How to File a Car Insurance Claim

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How to File a Car Insurance Claim: A Step-by-Step Guide

- 4 Step 1: Ensure Safety and Assess the Situation

- 5 Step 2: Document the Accident Scene

- 6 Step 3: Notify Your Insurance Company

- 7 Step 4: Work with the Claims Adjuster

- 8 Step 5: Finalize the Claim and Get Repaired

- 9 Step 6: What to Do If Your Claim Is Denied or Underpaid

- 10 Tips to Avoid Common Mistakes

- 11 Conclusion

- 12 Frequently Asked Questions

Filing a car insurance claim doesn’t have to be stressful. By knowing the right steps—from gathering evidence to working with your insurer—you can protect your rights and get back on the road faster. This guide walks you through the entire process clearly and simply.

Key Takeaways

- Act quickly after an accident: Report the incident to your insurer as soon as possible to avoid delays or claim denial.

- Document everything: Take photos, collect witness info, and keep records of all related expenses.

- Know your policy: Understand your coverage limits, deductibles, and exclusions before filing.

- Work with your adjuster: Be honest, responsive, and cooperative during the investigation.

- Avoid admitting fault: Let the insurance companies determine liability based on evidence.

- Keep detailed notes: Track every conversation, email, and document related to your claim.

- Appeal if necessary: If your claim is unfairly denied or underpaid, you have the right to dispute it.

📑 Table of Contents

- How to File a Car Insurance Claim: A Step-by-Step Guide

- Step 1: Ensure Safety and Assess the Situation

- Step 2: Document the Accident Scene

- Step 3: Notify Your Insurance Company

- Step 4: Work with the Claims Adjuster

- Step 5: Finalize the Claim and Get Repaired

- Step 6: What to Do If Your Claim Is Denied or Underpaid

- Tips to Avoid Common Mistakes

- Conclusion

How to File a Car Insurance Claim: A Step-by-Step Guide

Getting into a car accident is stressful—no one plans for it. But knowing how to file a car insurance claim can make a huge difference in how quickly you recover and get back on the road. Whether it’s a fender bender in a parking lot or a more serious collision on the highway, the claims process doesn’t have to be overwhelming. With the right preparation and understanding, you can navigate it smoothly and protect your financial interests.

This guide will walk you through every step of filing a car insurance claim—from the moment the accident happens to when you receive your settlement. We’ll cover what to do at the scene, how to communicate with your insurer, what documents you’ll need, and how to avoid common pitfalls. By the end, you’ll feel confident handling a claim, even if it’s your first time. Let’s get started.

Step 1: Ensure Safety and Assess the Situation

The very first thing to do after any car accident is to make sure everyone is safe. Check yourself and your passengers for injuries. If anyone is hurt, call 911 immediately. Even if injuries seem minor, it’s smart to get medical attention—some symptoms don’t show up right away.

Visual guide about How to File a Car Insurance Claim

Image source: lookinsure.com

Next, move your vehicle to a safe location if possible. If the car is drivable and blocking traffic, pull over to the shoulder or a nearby parking lot. Turn on your hazard lights to alert other drivers. If your car is not drivable, stay inside with your seatbelt on until help arrives, especially on busy roads.

Call the Police (When Necessary)

In many states, you’re required by law to report accidents that involve injuries, significant property damage, or hit-and-run situations. Even if the damage seems minor, calling the police can be helpful. A police report creates an official record of the incident, which can be crucial when filing your claim. The responding officer will document the scene, gather statements, and assign fault if possible.

For example, imagine you’re rear-ended at a stoplight. The other driver admits they were distracted, but later changes their story. A police report with the officer’s notes can support your version of events and speed up the claims process.

Exchange Information with the Other Driver

Once everyone is safe, exchange information with the other driver(s) involved. This includes:

- Full name and contact information

- Driver’s license number

- Insurance company name and policy number

- Vehicle make, model, and license plate number

Be polite but firm. Avoid arguing or admitting fault—even saying “I’m sorry” can be misinterpreted as an admission of guilt. Stick to the facts: “I was stopped at the red light when you hit me from behind.”

Also, ask if there were any witnesses. If so, get their names and phone numbers. Witness statements can be powerful evidence if there’s a dispute about what happened.

Step 2: Document the Accident Scene

Your next priority is gathering evidence. The more documentation you have, the stronger your claim will be. Start by taking photos and videos with your smartphone. Capture:

Visual guide about How to File a Car Insurance Claim

Image source: i2.wp.com

- Damage to all vehicles involved (from multiple angles)

- License plates

- Skid marks, debris, or road conditions

- Traffic signs, signals, and lighting

- Weather conditions (rain, fog, etc.)

For instance, if it was raining and the road was slick, that could affect liability. Or if a stop sign was obscured by overgrown bushes, that might be a factor. These details matter.

Write Down What Happened

As soon as possible, write a brief summary of the accident. Include the date, time, location, weather, road conditions, and a clear description of what happened. Note the speed you were traveling, whether you had a green light, and any other relevant details.

Example: “On Tuesday, June 11, at 3:15 PM, I was driving east on Main Street in clear weather. I had a green light at the intersection with Oak Avenue. The other driver ran the red light and T-boned my car on the driver’s side.”

This written account can help you stay consistent when speaking with your insurer or the police. Memory fades quickly, so do this while the details are fresh.

Keep a File for All Documents

Start a physical or digital folder to store everything related to the accident. Include:

- Photos and videos

- Police report (once available)

- Insurance information from all parties

- Medical records and bills (if injured)

- Repair estimates and receipts

- Correspondence with your insurer

Having everything in one place makes it easier to manage your claim and respond to requests from your insurance company.

Step 3: Notify Your Insurance Company

Most insurance policies require you to report an accident within a certain time frame—often 24 to 72 hours. Even if you’re not at fault, you should contact your insurer as soon as possible. Delaying could give them a reason to deny your claim.

Visual guide about How to File a Car Insurance Claim

Image source: carinsuranceexplain.com

Call your insurance agent or use your insurer’s online portal or mobile app to start the claim. Be ready to provide:

- Your policy number

- Date, time, and location of the accident

- Description of what happened

- Names and contact info of other drivers and witnesses

- Police report number (if available)

Be Honest and Accurate

When speaking with your insurer, stick to the facts. Don’t exaggerate or downplay the damage. If you’re unsure about something, say so. For example, “I think the other car was speeding, but I didn’t see their speedometer.”

Your insurer will assign a claims adjuster to your case. This person will investigate the accident, review evidence, and determine how much your claim is worth. They may contact you for additional information or schedule an inspection of your vehicle.

Understand Your Coverage

Before your adjuster starts working, take a moment to review your policy. Know what’s covered and what’s not. Common types of coverage include:

- Collision: Pays for damage to your car from a crash, regardless of fault.

- Comprehensive: Covers non-collision events like theft, vandalism, or weather damage.

- Liability: Covers damage or injuries you cause to others.

- Personal Injury Protection (PIP) or Medical Payments: Helps pay for your medical bills after an accident.

- Uninsured/Underinsured Motorist: Protects you if the other driver has no insurance or not enough.

For example, if you have collision coverage with a $500 deductible, your insurer will pay for repairs minus $500. If you don’t have collision coverage, you may have to pay out of pocket—even if you’re not at fault.

Step 4: Work with the Claims Adjuster

Once your claim is filed, your adjuster will take the lead. They may ask to inspect your vehicle, review the police report, or speak with witnesses. Be cooperative and responsive—this helps speed up the process.

Vehicle Inspection

The adjuster will likely want to see your car. They may visit the repair shop or ask you to bring it to a designated location. During the inspection, they’ll assess the damage and estimate repair costs.

Tip: Don’t authorize repairs until the adjuster has seen the vehicle. If you fix it too soon, they may not be able to verify the extent of the damage.

Get Multiple Repair Estimates

Some insurers require you to get estimates from approved shops. Others let you choose your own repair facility. Either way, it’s wise to get at least two or three estimates. This ensures you’re getting a fair price.

For example, one shop might quote $3,200 for front-end repairs, while another says $2,700. Your insurer will usually pay based on the lowest reasonable estimate. But if you believe a higher quote is justified (e.g., for OEM parts vs. aftermarket), you can discuss it with your adjuster.

Understand the Settlement Offer

After reviewing all evidence, your adjuster will make a settlement offer. This may include:

- Cost to repair your vehicle

- Value of your car if it’s totaled (actual cash value minus deductible)

- Medical expenses (if covered)

- Rental car reimbursement (if included in your policy)

If your car is totaled, the insurer will pay you the car’s market value before the accident, minus your deductible. They’ll then take ownership of the vehicle.

Review the offer carefully. If it seems low, ask for an explanation. You can negotiate or provide additional evidence (like recent maintenance records or comparable car listings) to support a higher value.

Step 5: Finalize the Claim and Get Repaired

Once you accept the settlement, your insurer will issue payment. This may be a check to you, the repair shop, or both. If your car is being repaired, make sure the shop uses quality parts and follows the estimate.

Use a Reputable Repair Shop

Choose a shop with good reviews and proper certifications (like ASE or I-CAR). Ask if they use original equipment manufacturer (OEM) parts or aftermarket parts. OEM parts are made by your car’s manufacturer and often come with a warranty, but they’re more expensive.

Example: If your bumper is damaged, an OEM bumper might cost $800, while an aftermarket one is $500. Your insurer may only cover the aftermarket version unless your policy specifies otherwise.

Keep Receipts and Follow Up

Save all receipts for repairs, rental cars, and medical treatments. If your policy covers rental reimbursement, submit those receipts to your insurer for reimbursement.

After repairs are done, inspect your car thoroughly. Make sure everything works properly and the paint matches. If you’re not satisfied, contact the shop and your insurer.

Close the Claim

Once everything is resolved, your insurer will close the claim. You may receive a final letter or email confirming the settlement. Keep this for your records.

If you later discover additional damage or injuries, contact your insurer immediately. Some policies allow you to reopen a claim within a certain time frame.

Step 6: What to Do If Your Claim Is Denied or Underpaid

Unfortunately, not all claims are approved. If your insurer denies your claim or offers less than expected, don’t panic. You have options.

Understand Why the Claim Was Denied

Your insurer must provide a reason for denial. Common reasons include:

- Policy exclusions (e.g., driving under the influence)

- Late reporting

- Lack of coverage

- Disputed liability

Read the denial letter carefully. If the reason doesn’t make sense, ask for clarification.

File an Appeal

Most insurers have an internal appeals process. Submit a written request with supporting evidence—photos, witness statements, repair estimates, etc. Your adjuster or a supervisor will review it.

Example: Your claim was denied because the other driver said you ran a red light. But you have a dashcam video showing you had a green light. Submit that video with your appeal.

Contact Your State Insurance Department

If the appeal doesn’t work, you can file a complaint with your state’s insurance department. They can investigate and help resolve disputes. Visit the National Association of Insurance Commissioners (NAIC) website to find your state’s contact info.

In some cases, you may need to hire a lawyer, especially if there are serious injuries or large financial losses. An attorney can negotiate on your behalf or take legal action if needed.

Tips to Avoid Common Mistakes

Even with the best intentions, people often make errors that delay or hurt their claims. Here are some tips to avoid them:

Don’t Admit Fault

It’s natural to want to apologize after an accident, but avoid saying things like “I’m sorry I didn’t see you” or “It was my fault.” These statements can be used against you later. Let the insurance companies determine liability based on evidence.

Don’t Delay Reporting

Even if the damage seems minor, report it to your insurer right away. Waiting too long can raise red flags and give them a reason to deny your claim.

Don’t Sign Anything Without Understanding It

Insurance companies may ask you to sign a release or settlement agreement. Read it carefully. Once you sign, you usually can’t go back and ask for more money. If you’re unsure, ask a trusted friend or lawyer to review it.

Don’t Ignore Medical Care

If you’re injured, see a doctor—even if you feel fine. Some injuries, like whiplash or concussions, don’t show symptoms right away. Delaying treatment can weaken your claim and harm your health.

Don’t Assume the Other Driver’s Insurance Will Pay

If the other driver is at fault, their insurance should cover your damages. But they may dispute liability or offer a low settlement. Don’t rely solely on them—file a claim with your own insurer too, especially if you have collision coverage.

Conclusion

Filing a car insurance claim doesn’t have to be a nightmare. By staying calm, acting quickly, and following the right steps, you can protect your rights and get the compensation you deserve. Remember: safety first, document everything, communicate clearly with your insurer, and don’t be afraid to ask questions or appeal a decision.

Accidents happen, but being prepared makes all the difference. Keep this guide handy, review your policy regularly, and know your coverage. That way, if you ever need to file a claim, you’ll be ready—not just to survive the process, but to come out ahead.

Frequently Asked Questions

How soon should I file a car insurance claim?

You should file a claim as soon as possible, ideally within 24 to 72 hours of the accident. Most insurers require prompt reporting, and delays can lead to claim denial.

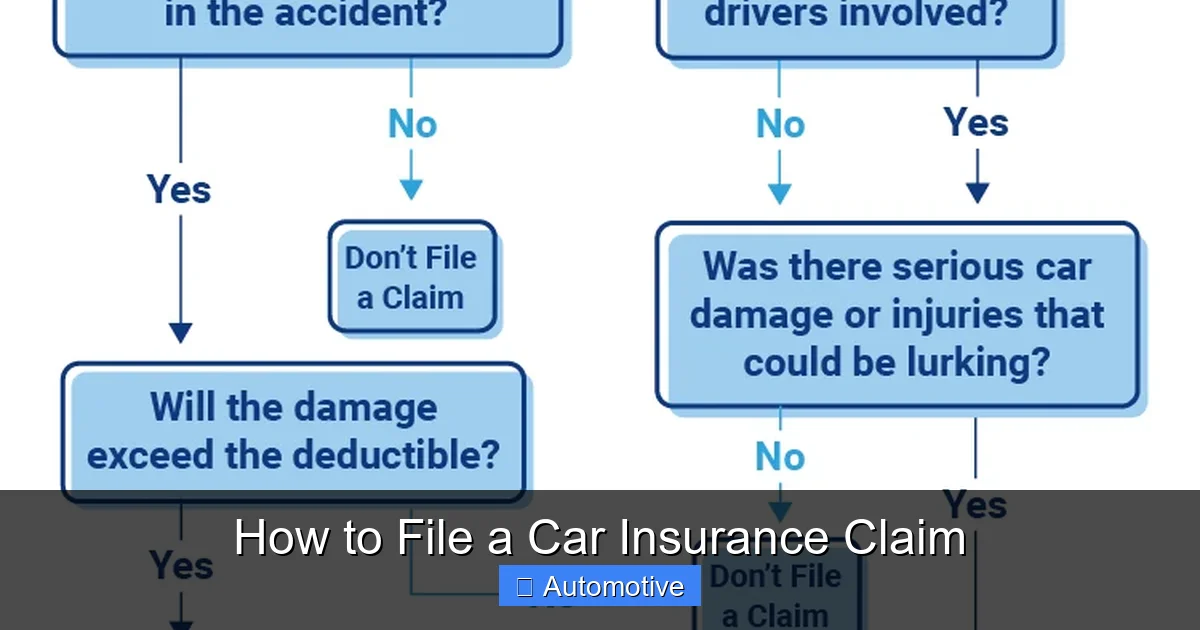

Do I need to file a claim if the damage is minor?

It depends on your policy and the cost of repairs. If the damage is less than your deductible, filing a claim may not be worth it. But if there are injuries or potential hidden damage, it’s best to report it.

Can I choose my own repair shop?

Yes, in most cases you can choose your own repair shop. Some insurers have preferred networks, but you’re not required to use them unless specified in your policy.

What if the other driver doesn’t have insurance?

If the other driver is uninsured, your uninsured motorist coverage (if you have it) can help pay for your damages. File a claim with your own insurer and provide all evidence.

Will filing a claim raise my insurance rates?

It depends on the circumstances. If you’re not at fault, your rates may not increase. But if you’re found at fault, especially for a major accident, your premiums could go up.

Can I reopen a claim after it’s closed?

Some insurers allow you to reopen a claim within a limited time (e.g., 30 days) if you discover new damage or injuries. Check with your adjuster or policy terms.