How Much Is Car Insurance in California?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is the Average Cost of Car Insurance in California?

- 4 California’s Minimum Car Insurance Requirements

- 5 Factors That Affect Car Insurance Rates in California

- 6 How to Save Money on Car Insurance in California

- 7 Best Car Insurance Companies in California

- 8 Special Considerations for California Drivers

- 9 Conclusion

- 10 Frequently Asked Questions

Car insurance in California costs an average of $1,800 to $2,500 per year for full coverage, but prices vary widely based on location, driving record, and vehicle type. Understanding state requirements and shopping around can help you find affordable, reliable coverage.

If you’re driving in California, you’re not just cruising down scenic highways—you’re also navigating one of the most expensive car insurance markets in the U.S. Whether you’re a new driver in Sacramento, a commuter in San Diego, or a rideshare driver in San Francisco, understanding how much car insurance costs in the Golden State is essential. The truth is, there’s no one-size-fits-all answer. Your premium depends on a mix of personal factors, location, and the type of coverage you choose.

But don’t let that overwhelm you. While car insurance in California can feel pricey, knowing what drives the cost—and how to manage it—can make a big difference. From state-mandated minimums to optional add-ons like comprehensive and collision, there’s a lot to unpack. The good news? With the right strategy, you can get solid protection without breaking the bank. In this guide, we’ll break down everything you need to know about car insurance costs in California, including average rates, key influencing factors, and practical tips to save money.

Key Takeaways

- Average annual cost: Full coverage car insurance in California averages $2,100, while minimum liability coverage costs around $600–$800 per year.

- Location matters: Urban areas like Los Angeles and San Francisco have higher premiums due to traffic, theft, and accident rates.

- Driving record impacts rates: A clean record can save you hundreds, while accidents or DUIs can double your premium.

- Vehicle type affects pricing: Luxury, sports, and high-theft vehicles cost more to insure than sedans or SUVs with safety features.

- Credit score plays a role: California allows insurers to use credit-based insurance scores, so better credit often means lower rates.

- Discounts can lower costs: Safe driver, multi-policy, good student, and low-mileage discounts help reduce premiums.

- Shop around annually: Comparing quotes from at least three insurers can save you $300 or more per year.

📑 Table of Contents

- What Is the Average Cost of Car Insurance in California?

- California’s Minimum Car Insurance Requirements

- Factors That Affect Car Insurance Rates in California

- How to Save Money on Car Insurance in California

- Best Car Insurance Companies in California

- Special Considerations for California Drivers

- Conclusion

What Is the Average Cost of Car Insurance in California?

So, how much is car insurance in California, really? According to recent data from the National Association of Insurance Commissioners (NAIC) and industry reports, the average annual premium for full coverage car insurance in California is around $2,100. That’s about $175 per month. For minimum liability coverage—the bare minimum required by law—the average cost drops to roughly $650 to $800 per year, or $55 to $67 per month.

To put that in perspective, California’s average is slightly above the national average of about $1,780 for full coverage. But why the higher price tag? Several factors contribute, including the state’s high population density, expensive repair costs, and strict insurance regulations. For example, California requires all drivers to carry uninsured motorist coverage, which isn’t mandatory in every state. This adds to the overall cost but also provides valuable protection.

Let’s look at a real-world example. Sarah, a 35-year-old teacher living in Irvine with a clean driving record and a 2020 Honda CR-V, pays about $1,900 per year for full coverage. Meanwhile, Jake, a 22-year-old college student in downtown Los Angeles driving a used BMW, pays closer to $3,200 annually—nearly double—due to his age, location, and vehicle type. These differences highlight how personal and geographic factors dramatically affect pricing.

It’s also worth noting that premiums can vary significantly between insurers. One company might offer Sarah a rate of $1,700, while another quotes $2,300 for the same coverage. That’s why shopping around is so important. Even a small difference in monthly payments adds up over time.

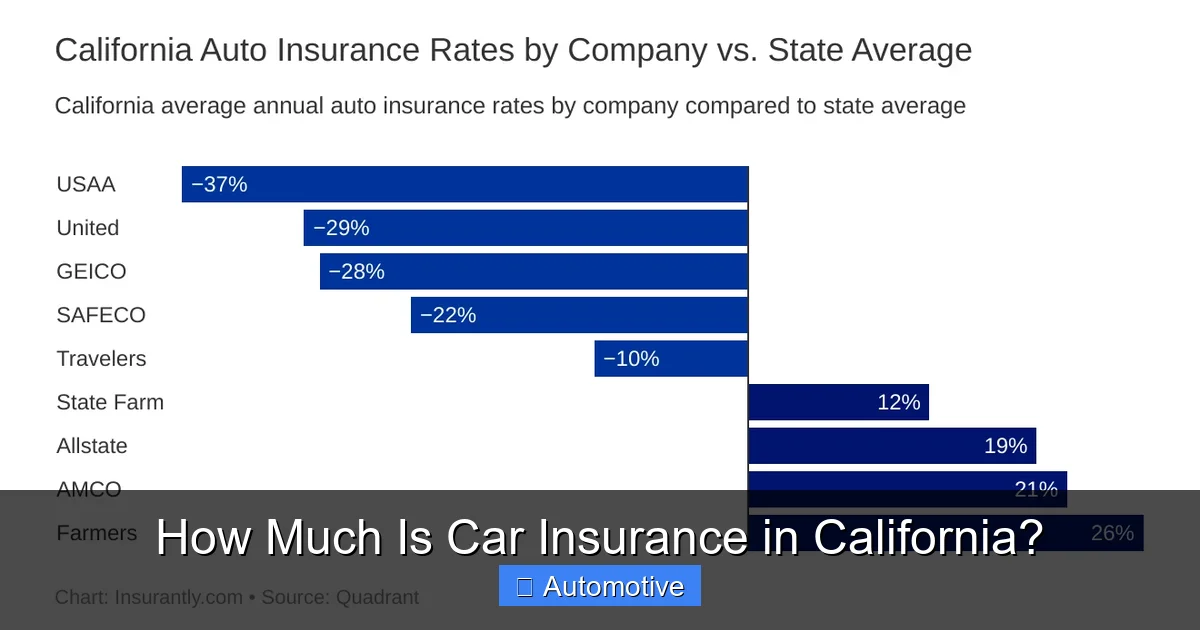

California’s Minimum Car Insurance Requirements

Visual guide about How Much Is Car Insurance in California?

Image source: insurantly.com

Before we dive deeper into costs, it’s crucial to understand what coverage California law requires. Unlike some states that allow drivers to post bonds or deposit cash, California mandates that all drivers carry auto insurance. The state follows a “fault-based” system, meaning the driver at fault in an accident is responsible for damages.

California’s minimum liability coverage is often referred to as “15/30/5.” Here’s what that means:

– $15,000 for bodily injury per person

– $30,000 for total bodily injury per accident

– $5,000 for property damage per accident

This coverage pays for injuries and damage you cause to others in an accident. It does not cover your own injuries or vehicle repairs. While this minimum meets legal requirements, it’s often insufficient for serious accidents. For instance, a single emergency room visit can easily exceed $15,000, leaving you personally liable for the difference.

Additionally, California requires uninsured/underinsured motorist (UM/UIM) coverage. This protects you if you’re hit by a driver with no insurance or insufficient coverage. The minimum UM/UIM limits match your liability limits—so if you carry 15/30/5, your UM/UIM must also be 15/30/5.

Many drivers opt for higher limits or full coverage to avoid financial risk. Full coverage typically includes liability, collision, and comprehensive insurance. Collision covers damage to your car from accidents, while comprehensive covers non-collision events like theft, vandalism, or natural disasters.

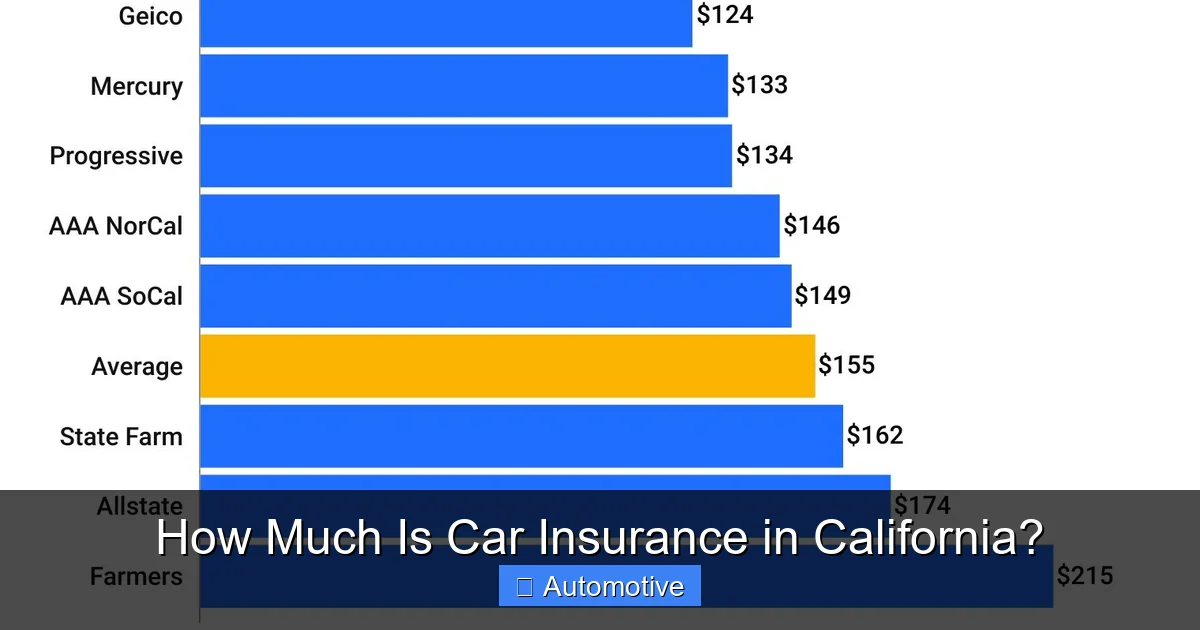

Factors That Affect Car Insurance Rates in California

Visual guide about How Much Is Car Insurance in California?

Image source: res.cloudinary.com

Now that you know the basics, let’s explore the key factors that determine how much you’ll pay for car insurance in California. Insurers use a complex algorithm to calculate premiums, but these are the most influential variables.

1. Your Driving Record

Your history behind the wheel is one of the biggest predictors of your insurance cost. A clean record with no accidents, tickets, or DUIs signals low risk to insurers. In contrast, even a single speeding ticket can increase your premium by 10–20%. A DUI? That can double or even triple your rates.

For example, a driver with a DUI conviction might pay $3,500 or more annually, compared to $1,800 for someone with a clean record. Some insurers even specialize in high-risk drivers, but their rates are significantly higher.

2. Where You Live

Location is a major factor in California. Urban areas like Los Angeles, San Francisco, and Oakland have higher premiums due to traffic congestion, higher accident rates, and increased vehicle theft. In contrast, rural areas like Redding or Bakersfield tend to have lower rates.

Even within the same city, ZIP codes matter. A driver in downtown San Jose might pay 20% more than someone in a suburban neighborhood just 15 miles away. Insurers analyze claims data by region, so high-crime or high-accident areas naturally cost more to insure.

3. Your Age and Gender

Young drivers, especially those under 25, face the highest premiums. Statistically, teens and young adults are more likely to be involved in accidents. A 19-year-old male in California might pay $4,000 or more per year for full coverage, while a 45-year-old woman with the same profile could pay half that.

Gender also plays a role, though California law limits how much insurers can use it. Historically, young men have higher accident rates, so they often pay more—but the gap is narrowing as driving behaviors evolve.

4. The Type of Vehicle You Drive

Your car’s make, model, year, and safety features directly impact your premium. Luxury vehicles, sports cars, and models with high theft rates (like certain Honda and Toyota models) cost more to insure. For example, insuring a Tesla Model 3 can be 30–50% more expensive than a Toyota Camry due to higher repair costs and advanced technology.

On the flip side, vehicles with strong safety ratings, anti-theft systems, and low repair costs often qualify for discounts. Hybrid and electric vehicles may also qualify for green discounts with some insurers.

5. Your Credit Score

California allows insurers to use credit-based insurance scores when setting rates. Studies show a correlation between credit history and claim frequency, so drivers with good credit (700+) typically pay less. Those with poor credit (below 600) may see premiums 20–40% higher.

Improving your credit score by paying bills on time, reducing debt, and checking for errors on your report can lead to lower insurance costs over time.

6. Coverage Level and Deductible

The more coverage you buy, the higher your premium. Choosing higher liability limits, adding comprehensive and collision, or lowering your deductible (the amount you pay out of pocket before insurance kicks in) will increase your cost.

For example, a $500 deductible might cost $200 more per year than a $1,000 deductible. But if you can afford the higher out-of-pocket cost, raising your deductible is a smart way to save.

How to Save Money on Car Insurance in California

Visual guide about How Much Is Car Insurance in California?

Image source: prontoinsurance.com

Now that you know what drives up your premium, let’s talk about how to bring it down. Saving on car insurance in California is absolutely possible—you just need the right strategy.

Shop Around and Compare Quotes

This is the single most effective way to save. Rates vary widely between insurers, even for identical coverage. Get quotes from at least three different companies, including national brands (like State Farm, Geico, and Progressive) and regional insurers (like Mercury or AAA).

Use online comparison tools or work with an independent agent who can access multiple carriers. Don’t just look at the price—compare coverage details, customer service ratings, and claims processes.

Take Advantage of Discounts

Most insurers offer a range of discounts. Common ones include:

– Safe driver discount: For accident-free driving over a set period

– Multi-policy discount: Bundling auto with home or renters insurance

– Good student discount: For students with a B average or higher

– Low-mileage discount: For driving fewer than 7,500 miles per year

– Defensive driving course: Completing an approved course can reduce rates

– Anti-theft device discount: For vehicles with alarms or tracking systems

Some insurers also offer telematics programs (like Progressive’s Snapshot or Allstate’s Drivewise), which monitor your driving habits and reward safe behavior with discounts.

Maintain a Clean Driving Record

This one’s obvious but worth repeating: avoid tickets and accidents. Even a minor fender bender can raise your rates for three to five years. If you do get a ticket, consider traffic school to keep it off your record—California allows this for most moving violations.

Improve Your Credit Score

Since credit affects your rate, take steps to boost your score. Pay bills on time, keep credit card balances low, and check your credit report annually for errors. Even a 50-point increase can lead to noticeable savings.

Choose the Right Vehicle

Before buying a car, check its insurance cost. Use online tools to estimate premiums for different models. Opt for vehicles with high safety ratings, low theft rates, and affordable repair costs.

Raise Your Deductible

If you have an emergency fund, consider raising your deductible from $500 to $1,000. This can reduce your premium by 15–30%. Just make sure you can afford the higher out-of-pocket cost if you need to file a claim.

Best Car Insurance Companies in California

With so many options, choosing the right insurer can feel overwhelming. Based on customer satisfaction, pricing, and coverage options, here are some of the top car insurance companies in California:

– State Farm: Known for excellent customer service and a large agent network. Offers competitive rates for safe drivers and strong bundling discounts.

– Geico: Often one of the cheapest options, especially for young drivers and military members. User-friendly online tools and mobile app.

– Progressive: Great for high-risk drivers and those with unique needs. Offers Name Your Price® tool and Snapshot telematics program.

– AAA: Popular in California for its roadside assistance and member perks. Rates can be higher, but service is top-notch.

– Mercury Insurance: A regional favorite with competitive pricing and strong local presence. Offers good discounts for multi-car and home policies.

When choosing a company, consider not just price but also claims handling, financial stability, and customer reviews. A cheap policy isn’t worth much if the insurer drags its feet on claims.

Special Considerations for California Drivers

California has some unique rules and challenges that affect car insurance.

Rideshare Insurance

If you drive for Uber or Lyft, your personal policy won’t cover you while you’re logged into the app. You need rideshare insurance, which bridges the gap between personal and commercial coverage. Many insurers now offer this add-on, but it can increase your premium by $100–$300 per year.

Wildfire and Natural Disaster Coverage

California is prone to wildfires, earthquakes, and mudslides. Standard comprehensive coverage includes fire and flood damage, but earthquake damage may require a separate policy. If you live in a high-risk area, make sure your policy includes adequate protection.

High Theft Rates

Certain vehicles, especially Honda Accords and Toyota Camrys, are frequently targeted by thieves. If you drive one of these models, you may pay more for comprehensive coverage. Installing a tracking device or parking in a secure garage can help reduce risk.

DMV Monitoring and SR-22 Requirements

If you’re convicted of a DUI or other serious violation, the DMV may require you to file an SR-22 form, proving you have insurance. This isn’t a policy—it’s a certificate filed by your insurer. High-risk drivers may need to maintain an SR-22 for one to three years, and not all insurers offer it.

Conclusion

So, how much is car insurance in California? The answer depends on you—your driving history, where you live, the car you drive, and the coverage you choose. While the average cost is around $2,100 per year for full coverage, your actual rate could be higher or lower.

The key takeaway? Don’t accept the first quote you get. Shop around, take advantage of discounts, and make informed decisions about your coverage. A little effort can save you hundreds—or even thousands—over the life of your policy.

Remember, car insurance isn’t just a legal requirement—it’s your financial safety net. Whether you’re commuting to work, road-tripping up the coast, or picking up the kids from school, the right policy gives you peace of mind. In a state as dynamic and diverse as California, that protection is priceless.

Frequently Asked Questions

How much is car insurance in California for a new driver?

New drivers in California, especially those under 25, typically pay higher premiums due to lack of experience. Expect to pay $3,000 to $5,000 per year for full coverage, depending on age, location, and vehicle. Taking a defensive driving course and maintaining good grades can help reduce costs.

Is car insurance cheaper in California if I have good credit?

Yes, drivers with good credit (700+) often pay 10–30% less than those with poor credit. California allows insurers to use credit-based insurance scores, so improving your credit can lead to lower premiums over time.

Can I drive without car insurance in California?

No. California law requires all drivers to carry at least minimum liability coverage. Driving without insurance can result in fines, license suspension, and vehicle impoundment. If you’re caught uninsured in an accident, you could face even harsher penalties.

Do I need full coverage car insurance in California?

Full coverage isn’t legally required, but it’s highly recommended if you have a loan or lease, or if your vehicle is valuable. It protects you from financial loss due to accidents, theft, or natural disasters, offering more comprehensive protection than minimum liability.

How often should I shop for car insurance in California?

It’s smart to compare quotes at least once a year, or whenever your circumstances change (like moving, buying a new car, or getting a ticket). Rates change frequently, and you could save $200–$500 by switching insurers.

Does California have a low-cost car insurance program?

Yes, the California Low Cost Automobile Insurance Program (CLCA) offers affordable liability coverage to eligible low-income drivers. Premiums start as low as $250 per year, but eligibility is based on income and other factors. Visit the CLCA website to see if you qualify.