Is Root Car Insurance Good

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is Root Car Insurance?

- 4 How Does Root Car Insurance Work?

- 5 Pros and Cons of Root Car Insurance

- 6 Who Should Consider Root Car Insurance?

- 7 Root vs. Traditional Car Insurance: A Comparison

- 8 Real Customer Experiences with Root

- 9 Tips for Getting the Best Rate with Root

- 10 Final Verdict: Is Root Car Insurance Good?

- 11 Frequently Asked Questions

Root Car Insurance uses smartphone technology to track your driving habits and reward safe behavior with lower premiums. While it can save careful drivers money, it may not be ideal for everyone—especially those with spotty records or inconsistent driving patterns.

Key Takeaways

- Usage-Based Pricing: Root determines your rate by analyzing your driving behavior through a mobile app, not just credit score or demographics.

- Potential Savings for Safe Drivers: If you brake smoothly, avoid hard accelerations, and drive during low-risk hours, you could save significantly compared to traditional insurers.

- No Agent Visits Required: Everything is handled via the Root app—from signing up to filing claims—making it convenient for tech-savvy users.

- Coverage Options Are Standard: Root offers liability, collision, comprehensive, uninsured motorist, and personal injury protection, similar to other major carriers.

- Not Available in All States: As of 2024, Root operates in 34 states, so availability depends on your location.

- Mixed Customer Reviews: Some users praise transparency and savings, while others report app glitches or unexpected rate increases after the initial discount period.

- Good for Low-Mileage Drivers: Since mileage factors into scoring, people who drive less often benefit more from Root’s model.

📑 Table of Contents

- What Is Root Car Insurance?

- How Does Root Car Insurance Work?

- Pros and Cons of Root Car Insurance

- Who Should Consider Root Car Insurance?

- Root vs. Traditional Car Insurance: A Comparison

- Real Customer Experiences with Root

- Tips for Getting the Best Rate with Root

- Final Verdict: Is Root Car Insurance Good?

What Is Root Car Insurance?

Root Car Insurance is a relatively new player in the auto insurance market that’s shaking up how premiums are calculated. Unlike traditional insurers who rely heavily on your credit score, age, gender, or ZIP code, Root uses a smartphone-based telematics program to assess your actual driving habits. The idea is simple: if you’re a safe driver, you should pay less—no matter your background.

Founded in 2015 and backed by venture capital, Root has positioned itself as a tech-forward alternative to legacy insurers like State Farm or Geico. Instead of visiting an agent or filling out lengthy forms online, you download the Root app, take a test drive (usually 2–4 weeks), and let the app collect data on your braking, acceleration, phone usage while driving, and time of day you’re on the road. Based on this “driving score,” Root offers you a personalized quote.

This model appeals especially to younger drivers, gig workers, and anyone tired of being penalized for factors outside their control—like living in a high-theft neighborhood or having a less-than-perfect credit history. But does it actually deliver on its promise of fairer, cheaper insurance? That’s what we’re here to unpack.

How Does Root Car Insurance Work?

The Test Drive Process

Getting started with Root begins with what they call a “test drive.” You download the free Root app (available on iOS and Android), enter basic info about yourself and your vehicle, and then drive normally for 2–4 weeks. During this period, the app runs in the background, collecting real-time data using your phone’s GPS and motion sensors.

Visual guide about Is Root Car Insurance Good

Image source: themoneyninja.com

The app tracks four key behaviors:

- Smooth braking: Sudden stops lower your score.

- Gentle acceleration: Rapid speeding up is flagged as risky.

- Phone handling: If the app detects your phone moving independently of the car (suggesting you’re holding it), it counts against you.

- Time of day: Driving late at night or during rush hour may negatively impact your score.

Importantly, Root doesn’t monitor your location or record conversations—just movement patterns. After the test drive, you receive a driving score and a customized quote. If you accept, you can activate your policy immediately through the app.

Policy Setup and Claims

Once you’re approved, setting up your policy is entirely digital. You choose your coverage limits, add drivers, and pay your premium—all within the app. There’s no paperwork, no phone calls with agents, and no in-person meetings. Payments can be made monthly or annually, and you can adjust your plan anytime.

Filing a claim is also app-based. If you’re in an accident, you open the Root app, tap “File a Claim,” and follow the prompts. You can upload photos, describe what happened, and even chat with a claims representative directly in the app. Root promises fast responses, often resolving minor claims within 24–48 hours.

For roadside assistance, Root partners with third-party providers like Agero. While it’s not included in all plans, it’s available as an add-on for a small fee. Towing, jump-starts, and lockout services are typically covered up to certain limits.

Pros and Cons of Root Car Insurance

Advantages of Choosing Root

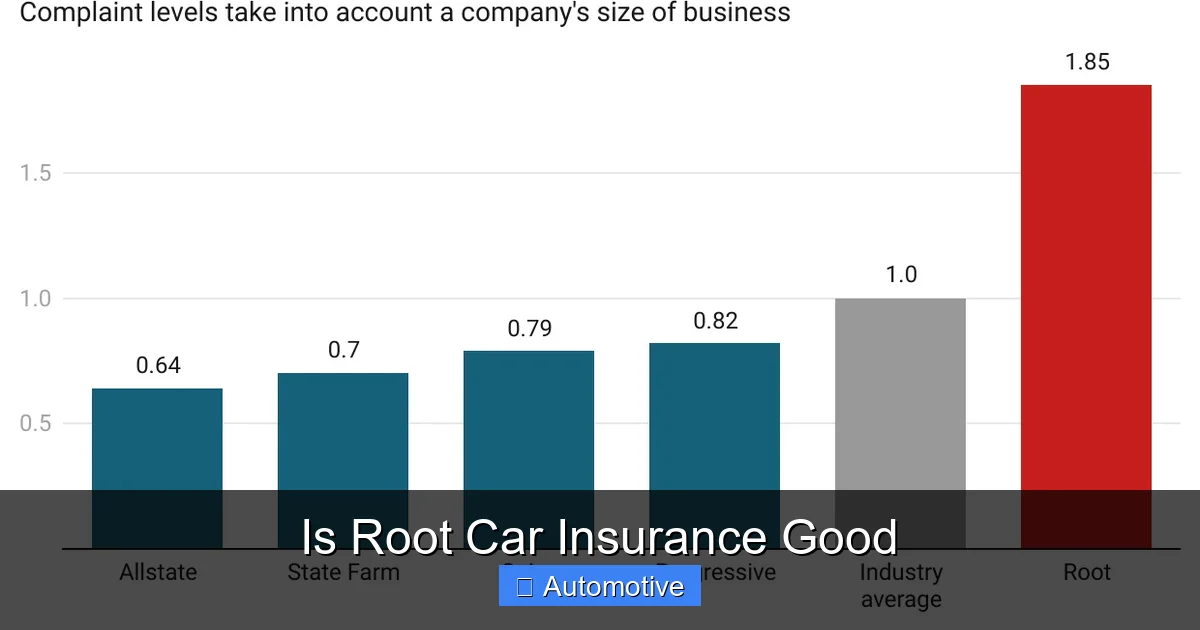

One of Root’s biggest selling points is transparency. Because your rate is based on how you drive—not where you live or what you do for work—it feels more equitable to many customers. Safe drivers genuinely see lower premiums. In fact, Root claims its customers save an average of $950 per year compared to other insurers.

Visual guide about Is Root Car Insurance Good

Image source: themoneyninja.com

Another major plus is convenience. The entire experience—from sign-up to claims—is designed for mobile-first users. If you’re comfortable managing finances and services via your smartphone, Root eliminates the hassle of dealing with call centers or paper forms.

Root also offers competitive coverage options. You can get standard liability, collision, and comprehensive coverage, plus extras like rental reimbursement and gap insurance. Their policies meet state minimum requirements everywhere they operate, and they’re rated “A-” (Excellent) by AM Best, a respected insurance rating agency.

For low-mileage drivers—such as remote workers, students, or retirees—Root can be a financial win. Since mileage affects your driving score, people who don’t drive much naturally perform better in the app and qualify for deeper discounts.

Drawbacks and Limitations

Despite its innovative approach, Root isn’t perfect. One common complaint is that the initial discount doesn’t always last. Some users report their rates increasing after the first renewal, even if their driving habits haven’t changed. This happens because Root recalculates your premium annually based on updated risk models—not just your past performance.

The app itself can be glitchy. Users on both iOS and Android have reported crashes, inaccurate scoring, or failure to record drives properly. If the app doesn’t capture your data correctly, your score—and thus your rate—could be unfairly affected. While Root allows you to dispute scores, the process isn’t always smooth.

Geographic availability is another limitation. As of 2024, Root operates in only 34 states, including California, Texas, Florida, and Illinois—but not New York, Massachusetts, or Pennsylvania. If you move to a non-covered state, you’ll need to switch insurers.

Finally, Root may not be ideal for high-risk drivers. If you have a history of accidents, DUIs, or frequent traffic violations, your driving score will likely suffer—and your premium could end up higher than with a traditional insurer that offers forgiveness programs or accident-free discounts.

Who Should Consider Root Car Insurance?

Ideal Candidates

Root shines brightest for safe, consistent drivers who log moderate to low mileage. Think: college students with clean records, young professionals who commute short distances, or empty nesters who only drive occasionally. These drivers typically score well in the app and reap the rewards in lower premiums.

Visual guide about Is Root Car Insurance Good

Image source: itriedrootcarinsurance.weebly.com

Tech-savvy individuals who prefer managing services digitally will also appreciate Root’s seamless app experience. If you already handle banking, shopping, and subscriptions through your phone, Root fits right into your lifestyle.

Gig economy workers—like DoorDash drivers or Uber Eats couriers—might find value in Root, too. While commercial driving isn’t covered under personal policies, many gig drivers use their personal cars for short trips and low mileage, which aligns well with Root’s scoring model.

Who Might Want to Look Elsewhere?

If you drive aggressively, frequently brake hard, or use your phone while driving (even hands-free), Root may not save you money. Similarly, if you often drive late at night or during heavy traffic, your score could dip—and so could your discount.

Families with multiple teen drivers should also proceed with caution. Adding a new driver—especially a young one—can spike your premium, even if they’re careful. Traditional insurers sometimes offer multi-car or good-student discounts that Root doesn’t match.

Lastly, if you value human interaction or prefer speaking with an agent during claims, Root’s fully digital model might feel impersonal. While their chat support is generally responsive, it’s not the same as having a dedicated agent who knows your history.

Root vs. Traditional Car Insurance: A Comparison

To truly understand whether Root is “good,” it helps to compare it side-by-side with conventional insurers. Let’s look at three key areas: pricing methodology, customer service, and flexibility.

Pricing Fairness

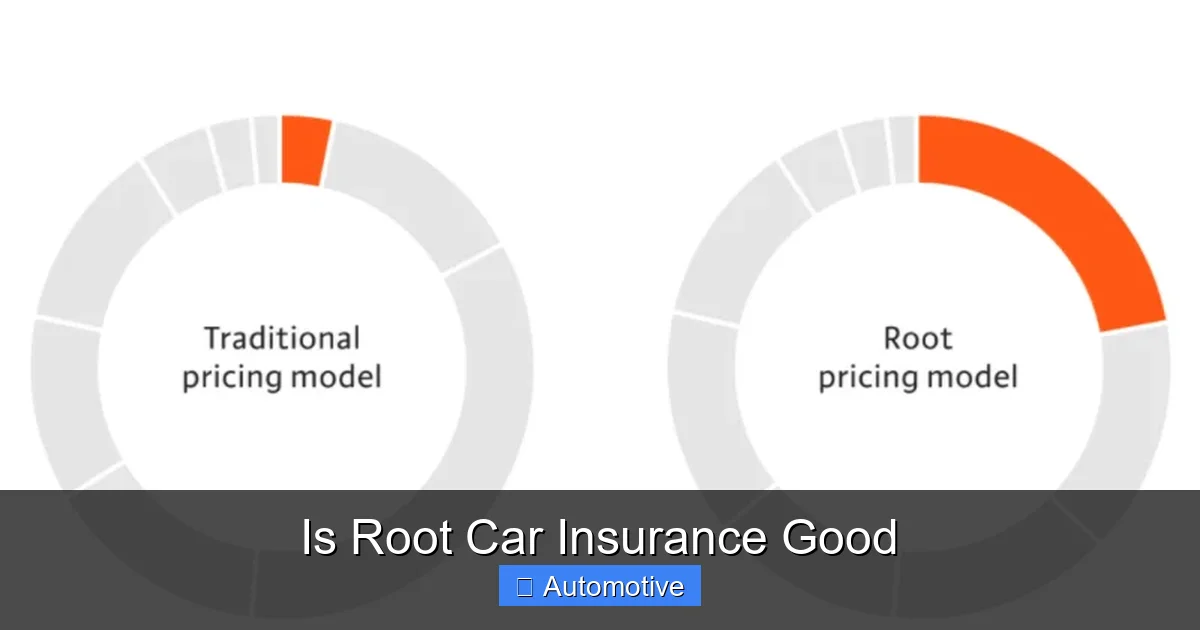

Traditional insurers use what’s called “proxy-based pricing.” They estimate your risk using indirect factors like age, marital status, credit history, and even your occupation. A 25-year-old male in Detroit with a B average in college might pay more than a 45-year-old female teacher in rural Ohio—even if they drive identically.

Root flips this model. Your rate depends solely on how you drive. Two people with identical cars and addresses could pay vastly different amounts based on their braking habits and phone discipline. For safe drivers, this is a win. For others, it might mean higher costs.

Customer Experience

Legacy insurers often have local agents, physical offices, and established reputations. That can be comforting if you prefer face-to-face service or need help navigating complex claims. However, it also means longer wait times, paperwork, and less transparency in how rates are set.

Root offers speed and clarity—but at the cost of personal touch. Their app is intuitive, and claims are processed quickly, but there’s no local agent to call when you’re stressed after an accident. Whether this is a pro or con depends on your preferences.

Flexibility and Customization

Both Root and traditional insurers let you customize coverage levels. However, Root’s pricing is more dynamic. If you improve your driving over time, your rate could drop at renewal. With many traditional carriers, discounts are static unless you manually request a review.

On the flip side, traditional insurers often offer more discount types—safe driver, multi-policy, anti-theft device, etc.—that Root doesn’t emphasize. So if you qualify for several of those, you might save more with a conventional provider.

Real Customer Experiences with Root

To get a balanced view, it’s helpful to hear from actual users. Online reviews (from sites like Trustpilot, BBB, and Reddit) show a mix of enthusiasm and frustration.

Many customers praise Root for finally rewarding their careful driving. One user in Ohio reported saving over $1,200 in their first year after switching from Progressive. “I brake gently, don’t speed, and never touch my phone while driving,” they wrote. “Root noticed—and paid me back.”

Others appreciate the simplicity. A freelance graphic designer in Austin said, “I signed up in 10 minutes while waiting for coffee. No calls, no forms. Just my phone.”

But not all feedback is positive. Several users complain about sudden rate hikes. One woman in Georgia said her premium doubled after renewal despite no change in her driving. “I checked my score—it was still 98/100. I don’t understand why my rate went up,” she shared.

App reliability is another pain point. A teacher in Colorado noted, “The app crashed three times during my test drive. I had to restart it manually each time. It felt unprofessional.”

These experiences highlight a key truth: Root works best for disciplined, low-mileage drivers who don’t mind a fully digital experience. If your habits or preferences differ, another insurer might suit you better.

Tips for Getting the Best Rate with Root

If you decide to try Root, here are some practical tips to maximize your savings:

- Drive during daylight hours: Avoid late-night trips, especially between 10 PM and 4 AM, when risk scores tend to rise.

- Keep your phone still: Use a mount or place your phone in the glove compartment. Even picking it up to change music can hurt your score.

- Brake gradually: Anticipate stops instead of slamming on the brakes. Smooth deceleration is a major scoring factor.

- Accelerate gently: Avoid rapid starts from stoplights or stop signs.

- Complete the full test drive: Don’t skip days. Consistent data gives Root a clearer picture of your habits.

- Review your score weekly: The app shows your progress—use it to adjust your behavior before your quote is finalized.

Remember, your initial discount is just the beginning. Continue practicing safe driving habits to maintain low premiums at renewal.

Final Verdict: Is Root Car Insurance Good?

So, is Root Car Insurance good? The answer isn’t black and white—it depends on who you are and how you drive.

For safe, low-mileage drivers who embrace technology and value transparency, Root can be an excellent choice. It offers real savings, a user-friendly app, and a refreshing alternative to outdated pricing models. If you’re tired of paying more because of where you live or what you do for work, Root puts the power back in your hands—literally.

However, if you’re a high-mileage driver, frequently drive at night, or prefer human interaction during stressful situations like accidents, Root might not be the best fit. Its limitations in availability, occasional app issues, and potential for rate increases after renewal mean it’s not a one-size-fits-all solution.

Ultimately, Root represents a shift toward personalized, behavior-based insurance—a trend that’s likely to grow. Whether it’s right for you comes down to your driving habits, lifestyle, and comfort with digital-only service. If you’re curious, take the test drive. It’s free, and you might just find yourself saving hundreds.

Frequently Asked Questions

How does Root determine my car insurance rate?

Root uses a smartphone app to track your driving behavior during a 2–4 week test drive. It analyzes braking, acceleration, phone usage, and time of day to calculate a personalized driving score, which determines your premium.

Can I get a discount if I’m a safe driver with Root?

Yes! Safe drivers who brake smoothly, accelerate gently, avoid phone use, and drive during low-risk hours typically receive significant discounts—often hundreds of dollars less than traditional insurers.

Is Root Car Insurance available in my state?

As of 2024, Root operates in 34 states, including California, Texas, and Florida. Check the Root website or app to see if your state is covered before signing up.

What happens if the Root app crashes during my test drive?

If the app fails to record your driving data, contact Root support immediately. You may need to restart the test drive or provide additional information to ensure your score is accurate.

Does Root offer roadside assistance?

Yes, but it’s not included in all plans. Roadside assistance can be added for a small fee and covers services like towing, jump-starts, and lockout help through third-party providers.

Will my Root premium increase after the first year?

Possibly. Root recalculates your rate annually based on updated risk models and your latest driving data. Even if your habits stay the same, external factors could lead to a rate change.