How Much Is Car Insurance in Pennsylvania

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Average Car Insurance Costs in Pennsylvania

- 4 What Does Pennsylvania Law Require?

- 5 Factors That Affect Your Car Insurance Rate

- 6 How to Save Money on Car Insurance in Pennsylvania

- 7 Choosing the Right Insurance Company

- 8 Final Thoughts: Is Car Insurance in Pennsylvania Worth It?

- 9 Frequently Asked Questions

Car insurance in Pennsylvania costs an average of $1,400 to $2,200 per year for full coverage, but rates vary widely based on location, driving record, and coverage choices. Understanding state requirements and shopping around can help you find affordable, reliable protection.

If you’re driving in Pennsylvania, one of the first things you’ll need to budget for is car insurance. Whether you’re a new driver in Pittsburgh, a commuter in Philadelphia, or a weekend road-tripper through the Poconos, understanding how much car insurance costs in Pennsylvania can save you hundreds—or even thousands—of dollars over time.

Car insurance isn’t just a legal requirement in the Keystone State; it’s a financial safety net. Accidents happen, weather can be unpredictable, and not everyone on the road is insured. That’s why having the right coverage matters. But with so many factors influencing your premium—from your ZIP code to your credit score—it’s easy to feel overwhelmed.

The good news? Car insurance in Pennsylvania is generally more affordable than in many other states, especially when compared to national averages. However, “affordable” doesn’t mean “one-size-fits-all.” Your personal rate depends on a mix of variables, including your age, driving history, vehicle type, and even your marital status. In this guide, we’ll break down everything you need to know about how much car insurance costs in Pennsylvania, what’s required by law, and how to get the best deal without sacrificing protection.

Key Takeaways

- Average annual premiums: Full coverage costs around $1,800, while minimum liability averages $600–$900.

- State requirements: Pennsylvania mandates liability, PIP, and uninsured motorist coverage—no-fault rules apply.

- Location matters: Urban areas like Philadelphia and Pittsburgh have higher rates than rural counties.

- Credit and driving history: Poor credit or accidents can increase premiums by 20–50%.

- Discounts available: Safe driver, multi-policy, and good student discounts can lower costs significantly.

- Shop every 2–3 years: Comparing quotes regularly ensures you’re getting the best deal.

- Usage-based programs: Telematics apps like Progressive’s Snapshot can reward safe driving with savings.

📑 Table of Contents

Average Car Insurance Costs in Pennsylvania

When people ask, “How much is car insurance in Pennsylvania?” they’re usually looking for a ballpark figure. While exact numbers vary, most drivers pay between $1,400 and $2,200 per year for full coverage. That’s roughly $117 to $183 per month. For minimum liability coverage—just enough to meet state law—the average cost drops to around $600 to $900 annually, or $50 to $75 per month.

To put that in perspective, the national average for full coverage is about $1,780 per year, according to recent data from the National Association of Insurance Commissioners (NAIC). That means Pennsylvania drivers are paying slightly below average, which is a win for your wallet. But again, these are averages. Your actual rate could be higher or lower depending on your profile.

Let’s look at some real-world examples. A 35-year-old driver with a clean record, driving a 2020 Honda Accord in a suburban area like King of Prussia, might pay around $1,500 per year for full coverage. The same driver in downtown Philadelphia could see that number jump to $2,100 or more due to higher traffic density, theft rates, and accident frequency. On the flip side, a driver in a rural area like Clarion County might pay closer to $1,200 for the same coverage.

Full Coverage vs. Minimum Coverage

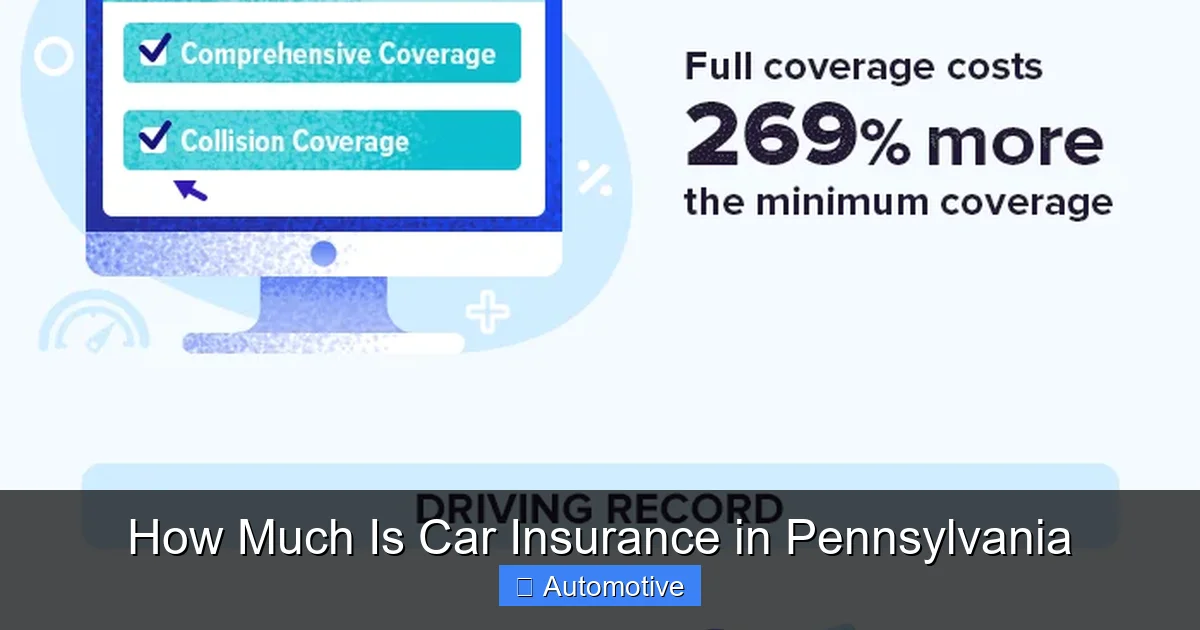

It’s important to understand the difference between full coverage and minimum coverage, as they serve very different purposes.

Minimum coverage in Pennsylvania includes three key components: bodily injury liability, property damage liability, and personal injury protection (PIP). We’ll dive deeper into these requirements later, but for now, know that minimum coverage only protects others—not your own vehicle. If you get into an accident, your insurer won’t pay to fix your car unless you have additional coverage like collision or comprehensive.

Full coverage, on the other hand, typically includes liability, PIP, uninsured motorist coverage, collision, and comprehensive. This broader protection means your insurer will help cover repairs to your vehicle after an accident, theft, vandalism, or even a tree falling on your car during a storm. Because it offers more protection, full coverage costs more—but for many drivers, especially those with newer or financed vehicles, it’s well worth the investment.

How Pennsylvania Compares to Neighboring States

If you’re considering a move or frequently drive across state lines, it’s helpful to know how Pennsylvania stacks up against nearby states. Here’s a quick comparison of average annual full coverage premiums:

– New York: ~$2,400

– New Jersey: ~$2,100

– Ohio: ~$1,300

– Maryland: ~$1,900

– West Virginia: ~$1,500

As you can see, Pennsylvania sits comfortably in the middle—more expensive than Ohio but significantly cheaper than New York or New Jersey. This makes it an attractive option for commuters and cross-border workers. However, keep in mind that insurance regulations differ by state, so your policy may not automatically transfer coverage if you move.

What Does Pennsylvania Law Require?

Visual guide about How Much Is Car Insurance in Pennsylvania

Image source: insurancepanda.com

Before we go any further, let’s talk about what you’re legally required to carry. Pennsylvania is a no-fault state, which means that after an accident, each driver’s own insurance pays for their medical expenses—regardless of who caused the crash. This system is designed to reduce lawsuits and speed up claims, but it also means your policy must include specific coverages.

Minimum Liability Coverage

Pennsylvania law requires all drivers to carry at least the following liability limits:

– $15,000 for bodily injury per person

– $30,000 for bodily injury per accident

– $5,000 for property damage per accident

These numbers might look low compared to other states, and that’s because they are. Many insurance experts recommend higher limits—like 100/300/100—to better protect your assets in case of a serious accident. If you cause a crash that results in $50,000 in medical bills, your $15,000 limit won’t cover it, and you could be personally liable for the difference.

Personal Injury Protection (PIP)

This is where Pennsylvania’s no-fault system comes into play. PIP covers medical expenses, lost wages, and other related costs for you and your passengers, up to your policy limit. The minimum PIP coverage is $5,000, but you can purchase up to $100,000. Higher limits are especially important if you don’t have robust health insurance.

One unique feature of Pennsylvania PIP is the choice between “limited” and “full” tort. With limited tort, you give up the right to sue for pain and suffering unless your injuries meet certain thresholds (like permanent disfigurement or significant loss of bodily function). In exchange, your insurance premiums are typically lower. Full tort gives you the right to sue, but costs more. Most drivers choose limited tort to save money.

Uninsured and Underinsured Motorist Coverage

Pennsylvania also requires uninsured motorist (UM) and underinsured motorist (UIM) coverage. These protect you if you’re hit by a driver who has no insurance or not enough to cover your damages. The minimum UM/UIM limits match your liability limits—so if you carry 15/30/5, your UM/UIM must be at least 15/30/5.

While this might seem redundant, it’s crucial. According to the Insurance Research Council, about 12% of Pennsylvania drivers are uninsured—higher than the national average of 12.6%, but still a significant risk. Without UM/UIM, you’d be left paying out of pocket if an uninsured driver totals your car.

Factors That Affect Your Car Insurance Rate

Visual guide about How Much Is Car Insurance in Pennsylvania

Image source: cdn.wallethub.com

Now that you know the basics, let’s explore what actually determines how much you’ll pay. Insurance companies use complex algorithms to assess risk, but the core factors are fairly consistent across providers.

Your Driving Record

This is one of the biggest influencers. A clean driving record with no accidents or tickets can qualify you for the lowest rates. But even one speeding ticket can increase your premium by 10–20%, while a DUI could double it. At-fault accidents are especially costly—expect a 30–50% hike, depending on severity.

For example, a driver with a clean record might pay $1,500 per year. After a single at-fault accident, that could jump to $2,250. And if you have multiple violations, insurers may classify you as a high-risk driver, which can limit your options and drive prices even higher.

Age and Experience

Young drivers, especially those under 25, pay significantly more than older, more experienced drivers. This is because statistics show that teens and young adults are more likely to be involved in accidents. A 17-year-old driver in Pennsylvania might pay $4,000 or more per year for full coverage, while a 45-year-old with a clean record could pay half that.

The good news? Rates tend to drop steadily after age 25 and stabilize around age 50. Married drivers also often receive discounts, as insurers view them as lower risk.

Location, Location, Location

Where you live plays a huge role in your premium. Urban areas like Philadelphia, Pittsburgh, and Allentown have higher rates due to traffic congestion, higher accident rates, and increased theft and vandalism. Rural areas, like parts of Lancaster or Erie County, tend to be cheaper.

Even within the same city, ZIP codes matter. A driver in a high-crime neighborhood might pay more than someone just a few miles away in a safer area. Insurers use geolocation data to assess risk, so your exact address can impact your rate.

Vehicle Type

The car you drive affects your insurance cost. Sports cars, luxury vehicles, and models with high theft rates typically cost more to insure. For example, insuring a Toyota Camry will be cheaper than insuring a BMW X5 or a Ford Mustang.

Safety features can help lower your rate. Vehicles with advanced driver assistance systems (ADAS) like automatic emergency braking, lane departure warnings, and adaptive cruise control may qualify for discounts. Similarly, cars with high safety ratings from the IIHS or NHTSA are often cheaper to insure.

Credit Score

In Pennsylvania, insurers can use your credit-based insurance score to determine your premium—unless you live in Philadelphia, where a 2022 law restricts this practice. Generally, drivers with excellent credit pay less than those with poor credit.

Why? Studies show a correlation between credit history and claim frequency. Someone with a low credit score is statistically more likely to file a claim. As a result, a driver with a 600 credit score might pay 20–30% more than someone with a 750 score, all else being equal.

Annual Mileage

The more you drive, the higher your risk of an accident. If you commute 50 miles each way to work, you’ll likely pay more than someone who only drives 5,000 miles per year. Some insurers offer low-mileage discounts, so if you work from home or use public transit, be sure to mention it.

How to Save Money on Car Insurance in Pennsylvania

Visual guide about How Much Is Car Insurance in Pennsylvania

Image source: res.cloudinary.com

Now that you know what affects your rate, let’s talk about how to lower it. The good news is there are several proven strategies to reduce your premium without cutting corners on coverage.

Shop Around and Compare Quotes

This is the single most effective way to save. Rates can vary by hundreds of dollars between insurers for the same coverage. Don’t just renew automatically—get quotes from at least three different companies every 2–3 years.

Start with major national carriers like State Farm, Geico, Progressive, and Allstate. Then check regional insurers like Erie Insurance or Donegal, which often offer competitive rates in Pennsylvania. Online comparison tools can help streamline the process, but don’t forget to call directly—sometimes agents can offer unadvertised discounts.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Common ones include:

– **Safe driver discount:** For maintaining a clean record

– **Multi-policy discount:** Bundling auto and home insurance

– **Good student discount:** For students with a B average or higher

– **Defensive driving course:** Completing an approved course can reduce your rate

– **Pay-in-full discount:** Paying your annual premium upfront

– **Low-mileage discount:** For driving fewer than 7,500 miles per year

– **Telematics program:** Using a usage-based app like Snapshot or Drivewise

For example, bundling your auto and home insurance with the same provider could save you 10–25%. A good student discount might knock $200 off your annual premium. These savings add up fast.

Raise Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Raising it from $500 to $1,000 can reduce your collision and comprehensive premiums by 15–30%. Just make sure you can afford the higher deductible if you need to file a claim.

Maintain a Good Credit Score

Since credit affects your rate in most of Pennsylvania, improving your credit can lead to lower premiums. Pay bills on time, keep credit card balances low, and check your credit report annually for errors.

Consider Usage-Based Insurance

Telematics programs track your driving habits—like speed, braking, and mileage—and reward safe behavior with discounts. Progressive’s Snapshot and State Farm’s Drive Safe & Save are popular options. Some drivers save up to 30% by participating.

Choosing the Right Insurance Company

With so many options, how do you pick the best insurer? It’s not just about price—customer service, claims handling, and financial stability matter too.

Top-Rated Insurers in Pennsylvania

Based on customer satisfaction, claims processing, and affordability, here are some of the top choices:

– **Erie Insurance:** Consistently ranks high for customer service and offers competitive rates, especially in rural areas.

– **State Farm:** Large agent network, strong financial strength, and good discounts for students and safe drivers.

– **Geico:** Known for low rates and a user-friendly online experience. Great for tech-savvy drivers.

– **Progressive:** Offers innovative tools like Name Your Price and Snapshot, plus competitive pricing.

– **Allstate:** Strong coverage options and accident forgiveness programs, though slightly higher premiums.

Reading reviews on sites like J.D. Power, Consumer Reports, or the Better Business Bureau can help you gauge real customer experiences.

Reading the Fine Print

Before signing up, read your policy carefully. Make sure you understand what’s covered, what’s excluded, and how claims are handled. Ask about add-ons like roadside assistance, rental car reimbursement, or gap insurance if you lease or finance your vehicle.

Final Thoughts: Is Car Insurance in Pennsylvania Worth It?

So, how much is car insurance in Pennsylvania? On average, between $1,400 and $2,200 per year for full coverage—slightly below the national average. But your personal rate depends on a mix of factors, from your driving history to your ZIP code.

The key is to balance affordability with adequate protection. Skimping on coverage to save a few dollars could leave you financially vulnerable in a serious accident. Instead, focus on smart strategies: shop around, take advantage of discounts, maintain a clean record, and choose a reputable insurer.

Remember, car insurance isn’t just a legal requirement—it’s peace of mind. Whether you’re cruising down the Pennsylvania Turnpike or navigating city streets, knowing you’re protected makes every drive safer and less stressful.

Frequently Asked Questions

What is the minimum car insurance required in Pennsylvania?

Pennsylvania requires liability coverage of 15/30/5, personal injury protection (PIP) of at least $5,000, and uninsured/underinsured motorist coverage matching your liability limits. These coverages are mandatory for all drivers.

Why is car insurance so expensive in Philadelphia?

Philadelphia has higher rates due to traffic density, accident frequency, theft, and vandalism. Urban areas generally pose more risk, leading insurers to charge higher premiums to offset potential claims.

Can I get car insurance with a bad driving record in Pennsylvania?

Yes, but it will cost more. High-risk drivers can still find coverage through standard insurers or specialty programs, though premiums may be significantly higher than average.

Does credit score affect car insurance rates in Pennsylvania?

Yes, in most of Pennsylvania, insurers use credit-based insurance scores to set rates. However, Philadelphia restricts this practice. Improving your credit can lead to lower premiums elsewhere in the state.

How often should I shop for car insurance quotes?

It’s wise to compare quotes every 2–3 years or after major life changes (like moving, getting married, or buying a new car). Rates change frequently, and you could save hundreds by switching.

Are there discounts for students in Pennsylvania?

Yes, many insurers offer good student discounts for drivers under 25 with a B average or higher. Some also provide discounts for completing a defensive driving course.