Should I Get Rental Car Insurance?

Deciding whether to get rental car insurance depends on your existing coverage, the type of trip, and your risk tolerance. While it’s not always necessary, understanding your options can save you hundreds—or even thousands—in unexpected expenses.

Key Takeaways

- Check your personal auto insurance first: Many policies extend to rental cars, covering liability, collision, and comprehensive damage.

- Credit cards may offer rental protection: Some premium cards include secondary coverage, but read the fine print for limitations and exclusions.

- Rental company insurance isn’t mandatory: You can decline it, but you’ll be responsible for any damage or theft unless covered elsewhere.

- International travel often requires extra coverage: Most U.S. policies don’t cover rentals abroad, so consider purchasing local or third-party insurance.

- CDW/LDW reduces your financial risk: Collision Damage Waiver or Loss Damage Waiver limits your liability but doesn’t cover everything (e.g., tires, windows, or misuse).

- Consider a standalone rental car insurance policy: For frequent renters or high-risk trips, a dedicated policy offers broader, primary coverage.

- Always document the car’s condition: Take photos and videos before and after your rental to avoid being charged for pre-existing damage.

📑 Table of Contents

- Should I Get Rental Car Insurance? A Complete Guide

- What Is Rental Car Insurance?

- Do You Already Have Coverage?

- When Should You Buy Rental Car Insurance?

- Types of Rental Car Insurance: What’s the Difference?

- How to Avoid Unnecessary Costs

- Real-Life Scenarios: When Rental Car Insurance Paid Off

- Final Thoughts: Should You Get Rental Car Insurance?

Should I Get Rental Car Insurance? A Complete Guide

Planning a trip often involves booking flights, hotels, and—especially if you’re traveling somewhere without public transit—a rental car. But when you arrive at the rental counter, you’re hit with a barrage of questions about insurance: “Would you like to add collision damage waiver?” “How about supplemental liability protection?” “Do you want to cover personal effects?” It’s easy to feel overwhelmed, especially when the agent makes it sound like you’re risking financial ruin by saying no.

The truth? Rental car insurance isn’t always necessary—but it’s not always a waste of money, either. Whether you should get rental car insurance depends on several factors, including your existing auto insurance policy, the type of vehicle you’re renting, where you’re traveling, and how much risk you’re comfortable taking on. In this guide, we’ll break down everything you need to know to make an informed decision, so you can hit the road with confidence—and without unnecessary stress or surprise bills.

What Is Rental Car Insurance?

Visual guide about Should I Get Rental Car Insurance?

Image source: jamisonlegacygroup.com

Rental car insurance refers to the various coverage options offered by rental car companies or third-party providers to protect you financially in case something goes wrong during your rental period. These options typically include:

- Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW): This isn’t technically insurance, but a waiver that limits your financial responsibility if the car is damaged or stolen. Instead of paying for repairs or replacement, you pay a daily fee and the rental company waives most of your liability.

- Liability Insurance: Covers damage or injury you cause to others while driving the rental car. In many states, this is required by law, but rental companies often offer supplemental coverage beyond the minimum.

- Personal Accident Insurance (PAI): Pays for medical expenses for you and your passengers in case of an accident.

- Personal Effects Coverage (PEC): Protects your personal belongings if they’re stolen from the rental car.

- Roadside Assistance: Covers towing, jump-starts, tire changes, and other emergency services.

It’s important to note that these are add-ons offered by the rental company, not mandatory purchases. You have the legal right to decline them—but doing so means you’re accepting full financial responsibility for any damage, theft, or liability that occurs during your rental.

How Much Does Rental Car Insurance Cost?

The cost of rental car insurance varies widely depending on the company, location, type of vehicle, and length of rental. On average, CDW/LDW costs between $10 and $30 per day. Liability coverage might run $10–$15 per day, while PAI and PEC are usually under $10 per day each.

For a week-long trip, that can add $70 to $200+ to your rental bill—money that could go toward gas, food, or activities. That’s why it’s crucial to compare these costs against what you might already have covered through your personal auto insurance or credit card.

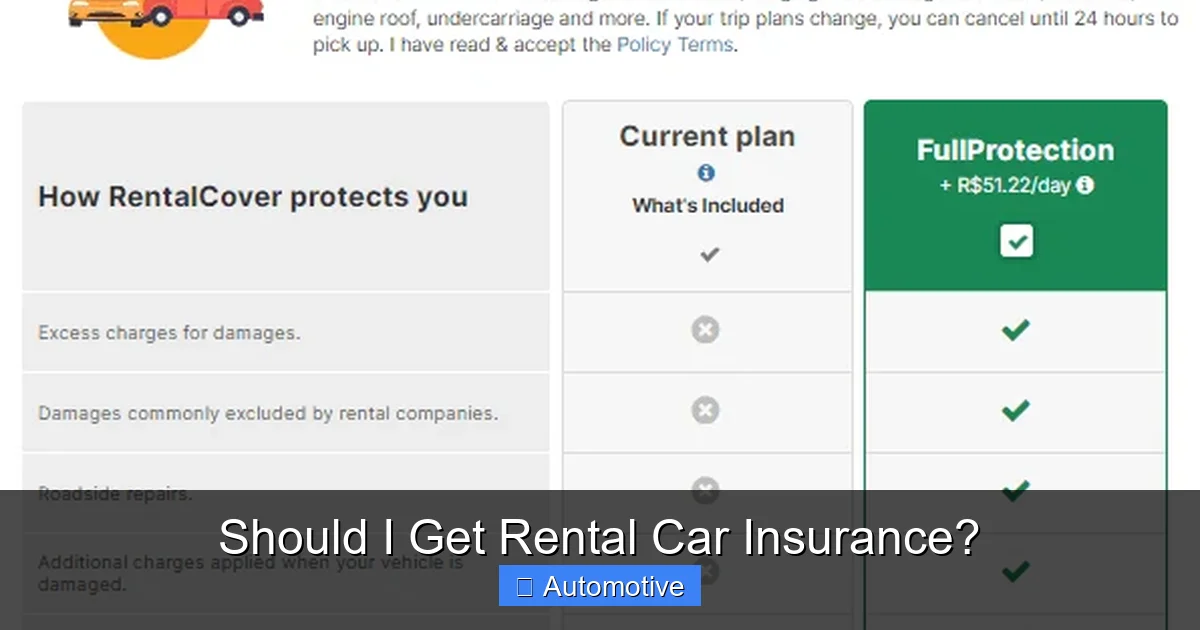

Do You Already Have Coverage?

Visual guide about Should I Get Rental Car Insurance?

Image source: blog.rentcars.com

Before you even step foot in a rental car office, the first thing you should do is check what coverage you already have. Many people don’t realize that their existing policies may already protect them when renting a car.

Your Personal Auto Insurance Policy

If you own a car and have auto insurance, there’s a good chance your policy extends to rental cars—especially if you have comprehensive and collision coverage. Most standard policies treat rental cars the same as your personal vehicle, meaning:

- Your liability coverage (for damage or injury you cause to others) applies.

- Your collision coverage pays for damage to the rental car if you’re at fault.

- Your comprehensive coverage handles theft, vandalism, fire, or weather-related damage.

However, there are exceptions. Some policies only cover rentals for a limited time (e.g., 30 days), or only for vehicles similar in size and value to your own. Luxury or exotic car rentals may not be covered. Also, if you don’t have collision or comprehensive coverage on your own car, you likely won’t have it on a rental either.

Pro Tip: Call your insurance agent before your trip and ask: “Does my policy cover rental cars? Are there any limits or exclusions?” Get it in writing if possible.

Credit Card Rental Car Coverage

Many premium credit cards—such as those from Chase Sapphire, American Express Platinum, or Capital One Venture—offer rental car insurance as a benefit. This is usually secondary coverage, meaning it only kicks in after your personal auto insurance has paid out.

Here’s how it typically works:

- You must pay for the entire rental with the eligible credit card.

- You must decline the rental company’s CDW/LDW.

- The card issuer covers damage due to collision or theft, up to the card’s limit (often the actual cash value of the car).

But beware: credit card coverage has major limitations. It usually doesn’t cover:

- Liability for damage or injury to others.

- Personal injury or medical expenses.

- Loss of use fees (when the rental company loses income while the car is being repaired).

- Rentals in certain countries (e.g., Australia, Ireland, Israel, Jamaica).

- Rentals exceeding a specific duration (often 15 days domestically, 31 internationally).

Also, some cards only cover certain types of vehicles—SUVs, trucks, or luxury cars may be excluded.

Example: Sarah rents a sedan in Florida using her Chase Sapphire Preferred card. She declines the CDW and pays with her card. If she gets into an accident, Chase will cover the damage to the rental car—but not any damage to the other vehicle or medical bills. She’d need separate liability coverage.

Homeowners or Renters Insurance

If you have homeowners or renters insurance, your personal belongings may be covered if they’re stolen from a rental car. This is usually included under your personal property coverage, but there may be limits for high-value items like electronics or jewelry.

However, this doesn’t cover the rental car itself—only your stuff inside it.

When Should You Buy Rental Car Insurance?

Visual guide about Should I Get Rental Car Insurance?

Image source: i.pinimg.com

Even if you have some existing coverage, there are situations where buying rental car insurance—or additional coverage—makes sense.

You Don’t Own a Car (or Don’t Have Auto Insurance)

If you don’t own a car and don’t have auto insurance, you have no personal policy to fall back on. In this case, the rental company’s liability coverage is essential. Without it, you could be personally responsible for thousands of dollars in damages if you cause an accident.

For example, if you rear-end another car and cause $15,000 in damage, and you didn’t buy liability coverage, you’d have to pay that out of pocket. That’s a huge financial risk.

You’re Renting a High-Value or Luxury Vehicle

If you’re renting a luxury car, sports car, or large SUV, the cost of repairs or replacement can be extremely high. Even with credit card coverage, you might hit the limit quickly. In these cases, the rental company’s CDW/LDW can provide peace of mind.

Example: Mike rents a $100,000 Porsche for a weekend getaway. His credit card only covers up to $50,000. If the car is totaled, he’d be on the hook for the remaining $50,000. Buying CDW would eliminate that risk.

You’re Traveling Internationally

Most U.S. auto insurance policies do not cover rental cars outside the country. Even credit card coverage often excludes international rentals or has strict limitations.

When traveling abroad, you’ll likely need to purchase insurance through the rental company or a third-party provider. Some countries even require specific types of coverage by law.

For instance, in Italy, liability coverage is mandatory and often not included in basic rental rates. In New Zealand, you may need to purchase additional coverage for gravel roads or remote areas.

Tip: Check the rental company’s website or contact them directly to understand local insurance requirements before you arrive.

You’re Planning a High-Risk Trip

If you’re renting a car for a road trip through rough terrain, driving in heavy traffic, or traveling during winter weather, the risk of damage increases. In these cases, the extra cost of CDW/LDW might be worth it to avoid potential repair bills.

Also, if you’re a nervous driver or unfamiliar with local traffic laws, having full coverage can reduce stress and let you focus on enjoying your trip.

Your Existing Coverage Has Gaps

Even if you have auto insurance or credit card coverage, there may be gaps. For example:

- Your personal policy has a high deductible (e.g., $1,000), and you’d prefer not to pay that out of pocket.

- Your credit card coverage is secondary and slow to process claims.

- You’re concerned about “loss of use” fees, which aren’t covered by most personal policies or credit cards.

In these cases, purchasing the rental company’s CDW/LDW can fill those gaps and provide faster, more comprehensive protection.

Types of Rental Car Insurance: What’s the Difference?

Not all rental car insurance is created equal. Understanding the differences between the options can help you choose the right level of protection.

Collision Damage Waiver (CDW) vs. Loss Damage Waiver (LDW)

These terms are often used interchangeably, but there’s a subtle difference:

- CDW (Collision Damage Waiver): Covers damage to the rental car from collisions, regardless of fault.

- LDW (Loss Damage Waiver): Broader than CDW—it covers collision damage plus theft, vandalism, and sometimes even total loss.

Both waive your financial responsibility up to the full value of the car, but they don’t cover everything. Common exclusions include:

- Damage to tires, windows, or undercarriage.

- Damage from driving under the influence or off-road.

- Loss of use fees (when the car is out of service).

- Administrative fees charged by the rental company.

Always read the terms carefully. Some waivers require you to report damage within a certain time frame or use approved repair shops.

Supplemental Liability Insurance

This covers bodily injury and property damage you cause to others. While your personal auto insurance may include liability, the limits might be low—especially if you have a basic policy.

Rental companies often offer supplemental liability coverage that increases your protection. For example, if your personal policy has a $100,000 limit, you might be able to add $1 million in supplemental coverage for $10–$15 per day.

This is especially important if you’re renting in a state with high liability requirements or if you’re driving in a busy urban area where accidents are more likely.

Personal Accident Insurance (PAI)

PAI covers medical expenses for you and your passengers if you’re injured in an accident. It typically pays for hospital bills, ambulance fees, and sometimes lost wages.

However, if you have health insurance or travel insurance that includes medical coverage, you may not need PAI. Check your policies before buying.

Personal Effects Coverage (PEC)

This protects your belongings if they’re stolen from the rental car. But again, your homeowners or renters insurance may already cover this—up to a certain limit.

If you’re carrying expensive items like cameras, laptops, or jewelry, consider whether your existing coverage is sufficient.

Third-Party Rental Car Insurance

Instead of buying coverage from the rental company, you can purchase a standalone policy from a third-party insurer like Allianz, Travel Guard, or InsureMyTrip. These policies often offer:

- Primary coverage (no need to file with your auto insurance first).

- Broader protection, including loss of use and administrative fees.

- Coverage for international rentals.

- 24/7 claims support.

These policies are ideal for frequent travelers or those taking long trips. They can cost $10–$25 per day, similar to rental company add-ons, but with better terms.

How to Avoid Unnecessary Costs

Even if you decide to buy rental car insurance, there are ways to minimize costs and avoid surprises.

Decline What You Don’t Need

Don’t feel pressured to buy every add-on. If you already have liability coverage through your auto insurance, you probably don’t need supplemental liability. If you have health insurance, skip PAI.

Only buy what fills a real gap in your coverage.

Compare Prices Online

Some rental companies allow you to add insurance when you book online, often at a lower rate than at the counter. You can also compare third-party policies before your trip.

Document the Car’s Condition

Before driving off, inspect the car thoroughly. Take timestamped photos and videos of:

- All four sides of the vehicle.

- The interior, including seats, dashboard, and trunk.

- Any existing dents, scratches, or damage.

- The fuel gauge and odometer.

This protects you from being charged for pre-existing damage. Many rental companies now offer digital inspection tools, but it’s still smart to take your own records.

Return the Car on Time and Full of Gas

Late returns and refueling fees can add up quickly. Returning the car late might also affect your insurance coverage, as some policies only cover the agreed rental period.

Understand the Fine Print

Read the rental agreement carefully. Look for:

- Exclusions in the CDW/LDW.

- Requirements for reporting damage.

- Approved repair shops.

- Penalties for violations (e.g., driving on unpaved roads).

If anything is unclear, ask the agent to explain it in plain language.

Real-Life Scenarios: When Rental Car Insurance Paid Off

Let’s look at a few real-world examples to illustrate when rental car insurance was worth it—and when it wasn’t.

Scenario 1: The Fender Bender

Lisa rents a compact car for a weekend trip. She declines CDW, relying on her credit card coverage. On the last day, she backs into a pole, causing $2,500 in damage. Her credit card covers the repair, but the rental company charges a $500 “loss of use” fee and a $100 administrative fee—costs not covered by the card. Lisa ends up paying $600 out of pocket.

Lesson: Credit card coverage has gaps. CDW would have waived all fees.

Scenario 2: The Theft

David rents an SUV for a family vacation. He buys LDW for $20/day. A week into the trip, the car is stolen from a hotel parking lot. The rental company replaces it immediately, and David pays nothing beyond the LDW fee.

Lesson: LDW provided peace of mind and financial protection against total loss.

Scenario 3: The International Trip

Maria rents a car in France. Her U.S. auto insurance doesn’t cover international rentals, and her credit card excludes Europe. She buys full coverage from the rental company. When she gets a small scratch, the company waives the repair cost.

Lesson: For international travel, rental company insurance is often essential.

Final Thoughts: Should You Get Rental Car Insurance?

So, should you get rental car insurance? The answer isn’t one-size-fits-all. It depends on your personal situation, existing coverage, and risk tolerance.

If you have comprehensive auto insurance and a credit card with rental protection, you may not need to buy additional coverage—especially for short, domestic trips in standard vehicles. But if you’re traveling internationally, renting a high-value car, or don’t have any personal coverage, the rental company’s insurance (or a third-party policy) is a smart investment.

The key is to do your homework before you rent. Check your insurance policies, read the fine print, and assess the risks. A little preparation can save you from a major financial headache down the road.

Remember: the goal isn’t to eliminate all risk—it’s to manage it wisely. With the right information, you can make a confident decision and enjoy your trip without worrying about what could go wrong.

Frequently Asked Questions

Is rental car insurance required by law?

No, rental car insurance is not required by law. However, you must meet the minimum liability requirements of the state or country where you’re renting. The rental company may require you to show proof of insurance or purchase their coverage.

Can I use my credit card’s rental car insurance if I don’t have auto insurance?

Yes, but only if the card offers primary coverage (most offer secondary). Also, you must pay for the entire rental with the card and decline the rental company’s CDW/LDW. Check your card’s terms for exclusions and limits.

Does rental car insurance cover roadside assistance?

Some rental companies offer roadside assistance as an add-on, but it’s not included in standard CDW/LDW. If you have a roadside assistance membership (like AAA), you may not need to purchase it separately.

What happens if I decline rental car insurance and get into an accident?

You’ll be financially responsible for all damages to the rental car, any other vehicles involved, and medical bills if applicable. Your personal auto insurance or credit card may cover some costs, but you could still face out-of-pocket expenses.

Can I buy rental car insurance after I’ve already rented the car?

Generally, no. Most rental companies require you to purchase insurance at the time of rental. However, some third-party insurers allow you to buy coverage up to 24 hours after pickup—check their policies.

Is rental car insurance refundable if I don’t use it?

No, rental car insurance is typically non-refundable, even if you don’t file a claim. It’s a fee for the peace of mind and risk coverage during your rental period.