What Age Does Car Insurance Go Down for Females?

Car insurance typically goes down for females around age 25, with further savings after 30 and beyond. Insurance companies view older, more experienced female drivers as lower risk, leading to reduced premiums over time.

Key Takeaways

- Premiums often drop at age 25: This is a major milestone where many insurers consider drivers more experienced and responsible.

- Steady decreases after 30: Female drivers typically see continued rate reductions as they enter their 30s and 40s.

- Good driving record matters most: Safe driving habits have a bigger impact on rates than age alone.

- Location and vehicle type influence costs: Urban areas and high-performance cars can offset age-based savings.

- Bundling policies saves money: Combining auto, home, or renters insurance often leads to discounts.

- Shop around annually: Rates vary widely between providers, so comparing quotes can uncover better deals.

- Defensive driving courses help: Completing approved courses may qualify you for additional discounts.

📑 Table of Contents

What Age Does Car Insurance Go Down for Females?

If you’re a woman behind the wheel, you’ve probably wondered: *When will my car insurance finally get cheaper?* It’s a fair question—especially when you’re paying hundreds of dollars a month and feel like you’re doing everything right. The good news is that car insurance rates do go down for females as they get older. But it’s not just about age. A mix of experience, driving history, and smart choices all play a role.

Insurance companies use complex algorithms to assess risk. They look at data from millions of drivers to predict who is most likely to file a claim. Historically, young male drivers have been involved in more accidents, which is why they often pay higher premiums—especially in their teens and early 20s. Female drivers, on average, tend to have fewer accidents and less severe claims, which is why their rates are generally lower to begin with. But even for women, there’s a clear pattern: the older you get, the lower your insurance costs tend to be.

So, when exactly does that drop happen? While every insurer is a little different, most see a significant decrease around age 25. That’s when many women are finishing school, starting careers, and building stronger driving records. After that, rates continue to decline gradually, with the biggest savings often seen between ages 30 and 50. But again, age is just one piece of the puzzle. Your location, the type of car you drive, your credit score (in most states), and even your marital status can influence your premium. The key is understanding how these factors work together—and how you can use them to your advantage.

Why Do Car Insurance Rates Decrease with Age?

Visual guide about What Age Does Car Insurance Go Down for Females?

Image source: clovered.com

Insurance companies aren’t being generous when they lower your rates—they’re responding to data. Statistically, older drivers are involved in fewer accidents than younger ones. This trend holds true for both men and women, but it’s especially noticeable for female drivers, who already tend to have safer driving habits.

The Role of Experience

One of the biggest reasons car insurance goes down with age is experience. A 16-year-old driver has only been on the road for a few months or years. They’re still learning how to handle different weather conditions, traffic patterns, and unexpected hazards. But by the time a woman reaches her mid-20s, she’s likely logged thousands of miles. She’s probably driven in rain, snow, heavy traffic, and on highways. That experience translates to better decision-making and fewer mistakes behind the wheel.

For example, imagine two drivers: one is 19, fresh out of driver’s ed, and the other is 28 with a decade of driving under her belt. Even if both have clean records, the 28-year-old is statistically less likely to speed, text while driving, or misjudge a turn. Insurers recognize this and reward experienced drivers with lower premiums.

Maturity and Responsibility

Age often brings maturity. As women enter their late 20s and 30s, many take on more responsibilities—jobs, families, mortgages. This shift in lifestyle often leads to more cautious behavior, including safer driving. A woman who’s rushing to pick up her kids from school is less likely to speed or take unnecessary risks than someone driving to a party at 2 a.m.

Insurance companies know this. They’ve analyzed claims data and found that drivers in their 30s and 40s are less likely to engage in reckless behaviors like drunk driving or street racing. As a result, they’re seen as lower-risk customers, which means lower premiums.

Fewer High-Risk Behaviors

Young drivers, especially those under 25, are more likely to engage in behaviors that increase accident risk. These include distracted driving (like texting), driving under the influence, and speeding. While these issues affect both genders, studies show that young men are more prone to risky driving. However, even young women aren’t immune.

As women age, they tend to adopt safer habits. They’re more likely to wear seat belts, follow speed limits, and avoid driving when tired or impaired. These behaviors reduce the likelihood of accidents and claims, which directly impacts insurance costs.

Longer Driving Records

Another factor is the length of your driving record. The longer you’ve been driving without incidents, the more confident insurers become in your ability to stay safe. A clean record over 10 years is far more valuable than a clean record over two years.

For instance, a 35-year-old woman with no accidents or tickets in the past decade will almost always pay less than a 22-year-old with a similar record. Why? Because the older driver has proven her reliability over a much longer period. Insurers see her as a stable, low-risk customer.

The Big Drop: Age 25 and Beyond

Visual guide about What Age Does Car Insurance Go Down for Females?

Image source: rvandplaya.com

If you’re a woman in your early 20s, you might be frustrated by high insurance rates. But here’s the silver lining: things get better—fast. Most insurance companies consider age 25 a major turning point. That’s when many young adults have finished school, started full-time jobs, and settled into more predictable routines.

Why 25 Is a Magic Number

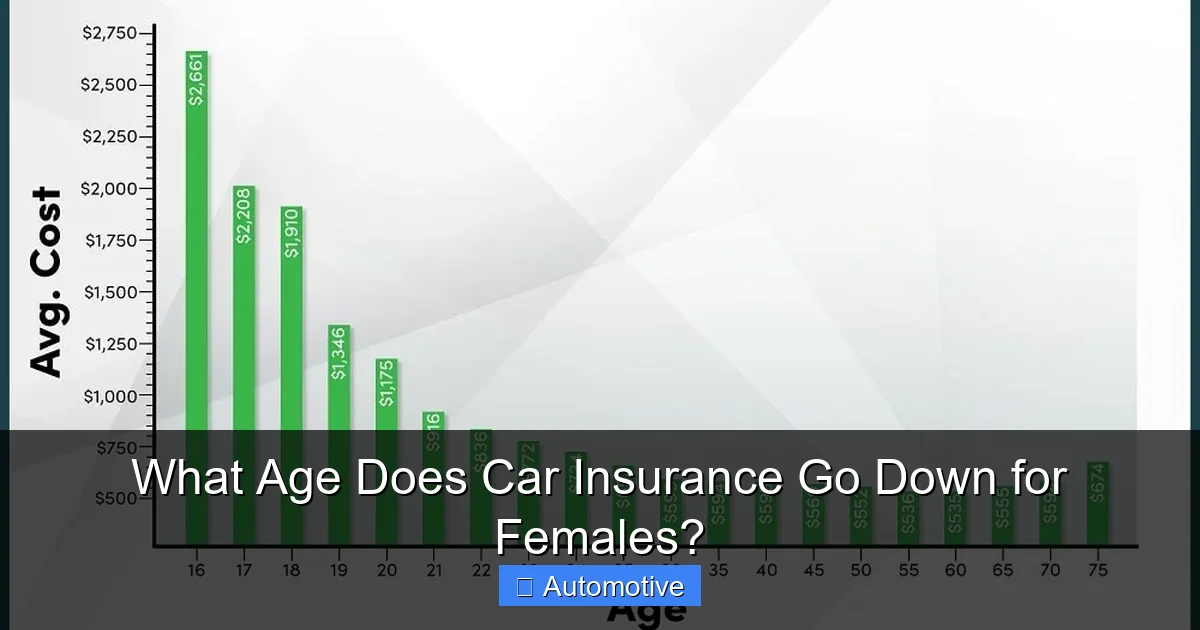

There’s no single reason why 25 is such a pivotal age, but it’s rooted in both data and tradition. Statistically, drivers under 25 are involved in more accidents per mile driven than any other age group. Once they hit 25, that trend starts to reverse. Insurers have noticed this pattern for decades, so they’ve built it into their pricing models.

For example, a 24-year-old woman might pay $200 a month for full coverage. But when she turns 25, that could drop to $160 or even $140—depending on the insurer and other factors. That’s a savings of $40 to $60 per month, or $480 to $720 per year. Over time, that adds up.

What Happens After 25?

The good news doesn’t stop at 25. Rates continue to decline as women enter their 30s, 40s, and beyond. By age 30, many female drivers see another noticeable drop. This is often due to a combination of experience, a clean driving record, and lifestyle changes like marriage or homeownership.

For instance, a 30-year-old woman who’s been driving safely for 12 years, owns a reliable sedan, and lives in a suburban area will likely pay significantly less than she did at 22. Some insurers even offer “mature driver” discounts starting at age 30 or 35.

Peak Savings in the 40s and 50s

The lowest car insurance rates for women typically occur between ages 40 and 60. During this time, drivers are usually at their most experienced, responsible, and financially stable. They’re less likely to drive recklessly, and more likely to maintain their vehicles and follow traffic laws.

A 45-year-old woman with a clean record, a mid-size SUV, and a good credit score might pay as little as $100 to $120 per month for full coverage—less than half what she might have paid at 20. These savings reflect not just age, but a lifetime of safe driving habits.

Other Factors That Influence Female Car Insurance Rates

Visual guide about What Age Does Car Insurance Go Down for Females?

Image source: clovered.com

While age is a major factor, it’s not the only one. Insurance companies look at a wide range of variables when setting premiums. Understanding these can help you take control of your costs—no matter your age.

Driving Record

Your driving history is one of the most important factors. A clean record with no accidents, tickets, or DUIs will always lead to lower rates. Even one speeding ticket can increase your premium by 10% to 20%, depending on the state and insurer.

For example, a 28-year-old woman with a clean record might pay $150 a month. But if she gets a speeding ticket, that could jump to $180. Over a year, that’s an extra $360. The lesson? Safe driving pays—literally.

Location

Where you live has a huge impact on your insurance costs. Urban areas with heavy traffic, high crime rates, and frequent accidents tend to have higher premiums. Rural areas, on the other hand, are usually cheaper.

For instance, a woman living in downtown Chicago might pay $200 a month, while someone in a small town in Iowa pays $120. Even within the same state, rates can vary widely. If you’re moving, it’s worth checking how your new location could affect your insurance.

Type of Vehicle

The car you drive matters. High-performance vehicles, luxury cars, and models with high repair costs typically come with higher premiums. Safer, more affordable cars are cheaper to insure.

For example, a 30-year-old woman driving a Honda Civic might pay $130 a month, while someone driving a BMW 3 Series could pay $180 or more. If you’re shopping for a new car, consider insurance costs as part of your decision.

Credit Score

In most states, insurers use credit-based insurance scores to help determine rates. Women with good or excellent credit often pay less than those with poor credit—even if they have clean driving records.

For instance, a 35-year-old woman with a credit score of 750 might pay $110 a month, while someone with a score of 600 pays $150. Improving your credit can lead to real savings.

Marital Status

Married women often pay less than single women. Insurers believe that married people are more responsible and less likely to take risks. This is especially true for women, who already tend to have lower accident rates.

For example, a 27-year-old single woman might pay $170 a month, while a married woman of the same age pays $140. While it’s not the biggest factor, it can make a difference.

Annual Mileage

The more you drive, the higher your risk of an accident. Women who drive fewer miles per year often qualify for low-mileage discounts.

For instance, someone who drives 5,000 miles a year might pay $120 a month, while someone driving 15,000 miles pays $160. If you work from home or use public transit, you could save significantly.

How to Lower Your Car Insurance Rates at Any Age

Even if you’re under 25 or still paying high premiums, there are steps you can take to reduce your costs. Age may help, but smart choices can speed up the process.

Maintain a Clean Driving Record

This is the most important thing you can do. Avoid speeding, running red lights, and distracted driving. Even minor violations can increase your rates. If you do get a ticket, consider taking a defensive driving course to reduce the impact.

Shop Around Annually

Insurance rates change frequently. What was a great deal last year might not be the best option now. Compare quotes from at least three different insurers each year. Use online comparison tools or work with an independent agent.

For example, a 26-year-old woman might find that her current insurer charges $160 a month, but a competitor offers the same coverage for $130. That’s a $360 annual savings just for switching.

Bundling Policies

Many insurers offer discounts if you bundle your auto insurance with home, renters, or life insurance. This can save you 10% to 25% on your total premium.

For instance, a 32-year-old woman paying $150 a month for auto insurance might save $30 by bundling with her renters policy. Over a year, that’s $360 back in her pocket.

Take a Defensive Driving Course

Completing an approved defensive driving course can qualify you for a discount—often 5% to 10%. These courses teach safe driving techniques and can also help you avoid points on your license after a violation.

For example, a 24-year-old woman who takes a course might reduce her $180 monthly premium to $162. That’s $216 saved in a year.

Choose a Higher Deductible

Raising your deductible—the amount you pay out of pocket before insurance kicks in—can lower your premium. Just make sure you can afford the higher deductible if you need to file a claim.

For instance, increasing your deductible from $500 to $1,000 might reduce your monthly payment by $20. That’s $240 saved annually.

Ask About Discounts

Many insurers offer discounts that aren’t always advertised. These can include good student discounts, low-mileage discounts, and discounts for safety features like anti-lock brakes or airbags.

For example, a 22-year-old college student with a B average might qualify for a 10% good student discount. That could save her $15 to $20 a month.

Common Misconceptions About Female Car Insurance

There are a lot of myths floating around about car insurance—especially when it comes to gender. Let’s clear up some of the most common misconceptions.

“Women Always Pay Less Than Men”

While it’s true that women generally pay less than men, especially when they’re young, the gap has narrowed in recent years. Some states have even banned the use of gender in insurance pricing. And in certain situations—like high-risk behaviors or luxury vehicles—women can end up paying more.

“Age Is the Only Thing That Matters”

Age helps, but it’s not the only factor. A 25-year-old with a DUI will pay more than a 20-year-old with a clean record. Your driving history, location, and vehicle choice all play a role.

“Once You Hit 25, Rates Drop Automatically”

While 25 is a common milestone, not all insurers apply the discount automatically. Some may require you to update your policy or re-quote. It’s important to check with your provider when you turn 25.

“Older Women Pay the Least”

While women in their 40s and 50s often have the lowest rates, this isn’t always true. A 60-year-old woman with multiple accidents or a poor credit score might pay more than a 30-year-old with a perfect record.

Conclusion

So, what age does car insurance go down for females? The answer is clear: it starts around age 25, with the biggest drops happening between 25 and 30, and continues to decline through the 40s and 50s. But age is just one piece of the puzzle. Your driving record, location, vehicle, and personal choices all influence your premium.

The best way to save on car insurance isn’t to wait for your birthday—it’s to drive safely, shop around, and take advantage of every discount available. Whether you’re 18 or 58, there are steps you can take to lower your costs and get the coverage you need at a price you can afford.

Remember, insurance isn’t just a bill—it’s protection. And the smarter you are about managing your policy, the more you’ll save over time. So keep your record clean, compare quotes regularly, and celebrate every birthday with the knowledge that your rates are getting better.

Frequently Asked Questions

At what age do car insurance rates typically drop for women?

Car insurance rates usually start to decrease for women around age 25. This is when insurers consider drivers more experienced and responsible, leading to lower premiums.

Do women always pay less for car insurance than men?

Generally, yes—especially when they’re young. However, the gap has narrowed, and in some cases, women with high-risk profiles may pay more than men with cleaner records.

Can I get a discount for being a safe driver?

Yes, many insurers offer safe driver discounts for maintaining a clean record. Some also reward low annual mileage or completing defensive driving courses.

Does getting married lower my car insurance?

In most cases, yes. Married women often receive lower rates because insurers view married individuals as more responsible and less likely to take risks.

Will my rates go down automatically when I turn 25?

Not always. Some insurers apply the discount automatically, while others require you to update your policy or request a new quote. It’s best to check with your provider.

How often should I shop for car insurance?

It’s a good idea to compare quotes at least once a year. Rates change frequently, and you could save hundreds by switching to a more competitive insurer.