What Affects Car Insurance Rates

Car insurance rates aren’t random—they’re based on real factors like your driving record, age, car model, and where you live. Understanding these elements helps you make smarter decisions and potentially lower your monthly premiums.

Key Takeaways

- Driving history matters most: Accidents, tickets, and claims significantly increase your rates.

- Age and experience play a big role: Younger drivers typically pay more due to higher risk.

- Your car affects your cost: Expensive, high-performance, or frequently stolen vehicles cost more to insure.

- Location impacts pricing: Urban areas with more traffic and crime lead to higher premiums.

- Credit score influences rates in most states: Better credit often means lower insurance costs.

- Coverage level and deductible choices: Higher coverage and lower deductibles raise your premium.

- Annual mileage and usage: Driving more miles or using your car for work can increase rates.

📑 Table of Contents

What Affects Car Insurance Rates

Let’s face it—car insurance can feel like a mystery. One month your premium is manageable, and the next, it jumps for reasons that aren’t always clear. You might wonder: Why is my insurance so expensive? or Why did my rate go up even though I didn’t have an accident? The truth is, car insurance companies use a complex formula to determine how much you pay, and it’s based on a mix of personal, vehicle, and environmental factors.

Understanding what affects car insurance rates doesn’t just satisfy curiosity—it empowers you to make smarter choices. Whether you’re shopping for your first policy or looking to lower your current premium, knowing the key factors can help you save hundreds of dollars each year. From your driving habits to the type of car you drive, even where you park at night can influence your rate. In this guide, we’ll break down the most important elements that insurers consider, explain how they impact your cost, and share practical tips to help you get the best possible deal.

Your Driving Record: The #1 Factor

When it comes to car insurance, your driving history is the single biggest factor insurers look at. Think of it as your “report card” behind the wheel. If you’ve got a clean record with no accidents, tickets, or claims, you’re seen as a low-risk driver—and that translates to lower premiums. On the flip side, even one speeding ticket or fender bender can cause your rates to spike.

Visual guide about What Affects Car Insurance Rates

Image source: zomgcandy.com

Accidents and Claims

Every time you file a claim—whether it’s for a minor scrape or a major collision—your insurer sees you as more likely to file another one in the future. That’s why even a small claim can increase your rate. For example, if you rear-end another car at a stoplight and the repair costs $2,000, your insurer may raise your premium by 20–40% for the next three to five years. The more severe the accident, the bigger the impact.

Traffic Violations

Speeding tickets, running red lights, DUIs, and reckless driving convictions all leave marks on your record. A single speeding ticket might add $100–$200 per year to your premium, while a DUI can double or even triple your rate. Some insurers may even drop you as a customer after a serious violation. The good news? Many states offer “forgiveness” programs or allow you to take a defensive driving course to reduce or remove points from your record.

Claims History

Even if you weren’t at fault in an accident, filing a claim can still affect your rate—especially if you use your own collision coverage. Insurers track how often you make claims, and frequent claims (even for small things like windshield repairs) can signal higher risk. Some companies offer “accident forgiveness” as a perk, which means your first at-fault accident won’t increase your rate—but this usually comes at a higher initial premium.

Tip: Drive Defensively and Stay Alert

The best way to keep your driving record clean is to practice safe driving habits. Avoid distractions like texting, follow speed limits, and maintain a safe following distance. Consider taking a defensive driving course—not only can it improve your skills, but many insurers offer discounts for completing one.

Age and Driving Experience

Your age and how long you’ve been driving play a major role in your insurance rate. It’s not just about being young or old—it’s about experience and risk. Statistically, younger drivers are more likely to be involved in accidents, which is why they pay the highest premiums.

Visual guide about What Affects Car Insurance Rates

Image source: cdn.howmuch.net

Teen Drivers: The Highest Risk Group

Drivers under 25, especially teens, face the steepest insurance rates. According to the Insurance Information Institute, 16-year-old drivers have crash rates nearly three times higher than drivers aged 20 and older. This is due to a combination of inexperience, risk-taking behavior, and distractions like passengers or phones. Adding a teen to your policy can increase your premium by 50–100%.

Young Adults: Gradual Improvement

As drivers gain experience, their rates begin to drop. By the time you’re in your mid-20s, premiums typically start to level off. However, other factors like credit score and location still play a role. Some insurers offer good student discounts or discounts for completing driver’s education, which can help offset the high cost for young drivers.

Older Drivers: Stability Pays Off

Drivers in their 30s, 40s, and 50s usually enjoy the lowest rates because they’re seen as experienced and responsible. However, rates can start to rise again after age 70, as age-related declines in vision, reaction time, and health may increase risk. Some insurers require older drivers to take a driving test or vision screening to maintain coverage.

Tip: Consider Usage-Based Insurance

If you’re a safe driver but still paying high rates due to age, consider usage-based insurance (UBI) programs. These use a mobile app or device to track your driving habits—like speed, braking, and mileage—and reward safe behavior with discounts. It’s a great way for younger or older drivers to prove they’re low-risk.

Vehicle Type and Features

The car you drive has a huge impact on your insurance rate. Insurers look at make, model, year, safety features, theft rates, and repair costs. A luxury sports car will cost far more to insure than a reliable, mid-size sedan—even if both drivers have identical records.

Visual guide about What Affects Car Insurance Rates

Image source: autoinsurance.org

Make and Model

High-performance vehicles like BMWs, Audis, and Mustangs are expensive to repair and more likely to be involved in accidents, so they come with higher premiums. Similarly, cars with high theft rates—like certain Honda and Acura models—cost more to insure because insurers anticipate more claims.

Age of the Vehicle

Newer cars often cost more to insure because they’re more expensive to replace and repair. However, they may also come with advanced safety features that can lower your rate. Older cars, while cheaper to insure for collision coverage, may not have modern safety tech, which could affect liability rates.

Safety and Anti-Theft Features

Cars equipped with features like automatic emergency braking, lane departure warnings, blind-spot monitoring, and anti-theft systems (like alarms or GPS trackers) can qualify for discounts. For example, a vehicle with a five-star safety rating from the National Highway Traffic Safety Administration (NHTSA) may be cheaper to insure than one with a lower rating.

Electric and Hybrid Vehicles

While eco-friendly cars are great for the planet, they can be more expensive to insure. Electric vehicles (EVs) like Teslas have high repair costs due to specialized parts and labor. However, some insurers offer green vehicle discounts, so it’s worth shopping around.

Tip: Compare Insurance Costs Before Buying

Before purchasing a car, check its insurance cost. Many insurers and websites offer tools to estimate premiums based on vehicle make and model. Choosing a safe, reliable, and commonly repaired car can save you money in the long run.

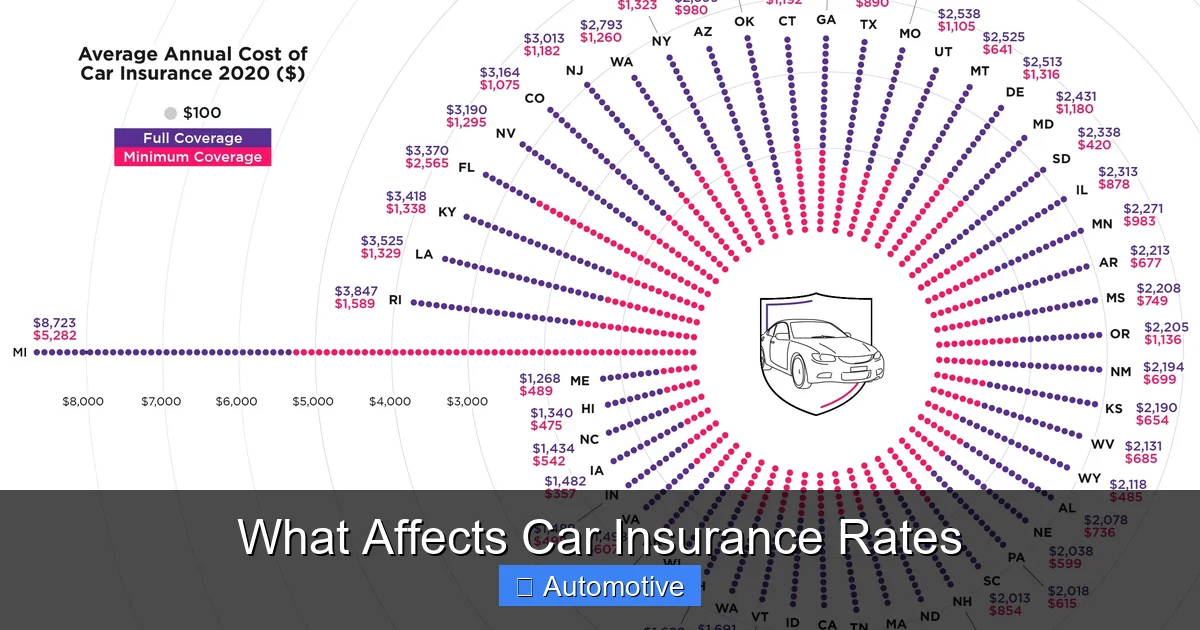

Location: Where You Live Matters

Your ZIP code can have a bigger impact on your insurance rate than you might think. Insurers analyze data by region to assess risk, and factors like traffic density, crime rates, weather, and population all play a role.

Urban vs. Rural Areas

Drivers in cities typically pay more than those in rural areas. Why? More traffic means more accidents, and urban areas often have higher rates of theft, vandalism, and uninsured drivers. For example, drivers in Detroit or Philadelphia may pay twice as much as those in rural Nebraska.

State and Local Regulations

Each state has different insurance requirements and regulations. Some states, like Michigan, have no-fault insurance laws that can drive up costs. Others, like New Hampshire, don’t require liability insurance at all (though it’s still highly recommended). Local laws, taxes, and even court systems can influence pricing.

Weather and Natural Disasters

If you live in an area prone to hurricanes, floods, hail, or wildfires, your comprehensive coverage may cost more. Insurers factor in the likelihood of weather-related damage when setting rates. For instance, drivers in Florida or Texas often pay higher premiums due to hurricane risk.

Parking Situation

Where you park your car overnight also matters. Cars parked in a locked garage are less likely to be stolen or vandalized, which can lower your rate. On the other hand, street parking in a high-crime area increases risk and cost.

Tip: Consider Moving? Think About Insurance

If you’re planning a move, research insurance costs in your new area. A cheaper house might be offset by higher car insurance. Even within a city, rates can vary by neighborhood, so it’s worth comparing.

Credit Score and Financial History

In most states (except California, Hawaii, and Massachusetts, where it’s restricted), insurers use your credit-based insurance score to help determine your rate. This isn’t the same as your regular credit score, but it’s closely related. The logic? People with better credit tend to file fewer claims.

How Credit Affects Rates

A poor credit score can increase your premium by 20–50%, sometimes more. For example, a driver with excellent credit might pay $1,200 per year, while someone with poor credit could pay $1,800 for the same coverage. Insurers see lower credit as a sign of financial instability, which they associate with higher risk.

Improving Your Credit

The good news is that improving your credit can lower your insurance costs over time. Pay bills on time, reduce debt, and check your credit report for errors. Even a small increase in your score can make a difference.

Tip: Monitor Your Credit Regularly

Use free services like AnnualCreditReport.com to check your credit report once a year. Dispute any inaccuracies, and consider using credit monitoring tools to stay on top of changes.

Coverage Level, Deductibles, and Usage

The type of coverage you choose and how you use your car also affect your rate. It’s not just about how much protection you have—it’s about how much risk you’re willing to take on.

Liability vs. Full Coverage

Liability insurance (required in most states) covers damage you cause to others. Full coverage includes collision and comprehensive, which protect your own vehicle. Full coverage costs more but offers greater protection. If you have an older car, you might save money by dropping collision coverage.

Choosing Your Deductible

Your deductible is what you pay out of pocket before insurance kicks in. A higher deductible (like $1,000) lowers your premium, while a lower deductible (like $250) increases it. Choose a deductible you can afford in case of an accident.

Annual Mileage and Usage

The more you drive, the higher your risk of an accident. Insurers ask for your annual mileage, and driving over 12,000–15,000 miles per year can increase your rate. Using your car for work or long commutes also raises costs compared to occasional pleasure driving.

Tip: Bundle and Save

Many insurers offer discounts if you bundle auto insurance with home, renters, or life insurance. You can also save by going paperless, paying in full, or setting up automatic payments.

Other Factors That Can Influence Rates

Beyond the major factors, several smaller elements can still affect your premium. These include your gender (in some states), marital status, occupation, and even your education level.

Gender and Marital Status

In states where it’s allowed, young male drivers often pay more than young females because statistics show they’re more likely to take risks. Married drivers tend to have lower rates than singles, as they’re seen as more responsible.

Occupation and Education

Some insurers offer discounts for certain professions (like teachers, engineers, or first responders) or for having a college degree. These discounts are based on the idea that these groups file fewer claims.

Insurance History

Maintaining continuous coverage is important. A lapse in insurance—even for a few days—can lead to higher rates. Insurers see gaps as a sign of risk.

Tip: Shop Around Annually

Insurance rates change frequently. What was a great deal last year might not be this year. Compare quotes from at least three insurers every 6–12 months to ensure you’re getting the best rate.

Conclusion

Car insurance rates aren’t set in stone—they’re based on a mix of personal choices, vehicle details, and environmental factors. By understanding what affects car insurance rates, you can take control of your premiums and make informed decisions. Whether it’s improving your driving record, choosing a safer car, or boosting your credit score, small changes can lead to big savings.

Remember, the cheapest policy isn’t always the best. Focus on getting the right coverage for your needs at a fair price. And don’t forget to review your policy regularly, ask about discounts, and shop around. With the right knowledge and a little effort, you can drive confidently—and affordably.

Frequently Asked Questions

Does my credit score really affect my car insurance rate?

Yes, in most states, insurers use a credit-based insurance score to help determine your rate. People with higher credit scores typically pay less because they’re seen as lower risk. Improving your credit can lead to lower premiums over time.

Will my rate go down when I turn 25?

Often, yes. Drivers under 25, especially teens, pay the highest rates due to inexperience. Once you turn 25, your rate may drop significantly, though other factors like driving record and location still apply.

Can I lower my rate if I drive less?

Absolutely. Many insurers offer low-mileage discounts for drivers who put fewer than 7,500–10,000 miles per year on their car. Be sure to report accurate mileage when getting a quote.

Does the color of my car affect insurance rates?

No, car color does not affect insurance rates. Insurers care about make, model, age, safety features, and theft rates—not the paint job. So feel free to drive that bright red sports car (though the car type itself may cost more).

Will my rate increase if I let someone else drive my car?

It depends. If a friend or family member with a clean record drives your car occasionally, it usually won’t affect your rate. But if they’re a high-risk driver (like a teen) and regularly use your car, your insurer may require them to be added to the policy, which could increase your premium.

How often should I shop for car insurance?

It’s a good idea to compare quotes at least once a year, or whenever you have a life change like moving, buying a new car, or improving your credit. Rates change frequently, and you could save hundreds by switching insurers.