Is Car Insurance Cheaper in Texas?

Car insurance in Texas is often more expensive than the national average due to high population density, severe weather, and uninsured drivers. However, smart shopping, discounts, and adjusting coverage can help you find affordable rates even in this high-cost state.

Key Takeaways

- Texas ranks among the most expensive states for car insurance: Average annual premiums exceed the national average, driven by urban congestion and weather-related claims.

- Minimum coverage requirements are low but risky: Texas law requires only 30/60/25 liability coverage, but this may not be enough for serious accidents.

- Your location within Texas matters: Drivers in Houston or Dallas pay more than those in rural areas due to traffic density and theft rates.

- Uninsured motorist coverage is crucial: Nearly 15% of Texas drivers are uninsured, making this optional coverage highly recommended.

- Discounts and bundling can lower your bill: Safe driver, multi-policy, and good student discounts can reduce premiums significantly.

- Credit score impacts your rate: Texas allows insurers to use credit-based insurance scores, so maintaining good credit helps lower costs.

- Shopping around annually saves money: Rates vary widely between providers, so comparing quotes each year is a smart financial move.

📑 Table of Contents

Is Car Insurance Cheaper in Texas?

If you’re considering moving to Texas—or you’re already a resident—you’ve probably asked yourself: *Is car insurance cheaper in Texas?* It’s a fair question, especially when you’re budgeting for a new life in the Lone Star State. After all, Texas is known for its wide-open spaces, friendly people, and no state income tax. But when it comes to auto insurance, the reality is a bit more complicated.

Unfortunately, the answer isn’t a simple “yes” or “no.” While some rural areas in Texas offer relatively affordable car insurance, the state as a whole tends to have higher-than-average premiums. In fact, according to recent data from the National Association of Insurance Commissioners (NAIC), Texas consistently ranks in the top 10 most expensive states for auto insurance. The average annual premium in Texas hovers around $1,800 to $2,000—well above the national average of about $1,700.

So why is car insurance more expensive in Texas? It’s not just one factor, but a combination of things: high population density in major cities, frequent severe weather events, a high rate of uninsured drivers, and even the state’s unique insurance regulations. But that doesn’t mean you’re stuck paying sky-high rates. With the right strategy, you can still find affordable coverage that fits your budget and protects your vehicle.

In this guide, we’ll break down everything you need to know about car insurance in Texas—from average costs and state requirements to tips for lowering your premium. Whether you’re a new driver, a long-time resident, or just comparing states, this article will help you understand the real cost of auto insurance in Texas and how to get the best deal.

Why Is Car Insurance So Expensive in Texas?

Visual guide about Is Car Insurance Cheaper in Texas?

Image source: res.cloudinary.com

To understand whether car insurance is cheaper in Texas, you first need to know what drives up the cost. While the state’s size and population might suggest lower costs due to less congestion, the opposite is often true—especially in urban areas.

High Population Density in Major Cities

Texas is home to some of the fastest-growing cities in the U.S., including Houston, Dallas, San Antonio, and Austin. These metropolitan areas are packed with drivers, leading to more traffic, more accidents, and higher insurance claims. More claims mean higher costs for insurers, and those costs are passed on to consumers.

For example, a driver in downtown Houston is far more likely to be involved in a fender bender or hit-and-run than someone living in a small town like Marfa. Insurers adjust their rates based on risk, so urban drivers pay more simply because they’re in a higher-risk environment.

Severe Weather and Natural Disasters

Texas is no stranger to extreme weather. From hurricanes along the Gulf Coast to tornadoes in the Panhandle and hailstorms in Central Texas, the state experiences a wide range of natural disasters. These events lead to thousands of insurance claims each year—especially for comprehensive coverage, which protects against non-collision damage.

In 2021, Winter Storm Uri caused over $10 billion in insured losses across Texas, including widespread vehicle damage from freezing temperatures and power outages. When insurers face massive payouts like this, they often raise premiums across the board to rebuild their reserves.

High Rate of Uninsured Drivers

One of the biggest reasons car insurance is more expensive in Texas is the high number of uninsured motorists. According to the Insurance Research Council, nearly 15% of Texas drivers are uninsured—well above the national average of about 12%. This means that when an uninsured driver causes an accident, your own insurance may have to cover the damages if you have uninsured motorist coverage.

Because insurers know they’ll have to pay out more in these situations, they charge higher premiums to all drivers to offset the risk. It’s a frustrating reality: even if you’re fully insured and drive safely, you’re still paying for the mistakes of others.

Legal and Regulatory Factors

Texas has a unique insurance system that allows insurers to set their own rates, as long as they’re approved by the Texas Department of Insurance (TDI). Unlike some states that strictly regulate pricing, Texas operates on a “file and use” system, meaning companies can start using new rates as soon as they file them—unless the TDI objects.

This flexibility can lead to rapid rate increases, especially after major events or rising claim costs. Additionally, Texas allows insurers to use credit scores, driving history, and even your zip code to determine your premium. While this helps insurers assess risk more accurately, it can also lead to higher costs for drivers with less-than-perfect credit or those living in high-risk areas.

Texas Car Insurance Requirements

Before we dive into whether car insurance is cheaper in Texas, it’s important to understand what coverage you’re legally required to carry. Texas has minimum liability insurance requirements that all drivers must meet.

Minimum Liability Coverage

In Texas, you must carry at least the following liability coverage:

– $30,000 for bodily injury per person

– $60,000 for bodily injury per accident

– $25,000 for property damage per accident

This is often written as 30/60/25. It’s the bare minimum required by law, and it only covers damages you cause to others—not your own vehicle or injuries.

While this minimum might seem affordable, it’s often not enough to cover serious accidents. For example, if you cause a multi-car pileup with serious injuries, $60,000 may not come close to covering medical bills, lost wages, and legal fees. That’s why many financial experts recommend carrying higher limits—such as 100/300/100—or even an umbrella policy for extra protection.

Uninsured/Underinsured Motorist Coverage

While not required, uninsured/underinsured motorist (UM/UIM) coverage is highly recommended in Texas. Given the high number of uninsured drivers, this coverage protects you if you’re hit by someone who doesn’t have insurance—or doesn’t have enough to cover your damages.

Without UM/UIM coverage, you could be left paying out of pocket for medical bills, car repairs, and other expenses. Adding this coverage typically increases your premium by $50 to $100 per year, but it’s a small price to pay for peace of mind.

Personal Injury Protection (PIP)

Texas also requires drivers to carry Personal Injury Protection (PIP) coverage, unless they explicitly reject it in writing. PIP pays for medical expenses and lost wages for you and your passengers, regardless of who caused the accident.

The minimum PIP coverage in Texas is $2,500, but you can purchase more if you choose. Like UM/UIM, PIP is especially valuable in a state with high accident rates and uninsured drivers.

Average Car Insurance Costs in Texas

Now that you know why rates are higher and what’s required, let’s look at the actual numbers. Is car insurance cheaper in Texas compared to other states? The short answer is no—but there’s more to the story.

Statewide Average Premiums

According to 2023 data from Quadrant Information Services, the average annual car insurance premium in Texas is approximately $1,950 for full coverage and $580 for minimum coverage. That’s about 15% higher than the national average for full coverage ($1,700) and slightly above average for minimum coverage.

These averages can vary widely depending on your age, driving record, vehicle type, and location. For example, a 25-year-old male with a clean driving record might pay $1,600 per year, while a 19-year-old with a speeding ticket could pay over $3,000.

Cost by City

Where you live in Texas makes a big difference in your insurance rate. Here’s a look at average annual premiums in major Texas cities:

– Houston: $2,200 (full coverage)

– Dallas: $2,100

– San Antonio: $1,900

– Austin: $1,850

– Fort Worth: $1,950

– El Paso: $1,600

– Lubbock: $1,550

As you can see, drivers in larger cities like Houston and Dallas pay significantly more than those in smaller cities like Lubbock or El Paso. This is due to higher traffic density, crime rates, and accident frequency.

Cost by Age and Gender

Age and gender also play a role in determining your premium. In Texas, young drivers—especially males under 25—pay the highest rates due to their higher risk of accidents.

For example:

– A 17-year-old male might pay $4,500 per year

– A 17-year-old female might pay $3,800

– A 35-year-old male with a clean record might pay $1,700

– A 35-year-old female might pay $1,600

These differences shrink as drivers get older and gain more experience. By age 50, rates tend to level out between genders.

Cost by Vehicle Type

The car you drive also affects your insurance cost. Sports cars, luxury vehicles, and trucks with high repair costs typically come with higher premiums. For example, insuring a Ford F-150 might cost $1,800 per year, while insuring a BMW X5 could cost $2,500 or more.

On the other hand, safe, reliable, and inexpensive-to-repair vehicles—like a Toyota Camry or Honda Civic—tend to have lower insurance rates. If you’re looking to save money, choosing a vehicle with good safety ratings and low theft rates can help reduce your premium.

How to Lower Your Car Insurance in Texas

Even though car insurance in Texas is generally more expensive, there are several strategies you can use to lower your premium and make coverage more affordable.

Shop Around and Compare Quotes

One of the most effective ways to save money is to shop around. Insurance rates can vary by hundreds of dollars between companies, even for the same coverage. Use online comparison tools or work with an independent agent to get quotes from at least three different insurers.

For example, you might find that Geico offers a $1,600 annual premium for your profile, while State Farm quotes $2,100. That’s a $500 difference just for doing a little research.

Take Advantage of Discounts

Most insurers offer a variety of discounts that can significantly reduce your premium. Common discounts in Texas include:

– Safe driver discount (for accident-free driving)

– Multi-policy discount (bundling auto and home insurance)

– Good student discount (for students with a B average or higher)

– Defensive driving course discount

– Low-mileage discount (for driving fewer than 7,500 miles per year)

– Anti-theft device discount

Some insurers also offer usage-based insurance programs, where you install a device or app that tracks your driving habits. If you drive safely—avoiding hard braking, speeding, and late-night driving—you could earn a discount of 10% to 20%.

Improve Your Credit Score

In Texas, insurers can use your credit-based insurance score to determine your premium. Drivers with good credit typically pay less than those with poor credit, even if they have the same driving record.

Improving your credit score by paying bills on time, reducing debt, and checking your credit report for errors can help lower your insurance costs over time. Just be aware that it may take several months to see a noticeable difference in your rate.

Raise Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Raising your deductible from $500 to $1,000 can lower your premium by 10% to 20%. Just make sure you have enough savings to cover the higher deductible if you ever need to file a claim.

Drop Unnecessary Coverage

If you drive an older car that’s not worth much, you might consider dropping collision and comprehensive coverage. These coverages pay to repair or replace your vehicle after an accident or theft, but they also add significantly to your premium.

For example, if your car is worth $3,000, paying $800 per year for full coverage may not make financial sense. In that case, you might be better off keeping only liability coverage and setting aside money for potential repairs.

Maintain a Clean Driving Record

Finally, the best way to keep your insurance costs low is to drive safely. Speeding tickets, accidents, and DUIs can all lead to rate increases—sometimes doubling your premium.

Defensive driving courses can not only help you avoid accidents but may also qualify you for a discount. And if you do get a ticket, consider taking a state-approved course to keep it off your record.

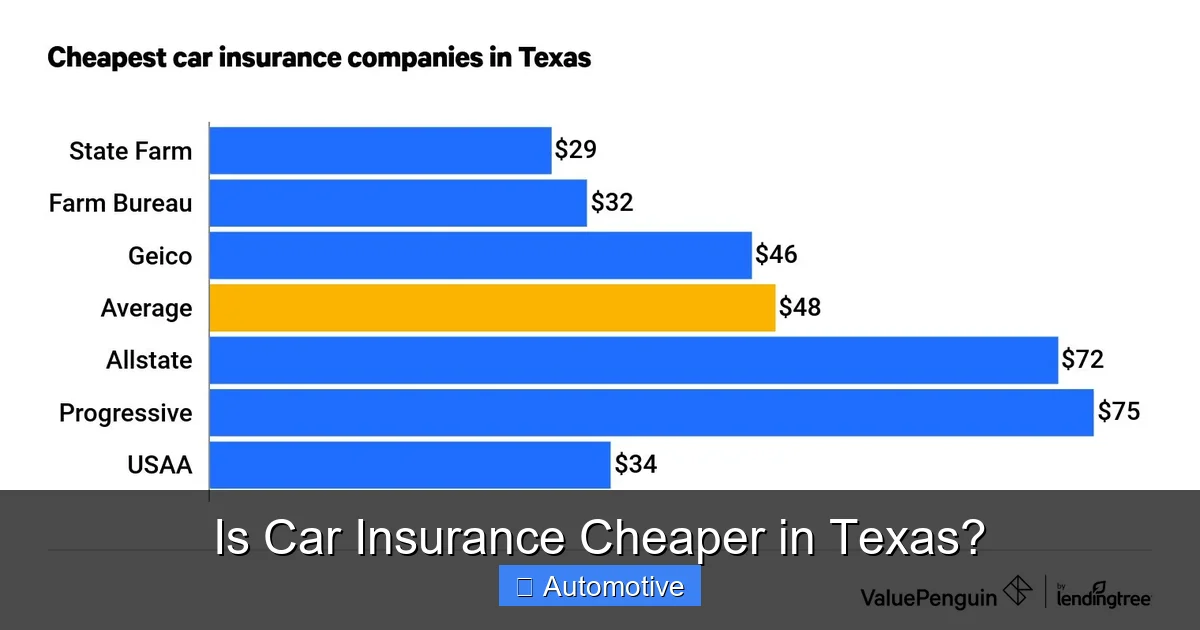

Best Car Insurance Companies in Texas

Not all insurers are created equal. Some offer better rates, customer service, and claims handling than others. Here are a few top-rated car insurance companies in Texas:

State Farm

State Farm is the largest auto insurer in Texas and offers competitive rates, especially for drivers with clean records. They also have a strong network of local agents and excellent customer service.

Geico

Geico is known for low rates and a user-friendly online experience. They offer a wide range of discounts and have a strong mobile app for managing your policy.

Progressive

Progressive is a great option for high-risk drivers or those with less-than-perfect credit. Their Name Your Price tool helps you find coverage within your budget.

USAA

If you’re a military member or veteran, USAA offers some of the lowest rates and best customer satisfaction in the industry. However, it’s only available to eligible individuals.

Allstate

Allstate offers a variety of coverage options and discounts, including accident forgiveness and new car replacement. Their Drivewise program rewards safe driving with discounts.

Final Thoughts: Is Car Insurance Cheaper in Texas?

So, is car insurance cheaper in Texas? The honest answer is no—not compared to the national average. Due to high population density, severe weather, uninsured drivers, and other risk factors, Texas consistently ranks among the most expensive states for auto insurance.

However, that doesn’t mean you can’t find affordable coverage. By understanding the factors that affect your rate, shopping around, taking advantage of discounts, and maintaining a clean driving record, you can significantly reduce your premium.

Remember, the cheapest policy isn’t always the best. Make sure you’re getting the right coverage for your needs—especially uninsured motorist and PIP coverage, which are crucial in Texas.

Ultimately, while car insurance in Texas may cost more than in other states, being an informed and proactive consumer can help you save money and stay protected on the road.

Frequently Asked Questions

Is car insurance required in Texas?

Yes, Texas law requires all drivers to carry minimum liability insurance of 30/60/25. Driving without insurance can result in fines, license suspension, and vehicle impoundment.

Why is car insurance so expensive in Houston?

Houston has high traffic density, frequent accidents, and a large number of uninsured drivers, all of which contribute to higher insurance premiums compared to rural areas.

Can I use my out-of-state insurance in Texas?

If you move to Texas, you must switch to a Texas-licensed insurer within 30 days. Out-of-state policies are not valid for long-term use in the state.

Does my credit score affect my car insurance in Texas?

Yes, Texas allows insurers to use credit-based insurance scores. Drivers with higher credit scores typically receive lower premiums.

What happens if I drive without insurance in Texas?

Driving uninsured can lead to fines up to $350 for a first offense, license suspension, and required SR-22 filing to reinstate your driving privileges.

How often should I shop for car insurance in Texas?

It’s a good idea to compare quotes at least once a year or whenever your policy renews. Rates change frequently, and you could save hundreds by switching insurers.