Can I Keep My Car If I File Chapter 13?

Yes, you can usually keep your car if you file Chapter 13 bankruptcy—as long as you stay current on payments and follow the court-approved plan. Unlike Chapter 7, Chapter 13 lets you reorganize debts and keep assets, including your vehicle, while catching up on missed payments over time.

Key Takeaways

- You can keep your car in Chapter 13: The bankruptcy allows you to retain your vehicle as long as you continue making payments and comply with the repayment plan.

- Missed payments can be caught up: Chapter 13 lets you spread overdue auto loan payments over 3–5 years, helping you avoid repossession.

- Equity matters: If your car has significant equity, the trustee may require you to pay that value back to unsecured creditors through your plan.

- Reaffirmation isn’t required: Unlike Chapter 7, you don’t need to sign a reaffirmation agreement to keep your car in Chapter 13.

- Stay insured: Keeping full coverage insurance is mandatory to protect the lender’s interest and your ability to keep the vehicle.

- Late payments risk repossession: Falling behind again after filing can lead to the lender repossessing the car, even during bankruptcy.

- Consult a bankruptcy attorney: Legal guidance ensures you understand your rights and make the best decisions for your financial situation.

📑 Table of Contents

- Can I Keep My Car If I File Chapter 13?

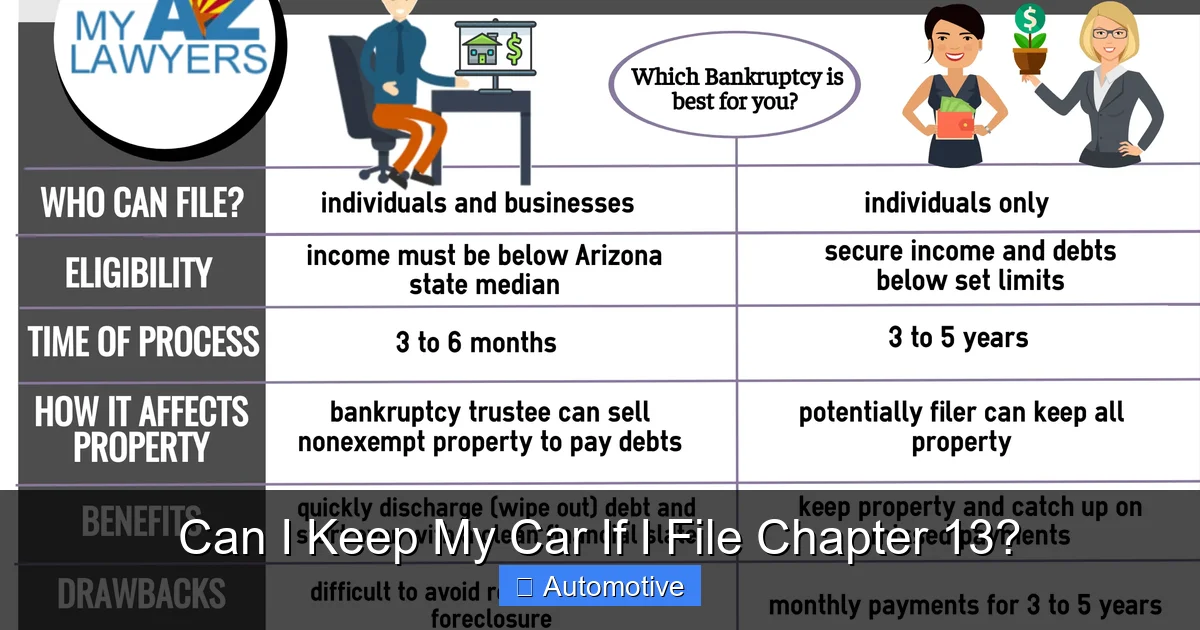

- How Chapter 13 Bankruptcy Works

- Keeping Your Car in Chapter 13: The Basics

- Reaffirmation vs. Retention: What’s the Difference?

- Insurance Requirements and Protecting Your Investment

- Common Pitfalls and How to Avoid Them

- Real-Life Example: Maria’s Story

- Conclusion: Yes, You Can Keep Your Car

Can I Keep My Car If I File Chapter 13?

Filing for bankruptcy is never an easy decision—but when you’re drowning in debt and facing the possibility of losing your car, it can feel like your only lifeline. If you’re considering Chapter 13 bankruptcy, one of your biggest concerns is likely: *Can I keep my car?* The good news is, in most cases, the answer is yes.

Chapter 13 bankruptcy, often called a “wage earner’s plan,” is designed to help individuals with regular income reorganize their debts and repay them over time—typically three to five years. Unlike Chapter 7, which liquidates assets to pay creditors, Chapter 13 focuses on restructuring what you owe while allowing you to keep your property, including your vehicle. This makes it a powerful tool for people who rely on their car for work, school, or family responsibilities.

But keeping your car isn’t automatic. It depends on several factors: the amount you owe on the loan, the value of the car, your payment history, and whether you can afford the monthly payments going forward. The key is understanding how Chapter 13 works and what steps you need to take to protect your wheels.

In this guide, we’ll walk you through everything you need to know about keeping your car during Chapter 13 bankruptcy—from how the repayment plan affects your auto loan to what happens if you’re behind on payments. We’ll also cover common pitfalls, practical tips, and real-life examples to help you make informed decisions. Whether you’re just exploring your options or already deep in the process, this article will give you the clarity and confidence you need.

How Chapter 13 Bankruptcy Works

Visual guide about Can I Keep My Car If I File Chapter 13?

Image source: horwitzlawsite.com

Before diving into how Chapter 13 affects your car, it’s important to understand the basics of this type of bankruptcy. Chapter 13 is a court-approved repayment plan that allows you to pay back a portion of your debts over time—usually 36 to 60 months. It’s ideal for people who have a steady income but are struggling with overwhelming debt, especially if they’re at risk of losing valuable assets like a home or car.

When you file Chapter 13, you submit a detailed repayment plan to the bankruptcy court. This plan outlines how you’ll pay your creditors, including priority debts (like taxes or child support), secured debts (like your mortgage or car loan), and unsecured debts (like credit cards or medical bills). The court reviews your income, expenses, and debt obligations to determine how much you can reasonably afford to pay each month.

One of the biggest advantages of Chapter 13 is the automatic stay. As soon as you file, creditors must stop all collection efforts—including calls, lawsuits, wage garnishments, and repossession attempts. This gives you immediate relief and time to get your finances back on track.

The Role of the Bankruptcy Trustee

A key player in your Chapter 13 case is the bankruptcy trustee. This is a court-appointed individual who oversees your case, reviews your repayment plan, collects your monthly payments, and distributes them to your creditors. The trustee ensures that your plan is fair and feasible and that you’re complying with all court requirements.

You’ll make one monthly payment to the trustee, who then pays your creditors according to the plan. For example, if you’re behind on your car payments, the trustee may use part of your payment to catch up on those arrears. Meanwhile, your regular car payment continues to go to the lender directly, unless the lender agrees to have it included in the plan.

Duration of the Repayment Plan

The length of your Chapter 13 plan depends on your income compared to your state’s median income. If your income is below the median, you’ll likely have a 36-month plan. If it’s above, the plan usually lasts 60 months. During this time, you must make all required payments on time and comply with court orders, such as attending financial counseling and providing tax returns.

Once you complete the plan, any remaining unsecured debts (like credit card balances) may be discharged—meaning you’re no longer legally obligated to pay them. However, secured debts like your car loan must be paid in full to keep the vehicle.

Keeping Your Car in Chapter 13: The Basics

Visual guide about Can I Keep My Car If I File Chapter 13?

Image source: myazlawyers.com

Now, let’s get to the heart of the matter: can you keep your car if you file Chapter 13? In most cases, the answer is yes—but there are important conditions.

The primary rule is simple: as long as you continue making your car payments and follow the terms of your bankruptcy plan, you can keep your vehicle. Chapter 13 doesn’t require you to surrender your car, unlike Chapter 7, where non-exempt assets may be sold.

But there are nuances. The way your car loan is treated depends on whether you’re current on payments, how much you owe, and the value of the car. Let’s break it down.

Current on Payments? You’re in Good Shape

If you’re up to date on your car payments when you file Chapter 13, keeping your car is usually straightforward. You’ll continue making your regular monthly payments directly to the lender, just as you did before filing. The bankruptcy doesn’t change your loan terms—you still owe the same amount at the same interest rate.

The automatic stay protects you from repossession, so even if the lender was threatening to take your car, they must stop. As long as you keep paying on time, you’ll retain ownership and drive away worry-free.

Behind on Payments? You Can Catch Up

One of the biggest benefits of Chapter 13 is the ability to catch up on missed payments. If you’re behind on your car loan, the bankruptcy allows you to include those arrears in your repayment plan. Instead of paying a large lump sum, you spread the overdue amount over 3–5 years.

For example, let’s say you’re $3,000 behind on your car payments. Your Chapter 13 plan might require you to pay $100 per month toward that arrearage, while continuing your regular $300 monthly payment to the lender. Over 30 months, you’ll catch up and stay current.

This is a huge advantage over Chapter 7, where you’d have to pay the full arrears immediately or risk losing the car. With Chapter 13, you get breathing room to get back on track.

What If the Car Is Worth Less Than You Owe?

If your car is “underwater”—meaning you owe more than it’s worth—you may still be able to keep it. However, the bankruptcy trustee will look at the equity in the vehicle. Equity is the difference between the car’s current market value and what you owe.

If there’s little or no equity, you’re unlikely to face any issues. But if the car has significant equity (say, you owe $10,000 but it’s worth $15,000), the trustee may require you to pay that $5,000 in equity back to unsecured creditors through your plan. This is to ensure that creditors receive fair treatment.

In some cases, you may be able to “cram down” the loan if the car was purchased more than 910 days (about 2.5 years) before filing. This means you can reduce the loan balance to the car’s current value and pay interest only on that amount. However, this only applies to certain types of loans and requires court approval.

Reaffirmation vs. Retention: What’s the Difference?

Visual guide about Can I Keep My Car If I File Chapter 13?

Image source: brunerwright.com

A common point of confusion is whether you need to sign a reaffirmation agreement to keep your car in Chapter 13. The short answer: no.

In Chapter 7 bankruptcy, you typically sign a reaffirmation agreement to keep a secured asset like a car. This legally reaffirms your debt and allows you to retain the vehicle, but it also means you’re personally liable if you default later.

Chapter 13 works differently. Because you’re already committing to repay your debts through the court-approved plan, reaffirmation isn’t required. Instead, you “retain” the car by continuing to make payments and complying with the plan.

Why Reaffirmation Isn’t Needed in Chapter 13

The logic is simple: in Chapter 13, you’re not discharging your secured debts immediately. You’re paying them off over time, so there’s no need to reaffirm the debt. The lender still has a security interest in the car, and you’re obligated to pay—but the bankruptcy court oversees the process.

This is a major advantage. If you later run into financial trouble and can’t make payments, you may be able to modify your plan or convert to Chapter 7, rather than facing immediate repossession.

What Happens If You Stop Paying?

Even though reaffirmation isn’t required, falling behind on payments can still lead to repossession. If you miss payments after filing, the lender can ask the court to lift the automatic stay and repossess the car. The bankruptcy doesn’t give you a free pass—it just gives you a structured way to catch up.

To avoid this, it’s crucial to budget carefully and prioritize your car payment. If you’re struggling, talk to your attorney or the trustee about modifying your plan.

Insurance Requirements and Protecting Your Investment

Keeping your car in Chapter 13 isn’t just about making payments—it’s also about protecting the asset. One of the most important requirements is maintaining full coverage auto insurance.

Why Insurance Is Mandatory

Your lender has a financial interest in the car, so they require insurance to protect their investment. If the car is damaged or totaled, the insurance payout helps repay the loan. Without coverage, the lender could lose money—and they won’t take that risk.

In Chapter 13, the court and trustee also expect you to maintain insurance. Failing to do so can be seen as a violation of your plan and may lead to dismissal of your case or repossession.

What Type of Coverage Do You Need?

You’ll need at least comprehensive and collision coverage, in addition to liability insurance. This protects against theft, vandalism, accidents, and natural disasters. The coverage amount should be sufficient to cover the car’s value or the loan balance, whichever is higher.

Some lenders may require a specific deductible (like $500) or additional coverage like gap insurance, especially if you’re underwater on the loan. Be sure to check your loan agreement and communicate with your lender.

Tips for Managing Insurance Costs

Insurance can be expensive, especially during bankruptcy when budgets are tight. Here are a few tips to keep costs down:

– Shop around for quotes from multiple insurers.

– Ask about discounts for safe driving, bundling policies, or paying annually.

– Consider raising your deductible (but only if you can afford it).

– Maintain a clean driving record to avoid rate increases.

Remember, skipping insurance to save money is never worth the risk. A single accident or theft could cost far more than your premiums.

Common Pitfalls and How to Avoid Them

While Chapter 13 can be a lifeline, it’s not without risks. Here are some common mistakes people make when trying to keep their car—and how to avoid them.

Falling Behind Again After Filing

One of the biggest mistakes is assuming bankruptcy gives you a permanent reprieve. It doesn’t. If you stop making payments after filing, the lender can still repossess your car.

To avoid this, create a realistic budget that includes your car payment, insurance, and any arrearage payments. Use automatic payments if possible, and communicate with your lender if you’re struggling.

Ignoring Communication from the Lender or Trustee

During bankruptcy, you’ll receive regular statements and notices from your lender and the trustee. Ignoring these can lead to missed deadlines, penalties, or even dismissal of your case.

Set up a system to track all correspondence. Open every letter, respond promptly, and keep copies for your records.

Not Updating the Court About Changes

If your income, expenses, or living situation change, you must notify the trustee. For example, if you get a raise, lose your job, or move, the court may need to adjust your plan.

Failing to report changes can result in penalties or loss of protection under the bankruptcy.

Trying to Handle It Alone

Bankruptcy law is complex, and mistakes can be costly. While it’s possible to file without an attorney, it’s not recommended—especially when your car is on the line.

A qualified bankruptcy attorney can help you understand your rights, negotiate with lenders, and ensure your plan is approved. Many offer free consultations, so there’s no reason not to get professional advice.

Real-Life Example: Maria’s Story

Let’s look at a real-world example to see how this works in practice.

Maria, a single mom from Ohio, was struggling to make ends meet after her hours at work were cut. She was three months behind on her $350 monthly car payment and feared repossession. Her car was essential for getting her kids to school and driving to her job.

After consulting a bankruptcy attorney, Maria filed Chapter 13. Her repayment plan included $1,050 in arrears (three missed payments) to be paid over 36 months—about $29 per month. She continued making her regular $350 payment directly to the lender.

Maria also maintained full coverage insurance and attended required financial counseling. After 36 months of on-time payments, she completed her plan, caught up on her loan, and kept her car. Today, she’s debt-free and driving confidently.

Maria’s story shows that with the right plan and discipline, keeping your car in Chapter 13 is not only possible—it’s achievable.

Conclusion: Yes, You Can Keep Your Car

So, can you keep your car if you file Chapter 13? The answer is a resounding yes—for most people, under the right conditions.

Chapter 13 bankruptcy offers a structured, court-supervised way to reorganize your debts and keep your vehicle. Whether you’re current on payments or need to catch up, the system is designed to help you succeed. You don’t need to sign a reaffirmation agreement, and you can include arrears in your plan to avoid repossession.

But success requires responsibility. You must make payments on time, maintain insurance, and stay in communication with your lender and trustee. Falling behind or ignoring requirements can put your car at risk.

If you’re considering Chapter 13, don’t go it alone. Consult a qualified bankruptcy attorney to review your situation, explore your options, and create a plan that works for you. With the right guidance and commitment, you can keep your car, regain control of your finances, and move toward a brighter future.

Your car is more than just a vehicle—it’s your freedom, your connection to work and family, and a symbol of stability. Chapter 13 can help you protect it.

Frequently Asked Questions

Can I keep my car if I file Chapter 13 bankruptcy?

Yes, in most cases you can keep your car when filing Chapter 13. As long as you continue making payments and follow the court-approved repayment plan, you can retain ownership of your vehicle.

Do I need to sign a reaffirmation agreement to keep my car in Chapter 13?

No, reaffirmation agreements are not required in Chapter 13. Unlike Chapter 7, you keep your car by staying current on payments and complying with the repayment plan.

What happens if I’m behind on my car payments when I file?

You can include missed payments in your Chapter 13 plan and catch up over 3–5 years. This prevents repossession and gives you time to get back on track.

Will the bankruptcy trustee take my car if it has equity?

If your car has significant equity, the trustee may require you to pay that amount to unsecured creditors through your plan. However, you can still keep the vehicle.

Can my lender repossess my car during Chapter 13?

Only if you stop making payments. The automatic stay stops repossession when you file, but falling behind again can lead to the lender requesting court permission to repossess.

Do I need full coverage insurance during Chapter 13?

Yes, maintaining full coverage insurance is required to protect the lender’s interest and comply with bankruptcy court rules. Skipping insurance can risk your case and your car.