What Does Toyota Gap Insurance Cover?

Toyota GAP insurance helps cover the difference between your car’s actual cash value and what you owe on your loan if your vehicle is totaled or stolen. It’s especially valuable for new cars that depreciate quickly, protecting you from financial loss.

Buying a new Toyota is exciting—whether it’s a sleek Camry, a rugged Tacoma, or a fuel-efficient Prius. But behind that excitement lies a financial reality many new car owners overlook: rapid depreciation. The moment you drive your shiny new Toyota off the lot, its value starts to drop. In fact, most new cars lose about 20% of their value in the first year and up to 60% over three years. That means if you’re financing your vehicle, you could quickly owe more than it’s worth.

This is where Toyota GAP insurance steps in. GAP stands for “Guaranteed Asset Protection,” and it’s designed to protect you from that financial gap—the difference between what your car is worth and what you still owe on your loan or lease. Without GAP insurance, a total loss (like an accident or theft) could leave you paying thousands out of pocket, even after your primary auto insurance pays out. But with Toyota GAP insurance, that gap is covered, giving you peace of mind and financial protection during the most vulnerable years of ownership.

Key Takeaways

- Covers the depreciation gap: Pays the difference between your car’s current value and your outstanding loan balance after a total loss.

- Applies to leased and financed vehicles: Works with both auto loans and lease agreements on eligible Toyota models.

- Includes theft and total loss scenarios: Activates when your car is declared a total loss by your primary insurer due to accident or theft.

- May cover deductibles: Some plans reimburse your primary insurance deductible, up to a set limit.

- Eligibility based on loan terms: Typically requires a loan-to-value ratio above 100% and a loan term of 60 months or less.

- Optional but highly recommended: Not required by law, but smart for buyers of new or rapidly depreciating vehicles.

- Expires when loan is paid off: Coverage ends once your loan balance reaches zero or the term ends.

📑 Table of Contents

What Is Toyota GAP Insurance?

Toyota GAP insurance is an optional coverage plan offered through Toyota Financial Services (TFS) that protects drivers from financial loss if their vehicle is declared a total loss due to an accident or theft. It’s not part of your standard auto insurance policy but is often purchased at the time of financing or leasing a Toyota vehicle.

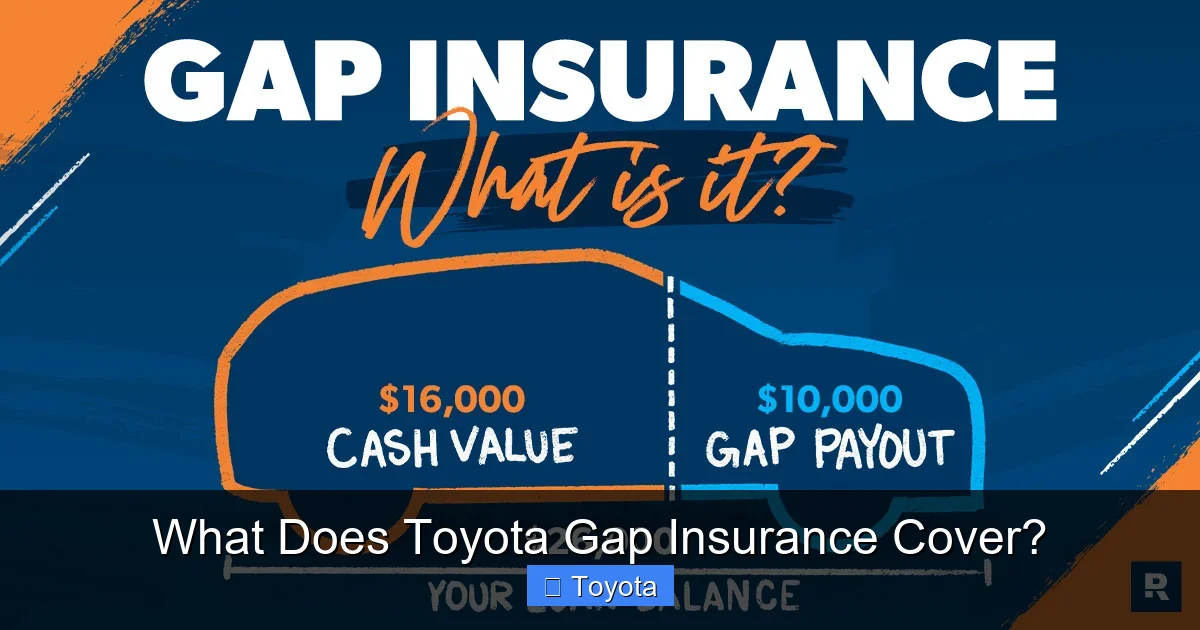

Think of it as a safety net. When your primary auto insurance company settles a claim for a totaled or stolen car, they pay the vehicle’s actual cash value (ACV) at the time of the loss. But because cars depreciate so quickly—especially new ones—that payout might not be enough to cover your remaining loan balance. For example, if your Toyota is worth $25,000 but you still owe $30,000 on your loan, you’re left with a $5,000 gap. Toyota GAP insurance steps in to cover that $5,000 (and sometimes more), so you’re not stuck paying for a car you no longer have.

This coverage is particularly valuable for buyers who:

– Made a small down payment (or none at all)

– Have a long loan term (60+ months)

– Are leasing their Toyota

– Purchased a vehicle that depreciates quickly

It’s important to note that Toyota GAP insurance is not the same as extended warranty coverage or mechanical breakdown insurance. It doesn’t cover repairs, maintenance, or mechanical failures. Its sole purpose is to protect you from financial loss due to depreciation after a total loss event.

How Does Toyota GAP Insurance Work?

Visual guide about What Does Toyota Gap Insurance Cover?

Image source: explaincharges.com

Understanding how Toyota GAP insurance functions in real-life scenarios can help you see its value. Let’s walk through the process step by step.

When you purchase a new or certified pre-owned Toyota and finance it through Toyota Financial Services, you have the option to add GAP insurance to your contract. This is usually done at the dealership during the financing process. The cost is typically a one-time fee, often rolled into your monthly payments, ranging from $500 to $1,000 depending on the vehicle, loan amount, and term.

Now, imagine this situation: You’re driving your new Toyota RAV4 home from work when another driver runs a red light and totals your vehicle. Your primary auto insurance company investigates and declares the car a total loss. They determine the actual cash value of your RAV4 to be $28,000 based on market conditions, mileage, and condition. However, you still owe $33,000 on your loan. That leaves a $5,000 gap.

Here’s where Toyota GAP insurance kicks in. Once your primary insurer pays their $28,000 settlement, you file a claim with Toyota Financial Services under your GAP policy. After verifying the details, TFS pays the remaining $5,000 directly to your lender, closing out your loan balance. You walk away with no out-of-pocket expense for the loan—just the cost of your primary insurance deductible (which may also be covered, depending on your plan).

Claim Process and Requirements

To file a claim under Toyota GAP insurance, you’ll need to follow a few key steps:

1. Notify your primary auto insurance company immediately after the accident or theft.

2. Allow them to process the claim and declare the vehicle a total loss.

3. Once the settlement is issued, contact Toyota Financial Services to initiate the GAP claim.

4. Provide required documentation, such as the insurance settlement letter, police report (if applicable), and loan payoff statement.

5. Wait for TFS to review and approve the claim, typically within 10–15 business days.

It’s important to act quickly. Delays in reporting or missing documentation can slow down the process. Also, your primary insurer must first determine the vehicle is a total loss—GAP insurance doesn’t apply to partial damage or repairs.

What Triggers Coverage?

Toyota GAP insurance activates under two main conditions:

– **Total Loss Due to Accident:** When your vehicle is damaged beyond repair in a collision, rollover, or other covered incident.

– **Theft:** If your Toyota is stolen and not recovered within a specified period (usually 30 days), and your insurer declares it a total loss.

Note that GAP insurance does not cover mechanical failure, wear and tear, or damage from natural disasters unless your primary policy includes comprehensive coverage and the loss is declared total. Also, intentional damage or losses due to illegal activity (like joyriding) are typically excluded.

What Does Toyota GAP Insurance Cover?

Visual guide about What Does Toyota Gap Insurance Cover?

Image source: cdn.ramseysolutions.net

Now let’s get into the specifics: what exactly does Toyota GAP insurance cover? While the core benefit is covering the loan balance gap, there are additional protections and limits to understand.

The Depreciation Gap

This is the primary purpose of GAP insurance. When your Toyota is totaled or stolen, your primary insurer pays the actual cash value (ACV), which is often less than what you owe. Toyota GAP insurance covers the difference up to the policy limit—usually the original loan amount or a percentage of it.

For example:

– Loan balance: $35,000

– ACV paid by insurer: $27,000

– Gap: $8,000

– Toyota GAP insurance pays: $8,000 (assuming it’s within policy limits)

This ensures your loan is fully satisfied, and you’re not left making payments on a car you no longer possess.

Deductible Reimbursement

Many Toyota GAP plans also cover your primary insurance deductible, up to a certain amount—often $1,000. So if your deductible is $500, the GAP policy may reimburse you for that cost. This is a valuable perk, especially since deductibles can be high on comprehensive and collision coverage.

For instance, if your deductible is $1,000 and your GAP plan covers up to $1,000, you get that money back after the claim is processed. This reduces your out-of-pocket expense to zero in many cases.

Lease Protection

If you’re leasing a Toyota, GAP insurance is especially important. Lease agreements often require you to carry GAP coverage, but even if not mandatory, it’s highly recommended. When a leased vehicle is totaled, the leasing company expects the full residual value to be paid. If the insurance payout falls short, you’re responsible for the difference—unless you have GAP insurance.

With Toyota GAP coverage on a lease, the policy pays the gap between the ACV and the remaining lease obligations, including any early termination fees or outstanding payments.

Loan Payoff and Refinancing

If you refinance your Toyota loan with another lender, your GAP insurance may still apply—but only if the new loan pays off the original TFS loan. Toyota GAP insurance is tied to the original financing agreement, so transferring the loan to a third party could void coverage unless properly documented.

Always check with Toyota Financial Services before refinancing to ensure your GAP protection remains valid.

What Doesn’t Toyota GAP Insurance Cover?

Visual guide about What Does Toyota Gap Insurance Cover?

Image source: cdn.ramseysolutions.net

While Toyota GAP insurance offers strong protection, it’s not a catch-all solution. Understanding its limitations helps you make informed decisions.

Partial Damage or Repairs

GAP insurance only applies when your vehicle is declared a total loss. If your Toyota is damaged but repairable, GAP coverage does not activate. You’ll need to rely on your collision or comprehensive insurance for repairs.

Mechanical Failures and Wear

Normal wear and tear, engine failure, transmission issues, or other mechanical problems are not covered. These fall under extended warranty or maintenance plans, not GAP insurance.

Late Payments or Default

If you stop making payments on your loan and the car is repossessed, GAP insurance does not apply. Coverage is only valid when the loss occurs due to an insured event (accident or theft), not financial default.

Exceeding Policy Limits

Toyota GAP insurance has a maximum payout, usually based on the original loan amount or a percentage of the vehicle’s value. If the gap exceeds this limit, you’re responsible for the excess. For example, if your policy covers up to $10,000 but the gap is $12,000, you’ll pay the remaining $2,000.

Non-Covered Vehicles

Not all Toyota models or financing arrangements qualify. Typically, GAP insurance is available for new and certified pre-owned Toyotas financed through TFS. Used vehicles outside the certified program or those with very high mileage may be excluded.

Who Should Consider Toyota GAP Insurance?

GAP insurance isn’t necessary for every driver, but it’s a smart choice for many. Here’s who benefits most:

Buyers with Low or No Down Payment

If you financed your Toyota with little or no money down, you’re likely “upside-down” on your loan from day one. A small down payment means higher loan balances and a bigger risk of owing more than the car is worth. GAP insurance protects you from that immediate depreciation hit.

Long-Term Loan Borrowers

Loans with terms of 60 months or longer increase the risk of negative equity. The longer you pay, the more time your car has to lose value. GAP insurance is especially useful for 72- or 84-month loans, where depreciation outpaces loan repayment.

Lease Customers

Leased vehicles are often driven harder and depreciate faster. Since you don’t own the car, you’re still responsible for its value if it’s totaled. GAP insurance ensures you’re not stuck with a large bill at the end of the lease.

Buyers of High-Depreciation Models

Some Toyota models, like luxury trims or high-performance variants, lose value faster than others. If you’re buying a fully loaded Highlander or a sporty GR Supra, GAP insurance can be a wise investment.

First-Time Car Buyers

New drivers or first-time buyers may not fully understand depreciation or loan dynamics. GAP insurance offers a safety net during the learning curve of car ownership.

How Much Does Toyota GAP Insurance Cost?

The cost of Toyota GAP insurance varies based on several factors, including the vehicle’s price, loan amount, term, and whether it’s new or certified pre-owned. On average, expect to pay between $500 and $1,000 for coverage.

This fee is typically added to your financing agreement and rolled into your monthly payments, making it easy to budget. For example, a $750 GAP policy on a 60-month loan adds about $12.50 per month—a small price for significant protection.

Compared to the potential out-of-pocket cost of a $5,000 to $10,000 gap, the upfront cost is minimal. It’s also often cheaper than purchasing GAP insurance from a third-party provider, as Toyota offers competitive rates through TFS.

Is It Worth the Cost?

For most new car buyers, especially those with low down payments or long loan terms, the answer is yes. The peace of mind and financial protection far outweigh the modest cost. However, if you made a large down payment (20% or more), have a short loan term (36–48 months), or are buying a used car with slow depreciation, GAP insurance may be less necessary.

Always weigh your personal risk tolerance and financial situation. If you can comfortably absorb a $5,000 loss, you might skip it. But if that amount would cause financial strain, GAP insurance is a smart buy.

Tips for Getting the Most Out of Toyota GAP Insurance

To maximize the value of your GAP coverage, keep these tips in mind:

Buy It at the Right Time

Purchase GAP insurance when you finance or lease your Toyota. It’s easiest to add at the dealership, and you’ll get the best rates through TFS. Waiting too long or trying to buy it afterward may limit your options or increase costs.

Read the Fine Print

Every GAP policy has terms, conditions, and exclusions. Review the contract carefully to understand coverage limits, deductible reimbursement caps, and claim procedures. Don’t assume it covers everything—know what’s included.

Keep Records Organized

Store your loan agreement, insurance documents, and GAP policy information in a safe place. If a claim arises, you’ll need quick access to these files.

Don’t Cancel Too Early

Some drivers cancel GAP insurance once they believe they’re no longer upside-down on their loan. But depreciation can be unpredictable. Wait until your loan balance is significantly below the car’s value—ideally 20–30%—before considering cancellation.

Consider Alternatives

While Toyota GAP insurance is convenient, compare it with third-party GAP providers. Some credit unions or insurance companies offer similar coverage at lower rates. Just ensure the policy is compatible with your Toyota financing.

Conclusion

Toyota GAP insurance is a powerful tool for protecting your financial investment in a new or certified pre-owned vehicle. It covers the critical gap between your car’s depreciated value and your outstanding loan or lease balance, ensuring you’re not left paying for a car you no longer have. Whether you’re financing with little down, leasing, or driving a high-depreciation model, GAP insurance offers peace of mind during the most vulnerable years of ownership.

While it’s not mandatory, the relatively low cost and high potential benefit make it a smart choice for many Toyota buyers. Just remember to understand what’s covered, what’s not, and how to file a claim if needed. With Toyota GAP insurance, you can drive confidently, knowing you’re protected from one of the biggest financial risks of car ownership.

Frequently Asked Questions

What does Toyota GAP insurance cover?

Toyota GAP insurance covers the difference between your vehicle’s actual cash value and your outstanding loan or lease balance if your car is totaled or stolen. It may also reimburse your insurance deductible, up to a set limit.

Is Toyota GAP insurance required?

No, it’s optional. However, some lenders or leasing companies may require it, especially for loans with low down payments or long terms.

Can I buy Toyota GAP insurance after financing?

It’s best to purchase it at the time of financing. While some third-party providers offer post-purchase GAP coverage, Toyota Financial Services typically requires it to be added during the initial loan or lease agreement.

Does GAP insurance cover theft?

Yes, if your Toyota is stolen and not recovered, and your primary insurer declares it a total loss, GAP insurance will cover the loan balance gap.

How long does Toyota GAP insurance last?

Coverage lasts for the duration of your loan or lease term, or until the loan balance reaches zero—whichever comes first.

Can I cancel Toyota GAP insurance early?

Yes, you can usually cancel it once your loan balance is significantly below the car’s value. Contact Toyota Financial Services to request cancellation and receive a prorated refund if applicable.