What Affects Car Insurance Rates?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Affects Car Insurance Rates?

- 4 Driving History and Record

- 5 Vehicle Type and Features

- 6 Location and Where You Live

- 7 Driver Age, Gender, and Experience

- 8 Credit Score and Financial History

- 9 Coverage Level, Deductibles, and Discounts

- 10 Conclusion

- 11 Frequently Asked Questions

Car insurance rates aren’t random—they’re based on real data and risk factors. Your driving history, vehicle choice, location, age, and even credit score can significantly influence how much you pay. Understanding these elements helps you make smarter decisions and potentially lower your premiums.

Key Takeaways

- Driving history matters most: Accidents, tickets, and DUIs can drastically increase your rates, while a clean record often leads to discounts.

- Your car impacts cost: High-performance, luxury, or frequently stolen vehicles typically cost more to insure than safe, common models.

- Location plays a big role: Urban areas with higher traffic, theft, and accident rates usually have higher premiums than rural zones.

- Age and experience count: Younger drivers, especially teens, pay more due to lack of experience, while middle-aged drivers often get the best rates.

- Credit score affects pricing: In most states, insurers use credit-based insurance scores to predict risk—better credit often means lower premiums.

- Coverage level and deductibles: Higher coverage limits and lower deductibles increase premiums, but offer more protection.

- Discounts can lower costs: Safe driver, multi-policy, good student, and low-mileage discounts can significantly reduce what you pay.

📑 Table of Contents

What Affects Car Insurance Rates?

If you’ve ever shopped for car insurance, you’ve probably noticed that two people with similar cars can end up paying very different premiums. One might pay $800 a year, while another pays $1,800—for the same coverage. So, what gives? The truth is, car insurance rates aren’t arbitrary. They’re carefully calculated based on a mix of personal, vehicle, and environmental factors that help insurers assess risk.

Insurance companies use complex algorithms to predict how likely you are to file a claim. The higher the perceived risk, the more you’ll pay. But don’t worry—most of these factors are within your control. By understanding what affects car insurance rates, you can take steps to reduce your premiums without sacrificing protection. Whether you’re a new driver, shopping for your first car, or just looking to save money, this guide will break down the key elements that influence your insurance costs.

From your driving record to where you park your car at night, every detail matters. Some factors, like your age or location, you can’t change. But others—like your vehicle choice, coverage options, and driving habits—are entirely up to you. The good news? Even small changes can lead to big savings over time.

Driving History and Record

Your driving history is one of the most significant factors affecting your car insurance rates. Insurance companies see your past behavior as a strong predictor of future risk. If you’ve been in accidents, received traffic tickets, or been convicted of a DUI, insurers will consider you a higher-risk driver—and charge you accordingly.

Accidents and Claims

Even a single at-fault accident can increase your premium by 20% to 50%, depending on the severity. For example, if you rear-end another car and cause $3,000 in damage, your insurer will likely raise your rates at renewal. The more claims you file, the more your risk profile grows. Some insurers offer accident forgiveness programs, which prevent your first accident from affecting your rate—but these often come at an extra cost or require a clean record for a set period.

Visual guide about What Affects Car Insurance Rates?

Image source: directasia.com

Traffic Violations

Speeding tickets, running red lights, and illegal turns all show up on your driving record and can lead to rate hikes. A minor speeding ticket might add 10–15% to your premium, while more serious offenses like reckless driving or a DUI can double or even triple your costs. In some states, points on your license directly correlate to insurance penalties. For instance, in New York, accumulating 11 points within 18 months can result in license suspension—and a massive insurance spike.

DUIs and Major Offenses

A DUI conviction is one of the worst things that can happen to your insurance rates. Not only will your premium skyrocket—often by 80% or more—but you may also be required to file an SR-22 form, which proves you carry the minimum required insurance. This form signals to the state and insurers that you’re a high-risk driver. Some companies may even refuse to insure you after a DUI, forcing you into the non-standard or high-risk insurance market, where premiums are significantly higher.

How to Improve Your Record

The best way to keep your rates low is to drive safely and avoid violations. If you do get a ticket, consider attending traffic school—many states allow you to remove points from your record by completing a defensive driving course. Over time, as violations age (usually 3–5 years), their impact on your rates decreases. Maintaining a clean record for several years can help you qualify for safe driver discounts, which can save you 10–25% on your premium.

Vehicle Type and Features

The car you drive has a huge impact on your insurance costs. Insurers evaluate vehicles based on safety, repair costs, theft rates, and performance. A high-end sports car will almost always cost more to insure than a reliable sedan—even if both drivers have identical records.

Make, Model, and Year

Some cars are simply more expensive to insure. Luxury brands like BMW, Mercedes, and Audi often come with higher premiums due to costly repairs and parts. Similarly, high-performance vehicles like the Ford Mustang GT or Chevrolet Corvette are more likely to be involved in speeding-related accidents, so insurers charge more. On the flip side, cars like the Honda Civic, Toyota Camry, and Subaru Outback are known for their safety and reliability, making them cheaper to insure.

Visual guide about What Affects Car Insurance Rates?

Image source: smcinsurance.com

Safety Ratings and Features

vehicles with top safety ratings from organizations like the National Highway Traffic Safety Administration (NHTSA) or the Insurance Institute for Highway Safety (IIHS) often qualify for discounts. Features like automatic emergency braking, lane departure warnings, blind-spot monitoring, and adaptive headlights reduce the likelihood of accidents—and insurers reward that. For example, a 2023 Honda Accord with advanced safety tech might cost $200 less per year to insure than a similar model without those features.

Theft Rates and Repair Costs

Cars that are frequently stolen or have high repair costs will cost more to insure. The Dodge Charger and Jeep Grand Cherokee, for instance, are among the most stolen vehicles in the U.S., leading to higher comprehensive coverage rates. Similarly, electric vehicles like the Tesla Model 3 may have lower collision rates but higher repair costs due to specialized parts and labor, which can offset potential savings.

New vs. Used Cars

New cars often cost more to insure because they’re more valuable and expensive to repair or replace. However, they may also come with better safety features and manufacturer warranties, which can help balance the cost. Used cars are generally cheaper to insure, but if they’re older models with poor safety ratings, you might not qualify for certain discounts. A good rule of thumb: if your car is more than 10 years old and you only carry liability coverage, the cost of full coverage might exceed the car’s value—making it less worthwhile.

Location and Where You Live

Where you live plays a major role in determining your car insurance rates. Insurers analyze data by ZIP code to assess risk factors like traffic density, crime rates, weather patterns, and accident frequency. Even moving just a few miles can change your premium.

Urban vs. Rural Areas

Drivers in cities like Los Angeles, New York, or Chicago typically pay much higher rates than those in rural areas. Why? More traffic means more accidents. Higher population density increases the chance of collisions, vandalism, and theft. For example, a driver in downtown Atlanta might pay $2,000 a year for full coverage, while someone in a small town in Montana with the same car and record might pay only $900.

Visual guide about What Affects Car Insurance Rates?

Image source: savvyadvisor.com

Crime and Theft Rates

Areas with high vehicle theft or vandalism rates will see higher comprehensive coverage costs. If you live in a neighborhood where car break-ins are common, your insurer may charge more to cover the risk of theft or damage. Parking in a garage or using anti-theft devices like steering wheel locks or GPS trackers can help reduce this risk—and may qualify you for discounts.

Weather and Natural Disasters

Your location’s climate also affects rates. States prone to hurricanes, floods, or hailstorms—like Florida, Texas, or Colorado—often have higher comprehensive premiums. For instance, a driver in Miami might pay extra for coverage against hurricane damage, while someone in Arizona might see higher rates due to extreme heat damaging roads and increasing tire blowouts. If you live in a disaster-prone area, consider adding comprehensive and collision coverage to protect your investment.

State Regulations and Minimum Coverage

Each state sets its own minimum insurance requirements, and these directly impact what you pay. States with no-fault laws (like Michigan or Florida) often have higher premiums because drivers must carry personal injury protection (PIP) coverage. In contrast, states like Maine or Ohio have lower minimums and tend to have more affordable rates. Additionally, some states allow insurers to use credit scores in pricing, while others ban the practice—so your location can influence how much your credit affects your premium.

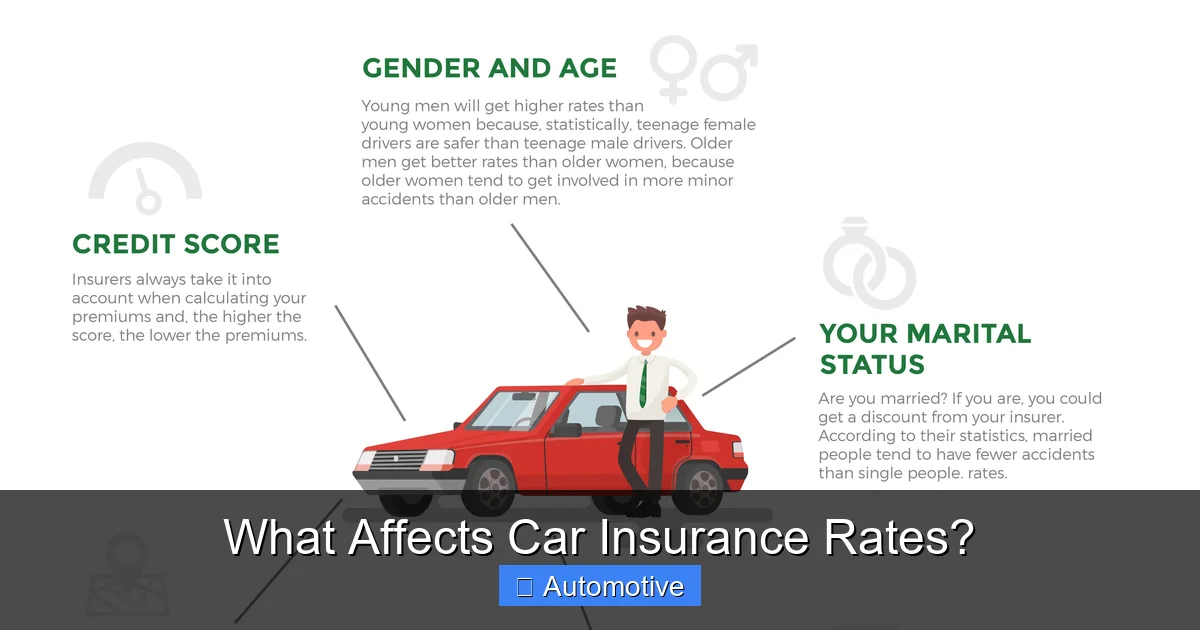

Driver Age, Gender, and Experience

Your age and driving experience are strong indicators of risk. Younger drivers, especially teens, are statistically more likely to be involved in accidents due to inexperience and risk-taking behavior. As you gain experience and reach middle age, your rates typically decrease—then slowly rise again after age 70.

Teen and Young Drivers

Insurance for drivers under 25 is notoriously expensive. A 16-year-old driver can pay $3,000 or more per year for full coverage—nearly three times the national average. This is because teens are involved in more accidents per mile driven than any other age group. Male teens tend to pay even more than female teens, as they’re statistically more likely to speed or drive recklessly. However, adding a teen to a parent’s policy is usually cheaper than getting them their own plan.

Middle-Aged Drivers

Drivers between 35 and 55 typically enjoy the lowest insurance rates. This age group has the most experience, the fewest accidents, and often the best credit scores. For example, a 45-year-old with a clean record might pay $1,200 a year for full coverage—significantly less than a 20-year-old with the same car and history.

Senior Drivers

After age 70, rates begin to rise again due to increased risk of medical issues that can affect driving ability, such as slower reaction times or vision problems. While not all seniors see rate hikes, those with recent accidents or traffic violations may face steep increases. Some insurers offer mature driver discounts or defensive driving courses to help offset costs.

Gender Differences

In most states, gender still affects insurance rates—though this is changing. Historically, young men paid more than young women because they were involved in more accidents. However, some states (like California, Hawaii, and Massachusetts) have banned the use of gender in pricing. Even where allowed, the gap is narrowing as driving behaviors become more similar across genders.

Credit Score and Financial History

Believe it or not, your credit score can affect your car insurance rates—in most states. Insurers use a credit-based insurance score, which is different from your regular credit score but closely related. It helps them predict how likely you are to file a claim.

How Credit Affects Rates

Studies show that people with lower credit scores tend to file more insurance claims. As a result, insurers charge them higher premiums. For example, a driver with excellent credit (750+) might pay $1,000 a year, while someone with poor credit (below 580) could pay $1,800 for the same coverage. The difference can be even steeper in states like Louisiana or Michigan, where credit plays a major role in pricing.

States That Allow Credit-Based Pricing

Currently, 47 states allow insurers to use credit information when setting rates. Only California, Hawaii, and Massachusetts prohibit the practice. If you live in a state that allows it, improving your credit can lead to significant savings. Paying bills on time, reducing debt, and checking your credit report for errors are all effective strategies.

What If You Have No Credit?

New drivers or immigrants with no credit history may be charged higher rates because insurers have less data to assess risk. Building credit responsibly—through a secured credit card or small loan—can help lower your premiums over time. Some insurers also offer “first-time buyer” programs or consider alternative data like rent payments.

Coverage Level, Deductibles, and Discounts

The type and amount of coverage you choose directly impact your premium. While state minimums are the cheapest option, they often leave you underinsured. Finding the right balance between cost and protection is key.

Liability vs. Full Coverage

Liability insurance covers damage you cause to others—but not your own vehicle. It’s the cheapest option but offers limited protection. Full coverage includes collision and comprehensive, which pay for damage to your car from accidents, theft, or weather. While more expensive, it’s essential if you have a newer or financed car. For example, a $30,000 car with full coverage might cost $1,500 a year, while liability-only could be $600.

Choosing Your Deductible

Your deductible is what you pay out of pocket before insurance kicks in. A higher deductible (like $1,000) lowers your premium, while a lower one (like $250) increases it. If you can afford to pay more in the event of a claim, choosing a higher deductible can save you hundreds per year. Just make sure you have the savings to cover it.

Available Discounts

Insurers offer many discounts that can reduce your premium. Common ones include:

- Safe driver discount: For maintaining a clean record.

- Multi-policy discount: Bundling auto and home insurance.

- Good student discount: For students with a B average or higher.

- Low-mileage discount: For driving fewer than 7,500 miles per year.

- Anti-theft device discount: For vehicles with alarms or tracking systems.

- Defensive driving course discount: For completing an approved course.

Always ask your insurer about available discounts—you might be missing out on savings.

Conclusion

Understanding what affects car insurance rates empowers you to make informed decisions and potentially save hundreds of dollars each year. While some factors—like your age or location—are out of your control, many others can be managed with smart choices. Maintaining a clean driving record, choosing a safe and affordable vehicle, improving your credit, and taking advantage of discounts are all proven ways to lower your premium.

Remember, insurance isn’t just a legal requirement—it’s a financial safety net. The goal isn’t to pay as little as possible, but to get the right coverage at a fair price. Regularly reviewing your policy, comparing quotes, and adjusting your coverage as your life changes can help you stay protected without overpaying.

Whether you’re a new driver, a parent adding a teen to your policy, or someone looking to cut costs, the key is awareness. By knowing what insurers look for, you can take control of your rates and drive with confidence.

Frequently Asked Questions

Does my car’s color affect insurance rates?

No, the color of your car does not affect your insurance rates. Insurers care about the make, model, year, and safety features—not the paint job. So go ahead and drive that bright red convertible if you want!

Can I lower my rates if I drive less?

Yes! Many insurers offer low-mileage discounts for drivers who travel fewer than 7,500 miles per year. If you work from home or use public transportation, ask your provider about pay-per-mile or low-mileage programs.

Will my rates go down when I turn 25?

Often, yes. Drivers typically see a significant drop in rates after age 25, as they’re no longer considered high-risk young adults. However, your actual savings depend on your driving record, location, and other factors.

Do I need full coverage on an older car?

It depends on the car’s value. If your vehicle is worth less than $4,000, the cost of full coverage may exceed its worth. In that case, liability-only coverage might make more financial sense.

Can I switch insurers to get a better rate?

Absolutely. Shopping around every 1–2 years can help you find better deals. Just make sure there’s no gap in coverage when you switch, and check for early cancellation fees.

Do insurance companies check my credit every year?

Not necessarily. Most insurers check your credit when you first apply and may re-check at renewal or if you request a quote. However, changes in your credit score can affect your rate over time.