How Much Is Car Insurance in Texas?

Car insurance in Texas costs more than the national average, with drivers paying around $2,000 per year for full coverage and over $700 for minimum coverage. Rates vary widely based on location, driving history, age, and vehicle type, but smart shopping and discounts can help you save significantly.

Key Takeaways

- Average annual cost: Full coverage in Texas averages about $2,000, while minimum liability coverage costs around $750 per year.

- State requirements: Texas law requires 30/60/25 liability coverage—$30,000 per person for bodily injury, $60,000 per accident, and $25,000 for property damage.

- Location matters: Urban areas like Houston and Dallas have higher premiums due to traffic, theft, and accident rates.

- Personal factors: Age, driving record, credit score, and annual mileage all influence your premium.

- Vehicle type impacts cost: Sports cars and luxury vehicles typically cost more to insure than sedans or SUVs.

- Discounts can help: Safe driver, multi-policy, good student, and low-mileage discounts can reduce your premium by 10–30%.

- Shop around annually: Comparing quotes from at least three insurers can save you hundreds of dollars each year.

📑 Table of Contents

- How Much Is Car Insurance in Texas? A Complete Guide

- Texas Car Insurance Requirements: What You Must Carry

- Average Car Insurance Rates in Texas

- Factors That Affect Your Car Insurance Premium in Texas

- How to Save Money on Car Insurance in Texas

- Common Misconceptions About Texas Car Insurance

- Final Thoughts: Finding the Right Coverage at the Right Price

How Much Is Car Insurance in Texas? A Complete Guide

If you’re driving in the Lone Star State, you’re probably wondering: How much is car insurance in Texas? It’s a fair question—and one that doesn’t have a one-size-fits-all answer. While the average Texan pays around $2,000 per year for full coverage, your actual rate could be significantly higher or lower depending on a mix of personal, geographic, and vehicle-related factors.

Texas has some of the highest car insurance rates in the country, and for good reason. The state’s large population, sprawling urban centers, high traffic volume, and frequent severe weather events all contribute to increased risk—and higher premiums. But that doesn’t mean you’re stuck paying top dollar. With the right knowledge and a little effort, you can find affordable coverage that still meets state requirements and protects your financial future.

In this guide, we’ll break down everything you need to know about car insurance costs in Texas. From understanding what the state requires to exploring the factors that affect your premium, we’ll help you make informed decisions and potentially save hundreds of dollars each year. Whether you’re a new driver, a long-time resident, or just shopping for a better deal, this article will give you the tools to navigate Texas auto insurance like a pro.

Texas Car Insurance Requirements: What You Must Carry

Visual guide about How Much Is Car Insurance in Texas?

Image source: insurancenoon.com

Before we dive into costs, it’s important to understand what Texas law requires. Unlike some states that allow drivers to go uninsured under certain conditions, Texas mandates that all drivers carry at least a minimum level of liability insurance. This isn’t just a suggestion—it’s the law, and driving without it can result in fines, license suspension, or even vehicle impoundment.

The minimum coverage required in Texas is known as 30/60/25. Here’s what that means:

– $30,000 for bodily injury per person

– $60,000 for bodily injury per accident (if more than one person is injured)

– $25,000 for property damage per accident

This coverage only protects others—not you or your vehicle. If you cause an accident, your insurance will pay up to these limits for the other party’s medical bills and car repairs. But if you want protection for your own car, medical expenses, or damages beyond these limits, you’ll need to purchase additional coverage.

Many drivers opt for full coverage, which typically includes:

– Liability (required)

– Collision (covers damage to your car in an accident)

– Comprehensive (covers theft, vandalism, weather damage, etc.)

– Uninsured/underinsured motorist coverage (protects you if the other driver lacks insurance)

While full coverage isn’t legally required, it’s highly recommended—especially if you’re financing or leasing your vehicle. Lenders usually require it, and it provides peace of mind knowing you’re protected in a wide range of scenarios.

Why Minimum Coverage Might Not Be Enough

It’s tempting to go with the minimum coverage to save money, especially if you’re on a tight budget. But here’s the reality: $25,000 for property damage might not go far in today’s world. A minor fender bender could easily exceed that amount, especially if it involves a newer or luxury vehicle. And if someone is seriously injured in an accident you cause, $30,000 may not cover their medical bills—let alone lost wages or long-term care.

Consider this: the average cost of a hospital stay in Texas is over $15,000 per day. If you’re at fault in a multi-car pileup, your liability limits could be exhausted in minutes. And if the damages exceed your policy limits, you could be personally sued for the difference.

That’s why many financial advisors recommend carrying at least 100/300/100 coverage—$100,000 per person, $300,000 per accident, and $100,000 for property damage. It’s a small increase in premium for a huge boost in protection.

Average Car Insurance Rates in Texas

Visual guide about How Much Is Car Insurance in Texas?

Image source: zimlon.com

So, how much is car insurance in Texas, exactly? Let’s look at the numbers.

According to recent data from the National Association of Insurance Commissioners (NAIC) and industry surveys, the average annual premium for car insurance in Texas is:

– $750–$850 for minimum liability coverage

– $1,800–$2,200 for full coverage

That’s higher than the national average, which sits around $1,700 for full coverage. But these are just averages—your actual rate could be much different.

How Texas Compares to Other States

Texas ranks among the top 10 most expensive states for car insurance. Why? Several factors contribute:

– High population density in cities like Houston, Dallas, and San Antonio

– Frequent severe weather (hailstorms, tornadoes, flooding)

– High rates of uninsured drivers (nearly 15% of Texas drivers are uninsured)

– Expensive vehicle repair and medical costs

For comparison:

– Louisiana: ~$2,500 (most expensive)

– Maine: ~$1,000 (least expensive)

– California: ~$2,000

– Florida: ~$2,300

So while Texas isn’t the most expensive, it’s definitely on the higher end. But again, your personal rate depends on more than just state averages.

Sample Rates by City

Where you live in Texas makes a big difference. Urban areas with heavy traffic, higher crime rates, and more accidents tend to have higher premiums. Here’s a rough breakdown of average annual full coverage rates by major city:

– Houston: $2,400

– Dallas: $2,300

– San Antonio: $2,100

– Austin: $2,000

– Fort Worth: $2,200

– El Paso: $1,800

Rural areas like Lubbock or Amarillo may see rates closer to $1,600–$1,800. But even within a city, your ZIP code can affect your premium. Insurers use location-based risk assessments, so two drivers with identical profiles might pay different rates just a few miles apart.

Factors That Affect Your Car Insurance Premium in Texas

Visual guide about How Much Is Car Insurance in Texas?

Image source: i.imgur.com

Now that you know the average costs, let’s explore what determines your individual rate. Insurance companies use complex algorithms to assess risk, and several personal and vehicle-related factors play a role.

1. Driving Record

Your driving history is one of the biggest factors. A clean record with no accidents or tickets can qualify you for significant discounts. But even one speeding ticket can increase your premium by 10–20%. A DUI? That could double or even triple your rate.

For example:

– A 35-year-old driver with a clean record might pay $1,800/year for full coverage.

– The same driver with a recent at-fault accident could pay $2,500 or more.

Insurers look at the past 3–5 years of your driving history. Safe driving pays off—literally.

2. Age and Experience

Young drivers, especially teens, pay the highest premiums. A 16-year-old driver in Texas might pay $4,000–$6,000 per year for full coverage. Why? Statistics show that inexperienced drivers are more likely to be in accidents.

Rates typically decrease as you gain experience and reach your late 20s. By age 30, many drivers see a noticeable drop in premiums. After 50, rates may rise slightly due to age-related risk factors, but safe drivers can still maintain low costs.

3. Credit Score

In Texas, insurers can use your credit-based insurance score to determine your premium. Studies show a correlation between credit history and claim frequency—drivers with poor credit are more likely to file claims.

If your credit score is below 600, you could pay significantly more. For example:

– Excellent credit (750+): $1,600/year

– Fair credit (650–699): $2,000/year

– Poor credit (below 600): $2,800/year

Improving your credit score can lead to lower insurance rates over time.

4. Vehicle Type

The car you drive affects your premium. Insurers consider:

– Make and model (luxury and sports cars cost more)

– Age of the vehicle (newer cars are more expensive to repair)

– Safety ratings and theft rates

For example:

– A 2023 Toyota Camry: ~$1,900/year

– A 2023 BMW 3 Series: ~$2,600/year

– A 2023 Ford F-150: ~$2,100/year

Electric vehicles (EVs) can also be pricier to insure due to high repair costs and specialized parts.

5. Annual Mileage

The more you drive, the higher your risk of an accident. Drivers who commute long distances or use their car for work typically pay more than those who drive only a few thousand miles per year.

If you work from home and drive less than 5,000 miles annually, you may qualify for a low-mileage discount—saving 10–15% on your premium.

6. Coverage Limits and Deductibles

Higher coverage limits and lower deductibles mean higher premiums. For example:

– $250 deductible: higher monthly cost

– $1,000 deductible: lower monthly cost

Choosing a higher deductible can save you money upfront, but make sure you can afford to pay it out of pocket if you need to file a claim.

How to Save Money on Car Insurance in Texas

The good news? There are many ways to reduce your car insurance costs without sacrificing coverage. Here are some proven strategies.

Shop Around and Compare Quotes

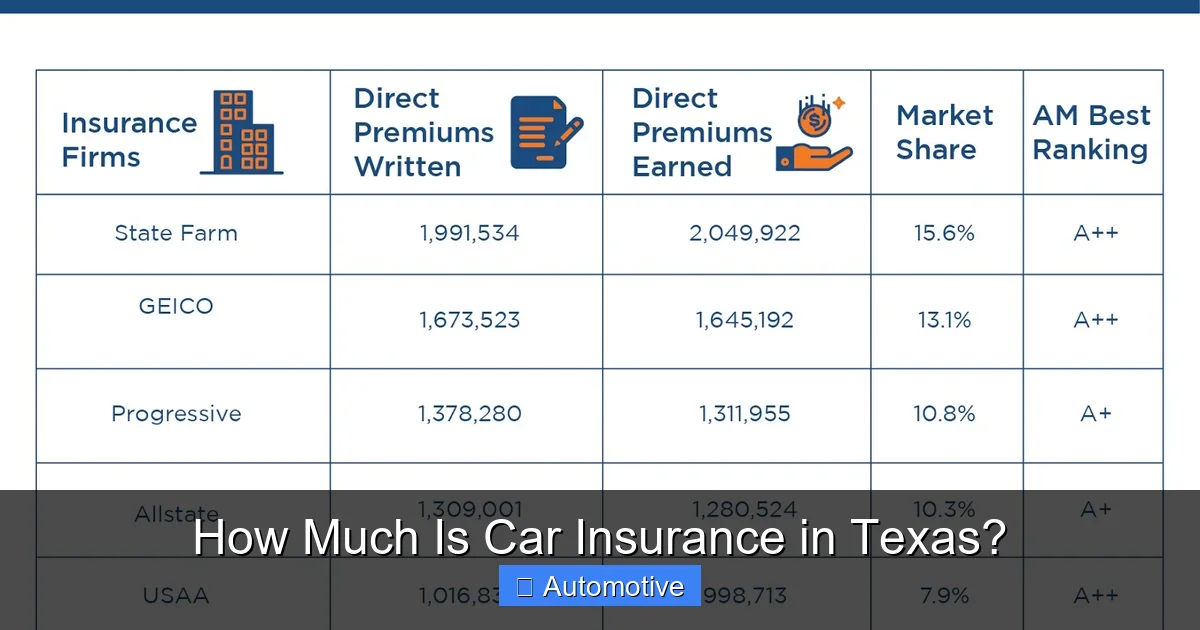

One of the easiest ways to save is to compare quotes from multiple insurers. Rates can vary by hundreds of dollars for the same coverage. Use online comparison tools or work with an independent agent to get quotes from companies like:

– State Farm

– GEICO

– Progressive

– Allstate

– USAA (if you’re military-affiliated)

Don’t just look at price—also consider customer service, claims process, and financial stability.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Common ones include:

– Safe driver discount: For no accidents or violations in the past 3–5 years

– Multi-policy discount: Bundle auto and home or renters insurance

– Good student discount: For students with a B average or higher

– Defensive driving course: Completing an approved course can save 5–10%

– Low-mileage discount: For driving under a certain number of miles per year

– Anti-theft device discount: For vehicles with alarms or tracking systems

Ask your insurer about all available discounts—you might be surprised how much you can save.

Improve Your Credit Score

Since credit affects your rate, taking steps to improve your score can lower your premium. Pay bills on time, reduce credit card balances, and check your credit report for errors.

Consider Usage-Based Insurance

Some insurers offer telematics programs that track your driving habits (speed, braking, mileage) via a mobile app or device. Safe driving can earn you discounts of 10–30%.

Raise Your Deductible

If you have an emergency fund, consider raising your deductible from $500 to $1,000. This could reduce your premium by 15–30%. Just make sure you can afford the higher out-of-pocket cost if you need to file a claim.

Maintain Continuous Coverage

Lapses in coverage can lead to higher rates. Even if you’re not driving, consider keeping a minimal policy or non-owner insurance to avoid a gap.

Common Misconceptions About Texas Car Insurance

There’s a lot of misinformation out there. Let’s clear up some common myths.

Myth: “Red cars cost more to insure.”

False. Insurers don’t care about your car’s color. They care about make, model, age, and safety features. A red Honda Civic costs the same as a blue one.

Myth: “My insurance will cover everything if I’m in an accident.”

Not necessarily. Your policy only covers what’s listed. If you only have liability, your own car repairs won’t be covered. And if damages exceed your limits, you could be on the hook for the difference.

Myth: “I can’t switch insurers mid-policy.”

You can switch at any time. Just make sure there’s no gap in coverage. Some insurers even offer to pay your cancellation fee.

Myth: “Older drivers always pay more.”

Not true. While rates may rise slightly after 70, many insurers offer discounts for mature drivers with clean records.

Final Thoughts: Finding the Right Coverage at the Right Price

So, how much is car insurance in Texas? The answer depends on you—your driving habits, your vehicle, your location, and your coverage needs. While the average Texan pays around $2,000 per year for full coverage, smart shopping and smart choices can help you pay less.

Start by understanding your state’s requirements, then assess your personal risk factors. Compare quotes from multiple insurers, take advantage of discounts, and consider raising your deductible or improving your credit score. And don’t forget to re-evaluate your policy annually—your needs and rates can change.

Remember, the cheapest policy isn’t always the best. Focus on value: the right coverage at a fair price from a reputable company. With the right approach, you can drive confidently in Texas—knowing you’re protected without breaking the bank.

Frequently Asked Questions

How much is car insurance in Texas for a new driver?

New drivers, especially teens, pay significantly more—often $4,000 to $6,000 per year for full coverage. Rates drop as they gain experience and maintain a clean record.

Is car insurance required in Texas?

Yes. Texas law requires all drivers to carry at least 30/60/25 liability coverage. Driving without insurance can result in fines, license suspension, or vehicle impoundment.

Can I get car insurance with a bad driving record in Texas?

Yes, but it will cost more. High-risk drivers may need to use non-standard insurers or state-assigned risk pools, and premiums can be double the average.

Does my credit score affect my car insurance rate in Texas?

Yes. Insurers in Texas can use your credit-based insurance score to set rates. Better credit typically leads to lower premiums.

How often should I shop for car insurance in Texas?

It’s wise to compare quotes at least once a year, especially when your policy renews. Rates change, and new discounts may be available.

What happens if I drive without insurance in Texas?

Driving uninsured can lead to fines up to $350 for a first offense, license suspension, and vehicle registration hold. Repeat offenses carry steeper penalties.