Who Has the Cheapest Car Insurance

Finding the cheapest car insurance isn’t just about picking the lowest number—it’s about getting the best value for your coverage needs. Rates vary widely based on location, driving history, vehicle type, and more, but some insurers consistently offer lower premiums without sacrificing service.

Key Takeaways

- Geico and State Farm often rank among the most affordable options for drivers with clean records and good credit.

- Your location plays a major role in pricing—urban areas with high traffic and theft rates typically see higher premiums.

- Maintaining a clean driving record and good credit score can significantly reduce your monthly payments.

- Usage-based insurance programs from companies like Progressive and Allstate reward safe driving with discounts.

- Comparing quotes from at least three insurers is the most effective way to find the best deal.

- Bundling auto with home or renters insurance can unlock substantial savings across policies.

- Minimum coverage may be cheaper upfront, but it leaves you financially vulnerable in serious accidents.

📑 Table of Contents

- Who Has the Cheapest Car Insurance? A 2024 Guide to Saving on Your Premiums

- Top Insurers with the Cheapest Car Insurance Rates

- Factors That Affect Your Car Insurance Rates

- How to Find the Cheapest Car Insurance for Your Situation

- Common Myths About Cheap Car Insurance

- Final Thoughts: Finding the Right Balance

Who Has the Cheapest Car Insurance? A 2024 Guide to Saving on Your Premiums

Car insurance is one of those expenses you can’t avoid—but that doesn’t mean you have to overpay. Whether you’re a new driver just getting behind the wheel or a seasoned commuter looking to trim your monthly budget, knowing who has the cheapest car insurance can make a real difference in your wallet. The good news? Affordable coverage isn’t out of reach. With the right strategy, you can find quality protection without breaking the bank.

But here’s the catch: “cheapest” doesn’t always mean “best.” The lowest premium might come with high deductibles, poor customer service, or inadequate coverage limits. That’s why it’s crucial to look beyond the headline number and consider what you’re actually getting for your money. In this guide, we’ll walk you through the insurers that consistently offer competitive rates, explain the factors that influence your premium, and share practical tips to help you save—without sacrificing peace of mind.

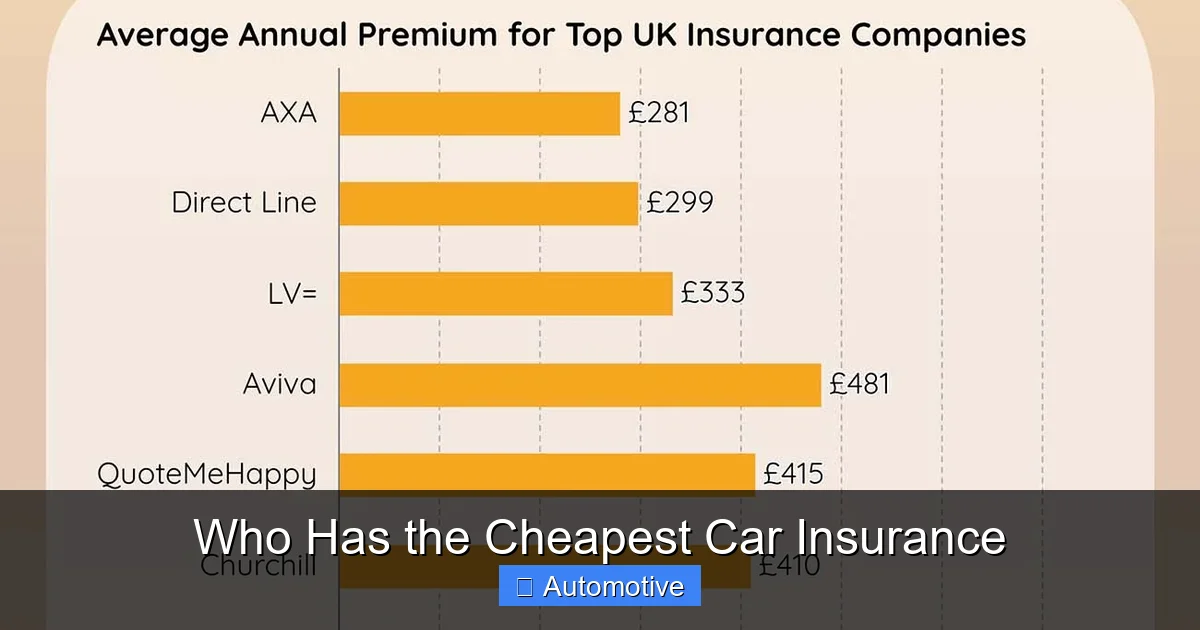

Top Insurers with the Cheapest Car Insurance Rates

Visual guide about Who Has the Cheapest Car Insurance

Image source: theentrepreneur-times.com

When it comes to affordability, not all insurance companies are created equal. While rates vary by state and individual profile, several providers stand out for offering some of the lowest average premiums in 2024. These companies combine competitive pricing with reliable service, making them strong contenders for budget-conscious drivers.

Geico: Consistently Low Rates and Strong Discounts

Geico frequently tops lists for the cheapest car insurance, especially for drivers with clean records. Known for its catchy ads and user-friendly online tools, Geico offers some of the most straightforward pricing in the industry. On average, Geico customers pay around $1,200 per year for full coverage—significantly less than the national average of about $1,700.

One reason Geico keeps costs down is its focus on direct-to-consumer sales. By minimizing overhead from physical offices and agents, the company passes savings directly to customers. They also offer a wide range of discounts, including safe driver, multi-vehicle, military, and good student discounts. For example, a college student with a B average could save up to 25% on their premium.

Geico also excels in digital convenience. Their mobile app allows you to file claims, view ID cards, and even get roadside assistance with just a few taps. This efficiency not only improves customer experience but also reduces administrative costs—another factor that helps keep premiums low.

State Farm: Personalized Service at Competitive Prices

State Farm is another major player known for affordable rates, particularly in rural and suburban areas. While it operates through a network of local agents, the company leverages technology to streamline quoting and claims processing. For drivers who prefer a human touch, State Farm offers the best of both worlds: personalized service and modern tools.

State Farm’s average annual premium for full coverage is around $1,300, making it one of the most budget-friendly options among large insurers. They also offer unique programs like Drive Safe & Save, which tracks your driving habits via a mobile app or device. Safe drivers can earn discounts of up to 30%, which can translate to hundreds of dollars in annual savings.

Additionally, State Farm rewards loyalty. Customers who stay with the company for several years often qualify for long-term customer discounts. They also offer bundling incentives—combining auto with home or renters insurance can save you up to 15% on both policies.

Progressive: Flexible Options and Snapshot Program

Progressive is a favorite among drivers who want flexibility and innovation. While their base rates are slightly higher than Geico or State Farm, Progressive makes up for it with powerful savings tools like Snapshot. This usage-based program monitors your driving behavior—things like hard braking, speeding, and mileage—and rewards safe habits with discounts.

Many Progressive customers see immediate savings after enrolling in Snapshot. In fact, the company reports that users save an average of $146 per year. For high-mileage drivers or those with less-than-perfect records, this program can be a game-changer.

Progressive also offers Name Your Price® tool, which lets you set a budget and see coverage options that fit. This is especially helpful if you’re on a tight budget and need to prioritize affordability. Plus, their website makes it easy to compare quotes side by side, so you can see exactly what you’re paying for.

USAA: Best for Military Members and Families

If you’re active-duty military, a veteran, or an eligible family member, USAA consistently offers the cheapest car insurance on the market. With average annual premiums under $1,000 for full coverage, USAA is hard to beat. They also rank highest in customer satisfaction year after year, according to J.D. Power.

USAA’s low rates come from a combination of member-focused pricing and low overhead. Because they only serve a specific group, they can tailor policies and discounts to military lifestyles—like deployment protection and overseas coverage. They also offer accident forgiveness and a vanishing deductible program, which reduces your deductible by $100 for every year you go claim-free.

While USAA isn’t available to the general public, it’s worth mentioning because it sets the gold standard for value and service. If you qualify, it’s almost always the cheapest and best option.

Other Budget-Friendly Options

Beyond the big names, several regional and niche insurers offer competitive rates. For example, Erie Insurance is known for low premiums in the Midwest and Pennsylvania, often beating national averages by 10–15%. Similarly, Auto-Owners Insurance provides affordable coverage in select states, with strong customer service and customizable policies.

For high-risk drivers—those with accidents, tickets, or poor credit—companies like The General and Dairyland specialize in non-standard insurance. While their rates are higher than average, they’re often the only option for drivers who’ve been denied coverage elsewhere. These insurers focus on getting you insured, even if it means paying a bit more upfront.

Factors That Affect Your Car Insurance Rates

Visual guide about Who Has the Cheapest Car Insurance

Image source: insuredaily.co.uk

Understanding what influences your premium is key to finding the cheapest car insurance. Insurers use a complex formula to calculate risk, and even small changes in your profile can lead to big savings. Here are the most important factors that determine how much you pay.

Location: Where You Live Matters

Your ZIP code is one of the biggest predictors of your insurance cost. Urban areas with high traffic density, crime rates, and accident frequency typically have higher premiums. For example, drivers in Detroit, Michigan, pay an average of $3,500 per year—more than double the national average—due to high theft and accident rates.

In contrast, rural areas with less traffic and lower crime see much lower rates. A driver in rural Montana might pay under $1,000 annually for the same coverage. Even within the same city, rates can vary by neighborhood. Insurers use location data to assess the likelihood of claims, so moving to a safer area—even just a few miles away—can reduce your premium.

Driving Record: Clean History = Lower Rates

Your driving history is a direct reflection of your risk level. Insurers look at accidents, speeding tickets, DUIs, and other violations when setting your rate. A single at-fault accident can increase your premium by 20–50%, while a DUI can double it.

On the flip side, maintaining a clean record for three to five years can qualify you for safe driver discounts. Many insurers offer accident forgiveness programs, which prevent your rate from increasing after your first accident. Geico, State Farm, and Progressive all offer this perk, making it easier to recover from a minor mistake.

Credit Score: The Hidden Factor

In most states, insurers use your credit-based insurance score to predict risk. Studies show that people with lower credit scores are more likely to file claims, so they’re charged higher premiums. A driver with excellent credit (750+) might pay $1,200 per year, while someone with poor credit (under 579) could pay $2,000 or more for the same coverage.

Improving your credit score—by paying bills on time, reducing debt, and checking for errors on your report—can lead to significant savings. Some states, like California, Hawaii, and Massachusetts, prohibit the use of credit in insurance pricing, but most still allow it.

Vehicle Type: What You Drive Impacts Cost

The make, model, and age of your car affect your premium. High-performance vehicles, luxury cars, and models with high theft rates cost more to insure. For example, insuring a BMW M3 will be far more expensive than a Honda Civic due to repair costs and theft risk.

On the other hand, safety features like anti-lock brakes, airbags, and electronic stability control can lower your rate. Some insurers offer discounts for vehicles with advanced safety tech, such as automatic emergency braking or lane departure warnings. Older cars may also be cheaper to insure, especially if they’re not worth much—comprehensive and collision coverage may not be cost-effective.

Coverage Level and Deductible

The type and amount of coverage you choose directly impact your premium. Minimum liability coverage is the cheapest option, but it only covers damage you cause to others—not your own vehicle. Full coverage, which includes collision and comprehensive, is more expensive but offers better protection.

Your deductible—the amount you pay out of pocket before insurance kicks in—also affects cost. A higher deductible means lower monthly payments, but you’ll pay more if you file a claim. For example, raising your deductible from $500 to $1,000 can save you 15–30% on your premium. Just make sure you can afford the deductible if an accident happens.

How to Find the Cheapest Car Insurance for Your Situation

Visual guide about Who Has the Cheapest Car Insurance

Image source: i.ytimg.com

Now that you know who offers low rates and what affects pricing, it’s time to take action. Finding the cheapest car insurance isn’t about luck—it’s about strategy. Follow these steps to get the best deal possible.

Shop Around and Compare Quotes

The single most effective way to save is to compare quotes from at least three different insurers. Prices can vary by hundreds of dollars for the same coverage, even among top companies. Use online comparison tools or contact insurers directly to get personalized quotes.

When comparing, make sure you’re looking at the same coverage limits and deductibles. A $100 difference in premium might not seem like much, but over a year, it adds up to $1,200. Don’t forget to ask about discounts—many people qualify for savings they don’t even know exist.

Take Advantage of Discounts

Most insurers offer a variety of discounts that can slash your premium. Common ones include:

– Safe driver discount (for no accidents or tickets)

– Good student discount (for maintaining a B average)

– Multi-car discount (for insuring more than one vehicle)

– Bundling discount (for combining auto with home or renters insurance)

– Low-mileage discount (for driving less than 7,500 miles per year)

– Defensive driving course discount (for completing an approved course)

Some companies also offer unique perks. For example, Geico gives a discount for federal employees, while State Farm rewards customers who install anti-theft devices. Be proactive—ask your agent or check the insurer’s website for a full list of available discounts.

Consider Usage-Based Insurance

If you’re a safe driver, usage-based programs can help you save big. These programs track your driving habits through a mobile app or plug-in device and reward good behavior with discounts. Progressive’s Snapshot, Allstate’s Drivewise, and State Farm’s Drive Safe & Save are popular options.

Most programs monitor things like speed, braking, acceleration, and time of day. The safer you drive, the more you save. Some users report discounts of 10–30%, which can mean hundreds of dollars in annual savings. Just remember: if you drive aggressively, these programs could actually increase your rate.

Raise Your Deductible (If You Can Afford It)

Increasing your deductible is one of the quickest ways to lower your premium. For example, raising your collision deductible from $500 to $1,000 can save you up to $200 per year. But only do this if you have enough savings to cover the higher out-of-pocket cost in case of an accident.

A good rule of thumb: keep at least $1,000 in an emergency fund if you choose a high deductible. This ensures you won’t be caught off guard by unexpected repair bills.

Maintain a Clean Driving Record and Good Credit

Long-term savings come from responsible habits. Avoid speeding tickets, accidents, and DUIs to keep your record clean. Over time, this will qualify you for lower rates and discounts.

Similarly, work on improving your credit score. Pay bills on time, keep credit card balances low, and check your credit report annually for errors. Even a 50-point increase in your score can lead to noticeable savings on your premium.

Common Myths About Cheap Car Insurance

There’s a lot of misinformation out there about car insurance. Let’s clear up some common myths that could be costing you money.

Myth 1: The Cheapest Policy Is Always the Best Deal

Not true. A low premium might come with high deductibles, limited coverage, or poor customer service. Always read the fine print and make sure the policy meets your needs. For example, minimum liability coverage might be cheap, but it won’t pay for your car if it’s totaled in an accident.

Myth 2: Red Cars Cost More to Insure

This is a persistent myth with no basis in fact. Insurers don’t care about your car’s color—only its make, model, age, and safety features. A red Honda Civic costs the same to insure as a blue one.

Myth 3: Your Insurance Will Automatically Cover a Rental Car

Most policies don’t include rental reimbursement unless you add it as an optional coverage. If you rent a car frequently or want peace of mind while your vehicle is in the shop, consider adding this feature—it usually costs just $5–$10 per month.

Myth 4: You Can’t Switch Insurers Mid-Term

You can switch at any time, though you may face a small cancellation fee. If you find a better deal, don’t wait—switching could save you hundreds. Just make sure your new policy starts before the old one ends to avoid a coverage gap.

Final Thoughts: Finding the Right Balance

So, who has the cheapest car insurance? The answer depends on your unique situation. Geico, State Farm, and Progressive consistently offer some of the lowest rates, especially for safe drivers with good credit. USAA is unbeatable for military members, while regional insurers like Erie and Auto-Owners provide competitive options in specific areas.

But the cheapest policy isn’t always the best. Focus on value—getting the right coverage at a fair price. Shop around, take advantage of discounts, and maintain good habits to keep your premiums low over time.

Remember, car insurance is about more than just cost. It’s about protection, peace of mind, and being prepared for the unexpected. By doing your research and making informed choices, you can find affordable coverage that truly works for you.

Frequently Asked Questions

Who has the cheapest car insurance for young drivers?

Geico and State Farm often offer the most affordable rates for young drivers, especially when discounts for good grades or defensive driving courses are applied. Some insurers also provide student-specific programs that reduce premiums for those under 25.

Does your car’s color affect insurance rates?

No, the color of your car does not impact your insurance premium. Insurers base rates on factors like make, model, age, safety features, and theft rates—not appearance.

Can I lower my car insurance by driving less?

Yes, many insurers offer low-mileage discounts for drivers who travel under 7,500 miles per year. Usage-based programs like Progressive’s Snapshot can also reward reduced driving with savings.

Is it worth switching insurers to save money?

Absolutely. Comparing quotes annually can reveal significant savings. Even if you’re happy with your current provider, shopping around ensures you’re not overpaying for coverage.

Do all states allow credit scores to affect insurance rates?

No, California, Hawaii, Massachusetts, and Michigan prohibit the use of credit scores in setting auto insurance rates. In most other states, insurers can use credit-based insurance scores to determine premiums.

What’s the difference between liability and full coverage?

Liability coverage pays for damage you cause to others, while full coverage includes collision and comprehensive, which protect your own vehicle. Full coverage is more expensive but offers greater financial protection.