What Is the Average Monthly Payment for a Toyota Highlander

The average monthly payment for a Toyota Highlander typically ranges from $450 to $750 for a new 2024 model, depending heavily on trim level, down payment, loan term, and your credit score. Choosing a base L or LE trim with a substantial down payment and good credit will yield the lowest payment, while a top Platinum trim with minimal down will be at the high end. Leasing can offer lower monthly payments than buying, but you build no equity. Understanding these variables and shopping around for financing are crucial steps to securing a manageable payment.

Key Takeaways

- Payment Range is Wide: Expect a new 2024 Highlander payment between $450-$750/month. This variance is due to trim choices, financing terms, and individual financial profiles.

- Your Credit Score is King: It’s the single biggest factor influencing your interest rate. A score of 720+ can save you thousands versus a score of 600.

- Down Payment Directly Lowers Payment: Every $1,000 you put down typically reduces your monthly payment by $15-$25 on a 60-month loan. It also improves your loan-to-value ratio.

- Trim Level Drives Base Price: The difference between a base L and a Platinum model is over $15,000, which translates to a $250+ monthly payment difference on the same loan terms.

- Lease vs. Buy Has Different Math: Leases offer lower monthly payments because you pay for depreciation only, but you have no asset at the end. Buying builds equity but has higher payments.

- Shop for Financing Separately: Getting pre-approved from your bank or credit union before going to the dealer gives you negotiating power and often a better rate than dealer financing.

- Total Cost Matters More: Focus on the total amount paid over the loan/lease term (price + interest + fees) rather than just the monthly payment to avoid long-term overpayment.

[FEATURED_IMAGE_PLACEHOLDER]

📑 Table of Contents

- Understanding the Toyota Highlander’s Appeal

- The Building Blocks of a Car Payment

- Key Factors That Influence Your Monthly Highlander Payment

- Average Monthly Payment by Trim: Real-World 2024 Examples

- Leasing vs. Buying: Which Has a Lower Monthly Payment?

- Practical Strategies to Lower Your Toyota Highlander Payment

- The Total Cost of Ownership: It’s Not Just the Monthly Payment

- Conclusion: Your Payment, Your Power

Understanding the Toyota Highlander’s Appeal

So, you’re eyeing a Toyota Highlander. Excellent choice. It’s consistently one of America’s best-selling three-row SUVs for good reason. It blends Toyota’s reputation for reliability with a spacious, comfortable cabin, strong V6 power, and a suite of standard safety features. For families and adventure-seekers alike, it’s a practical, capable, and trustworthy vehicle. But before you fall in love with the leather seats or the panoramic moonroof, we need to talk numbers. The big question on everyone’s mind is: “What is the average monthly payment for a Toyota Highlander?”

This isn’t a question with a single answer. It’s a question with a range of answers. The payment you see advertised or that your friend pays is a unique combination of the vehicle’s price, your financial health, and the terms you agree to. Our goal here is to pull back the curtain on that monthly payment. We’ll break down the real averages for 2024 models, walk through every single factor that pushes that number up or down, compare buying versus leasing, and give you actionable strategies to get the best possible deal. By the end, you won’t just know an average number; you’ll know exactly how to calculate your own potential payment and how to make it smaller.

The Building Blocks of a Car Payment

Before we dive into Highlander-specific numbers, let’s quickly review what a car payment actually is. It’s not magic. It’s a simple formula: Principal + Interest + Term.

Visual guide about What Is the Average Monthly Payment for a Toyota Highlander

Image source: evto.ca

- Principal: This is the amount you finance. It’s the vehicle’s final selling price (after any discounts or negotiations) minus your down payment or trade-in equity.

- Interest: This is the cost of borrowing money, expressed as an Annual Percentage Rate (APR). Your credit score primarily determines this rate. A 5% APR on a $30,000 loan costs you far less in total interest than a 10% APR on the same loan.

- Term: This is the length of your loan, usually 24, 36, 48, 60, or even 72 months. A longer term lowers your monthly payment but dramatically increases the total interest you pay.

For a lease, the payment is calculated based on the vehicle’s depreciation during the lease term (the difference between its initial value and its predicted residual value at lease-end), plus finance charges and fees. This is why lease payments are often lower than purchase payments for the same vehicle.

Key Factors That Influence Your Monthly Highlander Payment

Now, let’s apply these building blocks to the Highlander. Your personal payment is a fingerprint—unique to your situation. Here are the seven most powerful levers that determine your final number.

Visual guide about What Is the Average Monthly Payment for a Toyota Highlander

Image source: di-sitebuilder-assets.dealerinspire.com

1. The Trim Level You Choose (The Biggest Driver)

The Toyota Highlander comes in several trims, each with a significant price jump. The 2024 model starts with the L, then moves to LE, XLE, Limited, and the top-tier Platinum. There’s also a Hybrid line (LE and Limited) that commands a premium over the gas models. Here are the approximate MSRPs for the 2024 gas models before any incentives or negotiations:

- Toyota Highlander L: ~$37,000

- Toyota Highlander LE: ~$40,500

- Toyota Highlander XLE: ~$44,500

- Toyota Highlander Limited: ~$48,500

- Toyota Highlander Platinum: ~$52,500

As you can see, going from the base L to the Platinum adds over $15,000 to the sticker price. Financing that extra $15,000 over 60 months at 5% interest adds roughly $283 to your monthly payment. That’s the single largest controllable factor. Know what features you truly need versus what you just want.

2. Your Credit Score (The Interest Rate King)

This is non-negotiable and profoundly impactful. Lenders use your credit score to assign risk. A higher score means you’re a safer bet, so they offer a lower APR. For a new vehicle like the Highlander, here’s a realistic APR breakdown as of early 2024:

- Excellent (740+): 3.9% – 5.5% APR

- Good (700-739): 5.5% – 7.9% APR

- Fair (650-699): 8.9% – 12.9% APR

- Poor (649 and below): 13%+ APR (often requiring a co-signer or special financing)

Let’s compare the total interest on a $35,000 loan for 60 months. At 4.5%, you pay about $3,500 in total interest. At 10%, you pay over $9,500. That’s a $6,000 difference! Your credit score is the most powerful tool to control this cost. If your score is low, consider delaying your purchase to improve it first.

3. Down Payment or Trade-In Equity

How much cash you put down or how much your current vehicle is worth (if trading in) directly reduces the principal you need to finance. A common recommendation is to put down at least 10-20% of the vehicle’s price. For a $40,000 Highlander, that’s $4,000-$8,000. A larger down payment not only lowers your monthly payment but also:

- Helps you avoid being “upside down” (owing more than the car is worth) in the first few years.

- Can help you qualify for a better interest rate, as you’re borrowing less.

- May allow you to choose a shorter loan term with a higher payment but much less total interest.

4. Loan or Lease Term Length

Stretching your loan from 60 months to 72 months can slash your monthly payment by $50-$100. But beware: you’ll pay substantially more in interest over the life of the loan, and you’ll be underwater for longer. For a lease, the standard term is 24-39 months. Leasing terms are shorter by nature, which is part of why payments are lower. However, exceeding the annual mileage limits (usually 10,000-15,000 miles/year) or having excess wear and tear can result in costly fees at turn-in.

5. Factory Incentives and Dealer Discounts

This is where your negotiation skills come in. Toyota frequently offers:

- Cash Rebates: Direct discounts off the price (e.g., $1,500 off). This reduces your principal immediately.

- Low/Zero APR Financing: Special financing rates for well-qualified buyers (e.g., 0.9% for 60 months). This can be better than taking a rebate if the interest rate is low enough.

- Dealer Markdowns: Dealer inventory, end-of-month/quarter/year quotas, and regional demand can all lead to additional discounts below MSRP. Always check the vehicle’s invoice price as a negotiation baseline. You can research the invoice price for comparable models like the Toyota RAV4 to understand typical dealer margins in your area.

You usually have to choose between a cash rebate and a low APR financing offer—you rarely get both.

6. Your Location and Dealer

Pricing isn’t uniform across the country. High-demand areas with fewer dealers (like some rural regions) often have less negotiation room. Urban areas with high dealer competition can offer better prices. Additionally, some states have higher sales tax rates, which are rolled into the total financed amount if you choose to finance them. A 6% sales tax on a $40,000 car adds $2,400 to your total cost. If you finance that tax, it increases your monthly payment.

7. Financing Source

Where you get your loan matters. Options include:

- Dealer Financing: Convenient, and they can sometimes beat outside offers, especially with manufacturer incentives. Always get the written APR before negotiating the car price.

- Bank or Credit Union: Often provides more competitive rates, especially if you have an existing relationship. Getting pre-approved here gives you a solid bargaining chip.

- Online Lenders: Companies like LightStream or Upstart can offer quick approvals and competitive rates.

The difference between a 5% and a 6.5% APR on a $30,000 loan over 60 months is about $27 per month and over $1,600 in total interest.

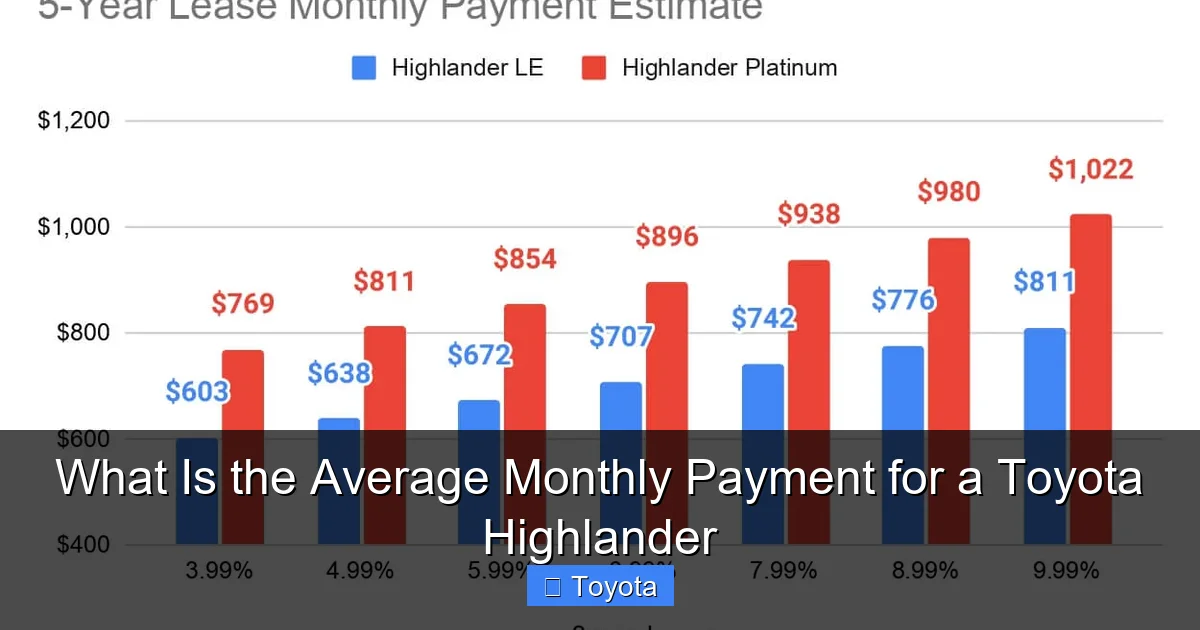

Average Monthly Payment by Trim: Real-World 2024 Examples

Enough theory. Let’s look at concrete examples. We’ll calculate estimated monthly payments for each major 2024 Highlander trim using a standard set of assumptions: a 60-month loan term, a 10% down payment, and a 5.5% APR (for a good credit score). We’ll use approximate selling prices after a modest $1,500 dealer discount, plus 6% sales tax financed into the loan.

Visual guide about What Is the Average Monthly Payment for a Toyota Highlander

Image source: pbs.twimg.com

Example 1: Toyota Highlander L (Base Model)

Selling Price (after discount): ~$36,500

With 10% down ($3,650) + 6% tax financed: Financed Amount = ($36,500 – $3,650) + ($36,500 * 0.06) = $32,850 + $2,190 = $35,040

Loan: $35,040 @ 5.5% for 60 months = $667/month

Example 2: Toyota Highlander LE (Popular Mid-Tier)

Selling Price: ~$40,000

With 10% down ($4,000) + 6% tax financed: Financed Amount = ($40,000 – $4,000) + ($2,400) = $38,400

Loan: $38,400 @ 5.5% for 60 months = $734/month

Example 3: Toyota Highlander XLE (Feature-Rich)

Selling Price: ~$44,000

With 10% down ($4,400) + 6% tax financed: Financed Amount = ($44,000 – $4,400) + ($2,640) = $42,240

Loan: $38,400 @ 5.5% for 60 months = $808/month

Important Note: These are estimates. Your actual payment will vary based on your exact negotiated price, down payment, credit score, and local tax rate. But they illustrate the clear payment climb as you move up trims. The jump from L to XLE is over $140/month in this scenario.

Leasing vs. Buying: Which Has a Lower Monthly Payment?

For many, the allure of a lower monthly payment is the primary reason to lease. Let’s compare our Highlander LE example from above.

Buying Scenario (Recap)

Financed Amount: $38,400

Term: 60 months

APR: 5.5%

Monthly Payment: ~$734

After 5 years: You own a paid-off Highlander (likely with some equity if you maintained it well).

Leasing Scenario (Estimate)

Leases are based on depreciation. A Highlander LE has a high residual value (what it’s worth at lease-end). Let’s assume:

- Negotiated Cap Cost: $40,000

- Residual Value at 36 months (approx 60% of MSRP): ~$27,000

- Depreciation Fee: ($40,000 – $27,000) / 36 months = $361/month

- Finance Fee (Money Factor ~0.00125, equivalent to ~3% APR): ($40,000 + $27,000) * 0.00125 = $84/month

- Estimated Monthly Payment: $445/month (plus tax, fees, and possibly a down payment)

The lease payment here is nearly $300 less per month. However, after 36 months, you return the car and have nothing to show for your payments (except the use of the vehicle). You must decide if the lower payment and the ability to drive a new car more frequently are worth the long-term cost without ownership.

Practical Strategies to Lower Your Toyota Highlander Payment

Armed with knowledge, here is your action plan to get the smallest, most sustainable payment possible.

1. Master Your Credit Score

This is step zero. Check your credit reports for free at AnnualCreditReport.com. Dispute any errors. Pay down revolving credit (credit cards) to lower your utilization ratio. If you’re not in a hurry, a 6-month focus on improving your score from 680 to 740 could save you 1-2% on your APR, which is thousands over the loan term.

2. Maximize Your Down Payment

This is the most direct lever. If you have $10,000 cash, using it all as a down payment on a $40,000 Highlander (financing $30,000) vs. financing $38,000 with a $2,000 down payment is a night-and-day difference in your monthly bill. Tapping savings or using trade-in equity aggressively here pays massive dividends.

3. Choose a Lower Trim or Consider a Previous Model Year

Do you really need the Platinum’s premium audio and heated rear seats? The LE and XLE are exceptionally well-equipped and satisfy the needs of 90% of buyers. A certified pre-owned (CPO) Highlander from last year with low miles can be 15-25% cheaper than a brand-new one, slashing your payment. Toyota’s CPO warranty is excellent.

4. Opt for a Longer Loan Term (With a Caveat)

If your priority is the absolute lowest monthly cash outflow, a 72-month loan will deliver. But we strongly advise against this if you can afford the 60-month payment. You pay more interest and are upside down for longer, making it harder to sell or trade later. Use this only as a last resort.

5. Shop Around for Financing BEFORE You Shop for the Car

Get pre-approved from your bank or credit union. This gives you a “blank check” with a known APR and term. You can then negotiate the car price as a cash buyer, which is a powerful position. You are no longer a “payment buyer” that dealers can manipulate. You can still see if the dealer can beat your pre-approval, but you walk in with leverage.

6. Negotiate the “Out-the-Door” Price, Not the Monthly Payment

Never let the conversation start with, “What monthly payment can you get me?” That plays right into the dealer’s hands. They will extend the term or manipulate the interest rate to hit a number you like, often at the expense of the total price. Instead, say, “I’m ready to buy today if we can agree on an out-the-door price.” This is the total price including all fees, taxes, and destination charges. Once you have that number locked in, then you discuss financing/leasing terms.

The Total Cost of Ownership: It’s Not Just the Monthly Payment

Focusing solely on the monthly payment is a classic trap. You must consider the full five-year or ownership cost.

Insurance

A fully loaded Highlander Platinum will cost significantly more to insure than a base L. Get insurance quotes for your specific trim before you buy. This is a fixed monthly cost that affects your budget.

Fuel Economy

The gas-only V6 Highlander gets an EPA-estimated 22-24 MPG combined. The Hybrid model gets 35-36 MPG combined. If you drive 15,000 miles per year and gas is $3.50/gallon, the gas model will cost about $2,250/year in fuel, while the Hybrid will cost about $1,500/year. That’s a $750 annual savings that could offset a slightly higher car payment for the hybrid.

Maintenance and Repairs

While Toyotas are reliable, all cars need upkeep. Budget for oil changes, tire rotations, brakes, and eventually new tires. A set of new tires for a Highlander can cost $800-$1,200. Following the manufacturer’s maintenance schedule is key. For other Toyota models, understanding specific maintenance needs is helpful; for instance, knowing the correct tire pressure for a Toyota Sienna is crucial for tire wear and fuel economy, and similar principles apply to the Highlander.

Taxes, Title, and Registration

These are one-time fees paid at purchase (and sometimes annually for registration). They can add $1,500-$3,000 to your initial outlay. If you finance them, they increase your monthly payment.

Conclusion: Your Payment, Your Power

So, what is the average monthly payment for a Toyota Highlander? The real answer is: it’s whatever you make it through smart planning. The raw data shows a range of $450 to $750 for new models, but that range is a landscape you can navigate. Your mission is to land on the lower end.

Start by honestly assessing your budget. How much total car cost (payment + insurance + fuel) can you comfortably afford each month? Then, work backward. Decide on the minimum trim that meets your needs. Aggressively improve your credit score. Save aggressively for a down payment. Get pre-approved financing. Negotiate the final selling price like a cash buyer. And always, always run the numbers on the total cost of ownership, not just the shiny monthly payment.

The Toyota Highlander is a fantastic vehicle that will serve you well for years. By taking control of the financial variables, you ensure that great vehicle brings you peace of mind, not financial stress. Now, go forth, armed with this knowledge, and get the Highlander payment that works for your life.

Frequently Asked Questions

How does my credit score affect my Toyota Highlander monthly payment?

Your credit score directly determines your loan’s interest rate (APR). A higher score (740+) qualifies you for the lowest rates (often 4-6%), significantly reducing your monthly payment and total interest paid. A lower score (below 650) can result in rates of 12% or higher, which can add hundreds to your monthly payment and thousands in total cost.

How much should I put down on a Highlander to lower my payment?

Aim for at least 10-20% of the vehicle’s selling price. On a $40,000 Highlander, that’s $4,000-$8,000. Every $1,000 you put down typically reduces your monthly payment by about $15-$25 on a 60-month loan. A larger down payment also helps you avoid being “upside down” on the loan and may secure a better interest rate.

Is leasing or buying better for getting a low monthly payment on a Highlander?

Leasing almost always provides a lower monthly payment because you only pay for the vehicle’s depreciation during the lease term, not the full purchase price. For the same Highlander, a lease payment can be $200-$300 less per month than a purchase payment. However, you build no equity and must return the vehicle at lease-end, subject to mileage and wear fees.

What is the typical loan term for a Toyota Highlander?

The most common loan term is 60 months (5 years). Some buyers choose 72 months (6 years) to lower the payment further, but this increases total interest paid and prolongs the period where they owe more than the car is worth. Shorter terms like 36 or 48 months have higher payments but save significantly on interest.

Does the advertised monthly payment include taxes and fees?

Almost never. Advertised “as low as” payments are usually based on the vehicle’s MSRP with a perfect credit score, a maximally sized down payment, and often exclude sales tax, registration fees, documentation fees, and any dealer-installed accessories. Always ask for the “out-the-door” price and have the dealer break down the full monthly payment including all costs.

How can I get the best interest rate on a Highlander loan?

First, improve your credit score as much as possible before applying. Second, get pre-approved from your bank or credit union before going to the dealer—this gives you a solid rate to negotiate with. Third, compare the dealer’s financing offer against your pre-approval. Finally, consider a shorter loan term, as lenders sometimes offer slightly lower APRs for shorter terms.