How Much Is Car Insurance in Florida per Month?

Car insurance in Florida costs an average of $2,400 to $3,600 per year, or $200 to $300 per month—among the highest in the U.S. Rates vary widely based on age, location, driving history, and coverage level, but understanding your options can help you find affordable protection.

Key Takeaways

- Average monthly cost: Florida drivers pay between $200 and $300 per month for full coverage car insurance, significantly higher than the national average.

- State requirements: Florida mandates Personal Injury Protection (PIP) and Property Damage Liability (PDL), but not bodily injury liability, which impacts coverage and cost.

- Location matters: Urban areas like Miami, Fort Lauderdale, and Orlando have higher premiums due to traffic density, theft, and accident rates.

- Age and driving history: Young drivers under 25 and those with accidents or violations face much higher rates than older, experienced drivers.

- Credit score impact: Florida allows insurers to use credit-based insurance scores, meaning better credit can lead to lower premiums.

- Discounts available: Safe driver, multi-policy, good student, and anti-theft device discounts can reduce your monthly bill by 10–25%.

- Shopping around saves money: Comparing quotes from at least three insurers can help you find the best rate for your needs.

📑 Table of Contents

- How Much Is Car Insurance in Florida per Month?

- Florida’s Unique Insurance Requirements

- Factors That Affect Your Car Insurance Rate in Florida

- Average Car Insurance Rates by Age and Coverage Type

- How to Save Money on Car Insurance in Florida

- The Impact of Hurricanes and Natural Disasters

- Final Thoughts: Is Car Insurance in Florida Worth It?

How Much Is Car Insurance in Florida per Month?

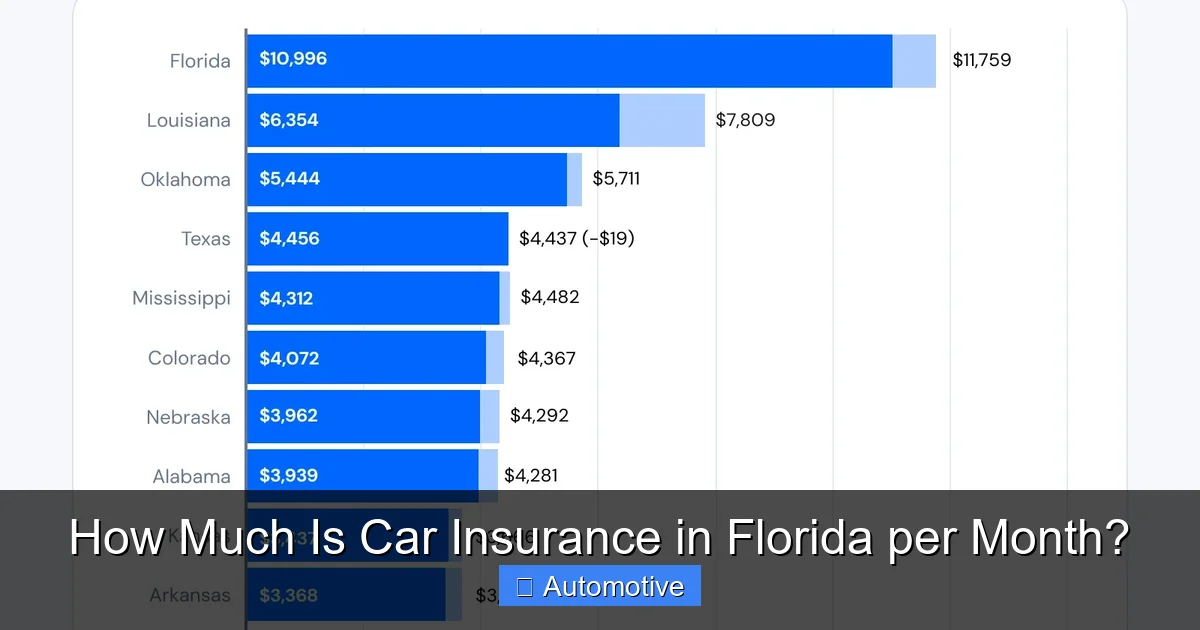

If you’re driving in the Sunshine State, you’ve probably noticed that car insurance isn’t cheap. In fact, Florida consistently ranks as one of the most expensive states for auto insurance in the country. So, how much is car insurance in Florida per month? The short answer: it depends. But on average, Florida drivers pay between $200 and $300 per month for full coverage—roughly $2,400 to $3,600 annually. That’s nearly double the national average of about $1,700 per year.

Why is Florida so expensive? It’s not just one thing—it’s a perfect storm of factors. High population density, frequent hurricanes, a large number of uninsured drivers, and a unique no-fault insurance system all contribute to higher premiums. Plus, Florida’s no-fault law requires drivers to carry Personal Injury Protection (PIP), which covers medical expenses regardless of who caused the accident. While this system aims to reduce lawsuits, it also drives up costs due to frequent claims and fraud.

But don’t panic just yet. While the numbers might look scary, there are ways to manage your car insurance costs. By understanding what affects your premium, knowing your coverage options, and shopping smart, you can find a policy that fits your budget without sacrificing protection. In this guide, we’ll break down everything you need to know about car insurance costs in Florida—from state requirements to money-saving tips.

Florida’s Unique Insurance Requirements

Visual guide about How Much Is Car Insurance in Florida per Month?

Image source: harrylevineinsurance.com

Unlike most states, Florida operates under a no-fault insurance system. This means that after an accident, your own insurance company pays for your medical expenses and lost wages, regardless of who was at fault. The goal is to reduce the number of lawsuits and speed up claims. But this system comes with specific requirements that directly impact how much you pay each month.

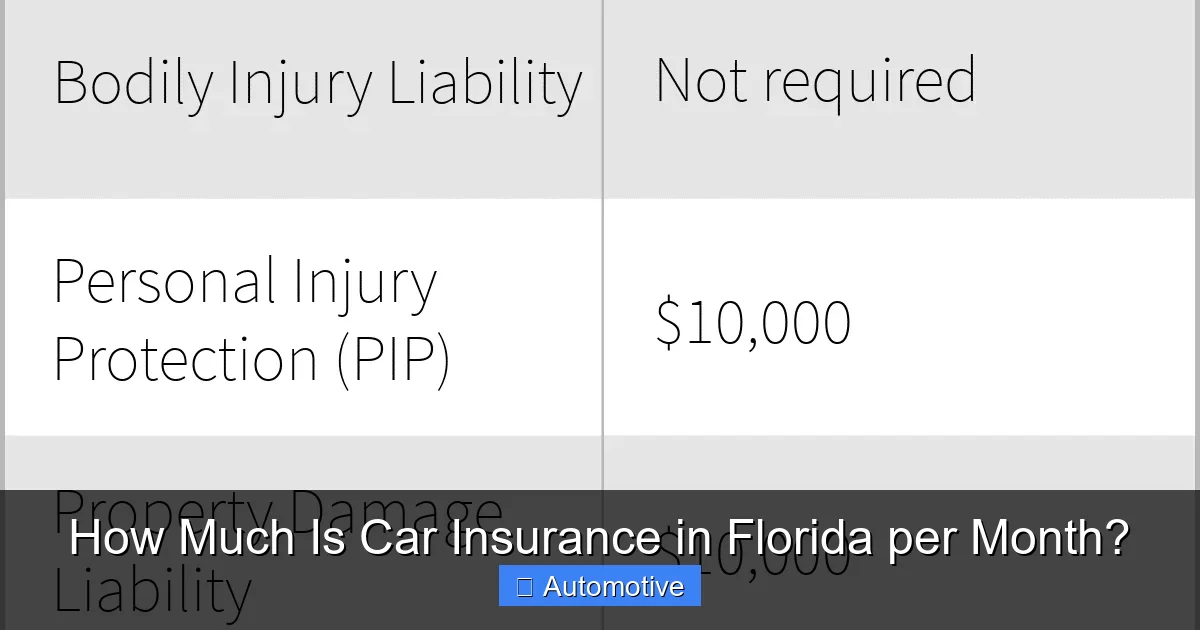

Minimum Coverage Requirements

In Florida, you must carry at least two types of coverage:

– Personal Injury Protection (PIP): This covers 80% of your medical expenses and 60% of lost wages up to $10,000, no matter who caused the accident. PIP is mandatory for all registered vehicles.

– Property Damage Liability (PDL): This covers damage you cause to someone else’s property, like their car or a fence. The minimum required is $10,000.

Notably, Florida does not require bodily injury liability (BIL) coverage, which pays for injuries you cause to others. This is unusual—most states require BIL—and it can leave drivers underinsured in serious accidents. While skipping BIL might lower your premium slightly, it’s risky. If you cause an accident that results in serious injuries, you could be personally sued for damages beyond your PIP limits.

Why No-Fault Increases Costs

The no-fault system sounds fair, but it has downsides. Because PIP covers your own injuries regardless of fault, there’s less incentive to drive carefully. This leads to more claims, especially for minor injuries. Additionally, Florida has a high rate of PIP fraud—some clinics and providers inflate bills or file fake claims, driving up costs for everyone.

Insurance companies pass these costs onto consumers. That’s why even basic coverage in Florida is more expensive than in many other states. For example, a driver in Ohio might pay $800 a year for similar coverage, while a Floridian pays over $2,000.

Optional Coverage You Should Consider

While PIP and PDL are the only legal requirements, they don’t offer complete protection. Here are optional coverages that can save you money in the long run:

– Bodily Injury Liability (BIL): Covers medical costs for others if you’re at fault. Recommended limits are $100,000 per person and $300,000 per accident.

– Collision Coverage: Pays for damage to your car from accidents, regardless of fault.

– Comprehensive Coverage: Covers non-collision events like theft, vandalism, fire, and hurricanes.

– Uninsured/Underinsured Motorist (UM/UIM): Protects you if you’re hit by a driver with no or insufficient insurance. Florida has one of the highest rates of uninsured drivers—nearly 20%—so this is highly recommended.

Adding these coverages will increase your monthly premium, but they provide peace of mind and financial protection in serious situations.

Factors That Affect Your Car Insurance Rate in Florida

Visual guide about How Much Is Car Insurance in Florida per Month?

Image source: a.storyblok.com

Your monthly car insurance premium isn’t set in stone. It’s based on a complex algorithm that considers dozens of factors. Understanding these can help you anticipate your cost and find ways to lower it.

Location: Urban vs. Rural

Where you live in Florida makes a big difference. Drivers in major cities like Miami, Fort Lauderdale, Tampa, and Orlando pay significantly more than those in smaller towns or rural areas. Why? Higher population density means more traffic, more accidents, and more theft. Miami, for example, has one of the highest car insurance rates in the nation, with average monthly premiums exceeding $400.

Even within a city, your ZIP code matters. Areas with higher crime rates or frequent flooding (common in South Florida) will have higher premiums. If you’re moving to Florida, consider how your location might affect your insurance costs.

Age and Driving Experience

Young drivers pay the most. Teens and drivers under 25 are considered high-risk because they’re more likely to be involved in accidents. A 16-year-old driver in Florida might pay $500 or more per month for full coverage. Rates begin to drop around age 25 and continue to decrease with age and clean driving records.

Older drivers (65+) may see slight increases due to slower reaction times, but they often qualify for discounts for safe driving or low mileage.

Driving Record and Claims History

Your driving history is one of the biggest factors. A clean record with no accidents or tickets can keep your rates low. But even one speeding ticket can increase your premium by 20–30%. At-fault accidents are worse—expect a 40–50% hike. DUIs or reckless driving convictions can double or even triple your rate.

If you’ve made multiple claims in the past three to five years, insurers may see you as a high-risk driver. Some companies may even refuse to renew your policy.

Credit Score

Yes, your credit score affects your car insurance in Florida. Unlike some states that ban the practice, Florida allows insurers to use credit-based insurance scores to determine risk. Drivers with excellent credit (750+) often pay 20–30% less than those with poor credit (below 600).

Why? Studies show that people with better credit tend to file fewer claims. If you’re working on improving your credit, you might see your insurance rates drop over time.

Vehicle Type and Usage

The car you drive matters. High-performance vehicles, luxury cars, and models with high repair costs come with higher premiums. For example, insuring a BMW or Tesla will cost more than a Honda Civic or Toyota Corolla.

How you use your car also plays a role. Commuting long distances, using your car for rideshare (like Uber or Lyft), or driving for work can increase your risk and your rate. Conversely, low annual mileage (under 7,500 miles) may qualify you for a discount.

Coverage Level and Deductible

The more coverage you buy, the higher your premium. Full coverage (liability, collision, comprehensive) costs more than minimum liability-only coverage. But skipping coverage to save money can backfire if you’re in an accident.

Your deductible—the amount you pay out of pocket before insurance kicks in—also affects your rate. A higher deductible (like $1,000) lowers your monthly premium, but you’ll pay more if you file a claim. A lower deductible (like $250) means higher monthly payments but less out-of-pocket cost when you need repairs.

Average Car Insurance Rates by Age and Coverage Type

To give you a clearer picture, let’s look at some real-world examples of how much car insurance costs in Florida per month, based on age, location, and coverage level.

Full Coverage vs. Minimum Coverage

For a 35-year-old driver with a clean record in Orlando:

– Minimum coverage (PIP + PDL): Around $150–$200 per month

– Full coverage (PIP, PDL, BIL, collision, comprehensive): $250–$350 per month

That’s a big difference. While minimum coverage meets legal requirements, it leaves you vulnerable in serious accidents. Full coverage offers much better protection, especially if you have a newer or financed vehicle.

Rates by Age Group

Here’s a breakdown of average monthly premiums for full coverage in Florida:

– 18-year-old: $450–$600

– 25-year-old: $300–$400

– 35-year-old: $250–$350

– 50-year-old: $200–$300

– 65-year-old: $180–$280

As you can see, young drivers pay a premium—literally. If you’re a parent adding a teen to your policy, expect a significant increase. But adding them to your policy (rather than getting them their own) is usually cheaper.

Rates by City

Location plays a huge role. Here are average monthly full coverage rates in major Florida cities:

– Miami: $350–$500

– Fort Lauderdale: $320–$450

– Tampa: $280–$400

– Orlando: $250–$350

– Jacksonville: $220–$320

– Tallahassee: $200–$300

South Florida is the most expensive due to hurricanes, traffic, and fraud. North Florida tends to be more affordable.

How to Save Money on Car Insurance in Florida

Even with high base rates, there are ways to reduce your monthly car insurance bill. A little effort can save you hundreds of dollars a year.

Shop Around and Compare Quotes

This is the #1 way to save. Rates vary widely between insurers. A policy that costs $300/month with one company might be $220/month with another. Get quotes from at least three insurers, including national brands (like GEICO, State Farm, Progressive) and regional companies (like Florida Farm Bureau or Tower Hill).

Use online comparison tools or work with an independent agent who can check multiple companies for you.

Take Advantage of Discounts

Most insurers offer discounts that can lower your premium by 10–25%. Common ones include:

– Safe driver discount: For no accidents or tickets in the past 3–5 years

– Multi-policy discount: Bundling auto and home or renters insurance

– Good student discount: For students with a B average or higher

– Low mileage discount: For driving under 7,500 miles per year

– Anti-theft device discount: For vehicles with alarms or tracking systems

– Defensive driving course: Completing an approved course can reduce your rate

Ask your insurer about all available discounts—you might be missing out.

Raise Your Deductible

If you can afford to pay more out of pocket in the event of a claim, raising your deductible from $500 to $1,000 can lower your monthly premium by 15–30%. Just make sure you have enough savings to cover the higher deductible if needed.

Improve Your Credit Score

Since Florida uses credit scores to set rates, improving your credit can lead to lower premiums. Pay bills on time, reduce credit card balances, and check your credit report for errors. Even a 50-point increase can make a difference.

Drive Safely and Avoid Claims

Maintaining a clean driving record is one of the best long-term strategies. Avoid speeding, distracted driving, and aggressive maneuvers. Also, consider whether a small claim is worth filing. If repair costs are close to your deductible, paying out of pocket might be cheaper than risking a rate increase.

Consider Usage-Based Insurance

Some insurers offer telematics programs that track your driving habits (speed, braking, mileage) via a mobile app or device. If you drive safely and infrequently, you could earn a discount of 10–20%. Programs like Progressive’s Snapshot or Allstate’s Drivewise are popular options.

The Impact of Hurricanes and Natural Disasters

Florida’s vulnerability to hurricanes and flooding also affects car insurance costs. Comprehensive coverage, which includes damage from storms, is especially important—and expensive—in coastal areas.

Hurricane Deductibles

In hurricane-prone regions, insurers often impose a separate hurricane deductible, which is a percentage of your car’s value (usually 2–5%) rather than a flat dollar amount. For a $30,000 car, a 5% deductible means you’d pay $1,500 out of pocket before insurance covers storm damage.

This can make comprehensive claims costly, but it also keeps premiums lower than they would be otherwise.

Flood Damage and Comprehensive Coverage

Standard auto insurance does not cover flood damage unless you have comprehensive coverage. Given Florida’s frequent storms and rising sea levels, this coverage is essential—especially if you live near the coast or in a flood zone.

If your car is totaled in a flood, comprehensive coverage will pay its actual cash value (minus your deductible). Without it, you’re on your own.

Insurance Fraud and Its Role in High Rates

Florida has a long-standing problem with insurance fraud, particularly in the PIP system. Fraudulent medical clinics, staged accidents, and inflated claims cost insurers billions each year. These losses are passed on to consumers in the form of higher premiums.

While the state has taken steps to combat fraud—such as stricter PIP regulations and anti-fraud task forces—it remains a challenge. Until fraud is reduced, rates are likely to stay high.

Final Thoughts: Is Car Insurance in Florida Worth It?

So, how much is car insurance in Florida per month? On average, $200 to $300 for full coverage. It’s expensive, no doubt. But given the state’s high accident rates, severe weather, and large number of uninsured drivers, having solid coverage is not just smart—it’s essential.

While you can’t control everything that affects your rate, you can take steps to lower it. Shop around, maintain a clean driving record, improve your credit, and take advantage of discounts. And don’t skimp on coverage—especially uninsured motorist and comprehensive protection.

Remember, the cheapest policy isn’t always the best. A low premium might mean high deductibles, poor customer service, or inadequate coverage. Focus on value: the right balance of price, protection, and reliability.

Driving in Florida comes with unique challenges, but with the right insurance, you can hit the road with confidence—knowing you’re protected, no matter what the Sunshine State throws your way.

Frequently Asked Questions

Why is car insurance so expensive in Florida?

Car insurance in Florida is expensive due to a combination of factors, including the no-fault insurance system, high rates of uninsured drivers, frequent hurricanes, and widespread insurance fraud. These issues lead to more claims and higher costs for insurers, which are passed on to consumers.

Do I need full coverage car insurance in Florida?

While only PIP and PDL are legally required, full coverage (including collision, comprehensive, and uninsured motorist) is highly recommended. It protects your vehicle from damage and provides financial security in serious accidents, especially given Florida’s high number of uninsured drivers.

Can I get car insurance in Florida with bad credit?

Yes, you can still get car insurance in Florida with bad credit, but your rates will likely be higher. Insurers use credit-based scores to assess risk, so improving your credit over time can help lower your premiums.

How much does it cost to add a teen driver in Florida?

Adding a teen driver to your policy can increase your premium by $200–$400 per month, depending on age and location. Teens are considered high-risk, but adding them to your policy is usually cheaper than getting them their own.

Does Florida require uninsured motorist coverage?

No, uninsured motorist (UM) coverage is not required in Florida, but it’s strongly recommended. Nearly 20% of Florida drivers are uninsured, so UM coverage protects you if you’re hit by someone without insurance.

How often should I shop for car insurance in Florida?

It’s a good idea to compare car insurance quotes at least once a year, or whenever your circumstances change (like moving, getting married, or improving your credit). Rates change frequently, and you could save hundreds by switching insurers.