you make smarter decisions—like choosing a safer car or enrolling in a defensive driving course—to offset some of that cost.

Average Monthly Costs: What to Expect

Visual guide about How Much Is Car Insurance for a 16-year-old Monthly

Image source: assets.goaaa.com

Now for the big question: How much will it actually cost? The national average for car insurance for a 16-year-old monthly ranges from **$200 to $500**, but this can vary widely based on several variables.

Let’s look at some real-world examples to give you a clearer picture.

National Averages by State

Insurance costs vary dramatically by location. In states like Michigan or Louisiana, where no-fault laws and high litigation rates drive up premiums, a 16-year-old could pay $600 or more per month. In contrast, states like Maine or North Dakota, which have lower population density and fewer accidents, might see rates closer to $150–$250.

For example:

– **California**: Average monthly premium for a 16-year-old: $350–$450

– **Texas**: $300–$400

– **Florida**: $400–$550 (due to high uninsured driver rates and hurricanes)

– **Ohio**: $200–$300

– **New York**: $450–$600

These are rough estimates and can change based on your specific ZIP code, driving record, and vehicle.

Standalone vs. Adding to Parent’s Policy

One of the biggest decisions you’ll make is whether to put your teen on their own policy or add them to yours. In almost every case, **adding your teen to your existing policy is cheaper**.

For instance, if your current family policy costs $1,800 per year ($150/month), adding a 16-year-old might increase it to $3,600–$4,800 annually—meaning an extra $150–$275 per month. That’s still far less than the $2,400–$6,000+ a standalone policy would cost.

Standalone policies are rare for teens and usually only used if the parent isn’t insured or the teen owns the car outright. Even then, most insurers prefer to keep young drivers on family plans.

Impact of Vehicle Type

The car your teen drives has a huge impact on insurance costs. Insurers consider safety ratings, repair costs, theft rates, and performance.

For example:

– A **2020 Honda Civic** (safe, reliable, low theft rate): $220/month

– A **2022 Ford Mustang GT** (high-performance, expensive to repair): $450+/month

– A **2018 Toyota RAV4** (safe SUV, moderate repair costs): $260/month

– A **2023 BMW 3 Series** (luxury, high theft, costly parts): $500+/month

Choosing a used, mid-size sedan with good crash test ratings can save hundreds per year.

Credit and Driving Record (Even for Teens)

While teens don’t have long credit histories, some states allow insurers to use credit-based insurance scores. A poor score—even at 16—can increase rates. Similarly, even a single speeding ticket can raise premiums by 10–20%.

For example, a clean-record 16-year-old in Ohio might pay $220/month, but with a speeding ticket, that jumps to $260–$280.

How to Reduce Car Insurance Costs for a 16-Year-Old

Visual guide about How Much Is Car Insurance for a 16-year-old Monthly

Image source: eggbev.com

The good news? There are several proven ways to lower car insurance for a 16-year-old monthly. With a little effort, you can cut your bill by 20%, 30%, or even more.

1. Add Your Teen to Your Policy

As mentioned earlier, this is almost always the cheapest option. Most insurers offer multi-car and multi-driver discounts when you bundle policies. Plus, your teen benefits from your (hopefully) clean driving record and years of loyalty.

2. Take Advantage of Good Student Discounts

Many insurers offer **good student discounts** of 10–25% for teens who maintain a B average or higher. You’ll usually need to provide a report card or transcript, but the savings add up fast.

For example, if your base premium is $300/month, a 15% discount saves you $45 every month—$540 per year.

3. Choose a Safe, Practical Vehicle

Avoid sports cars, luxury vehicles, and models with high theft rates. Instead, opt for:

– Sedans with top safety picks (e.g., Honda Accord, Toyota Camry)

– Compact SUVs with advanced safety features (e.g., Subaru Forester, Mazda CX-5)

– Older, reliable models (e.g., 2015–2018 Honda CR-V)

These vehicles are cheaper to insure because they’re less likely to be stolen, cost less to repair, and perform well in crashes.

4. Enroll in a Defensive Driving Course

Many insurers offer discounts for completing an approved driver education or defensive driving course. These programs teach hazard recognition, skid control, and distraction management.

For example, State Farm offers up to a 15% discount for teens who complete their Steer Clear® program. GEICO and Progressive also offer similar programs.

5. Use Telematics or Usage-Based Insurance

Programs like Allstate’s Drivewise®, Progressive’s Snapshot®, or State Farm’s Drive Safe & Save® use a mobile app or device to monitor driving habits. Safe behaviors—like smooth braking, low speeds, and limited nighttime driving—can earn discounts of 10–30%.

For a 16-year-old, this is a great way to prove responsibility and earn lower rates over time.

6. Increase Deductibles (Carefully)

Raising your deductible from $500 to $1,000 can lower your premium by 10–15%. Just make sure you can afford to pay the higher out-of-pocket cost if you ever need to file a claim.

7. Maintain Continuous Coverage

Never let your policy lapse. A gap in coverage can lead to higher rates when you reapply. Even if your teen isn’t driving much, keep the policy active to avoid penalties.

8. Shop Around Annually

Insurance rates change frequently. What was the cheapest option last year might not be this year. Get quotes from at least three insurers every 12 months to ensure you’re getting the best deal.

Types of Coverage You Need for a Teen Driver

When insuring a 16-year-old, it’s important to have the right mix of coverage—not just the minimum required by law.

Liability Coverage (Required in Most States)

This covers damage and injuries your teen causes to others. It includes:

– **Bodily Injury Liability**: Pays for medical bills, lost wages, and pain and suffering of others.

– **Property Damage Liability**: Covers repairs to other vehicles or property.

Minimums vary by state, but experts recommend at least $100,000/$300,000/$100,000 (per person/per accident/property damage) for teens.

Collision Coverage

Pays to repair or replace your teen’s car after an accident, regardless of fault. Essential if the car is newer or valuable.

Comprehensive Coverage

Covers non-collision events like theft, vandalism, fire, or weather damage. Highly recommended, especially in high-risk areas.

Uninsured/Underinsured Motorist Coverage

Protects your teen if they’re hit by a driver with no or insufficient insurance. Required in some states, optional in others—but strongly advised.

Medical Payments (MedPay) or Personal Injury Protection (PIP)

Covers medical expenses for your teen and passengers, regardless of fault. PIP is broader and includes lost wages and rehab costs.

Rental Reimbursement and Roadside Assistance

These optional add-ons can be lifesavers. Rental reimbursement pays for a rental car while yours is being repaired. Roadside assistance covers towing, jump-starts, and flat tires.

For a 16-year-old, we recommend full coverage (liability + collision + comprehensive) if the car is worth more than $4,000. For older cars, you might drop collision and comprehensive to save money—but only if you can afford to replace the car out of pocket.

Common Mistakes to Avoid

Even with the best intentions, parents often make costly mistakes when insuring their teen drivers.

1. Putting the Car in the Teen’s Name

This might seem fair, but it can backfire. If the car is titled to your teen, they’ll need their own policy—which is much more expensive. Keep the car in your name and add your teen as a driver on your policy.

2. Skimping on Coverage to Save Money

Cutting corners on liability limits or dropping comprehensive coverage might save $20/month now, but it could cost you thousands if your teen causes a serious accident.

3. Not Reporting Good Grades

Many parents forget to submit report cards for good student discounts. Set a reminder each semester to update your insurer.

4. Ignoring Telematics Programs

If your insurer offers a safe driving app, use it. Even if your teen isn’t the safest driver yet, the data can help them improve—and earn discounts over time.

5. Not Updating the Policy When Circumstances Change

If your teen moves out, goes to college, or stops driving, notify your insurer. You might qualify for a “student away at school” discount or lower rates if the car is driven less.

Long-Term Strategies to Keep Costs Down

While car insurance for a 16-year-old monthly is expensive now, it will decrease over time—especially if your teen maintains a clean record.

Maintain a Clean Driving Record

No tickets, accidents, or claims. Even one at-fault accident can keep rates high for 3–5 years.

Continue Education and Training

Advanced driving courses, like those offered by AAA or local driving schools, can further reduce risk and may qualify for additional discounts.

Build a Positive Insurance History

The longer your teen drives without incidents, the more their risk profile improves. By age 18 or 19, premiums often drop significantly.

Consider a Named Driver Exclusion (Rarely Recommended)

Some policies allow you to exclude a driver from coverage. This means your teen wouldn’t be covered if they drive the car—even in an emergency. This is risky and not advised unless your teen truly never drives.

Plan for the Future

As your teen approaches 18, start comparing standalone policies. By then, they may qualify for lower rates, especially if they’ve completed driver training and maintained good grades.

Conclusion

So, how much is car insurance for a 16-year-old monthly? On average, expect to pay between $200 and $500—but that number isn’t set in stone. With smart choices, you can reduce that cost and protect your family at the same time.

Start by adding your teen to your existing policy, choosing a safe and affordable vehicle, and taking advantage of every discount available. Encourage responsible driving habits, enroll in telematics programs, and keep your teen’s grades up. Over time, these efforts will not only lower your premiums but also help your teen become a safer, more confident driver.

Remember, the goal isn’t just to save money—it’s to ensure your teen is protected on the road. A few extra dollars a month now can prevent financial disaster later. And as your teen gains experience, those high premiums will gradually come down, making car ownership a more manageable part of family life.

Investing in good insurance today is an investment in your teen’s future—and your peace of mind.

Frequently Asked Questions

How much is car insurance for a 16-year-old monthly on average?

Car insurance for a 16-year-old monthly typically ranges from $200 to $500, depending on location, vehicle, and driving record. Adding your teen to your policy is usually the most affordable option.

Can I get a discount if my 16-year-old has good grades?

Yes! Most insurers offer good student discounts of 10–25% for teens who maintain a B average or higher. You’ll need to submit a report card or transcript to qualify.

Is it cheaper to add my teen to my policy or get them their own?

Adding your teen to your existing policy is almost always cheaper than a standalone plan. Standalone policies for 16-year-olds are rare and significantly more expensive.

Does the type of car affect insurance rates for teens?

Absolutely. Sports cars, luxury vehicles, and models with high theft rates cost more to insure. Safe, practical cars like sedans or compact SUVs with high safety ratings are cheaper options.

Will taking a defensive driving course lower my teen’s insurance?

Yes, many insurers offer discounts of 10–15% for completing an approved defensive driving or driver education course. Check with your provider for eligible programs.

Can my teen earn lower rates by using a safe driving app?

Yes. Usage-based insurance programs like Progressive’s Snapshot or Allstate’s Drivewise monitor driving habits and can reward safe behavior with discounts of up to 30%.