How to Negotiate Car Insurance Rates

Negotiating car insurance rates isn’t just for new customers—existing policyholders can save hundreds too. With the right approach, you can lower your premiums, improve coverage, and get better service—all without switching providers.

Key Takeaways

- Shop around regularly: Comparing quotes from multiple insurers every 6–12 months helps you find the best rates and strengthens your negotiating position.

- Leverage your loyalty: Long-term customers often qualify for hidden discounts—ask about loyalty, safe driver, or multi-policy perks.

- Improve your credit and driving record: Insurers use these factors to set rates; small improvements can lead to big savings.

- Bundle policies: Combining auto, home, or renters insurance with one provider often unlocks significant discounts.

- Ask for a review: Request an annual policy review to ensure you’re not overpaying for outdated coverage or missing out on new discounts.

- Negotiate confidently: Be polite but firm—know your worth, use competitor quotes as leverage, and don’t fear asking for a better deal.

- Consider raising your deductible: A higher deductible lowers your premium, but only choose an amount you can afford in an emergency.

📑 Table of Contents

How to Negotiate Car Insurance Rates

Let’s be honest—car insurance isn’t exactly exciting. It’s one of those monthly bills we pay without much thought, like electricity or internet. But what if I told you that you’re probably overpaying? And not just a little—maybe hundreds of dollars a year?

The truth is, most people never question their car insurance rates. They renew their policy automatically, assuming the price is fair. But insurance companies don’t reward loyalty with lower prices—they often do the opposite. In fact, studies show that long-term customers can pay up to 20% more than new ones for the same coverage.

The good news? You don’t have to settle. Negotiating your car insurance rates is not only possible—it’s easier than you think. Whether you’ve been with your insurer for five years or five months, there are proven strategies to lower your premium without sacrificing coverage. And you don’t need to be a financial expert or a master negotiator to do it.

In this guide, we’ll walk you through everything you need to know about how to negotiate car insurance rates. From understanding how insurers set prices to using competitor quotes as leverage, we’ll cover practical, actionable steps you can take today. By the end, you’ll feel confident calling your insurer and walking away with a better deal.

Why You Should Negotiate Your Car Insurance Rates

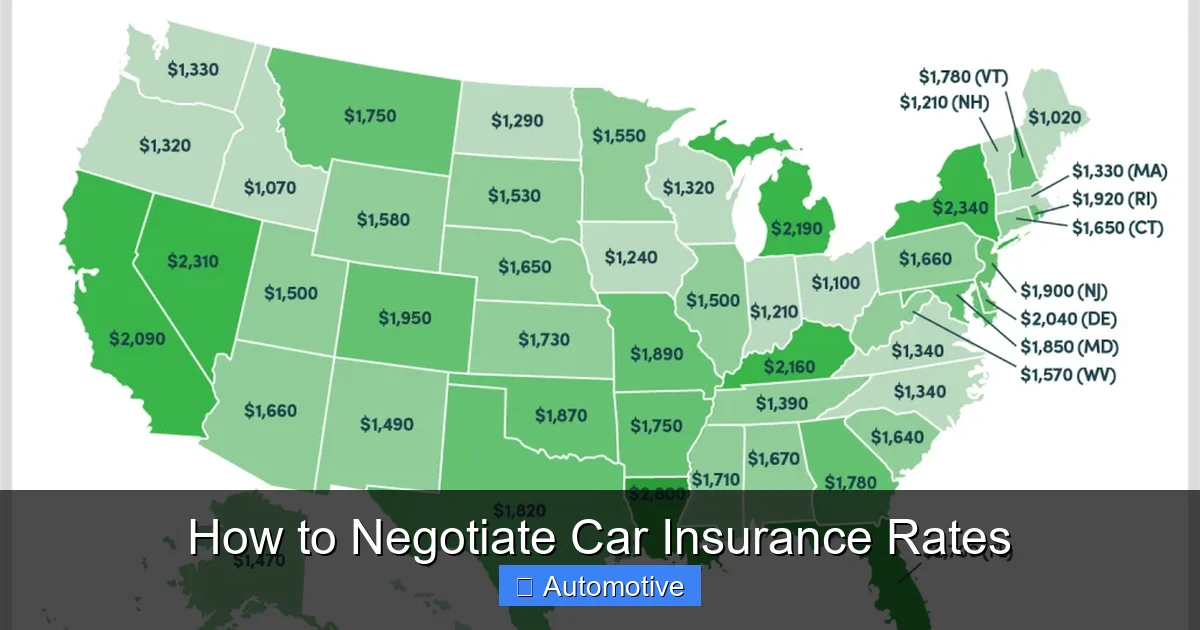

Visual guide about How to Negotiate Car Insurance Rates

Image source: koonz.com

You might be wondering: “Why bother negotiating? Isn’t my rate set in stone?” The short answer is no. Insurance premiums are not fixed—they’re based on a complex mix of factors, many of which change over time. And insurers have room to adjust them.

One of the biggest reasons to negotiate is that insurance companies often increase rates gradually, hoping customers won’t notice. They count on inertia—the tendency for people to stick with what they know. But when you take action, you disrupt that pattern.

Another reason? You might qualify for discounts you didn’t even know existed. For example, many insurers offer “loyalty discounts” for customers who’ve been with them over three years. Others reward safe driving, low mileage, or completing defensive driving courses. If you’ve made positive changes—like improving your credit score or installing anti-theft devices—your rate should reflect that.

Negotiating also gives you control. Instead of passively accepting a rate hike, you can advocate for yourself. And if your current insurer won’t budge? You can use that as leverage to switch to a competitor—or simply threaten to do so.

The Psychology Behind Insurance Pricing

Insurance companies use data-driven models to set rates. They analyze your age, location, driving history, vehicle type, credit score, and even your occupation. But here’s the catch: these models aren’t perfect. They rely on averages and assumptions, which means you might be paying more than you should.

For instance, if you live in a city with high traffic, your rate might be higher—even if you rarely drive. Or if you have a minor traffic violation from five years ago, it could still be affecting your premium, even though it’s no longer relevant.

Insurers also use behavioral economics. They know that most people won’t call to negotiate, so they don’t proactively offer the best rates. Instead, they wait for you to ask. That’s why negotiation is so powerful—it forces them to reconsider your value as a customer.

When to Negotiate

Timing matters. The best times to negotiate your car insurance rates include:

– **When your policy is up for renewal:** This is the most natural time to review your coverage and ask for a better rate.

– **After a life change:** Got married? Moved to a safer neighborhood? Improved your credit score? These can all lower your risk profile.

– **When you receive a rate increase notice:** Don’t just accept it—ask why and what you can do to reduce it.

– **After shopping around:** If you’ve found a better quote, use it as leverage.

– **During promotional periods:** Some insurers offer discounts during certain times of the year, like back-to-school or holiday seasons.

Step-by-Step Guide to Negotiating Your Car Insurance Rate

Visual guide about How to Negotiate Car Insurance Rates

Image source: isure.ca

Now that you understand why negotiation works, let’s get into the how. Follow these steps to negotiate your car insurance rate like a pro.

Step 1: Know Your Current Policy Inside and Out

Before you call your insurer, review your current policy. Know your coverage limits, deductibles, and any add-ons like roadside assistance or rental reimbursement. Also, check your premium—how much you’re paying monthly or annually.

Why is this important? You need to understand what you’re paying for so you can identify areas to adjust. For example, if you’re paying for full coverage on an older car, you might be over-insured. Or if your deductible is low, raising it could save you money.

Pro tip: Download a copy of your policy from your insurer’s website or app. Most companies make this easy. If you can’t find it, call customer service and request one.

Step 2: Gather Competing Quotes

This is your secret weapon. Get quotes from at least three other insurers. Use online comparison tools like NerdWallet, The Zebra, or Insurify, or contact agents directly.

When getting quotes, make sure the coverage is identical to your current policy. That way, you’re comparing apples to apples. For example, if your current policy has $100,000 in liability coverage and a $500 deductible, use those same numbers when requesting quotes.

Once you have the quotes, note the premiums. Even if they’re just slightly lower, they give you leverage. Insurers don’t want to lose customers to competitors, so a better quote can prompt them to match or beat it.

Step 3: Improve Your Risk Profile

Before negotiating, take steps to make yourself a lower-risk customer. This can include:

– **Improving your credit score:** Many states allow insurers to use credit-based insurance scores. Paying bills on time and reducing debt can boost your score.

– **Maintaining a clean driving record:** Avoid tickets and accidents. Some insurers offer accident forgiveness, but it’s not guaranteed.

– **Reducing mileage:** If you’ve started working from home or driving less, update your insurer. Low-mileage discounts can save you 5–15%.

– **Installing safety features:** Anti-theft devices, dash cams, or advanced driver assistance systems (ADAS) may qualify for discounts.

These changes don’t happen overnight, but even small improvements can help. For example, raising your credit score by 50 points could lower your premium by $100 or more per year.

Step 4: Call Your Insurer and Ask for a Better Rate

Now it’s time to make the call. Be polite, confident, and prepared.

Start by saying something like:

“Hi, I’ve been a loyal customer for [X] years, and I’ve always paid my premiums on time. I’ve recently shopped around and found a better rate with [Competitor Name]. I’d like to stay with you, but I need a more competitive offer.”

Then, present your case:

– Mention your loyalty and good payment history.

– Share the competing quote (be specific: “They’re offering the same coverage for $15 less per month”).

– Ask if there are any discounts you’re missing.

If the agent says no, ask to speak with a supervisor. Sometimes frontline agents don’t have the authority to offer discounts, but managers do.

Step 5: Be Ready to Walk Away

If your insurer won’t budge, be prepared to switch. Let them know you’re serious:

“I really value the service I’ve received, but I can’t justify paying more when I can get the same coverage elsewhere. I’ll need to cancel my policy unless we can find a better rate.”

In many cases, this prompts a last-minute offer. Insurers often have retention departments trained to keep customers. They may offer a discount, waive a fee, or upgrade your coverage at no extra cost.

But if they still say no? Don’t panic. You’ve already done the hard work—gathering quotes and knowing your worth. Switching is easier than you think, and the savings can be significant.

Common Discounts to Ask For

Visual guide about How to Negotiate Car Insurance Rates

Image source: clovered.com

Many people don’t realize how many discounts are available. Here are some of the most common ones to ask about:

Loyalty Discounts

If you’ve been with your insurer for three or more years, you may qualify for a loyalty discount. These can range from 5% to 15% off your premium. Ask specifically: “Do you offer a loyalty discount for long-term customers?”

Safe Driver Discounts

If you’ve gone three to five years without an accident or ticket, you likely qualify. Some insurers also offer discounts for completing a defensive driving course. These courses are often free or low-cost and can be completed online.

Multi-Policy (Bundling) Discounts

Combining your auto insurance with home, renters, or umbrella insurance can save you 10–25%. If you’re not already bundling, ask if it’s an option. Even if you rent, bundling auto and renters insurance can lead to savings.

Low-Mileage Discounts

If you drive less than 7,500–10,000 miles per year, you may qualify. Some insurers use telematics programs (like Progressive’s Snapshot or Allstate’s Drivewise) to track your mileage and driving habits. Safe, low-mileage drivers can earn significant discounts.

Good Student Discounts

Full-time students with a B average or higher may qualify for a discount. This usually applies to drivers under 25, but some insurers extend it to older students.

Pay-in-Full Discounts

Paying your annual premium upfront instead of monthly can save you 5–10%. It also avoids monthly service fees.

Paperless and Auto-Pay Discounts

Many insurers offer small discounts (usually $5–$10 per month) for going paperless or setting up automatic payments.

How to Use Competitor Quotes as Leverage

One of the most effective negotiation tactics is using competitor quotes. Here’s how to do it right.

Get Accurate, Detailed Quotes

When requesting quotes, provide the same information each time:

– Vehicle make, model, and year

– Driving history (accidents, tickets)

– Annual mileage

– Coverage limits and deductibles

– Personal details (age, gender, marital status)

Avoid estimates. The more accurate your info, the more reliable the quote.

Present the Quote Confidently

When you call your insurer, say:

“I’ve received a quote from [Competitor] for the same coverage at $[Amount] per month. That’s $[Difference] less than what I’m currently paying. Can you match or beat that rate?”

Be specific. Vague statements like “I found a better deal” won’t carry as much weight.

Ask for a Price Match or Better

Some insurers will match a competitor’s rate. Others may offer a slightly lower rate or throw in extras like free roadside assistance or a lower deductible.

If they refuse, ask: “Is there anything else you can offer to keep me as a customer?” Sometimes they’ll surprise you.

Document Everything

Keep records of your quotes, phone calls, and any offers made. If you decide to switch, you’ll need this info. If your insurer later claims they offered a discount you didn’t receive, you’ll have proof.

What to Do If Your Insurer Says No

Not every negotiation will succeed. If your insurer refuses to lower your rate, here’s what to do.

Ask for a Detailed Explanation

Politely ask why they can’t offer a better rate. Is it due to your driving record? Credit score? Location? Understanding the reason helps you address it.

For example, if your credit score is the issue, you can work on improving it and reapply in six months.

Request a Policy Review

Ask for a full review of your policy. Maybe you’re over-insured or paying for coverage you don’t need. Adjusting your coverage can lower your premium.

For instance, if your car is over 10 years old, you might drop collision and comprehensive coverage. Or if you have high liability limits, you could reduce them slightly (but not below state minimums).

Consider Switching Insurers

If all else fails, it’s time to switch. Use your competitor quotes to find the best deal. Make sure the new policy starts before your current one ends to avoid a coverage gap.

Switching is easier than you think. Most insurers handle the paperwork, and you can often keep the same agent if you’re working with an independent broker.

Leave on Good Terms

Even if you leave, be polite. You never know when you might want to return. And a positive exit can sometimes prompt a last-minute retention offer.

Long-Term Strategies to Keep Rates Low

Negotiating once isn’t enough. To keep your car insurance rates low over time, adopt these habits.

Review Your Policy Annually

Set a calendar reminder to review your policy every 12 months. Check for rate increases, new discounts, or changes in your needs.

Maintain a Clean Driving Record

Avoid speeding, distracted driving, and DUIs. Even one ticket can increase your premium by 20% or more.

Monitor Your Credit Score

Check your credit report annually and dispute errors. Pay bills on time and keep credit utilization low.

Drive Less

If possible, carpool, use public transit, or work from home. Lower mileage = lower risk = lower rates.

Stay Informed About Discounts

Insurance companies frequently update their discount programs. Follow your insurer on social media or check their website regularly.

Consider Usage-Based Insurance

Telematics programs track your driving and reward safe behavior. If you’re a cautious driver, this can lead to big savings.

Conclusion

Negotiating your car insurance rates isn’t just possible—it’s one of the easiest ways to save money without sacrificing coverage. By understanding how insurers set prices, gathering competitor quotes, and confidently advocating for yourself, you can lower your premium and keep more cash in your pocket.

Remember, insurance companies expect you to accept their rates. But when you take action, you stand out. You show that you’re informed, proactive, and worth keeping.

So don’t wait for your next renewal notice to roll in. Start today. Review your policy, shop around, and make that call. Whether you save $10 or $100, it’s money you didn’t have before.

And the best part? Once you’ve negotiated once, it gets easier. You’ll know what to say, what to ask for, and how to get results. Over time, those small savings add up—potentially hundreds of dollars a year.

So go ahead. Pick up the phone. Ask for a better rate. You’ve earned it.

Frequently Asked Questions

Can I negotiate my car insurance rate if I’ve had an accident?

Yes, you can still negotiate, but your options may be limited. Focus on other factors like loyalty, bundling, or improving your credit score. Some insurers offer accident forgiveness, so ask if you qualify.

How often should I shop around for car insurance?

It’s wise to shop around every 6–12 months. Rates change frequently, and new discounts may become available. Regular comparison ensures you’re always getting the best deal.

Will negotiating hurt my relationship with my insurer?

No, as long as you’re polite and professional. Insurers expect customers to ask for better rates. In fact, it shows you’re engaged and value their service.

Can I negotiate if I’m a new driver?

Yes, but your leverage may be limited. Focus on discounts for good grades, defensive driving courses, or low mileage. As you build a clean record, your negotiating power will grow.

What if my insurer won’t lower my rate even with a competitor quote?

If they refuse, consider switching. Use your quote to find a better deal elsewhere. Many insurers offer seamless transitions and may even cover your cancellation fees.

Is it better to negotiate or just switch insurers?

Try negotiating first—it’s free and could save you time. If your current insurer won’t budge, switching is a smart next step. Either way, you win.