How Much Is Car Insurance in New York per Month?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance in New York per Month? A Complete Guide

- 4 What Is the Average Monthly Cost of Car Insurance in New York?

- 5 What Does New York Require for Car Insurance?

- 6 What Factors Influence Your Car Insurance Rate in New York?

- 7 How to Save Money on Car Insurance in New York

- 8 Common Misconceptions About Car Insurance in New York

- 9 Final Thoughts: Finding the Right Coverage for Your Budget

- 10 Frequently Asked Questions

Magnetic Car Phone Mount

Interior Cleaner Spray

Jack Stands

Car MP3 Player

Car insurance in New York costs an average of $150–$300 per month, but your rate depends on age, driving record, vehicle type, and coverage level. New York requires minimum liability coverage, and rates can vary widely by ZIP code and insurer.

Key Takeaways

- Average monthly cost: Most New York drivers pay between $150 and $300 per month for car insurance, with higher rates in urban areas like NYC.

- State minimum requirements: New York mandates liability, personal injury protection (PIP), and uninsured motorist coverage—no-fault insurance is required.

- Factors that affect rates: Age, driving history, credit score (in most cases), vehicle make/model, and location heavily influence your premium.

- High-risk drivers pay more: Drivers with accidents, tickets, or DUIs can see monthly premiums exceed $400.

- Shop around for savings: Comparing quotes from at least 3–5 insurers can save you hundreds per year.

- Discounts help reduce costs: Safe driver, multi-car, good student, and telematics programs can lower your monthly bill.

- Usage-based insurance is growing: Programs like Snapshot or Drivewise track driving behavior and reward safe habits with lower rates.

📑 Table of Contents

- How Much Is Car Insurance in New York per Month? A Complete Guide

- What Is the Average Monthly Cost of Car Insurance in New York?

- What Does New York Require for Car Insurance?

- What Factors Influence Your Car Insurance Rate in New York?

- How to Save Money on Car Insurance in New York

- Common Misconceptions About Car Insurance in New York

- Final Thoughts: Finding the Right Coverage for Your Budget

How Much Is Car Insurance in New York per Month? A Complete Guide

If you’re driving in New York, one of the first things you’ll need to budget for is car insurance. Whether you’re a new driver in Buffalo, a commuter in Long Island, or navigating the busy streets of Manhattan, understanding how much car insurance costs in New York per month is essential. The truth is, there’s no one-size-fits-all answer. Rates vary widely based on personal factors, location, and the type of coverage you choose.

On average, New York drivers pay between $150 and $300 per month for car insurance. That’s higher than the national average, which hovers around $120–$180 per month. But why the difference? New York is a densely populated state with high traffic volume, expensive repair costs, and strict insurance laws. These factors all contribute to higher premiums. Plus, New York operates under a no-fault insurance system, which means your own insurance covers your medical expenses after an accident—no matter who’s at fault. This added protection comes at a cost.

But don’t let the numbers scare you. With the right knowledge and a little effort, you can find affordable coverage that meets your needs. In this guide, we’ll break down everything you need to know about car insurance costs in New York, including what affects your rate, how to save money, and what coverage is legally required.

What Is the Average Monthly Cost of Car Insurance in New York?

Visual guide about How Much Is Car Insurance in New York per Month?

Image source: americaninsurance.com

Let’s start with the big question: how much is car insurance in New York per month? According to recent data from the National Association of Insurance Commissioners (NAIC) and consumer reports, the average monthly premium for full coverage in New York is around $250. For minimum coverage, the average drops to about $150 per month.

But averages only tell part of the story. Your actual cost could be much higher or lower depending on several key factors. For example, a 25-year-old male with a clean driving record living in upstate New York might pay $120 per month for minimum coverage. Meanwhile, a 19-year-old driver in Brooklyn with a speeding ticket could be looking at $400 or more.

Here’s a quick breakdown of average monthly premiums by coverage type in New York:

– Minimum liability coverage: $140–$180

– Full coverage (liability + collision + comprehensive): $220–$320

– High-risk drivers (accidents, DUIs): $350–$500+

Keep in mind that these are estimates. Your actual rate will depend on your insurer, driving history, and personal details.

How Location Affects Your Premium

Where you live in New York plays a huge role in your insurance cost. Urban areas like New York City, especially Manhattan and the Bronx, have the highest premiums due to traffic congestion, higher accident rates, and increased theft and vandalism. In contrast, rural areas like the Adirondacks or parts of upstate New York tend to have lower rates.

For example, drivers in ZIP codes like 10001 (Manhattan) might pay $300+ per month for full coverage, while someone in 12936 (Lake Placid) could pay closer to $180. Even within the same city, premiums can vary by neighborhood. Insurers use ZIP code data to assess risk, so moving just a few miles can sometimes make a noticeable difference in your rate.

Age and Driving Experience Matter

Young drivers, especially those under 25, face the highest insurance rates in New York. This is because statistics show that younger drivers are more likely to be involved in accidents. A 16-year-old driver might pay $400–$600 per month for minimum coverage, while a 35-year-old with a clean record could pay half that.

On the flip side, older drivers (65+) may also see slight increases in premiums, especially if they have health conditions that affect driving. However, many insurers offer discounts for mature drivers who complete defensive driving courses.

What Does New York Require for Car Insurance?

Visual guide about How Much Is Car Insurance in New York per Month?

Image source: image.typedream.com

Before we dive deeper into costs, it’s important to understand what coverage is legally required in New York. The state has strict minimum insurance requirements, and driving without it can result in fines, license suspension, or even vehicle impoundment.

New York is a no-fault state, which means your own insurance pays for your medical expenses after an accident, regardless of who caused it. This system is designed to reduce lawsuits and ensure quick medical payments.

Minimum Coverage Requirements

Here’s what you must carry to legally drive in New York:

– Bodily Injury Liability: $25,000 per person / $50,000 per accident

– Property Damage Liability: $10,000 per accident

– Personal Injury Protection (PIP): $50,000 per person

– Uninsured Motorist Bodily Injury: $25,000 per person / $50,000 per accident

These are the bare minimums. While they meet legal requirements, they may not provide enough protection in a serious accident. For example, medical bills can easily exceed $50,000, and property damage from a collision with a luxury car could far surpass $10,000.

Why Full Coverage Is Worth Considering

Many drivers opt for full coverage, which includes collision and comprehensive insurance. Collision covers damage to your car from accidents, while comprehensive covers non-collision events like theft, fire, or weather damage.

Full coverage is especially important if you drive a newer or more expensive vehicle. For instance, if you own a 2023 Honda Accord, replacing it after a total loss could cost $30,000 or more. Minimum coverage won’t help with that—only full coverage will.

The average cost for full coverage in New York is about $275 per month, but it can be worth the extra expense for peace of mind.

What Factors Influence Your Car Insurance Rate in New York?

Visual guide about How Much Is Car Insurance in New York per Month?

Image source: i.pinimg.com

Now that you know the basics, let’s explore the factors that determine how much you’ll actually pay. Insurance companies use complex algorithms to assess risk, and even small details can impact your premium.

Driving Record

Your driving history is one of the biggest factors. A clean record with no accidents or tickets will keep your rates low. But even one speeding ticket can increase your premium by 10–20%. A DUI conviction? That could double or even triple your rate.

For example, a driver with a DUI might pay $600 per month for full coverage, compared to $250 for someone with a clean record. Some insurers may even refuse to cover high-risk drivers, forcing them to seek coverage through the New York Automobile Insurance Plan (NYAIP), which is more expensive.

Credit Score (in Most Cases)

In New York, insurers can use your credit-based insurance score to determine your rate—unless you’re a victim of domestic violence or have filed for bankruptcy in the past 24 months. Studies show that people with lower credit scores tend to file more claims, so insurers charge them more.

Improving your credit score from “fair” (600–649) to “good” (650–749) could save you $50–$100 per month. Paying bills on time, reducing credit card balances, and checking your credit report for errors are great ways to boost your score.

Vehicle Type and Usage

The car you drive affects your insurance cost. Sports cars, luxury vehicles, and models with high theft rates typically cost more to insure. For example, insuring a BMW M3 will be significantly more expensive than a Toyota Corolla.

How you use your car also matters. If you drive 20,000 miles a year for work, you’ll pay more than someone who only drives 5,000 miles for errands. Insurers consider high mileage a higher risk because more time on the road increases the chance of an accident.

Marital Status and Gender

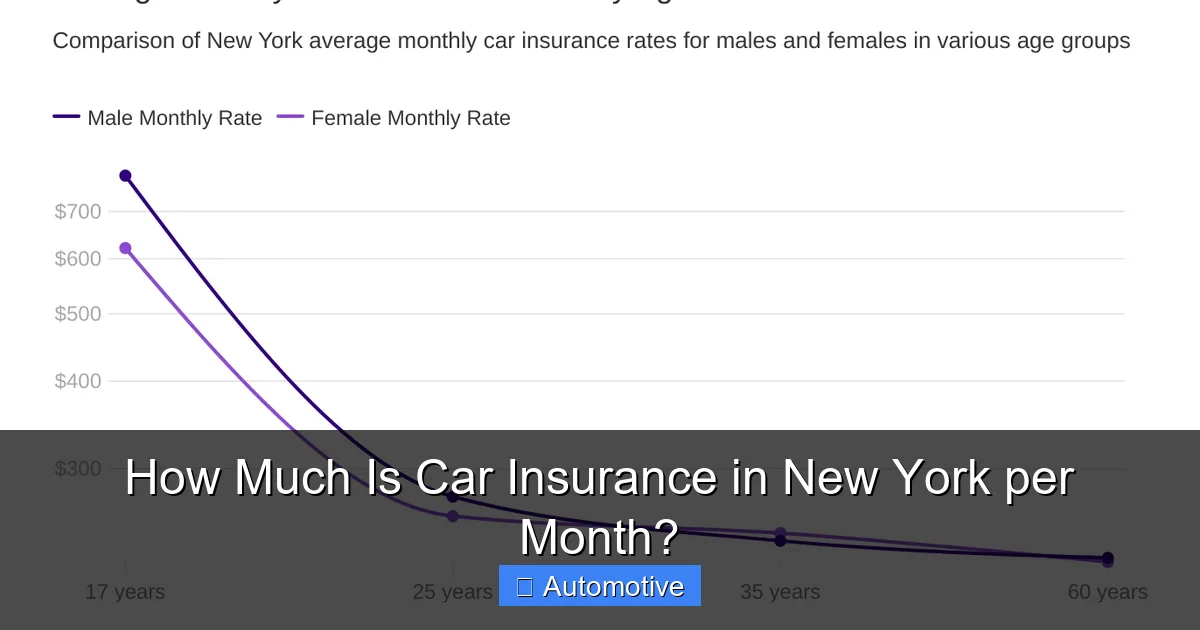

Believe it or not, marital status can affect your rate. Married drivers tend to have lower premiums because they’re statistically safer drivers. Gender also plays a role, especially for young drivers. Male drivers under 25 typically pay more than female drivers of the same age, though this gap narrows with age.

Discounts Can Lower Your Bill

The good news? There are many ways to reduce your premium. Most insurers offer discounts for:

– Safe driving (no accidents or tickets for 3+ years)

– Multi-car policies

– Bundling home and auto insurance

– Good student (for drivers under 25 with a B average or higher)

– Defensive driving course completion

– Low mileage

– Anti-theft devices

– Telematics programs (like Progressive’s Snapshot or Allstate’s Drivewise)

For example, a good student discount might save you 10–25%, while a multi-car discount could reduce your bill by 15–20%. Combining several discounts can save you hundreds per year.

How to Save Money on Car Insurance in New York

Now that you know what affects your rate, let’s talk about how to save. With a little effort, you can lower your monthly premium without sacrificing coverage.

Shop Around and Compare Quotes

One of the best ways to save is to compare quotes from multiple insurers. Rates can vary by hundreds of dollars between companies for the same coverage. Use online comparison tools or work with an independent agent to get quotes from at least 3–5 insurers.

For example, you might find that Geico offers a $180 monthly rate for full coverage, while State Farm quotes $240. Over a year, that’s a $720 difference—just for doing a little research.

Raise Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Raising your deductible from $500 to $1,000 can lower your premium by 10–20%. Just make sure you have enough savings to cover the higher deductible if you need to file a claim.

Maintain a Clean Driving Record

This one’s simple: drive safely. Avoid speeding, distracted driving, and aggressive maneuvers. Many insurers offer accident forgiveness programs, but they’re not available to everyone. A clean record over time will lead to lower rates.

Consider Usage-Based Insurance

Telematics programs track your driving habits—like speed, braking, and mileage—using a smartphone app or a device plugged into your car. If you’re a safe driver, you could earn discounts of 10–30%.

For example, Allstate’s Drivewise program offers up to 25% off for safe driving. If your current premium is $250, that’s a $62.50 monthly savings.

Review Your Policy Annually

Your life changes—so should your insurance. Review your policy every year to make sure you’re not overpaying. Maybe you’ve paid off your car loan and no longer need collision coverage. Or perhaps you’ve moved to a safer neighborhood with lower rates.

Also, check for new discounts you might qualify for. Insurers often update their programs, and you could be missing out on savings.

Common Misconceptions About Car Insurance in New York

There are a lot of myths floating around about car insurance. Let’s clear up a few common ones.

“Red Cars Cost More to Insure”

Nope. The color of your car has no effect on your insurance rate. What matters is the make, model, year, and safety features. A red Honda Civic costs the same to insure as a blue one.

“Minimum Coverage Is Always Cheaper”

While minimum coverage has a lower premium, it may not be the best value. If you’re in a serious accident, the out-of-pocket costs could far exceed what you’d pay for full coverage. Think of insurance as protection, not just a legal requirement.

“Your Rate Will Drop Automatically After an Accident”

Not necessarily. Some insurers offer accident forgiveness, but it’s not guaranteed. And if you file multiple claims, your rate could go up even more. Always weigh the cost of repairs against your deductible before filing a claim.

“All Insurers Are the Same”

Far from it. Each company uses different formulas to calculate rates. One might reward safe driving more than another, or offer better discounts for students. That’s why shopping around is so important.

Final Thoughts: Finding the Right Coverage for Your Budget

So, how much is car insurance in New York per month? The answer depends on you. While the average is around $150–$300, your actual cost will be shaped by your driving habits, vehicle, location, and coverage choices.

The key is to balance affordability with protection. Don’t just go for the cheapest policy—make sure it covers your needs. And remember, insurance isn’t a one-time decision. Review your policy regularly, take advantage of discounts, and stay informed about changes in the market.

By understanding the factors that affect your rate and taking proactive steps to save, you can find quality car insurance in New York that fits your budget. Whether you’re a new driver or a seasoned commuter, the right coverage gives you peace of mind on the road.

Frequently Asked Questions

How much is car insurance in New York per month for a new driver?

New drivers in New York typically pay $300–$500 per month for full coverage due to lack of experience and higher risk. Minimum coverage may cost $200–$300. Rates drop significantly after a few years of safe driving.

Is car insurance cheaper in upstate New York?

Yes, car insurance is generally cheaper in upstate New York compared to New York City. Rural areas have lower traffic, fewer accidents, and less theft, resulting in lower premiums—often $50–$100 less per month.

Can I drive without car insurance in New York?

No. New York requires all drivers to carry minimum liability, PIP, and uninsured motorist coverage. Driving without insurance can result in fines, license suspension, and vehicle impoundment.

Do insurance companies check your credit in New York?

Yes, most insurers in New York use credit-based insurance scores to determine rates, unless you’re exempt due to domestic violence or recent bankruptcy. A higher credit score can lead to lower premiums.

How can I lower my car insurance premium in New York?

You can lower your premium by maintaining a clean driving record, raising your deductible, bundling policies, taking defensive driving courses, and using telematics programs. Always compare quotes from multiple insurers.

What happens if I’m in an accident and don’t have enough coverage?

If your coverage limits are too low, you may have to pay out of pocket for medical bills or property damage that exceeds your policy. This can lead to financial hardship, lawsuits, or wage garnishment.