What Is the Lowest Credit Score to Buy a Car

There’s no universal “lowest credit score to buy a car,” but most lenders consider scores below 580 as high-risk. While it’s possible to get approved with poor credit, expect higher interest rates and stricter terms. With the right strategy, even borrowers with bad credit can drive off in a reliable vehicle.

Key Takeaways

- Minimum credit scores vary by lender: Some accept scores as low as 500, while others require 600 or higher for auto loans.

- Subprime lenders specialize in bad credit: These lenders work with borrowers who have scores below 580 but often charge higher interest rates.

- Down payments help offset low scores: A larger down payment reduces risk for lenders and improves approval chances.

- Co-signers can boost approval odds: Adding a co-signer with good credit increases your chances of qualifying for better loan terms.

- Interest rates rise sharply with lower scores: Borrowers with scores under 580 may face APRs over 15%, significantly increasing total loan costs.

- Credit unions offer more flexibility: Local credit unions often have more lenient requirements than big banks or dealerships.

- Improving your score before buying saves money: Even a small score increase can qualify you for lower rates and save thousands over the loan term.

📑 Table of Contents

Understanding Credit Scores and Car Buying

Buying a car is one of the biggest financial decisions many people make—right after purchasing a home. But unlike houses, cars lose value the moment you drive them off the lot. That’s why lenders are especially cautious when approving auto loans, especially for buyers with less-than-perfect credit.

Your credit score plays a major role in whether you’ll get approved for a car loan and what kind of interest rate you’ll pay. But here’s the good news: there’s no single “magic number” that determines whether you can buy a car. The lowest credit score to buy a car depends on the lender, the type of financing, and your overall financial picture.

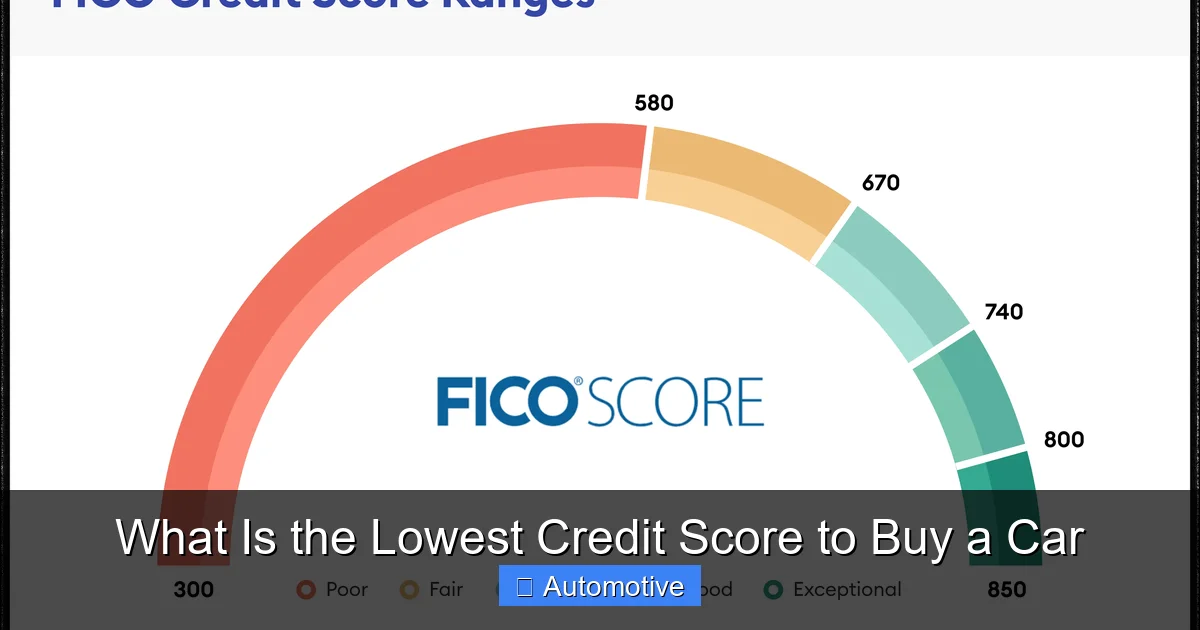

Most credit scoring models, like FICO and VantageScore, range from 300 to 850. Generally, scores fall into these categories:

– Excellent: 750–850

– Good: 660–749

– Fair: 600–659

– Poor: 500–599

– Bad: Below 500

While a higher score opens doors to better loan terms, even people with scores in the 500s or lower can still buy a car—they just need to know where to look and how to prepare.

Why Credit Scores Matter for Auto Loans

Lenders use your credit score to assess risk. A low score signals that you’ve had trouble managing debt in the past—maybe you missed payments, defaulted on a loan, or maxed out credit cards. Because of this history, lenders see you as a higher-risk borrower.

Higher risk means higher costs. If you have a low credit score, lenders may:

– Charge a higher interest rate

– Require a larger down payment

– Limit the loan amount

– Shorten the repayment term

For example, someone with a 720 credit score might qualify for a 5% APR on a $25,000 loan, while someone with a 550 score could be offered 18% APR for the same loan. Over a 60-month term, that difference adds up to over $7,000 in extra interest.

But credit scores aren’t the only factor. Lenders also look at your income, employment history, debt-to-income ratio, and down payment amount. So even with a low score, strong financial habits can improve your chances.

What Is the Lowest Credit Score to Buy a Car?

Visual guide about What Is the Lowest Credit Score to Buy a Car

Image source: carsmaster.com

So, what’s the actual lowest credit score to buy a car? The answer isn’t straightforward because it depends on the lender and the type of financing you’re seeking.

Most traditional banks and credit unions prefer borrowers with scores of 600 or higher. However, many subprime lenders—specialized auto finance companies—work with borrowers who have scores as low as 500 or even 400 in rare cases.

Here’s a breakdown of typical credit score requirements by lender type:

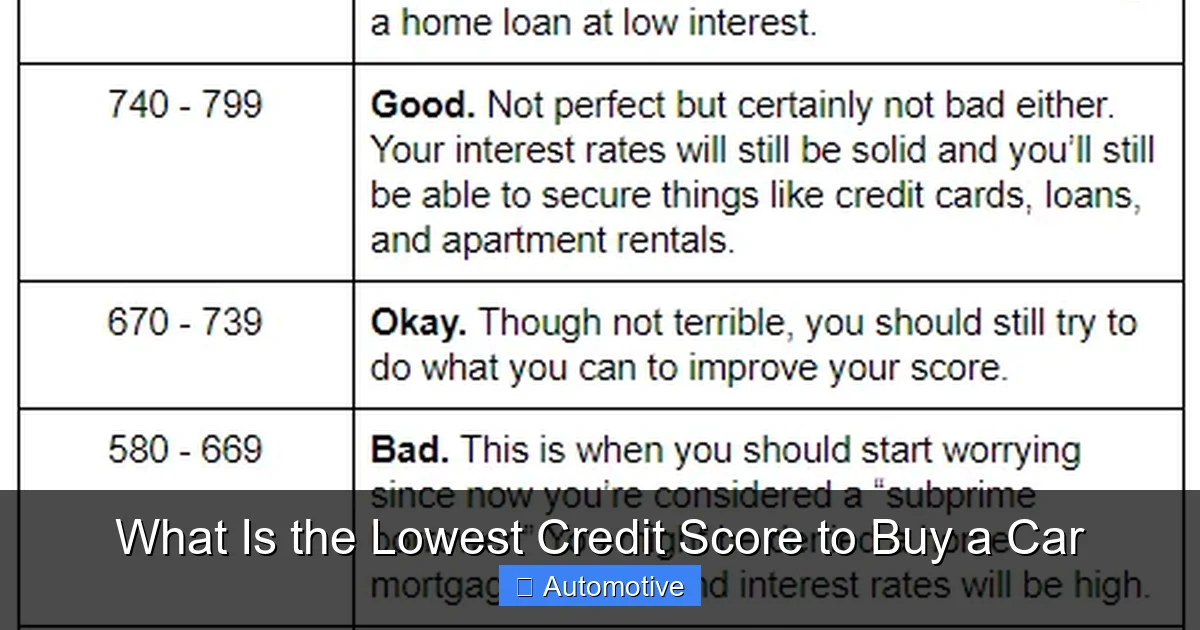

– **Prime lenders (banks, credit unions):** 660+

– **Near-prime lenders:** 600–659

– **Subprime lenders:** 500–599

– **Deep subprime lenders:** Below 500

That means if your score is 580, you’re likely to qualify with a subprime lender, but not with a major bank. If your score dips below 500, your options shrink, but they don’t disappear.

Real-World Examples of Approval with Low Scores

Let’s say Maria has a credit score of 520. She’s had a few late payments and a charged-off credit card from two years ago. She wants to buy a used car for $15,000.

Maria applies at her local credit union first. They decline her application due to her low score. Undeterred, she researches subprime auto lenders and finds one that specializes in bad credit loans. They approve her for a $15,000 loan at 19.9% APR with a $2,000 down payment.

Now consider James, who has a 480 credit score. He’s been rebuilding his credit after bankruptcy. He knows his options are limited, so he saves $3,000 for a down payment and finds a buy-here-pay-here dealership. These dealerships finance the car directly and often don’t check credit scores. James gets approved for a $12,000 used car with weekly payments and a 22% interest rate.

Both Maria and James bought cars with low credit scores—but their experiences and costs were very different. Maria’s higher score and down payment helped her secure slightly better terms, while James paid more due to his lower score and the dealership’s high-risk model.

Lender Types and Their Credit Requirements

Visual guide about What Is the Lowest Credit Score to Buy a Car

Image source: thumbor.forbes.com

Not all lenders are created equal when it comes to credit score requirements. Understanding the different types of lenders can help you find the best fit for your financial situation.

Traditional Banks and Credit Unions

Banks and credit unions are often the first stop for car buyers. They typically offer the lowest interest rates and most favorable terms—but they also have stricter credit requirements.

Most banks want to see a credit score of at least 660. Credit unions, which are member-owned and often more community-focused, may be more flexible. Some credit unions accept scores as low as 600, especially if you have a strong income or existing relationship with the institution.

For example, Navy Federal Credit Union, which serves military members and their families, has been known to approve auto loans for borrowers with scores in the low 600s. Similarly, local credit unions might consider your full financial profile, not just your credit score.

Subprime Auto Lenders

Subprime lenders specialize in working with borrowers who have poor or no credit. These lenders understand that life happens—job loss, medical bills, divorce—and they’re willing to take on higher-risk customers.

Companies like Santander Consumer USA, Westlake Financial, and Credit Acceptance are well-known subprime lenders. They often approve borrowers with scores as low as 500, though interest rates can be steep.

These lenders may also require:

– Proof of income (pay stubs or tax returns)

– A down payment (usually 10–20% of the car’s value)

– A co-signer (someone with better credit who agrees to repay the loan if you can’t)

While subprime loans make car ownership possible for many, they come with risks. High interest rates mean you’ll pay significantly more over time. And if you miss payments, your credit could take another hit.

Buy-Here-Pay-Here Dealerships

Buy-here-pay-here (BHPH) dealerships are a last-resort option for buyers with very low credit scores. These dealerships finance the car directly—no third-party lender involved—and often don’t check your credit at all.

Instead, they focus on your income and employment. You’ll typically need to show proof of steady income and may be required to make weekly or biweekly payments in person.

The downside? BHPH cars are often older, higher-mileage models with limited warranties. Interest rates can exceed 20%, and repossession is common if you miss a payment.

Still, for someone with a 450 credit score and no other options, a BHPH dealership might be the only way to get behind the wheel.

Online Lenders and Brokers

Online lenders like LightStream, Upstart, and myAutoloan offer a middle ground. Some accept lower credit scores, especially if you have a strong income or collateral.

Brokers connect you with multiple lenders at once, increasing your chances of approval. They can be especially helpful if you’re unsure where to start or have been turned down elsewhere.

Just be cautious of predatory lenders. Always read the fine print, check for prepayment penalties, and verify the lender’s reputation through the Better Business Bureau or Consumer Financial Protection Bureau.

How to Improve Your Chances with a Low Credit Score

Visual guide about What Is the Lowest Credit Score to Buy a Car

Image source: i.pinimg.com

Even if your credit score is low, you’re not out of options. With the right strategy, you can improve your chances of getting approved—and maybe even secure better loan terms.

Save for a Larger Down Payment

A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. It also shows financial responsibility.

For example, putting down $3,000 on a $15,000 car means you only need a $12,000 loan. That’s easier to approve and results in lower monthly payments.

Aim for at least 10–20% down. If you can’t afford that much, even $1,000 can make a difference.

Consider a Co-Signer

A co-signer is someone with good credit who agrees to repay the loan if you can’t. This gives lenders extra confidence and can help you qualify for lower interest rates.

But be careful: if you miss payments, your co-signer’s credit will also be damaged. Only ask someone you trust—and make sure they understand the risks.

Choose a More Affordable Car

Lenders are more likely to approve smaller loan amounts. Instead of aiming for a $30,000 SUV, consider a reliable used car under $15,000.

Look for models known for longevity and low maintenance costs, like a Toyota Corolla, Honda Civic, or Hyundai Elantra. These cars hold their value and are cheaper to insure and repair.

Get Pre-Approved

Before visiting dealerships, get pre-approved for a loan. This gives you a clear budget and strengthens your negotiating power.

You can apply with multiple lenders to compare offers. Just be aware that too many hard inquiries in a short time can temporarily lower your credit score.

Rebuild Your Credit Before Buying

If you have time, work on improving your credit score before applying for a car loan. Even a 50-point increase can make a big difference.

Ways to boost your score:

– Pay all bills on time

– Reduce credit card balances

– Avoid opening new credit accounts

– Dispute errors on your credit report

Consider using a secured credit card or credit-builder loan to establish positive payment history.

The True Cost of Buying a Car with Bad Credit

While it’s possible to buy a car with a low credit score, it’s important to understand the financial impact.

Higher Interest Rates

Interest rates for bad credit auto loans can be shockingly high. While prime borrowers might pay 4–6% APR, subprime borrowers often face rates of 15–25%.

Let’s compare two $20,000 loans over 60 months:

– At 5% APR: Monthly payment = $377 | Total interest = $2,633

– At 20% APR: Monthly payment = $529 | Total interest = $11,740

That’s over $9,000 more in interest—just because of the credit score difference.

Longer Loan Terms

To keep monthly payments manageable, lenders may extend the loan term to 72 or 84 months. While this lowers your payment, it increases total interest paid and puts you at risk of being “upside down” (owing more than the car is worth).

Additional Fees and Requirements

Some subprime lenders charge origination fees, documentation fees, or require GPS tracking devices that disable the car if you miss a payment. These add-ons increase the overall cost.

Impact on Insurance

Insurance companies also consider credit when setting premiums. Drivers with poor credit often pay higher rates, adding to the monthly cost of car ownership.

Tips for Success When Buying with Low Credit

Buying a car with bad credit doesn’t have to be a nightmare. With preparation and smart choices, you can drive away with a reliable vehicle and a manageable payment.

Shop Around

Don’t settle for the first offer. Compare rates from banks, credit unions, online lenders, and dealerships. Use pre-qualification tools that don’t affect your credit score.

Read the Fine Print

Make sure you understand all terms: interest rate, loan term, fees, prepayment penalties, and repossession policies. Ask questions if anything is unclear.

Avoid Add-Ons You Don’t Need

Dealerships often push extended warranties, gap insurance, and maintenance plans. While some are useful, others are overpriced. Only buy what you truly need.

Make Payments on Time

Once you have the loan, prioritize on-time payments. This helps rebuild your credit and avoids late fees or repossession.

Refinance Later

If you make consistent payments and improve your credit, you may qualify to refinance your loan at a lower rate in 12–24 months. This can save you hundreds or thousands in interest.

Conclusion

So, what is the lowest credit score to buy a car? There’s no single answer, but most lenders consider scores below 580 as high-risk. While it’s possible to get approved with a score in the 500s or even lower, your options will be limited, and your costs will be higher.

The key is to understand your situation, explore all lender types, and take steps to improve your financial profile. Whether you go with a subprime lender, a credit union, or a buy-here-pay-here dealership, make sure the loan fits your budget and helps you move forward—not backward.

Remember, a car loan isn’t just about getting from point A to point B. It’s also an opportunity to rebuild your credit and set yourself up for better financial opportunities in the future. With patience, planning, and persistence, you can drive off in a car that meets your needs—and your budget.

Frequently Asked Questions

Can I buy a car with a credit score of 500?

Yes, it’s possible to buy a car with a 500 credit score, especially through subprime lenders or buy-here-pay-here dealerships. However, expect higher interest rates and stricter terms.

What is the minimum credit score for a car loan at a bank?

Most banks require a credit score of at least 660 for auto loan approval. Some may accept scores as low as 600, but rates will be higher.

Will a larger down payment help with a low credit score?

Yes, a larger down payment reduces the loan amount and shows financial responsibility, which can improve your chances of approval and lower your interest rate.

Can I get a car loan with no credit history?

Yes, but it’s more difficult. Lenders may require a co-signer, larger down payment, or proof of steady income. Some online lenders specialize in no-credit borrowers.

How can I improve my credit score before buying a car?

Pay bills on time, reduce credit card balances, avoid new credit applications, and check your credit report for errors. Even small improvements can help.

Is it better to finance through a dealership or a bank?

It depends. Banks and credit unions often offer lower rates, but dealerships may have special promotions. Compare offers from both to find the best deal.