Does Chase Sapphire Cover Rental Car Insurance

Yes, the Chase Sapphire Preferred® and Chase Sapphire Reserve® cards offer primary rental car insurance coverage when you pay for your rental with the card. This benefit can save you money by covering damage due to collision or theft—without filing a claim on your personal auto policy.

If you’ve ever rented a car—whether for a quick weekend trip, a business meeting across town, or a dream vacation abroad—you’ve probably stood at the counter and been asked: “Would you like to add collision damage waiver?” It’s that moment where your heart skips a beat, your wallet feels lighter, and you wonder if your credit card already has your back.

Well, if you’re a proud cardholder of either the Chase Sapphire Preferred® or the Chase Sapphire Reserve®, the answer might just be yes. These premium travel credit cards come packed with benefits, and one of the most valuable—and often underused—is their rental car insurance coverage. But here’s the catch: not all rentals are covered, not all situations qualify, and understanding the fine print can mean the difference between saving hundreds of dollars or paying out of pocket after an accident.

In this guide, we’ll walk you through everything you need to know about whether Chase Sapphire covers rental car insurance, how it works, what’s included (and what’s not), and how to make the most of this powerful perk. Whether you’re planning a cross-country road trip or just need a temporary ride while your car’s in the shop, knowing your coverage options can give you peace of mind—and keep more money in your pocket.

Key Takeaways

- Primary Coverage Included: Both Chase Sapphire Preferred and Reserve provide primary rental car insurance, meaning it pays first before your personal auto insurance.

- Eligible Vehicles Only: Coverage applies to most standard rental cars, but excludes luxury, exotic, or oversized vehicles like RVs and trucks.

- Must Decline CDW/LDW: To activate coverage, you must decline the rental company’s Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW).

- International Coverage Varies: The Chase Sapphire Reserve offers broader international protection, while the Preferred has limitations outside the U.S.

- Time Limits Apply: Coverage typically lasts up to 31 days per rental period—perfect for weekend getaways or extended road trips.

- Documentation Is Key: Keep all rental receipts, incident reports, and communication with the rental company in case you need to file a claim.

- Not a Replacement for Full Insurance: Rental car coverage doesn’t include liability or personal injury—so always check local laws when traveling abroad.

📑 Table of Contents

- How Does Chase Sapphire Rental Car Insurance Work?

- What Types of Vehicles Are Covered?

- Domestic vs. International Coverage: What’s the Difference?

- How to File a Claim with Chase Sapphire

- Common Mistakes to Avoid

- Should You Still Buy Rental Car Insurance?

- Final Thoughts: Make the Most of Your Sapphire Perk

How Does Chase Sapphire Rental Car Insurance Work?

Let’s start with the basics: both the Chase Sapphire Preferred and Chase Sapphire Reserve offer **primary rental car insurance** as a built-in benefit. That means if your rental car gets damaged or stolen, Chase will cover the cost—up to the actual cash value of the vehicle—before your personal auto insurance kicks in. This is a huge advantage because filing a claim with your own insurer could raise your premiums, even if the accident wasn’t your fault.

To activate this coverage, you must meet three key conditions:

1. **Pay for the entire rental with your eligible Chase Sapphire card** (or a combination of the card and rewards points).

2. **Decline the rental company’s Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW)** at the counter.

3. **Rent from a commercial rental agency** (like Hertz, Avis, Enterprise, etc.)—not private individuals or peer-to-peer platforms like Turo.

Once those boxes are checked, you’re protected against physical damage to the rental car due to collision or theft. Importantly, this is **not liability insurance**—it won’t cover injuries to people or damage to other vehicles. It also doesn’t cover personal belongings inside the car. Think of it as a safety net for the vehicle itself.

For example, imagine you’re driving through Colorado on a ski trip and accidentally back into a snowbank, denting the rear bumper. If you paid with your Chase Sapphire Reserve and declined the CDW, you can file a claim with Chase instead of paying the rental company’s repair fees out of pocket. Just remember to document everything: take photos, get a police report if needed, and keep all receipts.

What Types of Vehicles Are Covered?

Visual guide about Does Chase Sapphire Cover Rental Car Insurance

Image source: milepro.com

Not every vehicle you rent will qualify for Chase Sapphire’s insurance protection. The coverage is designed for everyday, standard passenger vehicles—think sedans, SUVs, minivans, and small trucks commonly used for personal travel.

Eligible Vehicles

Most mainstream rentals fall under this umbrella. Examples include:

– Toyota Camry or Honda Accord

– Ford Explorer or Jeep Grand Cherokee

– Nissan Rogue or Hyundai Tucson

– Standard pickup trucks (like a Ford F-150, as long as it’s not modified or used for commercial purposes)

These vehicles are typically rented for personal use and fall within the “normal” range of what you’d expect from a national rental chain.

Vehicles NOT Covered

Chase explicitly excludes certain categories of vehicles from coverage. These include:

– Luxury or exotic cars (e.g., Lamborghinis, Ferraris, high-end Mercedes-Benz models)

– Antique or classic cars

– Recreational vehicles (RVs), motorhomes, or camper vans

– Large trucks or vehicles designed for commercial use (e.g., box trucks, dump trucks)

– Vehicles with more than nine passenger seats (excluding minivans)

– Motorcycles, mopeds, or ATVs

So if you’re dreaming of cruising down the Pacific Coast Highway in a vintage Mustang or renting a massive RV for a national park tour, don’t assume your Chase Sapphire card has you covered. In these cases, you’ll likely need to purchase the rental company’s CDW or seek separate travel insurance.

It’s also worth noting that modifications matter. Even if you rent a standard SUV, if it’s been lifted, fitted with off-road tires, or used for towing heavy loads, Chase may deny your claim. Always err on the side of caution and assume anything outside the norm isn’t protected.

Domestic vs. International Coverage: What’s the Difference?

Visual guide about Does Chase Sapphire Cover Rental Car Insurance

Image source: milepro.com

One of the biggest questions travelers have is whether Chase Sapphire rental car insurance works abroad. The short answer: it depends on which card you have.

Chase Sapphire Preferred: Limited International Coverage

The Chase Sapphire Preferred offers **secondary coverage** outside the United States. That means if you’re renting a car in France, Japan, or Australia, your personal auto insurance (if you have international coverage) would pay first, and Chase would cover any remaining costs up to the card’s limit.

This is still helpful—but less convenient than primary coverage. You’ll need to file with your own insurer first, which can be a hassle, especially if you don’t have an international policy. Plus, some countries require mandatory liability insurance that your credit card won’t provide.

Chase Sapphire Reserve: Primary Coverage Almost Everywhere

The Chase Sapphire Reserve, on the other hand, provides **primary coverage worldwide**, including most international destinations. This is a major upgrade and one of the reasons the Reserve is so popular among frequent travelers.

Whether you’re exploring Tuscany in a Fiat 500 or navigating Tokyo’s streets in a compact Toyota, your Reserve card can cover damage or theft—again, as long as you pay with the card and decline the CDW.

However, there are exceptions. Some countries—like Italy, Ireland, and Israel—have strict local laws requiring all drivers to carry third-party liability insurance. In these places, even the Sapphire Reserve’s coverage may not fully protect you. Always check the rental company’s requirements and consider supplemental travel insurance if you’re unsure.

Pro tip: Before your trip, call Chase’s benefits administrator (the number is on the back of your card) and confirm coverage details for your destination. Rules can change, and it’s better to know ahead of time.

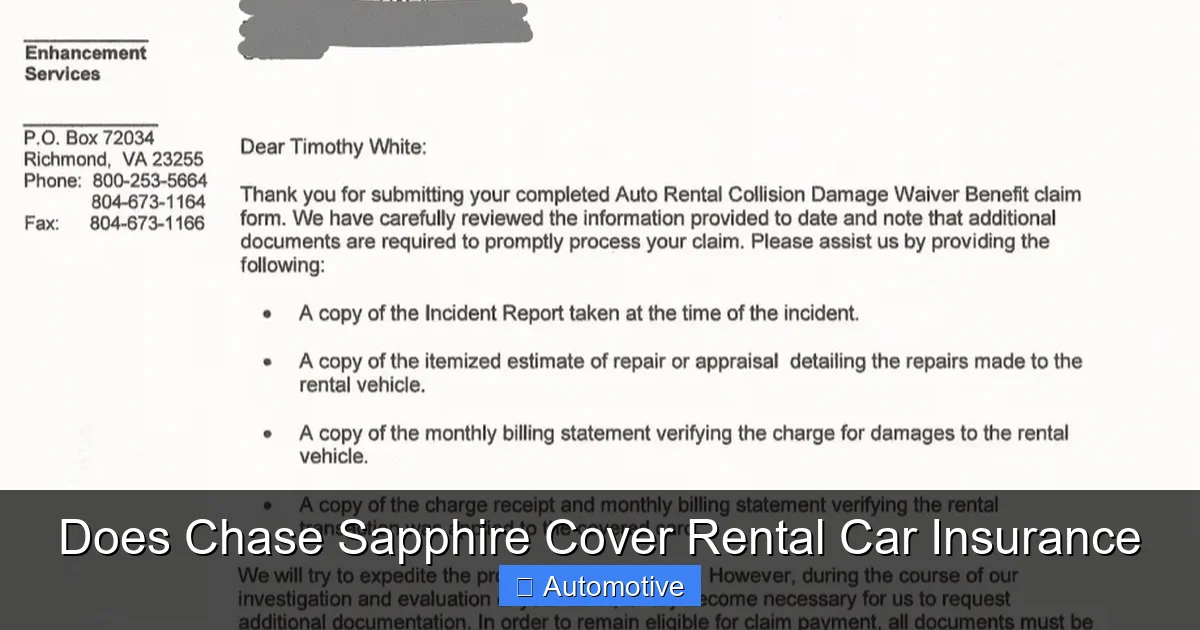

How to File a Claim with Chase Sapphire

Visual guide about Does Chase Sapphire Cover Rental Car Insurance

Image source: 10xtravel.com

Accidents happen—even to the most careful drivers. If your rental car is damaged or stolen, here’s how to file a claim with Chase:

Step 1: Report the Incident Immediately

Contact the rental company as soon as possible. Get a copy of the incident report, damage assessment, and any repair estimates. If there’s a police report (especially for theft or major accidents), obtain that too.

Step 2: Notify Chase Within 60 Days

You must report the claim to Chase’s benefits administrator within 60 days of the incident. You can do this online through the Chase Ultimate Rewards portal or by calling the number on your card.

Step 3: Submit Required Documentation

Chase will ask for:

– A copy of your rental agreement

– Proof of payment with your eligible Chase Sapphire card

– The rental company’s damage report or repair estimate

– Photos of the damage (if available)

– Police report (if applicable)

– Any correspondence with the rental agency

Step 4: Wait for Review and Reimbursement

Chase will review your claim and, if approved, reimburse you for covered expenses—usually via check or direct deposit. Processing can take several weeks, so patience is key.

Real-life example: Sarah rented a car in Miami using her Chase Sapphire Reserve. While parked, someone backed into her door, causing significant denting. She declined the CDW, took photos, got a police report, and filed her claim online. Within four weeks, Chase reimbursed her for the full repair cost—no impact on her personal insurance.

Common Mistakes to Avoid

Even with great coverage, it’s easy to make errors that could void your protection. Here are the top pitfalls to watch out for:

Paying Partially with Another Method

If you use cash, another credit card, or a discount code that reduces the amount charged to your Chase Sapphire, your coverage may be invalidated. The entire rental cost must be paid with the eligible card.

Accepting the Rental Company’s CDW

This is the #1 mistake travelers make. If you accept the CDW, you’re essentially waiving your right to use your credit card’s coverage. Always say “no” unless you’re driving a non-covered vehicle.

Renting from Non-Commercial Sources

Platforms like Turo, Getaround, or private owners don’t qualify. Only rentals from licensed, commercial agencies are eligible.

Ignoring Time Limits

Coverage lasts up to 31 days per rental. If you need a car longer than that (say, for a month-long assignment), you’ll need to re-rent or find alternative coverage.

Failing to Document Everything

No photos? No police report? No claim. Always document the condition of the car before and after your rental.

Should You Still Buy Rental Car Insurance?

Given all this, you might wonder: “Do I even need to buy extra coverage?” The answer depends on your situation.

If you’re using a standard car domestically with your Chase Sapphire Reserve, you’re likely well-protected—and can confidently decline the CDW. For international trips, especially in high-risk areas or countries with strict liability laws, consider supplemental travel insurance that includes rental car protection.

Also, remember: rental car insurance from Chase doesn’t cover:

– Personal injury or medical expenses

– Damage to other vehicles or property

– Lost wages or rental car downtime fees

– Personal belongings stolen from the car

If any of these matter to you—or if you’re traveling with family and want comprehensive protection—it may be worth investing in a travel insurance policy that bundles rental car coverage with medical, trip cancellation, and baggage protection.

Final Thoughts: Make the Most of Your Sapphire Perk

The Chase Sapphire rental car insurance benefit is one of the most underrated features of these premium cards. It’s not flashy like airport lounge access or bonus points on dining—but it can save you hundreds, even thousands, in unexpected repair costs.

By understanding what’s covered, how to activate the benefit, and what to avoid, you can travel with confidence knowing your card has your back. Just remember: pay with your card, decline the CDW, rent from a reputable agency, and document everything.

Whether you’re zipping through Napa Valley in a convertible or navigating the Alps in a compact hatchback, your Chase Sapphire isn’t just a payment tool—it’s a travel safety net. Use it wisely, and drive worry-free.

Frequently Asked Questions

Does the Chase Sapphire Preferred cover rental car insurance?

Yes, the Chase Sapphire Preferred offers primary rental car insurance in the U.S. and secondary coverage internationally when you pay for the rental with the card and decline the CDW.

Is rental car insurance included with the Chase Sapphire Reserve?

Absolutely. The Chase Sapphire Reserve provides primary rental car insurance both domestically and in most international locations, making it ideal for global travelers.

Can I use my Chase Sapphire card for Turo rentals?

No. Coverage only applies to rentals from commercial agencies like Hertz or Enterprise. Peer-to-peer platforms like Turo are not eligible.

What happens if I accept the rental company’s CDW?

If you accept the CDW or LDW, you forfeit your right to use your Chase Sapphire’s rental car insurance benefit. Always decline it to activate coverage.

Does Chase Sapphire cover luxury or exotic cars?

No. Vehicles classified as luxury, exotic, antique, or commercial (like RVs or large trucks) are excluded from coverage under both Sapphire cards.

How long does rental car coverage last with Chase Sapphire?

Coverage applies for up to 31 consecutive days per rental period. For longer rentals, you’ll need to re-rent or seek alternative insurance.