What Is a Good 6-month Car Insurance Premium

Understanding what is a good 6-month car insurance premium helps you make smarter financial decisions. While national averages hover around $900–$1,200, your actual rate depends on driving history, location, vehicle type, and coverage needs. Comparing quotes and adjusting deductibles can significantly lower your premium.

Key Takeaways

- National average for 6-month premiums: Most drivers pay between $900 and $1,200 every six months, but this varies widely by state and individual profile.

- Your driving record matters most: A clean record can save you hundreds, while accidents or tickets may double your premium.

- Location plays a big role: Urban areas with high traffic and theft rates typically have higher premiums than rural zones.

- Vehicle type affects cost: Sports cars and luxury vehicles cost more to insure than sedans or compact SUVs.

- Coverage level determines price: Minimum liability coverage is cheapest, but full coverage offers better protection at a higher cost.

- Discounts can lower your bill: Safe driver, multi-policy, good student, and low-mileage discounts are common ways to save.

- Shopping around pays off: Getting quotes from at least three insurers can reveal savings of $200 or more per term.

📑 Table of Contents

What Is a Good 6-Month Car Insurance Premium?

If you’re like most drivers, you probably don’t think about your car insurance premium until it’s time to renew—or worse, until you get a rate increase in the mail. But understanding what is a good 6-month car insurance premium isn’t just about avoiding sticker shock. It’s about making informed choices that protect your wallet and your peace of mind.

Car insurance is a necessary expense for every licensed driver in the U.S., but not all policies are created equal. Some people pay $500 every six months, while others shell out over $2,000. So how do you know if you’re paying a fair price? The answer isn’t one-size-fits-all. A “good” premium depends on a mix of personal factors, market conditions, and the level of coverage you choose.

In this guide, we’ll break down everything you need to know about 6-month car insurance premiums—from national averages to hidden discounts—so you can confidently evaluate your policy and potentially save hundreds of dollars.

Understanding the Basics of Car Insurance Premiums

Visual guide about What Is a Good 6-month Car Insurance Premium

Image source: s3.amazonaws.com

Before diving into what makes a premium “good,” it helps to understand how insurers calculate your rate. Your car insurance premium is the amount you pay every six months (or monthly, if you choose that option) to keep your policy active. This fee covers the risk the insurer takes on by protecting you against accidents, theft, vandalism, and other covered events.

How Premiums Are Calculated

Insurance companies use complex algorithms—often called “rating factors”—to determine your premium. These factors include your age, gender (in most states), driving history, credit score (where allowed), location, vehicle type, annual mileage, and even your marital status. The more risk you present, the higher your premium will be.

For example, a 25-year-old male with a speeding ticket and a sports car living in downtown Chicago will likely pay much more than a 45-year-old married woman with a clean record driving a minivan in rural Iowa. That’s not discrimination—it’s actuarial science. Insurers analyze millions of claims data to predict who is more likely to file a claim.

Why 6-Month Terms Are Common

Most auto insurers offer policies in six-month terms because it allows them to adjust rates more frequently based on changing risk factors. If you get into an accident or move to a new city, your insurer can update your premium at renewal. It also gives you flexibility—if you find a better deal elsewhere, you’re only locked in for half a year.

Some companies also offer 12-month policies, but these are less common and often come with slightly higher overall costs due to administrative fees. For most drivers, the 6-month term strikes a balance between stability and adaptability.

National and State-by-State Averages

Visual guide about What Is a Good 6-month Car Insurance Premium

Image source: insurance6.co.uk

So, what is a good 6-month car insurance premium in real numbers? Let’s look at the data.

The National Average

According to recent reports from sources like the National Association of Insurance Commissioners (NAIC) and ValuePenguin, the average 6-month car insurance premium in the U.S. is around $1,050. That breaks down to about $175 per month. However, this is just an average—many drivers pay significantly less, while others pay much more.

Full coverage policies (which include comprehensive and collision) tend to cost more than minimum liability-only policies. On average, full coverage runs about $1,200–$1,500 every six months, while minimum coverage averages $500–$700.

State-by-State Variations

Where you live has a huge impact on your premium. States with high population density, strict insurance laws, or frequent natural disasters often have higher rates.

For example:

– Michigan has the highest average 6-month premium in the nation—over $2,500—due to its unique no-fault insurance system and unlimited personal injury protection (PIP) coverage.

– Louisiana and Florida also rank among the most expensive, with averages above $2,000, driven by high accident rates, hurricanes, and litigation culture.

– On the lower end, Maine, Wisconsin, and Ohio offer some of the most affordable premiums, often under $700 for six months.

Here’s a quick snapshot of average 6-month premiums by state (rounded):

– California: $1,100

– Texas: $1,300

– New York: $1,400

– Illinois: $1,000

– Georgia: $1,600

– North Carolina: $750

Keep in mind that these are averages. Your actual rate could be higher or lower based on your personal profile.

Factors That Influence Your Premium

Visual guide about What Is a Good 6-month Car Insurance Premium

Image source: images.ctfassets.net

Now that you know the averages, let’s explore the key factors that determine whether your premium is “good” or not.

Driving History

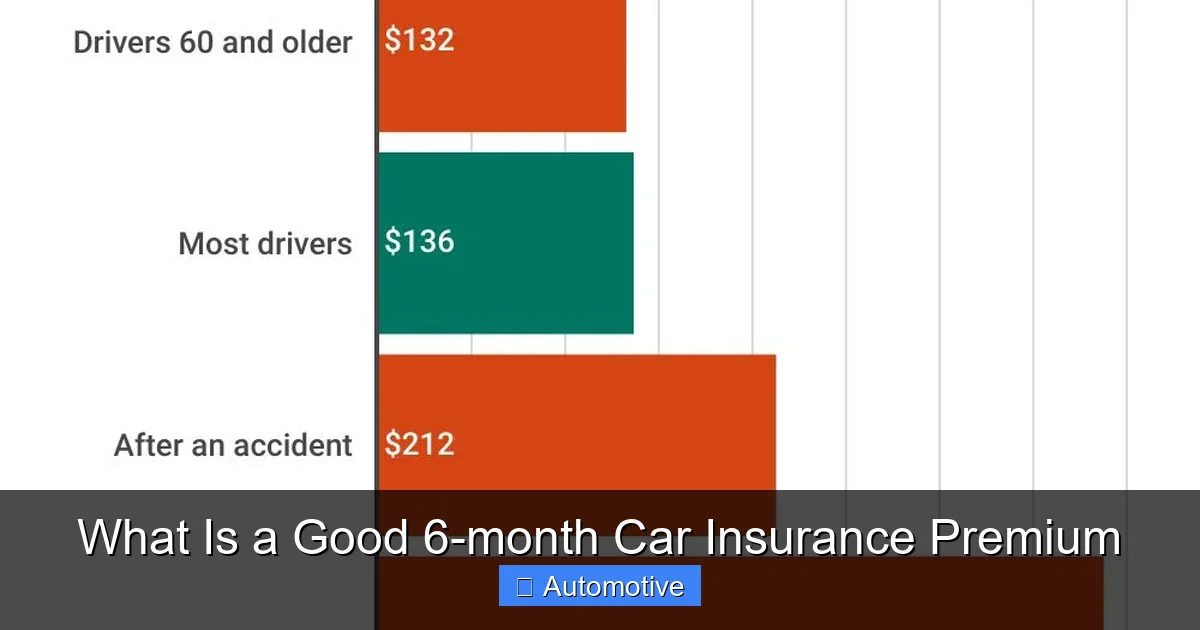

Your driving record is one of the biggest predictors of your insurance cost. Insurers love safe drivers—they’re less likely to file claims. If you have a clean record with no accidents, tickets, or DUIs, you’re in a strong position to qualify for lower rates.

Conversely, even one at-fault accident can increase your premium by 20–50%. A DUI? That could double your rate or more. For example, a driver with a clean record paying $900 every six months might see their premium jump to $1,350 after a speeding ticket—and even higher after an accident.

Age and Experience

Young drivers, especially teens, face the highest premiums due to their lack of experience and higher accident rates. A 16-year-old driver might pay $3,000 or more every six months, while a 30-year-old with five years of clean driving might pay half that.

Premiums generally decrease as you gain experience, reaching a low point around age 50–60. After that, rates may start to rise again due to increased risk of health-related driving issues.

Vehicle Type

The car you drive directly affects your premium. Insurers consider:

– Safety ratings: Safer cars cost less to insure.

– Theft rates: High-theft vehicles (like certain Honda and Toyota models) cost more.

– Repair costs: Luxury and electric vehicles often have expensive parts and labor.

– Performance: Sports cars and high-horsepower vehicles are riskier to insure.

For example, insuring a Toyota Camry will typically cost less than insuring a BMW M3 or a Tesla Model S—even if both drivers have identical profiles.

Location and Usage

Urban drivers pay more than rural ones. Why? More traffic means more accidents. Higher population density increases the risk of theft, vandalism, and uninsured motorists. Parking in a garage vs. on the street also matters.

Annual mileage is another factor. If you drive 20,000 miles a year, you’re on the road more—and more likely to have an accident—than someone who drives 5,000 miles. Insurers may charge higher rates for high-mileage drivers.

Credit Score (Where Allowed)

In most states (except California, Hawaii, and Massachusetts), insurers use credit-based insurance scores to predict risk. Studies show that people with lower credit scores tend to file more claims. As a result, a poor credit score can increase your premium by hundreds of dollars.

Improving your credit—even by a few points—can lead to noticeable savings over time.

Coverage Level and Deductibles

The type and amount of coverage you choose dramatically affect your premium. Here’s a quick breakdown:

– Liability-only: Covers damage and injuries you cause to others. Cheapest option, but leaves your own car unprotected.

– Collision: Pays for damage to your car from accidents, regardless of fault.

– Comprehensive: Covers non-collision events like theft, fire, hail, or hitting an animal.

– Uninsured/Underinsured Motorist: Protects you if you’re hit by someone without adequate insurance.

Most drivers opt for full coverage (liability + collision + comprehensive), which offers the best protection but costs more.

Your deductible—the amount you pay out of pocket before insurance kicks in—also impacts your premium. A higher deductible (e.g., $1,000 vs. $500) lowers your premium because you’re taking on more risk. Just make sure you can afford the deductible if you need to file a claim.

How to Determine If Your Premium Is “Good”

Now that you understand the factors, how do you know if your 6-month premium is fair?

Compare to National and Local Averages

Start by comparing your premium to the national average ($1,050) and your state’s average. If you’re paying $1,400 in a state where the average is $800, you might be overpaying—especially if your profile is low-risk.

But don’t stop there. Look at local averages too. Rates can vary widely even within the same state. A driver in downtown Los Angeles will pay more than someone in a small town 50 miles away.

Evaluate Your Personal Risk Profile

Ask yourself:

– Do I have a clean driving record?

– Am I a low-mileage driver?

– Do I drive a safe, common vehicle?

– Do I live in a low-risk area?

If you answered “yes” to most of these, and your premium is above $1,200, you might be paying too much.

Conversely, if you’re a young driver with a sports car in a high-theft area, a $1,500 premium might actually be a good deal.

Use Online Comparison Tools

Websites like NerdWallet, The Zebra, and Insurify allow you to compare quotes from multiple insurers in minutes. Simply enter your details and see how your current rate stacks up.

For example, you might discover that switching from State Farm to Geico could save you $200 every six months—without changing your coverage.

Tips to Lower Your 6-Month Premium

Even if your premium seems fair, there’s almost always room to save. Here are proven strategies to reduce your cost.

Shop Around Annually

Insurance companies don’t reward loyalty with lower rates—they often raise prices over time. Make it a habit to get new quotes every year, even if you don’t plan to switch. You might be surprised by the savings.

Ask About Discounts

Many drivers don’t realize how many discounts are available. Common ones include:

– Safe driver discount: For accident-free driving.

– Multi-policy discount: Bundling auto and home insurance.

– Good student discount: For students with B averages or higher.

– Low-mileage discount: For driving under a certain number of miles per year.

– Defensive driving course discount: Completing an approved course.

– Pay-in-full discount: Paying your entire 6-month premium upfront.

Some insurers even offer telematics programs (like Progressive’s Snapshot or Allstate’s Drivewise), where you install a device or app that tracks your driving habits. Safe driving can earn you up to 30% off.

Raise Your Deductible

If you have savings to cover a higher out-of-pocket cost, increasing your deductible from $500 to $1,000 can reduce your premium by 10–25%. Just don’t set it so high that you can’t afford it in an emergency.

Drop Unnecessary Coverage

If you drive an older car worth less than $4,000, collision and comprehensive coverage might not be worth it. The cost of the coverage could exceed the car’s value. In that case, liability-only might be the smarter choice.

Improve Your Credit

In states where credit matters, boosting your score can lead to lower rates. Pay bills on time, reduce credit card balances, and check your credit report for errors.

Consider Usage-Based Insurance

If you don’t drive much, pay-per-mile or usage-based insurance might save you money. Companies like Metromile charge based on how many miles you drive, which can be a game-changer for retirees or remote workers.

When to Reassess Your Policy

Your insurance needs change over time. Here are signs it’s time to review your policy:

– You’ve moved to a new city or state.

– You’ve bought a new car.

– You’ve had an accident or ticket.

– Your driving habits have changed (e.g., working from home).

– You’ve gotten married or added a teen driver.

– You’ve improved your credit score.

Even if nothing has changed, it’s smart to reevaluate your policy every 6–12 months. The insurance market is competitive, and new discounts or plans may be available.

Conclusion

So, what is a good 6-month car insurance premium? There’s no single answer, but a good premium is one that offers fair value for your risk profile and coverage needs. For most drivers, that means paying between $900 and $1,200 every six months—though your actual cost could be higher or lower.

The key is to stay informed, compare options regularly, and take advantage of every discount available. A few smart choices—like raising your deductible, bundling policies, or switching insurers—can save you hundreds of dollars a year.

Remember, car insurance isn’t just a legal requirement—it’s a financial safety net. Paying a little more for the right coverage is always better than facing a huge bill after an accident. By understanding what goes into your premium and how to control it, you can drive with confidence—and keep more money in your pocket.

Frequently Asked Questions

What is the average 6-month car insurance premium in the U.S.?

The average 6-month car insurance premium in the United States is around $1,050, though this varies by state, driving history, and coverage level. Full coverage typically costs more than minimum liability-only policies.

Is $800 for 6 months a good car insurance premium?

Yes, $800 for six months is generally considered a good premium, especially if you have a clean driving record and live in a low-risk area. It’s below the national average, so you’re likely getting a fair deal.

Why is my car insurance so high?

Your premium may be high due to factors like a poor driving record, young age, expensive vehicle, urban location, or low credit score. Shopping around and asking about discounts can help reduce costs.

Can I lower my car insurance premium after an accident?

Yes, over time. As the accident ages (usually after 3–5 years), its impact on your premium decreases. Maintaining a clean record and taking a defensive driving course can also help lower your rate.

Should I choose a higher deductible to save money?

A higher deductible can lower your premium, but only choose it if you can afford to pay that amount out of pocket after a claim. It’s a good strategy for drivers with emergency savings.

How often should I shop for car insurance?

It’s wise to compare car insurance quotes at least once a year, even if you don’t plan to switch. Rates change frequently, and you could miss out on significant savings by staying with the same insurer.