How Much Is Car Insurance in New York

Car insurance in New York averages $2,800 per year for full coverage, but rates vary widely based on location, age, driving history, and coverage choices. Urban drivers in NYC often pay more than those upstate, and understanding state requirements can help you find affordable, compliant coverage.

Key Takeaways

- Average cost: Full coverage car insurance in New York costs around $2,800 annually, while minimum liability coverage averages $1,400.

- Location matters: Drivers in New York City pay significantly more than those in rural areas like upstate New York due to traffic density and theft rates.

- State requirements: New York mandates no-fault insurance with minimum liability, personal injury protection (PIP), and uninsured motorist coverage.

- Factors affecting rates: Age, driving record, credit score (in most cases), vehicle type, and annual mileage all influence your premium.

- Discounts available: Safe driver, multi-policy, good student, and low-mileage discounts can reduce your monthly payments.

- Shopping around pays off: Comparing quotes from at least three insurers can save hundreds of dollars per year.

- Usage-based programs: Telematics programs like Snapshot or Drivewise monitor driving habits and may lower your rate for safe behavior.

📑 Table of Contents

How Much Is Car Insurance in New York? A Complete Guide

If you’re driving in New York, you’re not just navigating busy streets and unpredictable weather—you’re also dealing with some of the highest car insurance rates in the country. Whether you’re a lifelong New Yorker or just moved to the Empire State, understanding how much car insurance costs can feel overwhelming. But don’t worry—we’re here to break it down in simple terms.

Car insurance in New York isn’t one-size-fits-all. Your premium depends on a mix of personal factors, where you live, and the type of coverage you choose. On average, drivers pay around $2,800 per year for full coverage, which includes liability, collision, and comprehensive protection. If you’re only carrying the state-mandated minimum liability coverage, you might pay closer to $1,400 annually. But these are just averages—your actual rate could be higher or lower depending on your unique situation.

New York operates under a no-fault insurance system, which means your own insurance covers your medical expenses after an accident, regardless of who caused it. This system is designed to reduce lawsuits and speed up claims, but it also contributes to higher premiums. Add in the high cost of living, dense urban traffic, and frequent claims in cities like New York City, and it’s easy to see why insurance costs can add up quickly.

But here’s the good news: you have control over many of the factors that influence your rate. By understanding what insurers look at and how to shop smart, you can find affordable coverage that meets your needs and keeps you legal on the road.

New York Car Insurance Requirements

Visual guide about How Much Is Car Insurance in New York

Image source: americaninsurance.com

Before we dive into costs, it’s important to know what the state requires. New York has strict insurance laws, and driving without proper coverage can lead to fines, license suspension, or even vehicle impoundment.

Minimum Liability Coverage

New York mandates that all drivers carry at least the following liability coverage:

- $25,000 for bodily injury per person

- $50,000 for bodily injury per accident

- $10,000 for property damage per accident

This is often written as 25/50/10. Liability coverage pays for injuries and damages you cause to others in an accident. It does not cover your own injuries or vehicle damage.

Personal Injury Protection (PIP)

New York is a no-fault state, so every driver must carry Personal Injury Protection (PIP) coverage. The minimum PIP limit is $50,000 per person. This covers medical expenses, lost wages, and other out-of-pocket costs for you and your passengers, regardless of fault.

Uninsured Motorist Coverage

You’re also required to carry uninsured motorist (UM) coverage, with minimum limits matching your liability coverage: $25,000 per person and $50,000 per accident. This protects you if you’re hit by a driver who doesn’t have insurance or flees the scene.

Additional Coverage Options

While not required, many drivers choose to add:

- Collision coverage: Pays for damage to your car from a crash, regardless of fault.

- Comprehensive coverage: Covers non-collision incidents like theft, vandalism, fire, or weather damage.

- Gap insurance: Useful if you’re leasing or financing a car, covering the difference between what you owe and the car’s value if it’s totaled.

Adding these coverages increases your premium but offers greater financial protection.

Factors That Affect Car Insurance Rates in New York

Visual guide about How Much Is Car Insurance in New York

Image source: insurancepanda.com

Your car insurance premium isn’t set in stone—it’s calculated based on a variety of risk factors. Insurers use these to predict how likely you are to file a claim. Here’s what they consider:

Location

Where you live has a huge impact on your rate. New York City drivers, especially in boroughs like Brooklyn, Queens, and the Bronx, often pay 30–50% more than drivers in upstate areas like Albany or Buffalo. Why? Higher traffic density, more accidents, greater risk of theft and vandalism, and longer commutes all contribute to increased risk.

For example, a 35-year-old driver with a clean record might pay $2,200 per year in Rochester but over $3,500 in Manhattan for the same coverage.

Age and Driving Experience

Young drivers under 25 typically face the highest premiums due to their lack of experience and higher accident rates. A 19-year-old in New York might pay $4,000 or more annually for full coverage. Rates generally decrease as you gain experience, with the biggest drops happening after age 25.

On the flip side, seniors over 70 may see slight increases due to slower reaction times, though many insurers offer discounts for mature drivers with clean records.

Driving Record

Your history behind the wheel is one of the biggest factors. A clean record with no accidents or tickets can qualify you for safe driver discounts. But even one speeding ticket can increase your rate by 10–20%, and a DUI can double or even triple your premium.

For instance, a driver with a recent at-fault accident might see their annual premium jump from $2,500 to $3,200 or more.

Credit Score

In most of New York, insurers can use your credit-based insurance score to determine your rate. Drivers with excellent credit often pay significantly less than those with poor credit. However, New York City has restrictions on how much weight insurers can give to credit scores, which helps keep rates more balanced for city drivers.

Still, maintaining good credit can save you hundreds of dollars a year across the state.

Vehicle Type

The car you drive affects your premium. High-performance vehicles, luxury cars, and models with high theft rates (like certain Honda and Toyota models) cost more to insure. Safety features like anti-lock brakes, airbags, and anti-theft systems can lower your rate.

For example, insuring a Toyota Camry will be cheaper than insuring a BMW 3 Series or a Dodge Charger.

Annual Mileage

The more you drive, the higher your risk of an accident. If you commute 30 miles each way in NYC traffic, your rate will likely be higher than someone who drives 5,000 miles a year for weekend trips.

Some insurers offer low-mileage discounts for drivers who put fewer than 7,500 miles on their car annually.

Coverage Level and Deductible

Choosing higher coverage limits and lower deductibles increases your premium. For example, raising your liability from 25/50/10 to 100/300/100 will cost more but offers better protection. Similarly, lowering your collision deductible from $1,000 to $500 adds to your monthly cost.

Conversely, raising your deductible can lower your premium—just make sure you can afford to pay it out of pocket if you need to file a claim.

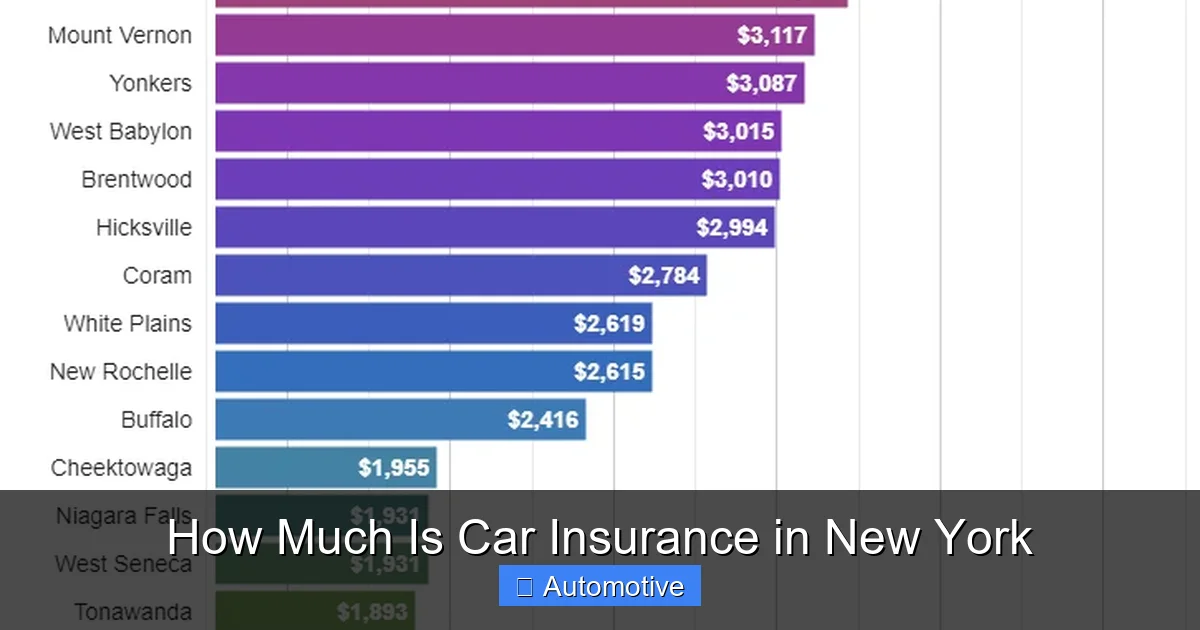

Average Car Insurance Costs by City and Region

Visual guide about How Much Is Car Insurance in New York

Image source: quoteinspector.com

Let’s look at how location impacts your wallet. Here’s a breakdown of average annual premiums for full coverage in key New York areas:

New York City (Manhattan, Brooklyn, Queens, Bronx, Staten Island)

- Average cost: $3,200–$4,000 per year

- Why so high? High population density, frequent accidents, traffic congestion, and elevated theft and vandalism rates.

- Tip: Consider parking in a secure garage and installing anti-theft devices to lower your rate.

Buffalo

- Average cost: $2,100–$2,600 per year

- Why lower? Less traffic, lower crime rates, and fewer claims compared to NYC.

- Tip: Take advantage of regional discounts and bundle home and auto policies.

Rochester

- Average cost: $2,000–$2,500 per year

- Why affordable? Moderate traffic, lower accident frequency, and competitive insurance market.

- Tip: Compare quotes from local insurers like Progressive and GEICO for the best deals.

Albany

- Average cost: $1,900–$2,400 per year

- Why cheaper? State capital with steady traffic but less congestion than NYC.

- Tip: Ask about government employee or alumni discounts if you work for the state or a local university.

Syracuse

- Average cost: $1,800–$2,300 per year

- Why low? Smaller city with fewer drivers and lower risk of accidents.

- Tip: Consider usage-based insurance if you drive infrequently.

These averages are based on a 35-year-old driver with a clean record, driving a mid-size sedan, and carrying full coverage. Your actual rate may vary.

How to Save Money on Car Insurance in New York

Paying high premiums doesn’t mean you’re stuck with them. With a few smart strategies, you can reduce your car insurance costs without sacrificing coverage.

Shop Around and Compare Quotes

Never accept your first quote. Prices can vary by hundreds of dollars between insurers for the same coverage. Use online comparison tools or work with an independent agent to get quotes from at least three companies.

For example, one insurer might offer $2,600 for full coverage, while another offers the same policy for $2,100. That’s a $500 savings just for comparing.

Take Advantage of Discounts

Most insurers offer a range of discounts. Common ones include:

- Safe driver discount: For maintaining a clean record for 3–5 years.

- Multi-policy discount: Save 10–25% by bundling auto and home insurance.

- Good student discount: For students with a B average or higher.

- Low-mileage discount: For driving fewer than 7,500 miles per year.

- Defensive driving course: Completing an approved course can reduce your rate by 10%.

- Anti-theft device discount: For vehicles equipped with alarms or tracking systems.

Ask your insurer about all available discounts—you might be missing out on savings.

Raise Your Deductible

Increasing your collision or comprehensive deductible from $500 to $1,000 can lower your premium by 15–30%. Just make sure you have enough savings to cover the higher out-of-pocket cost if you need to file a claim.

Maintain a Clean Driving Record

Avoiding accidents and tickets is one of the best ways to keep your rates low. Even a single speeding ticket can increase your premium for three years.

Consider enrolling in a defensive driving course to improve your skills and possibly earn a discount.

Improve Your Credit Score

In most of New York, a higher credit score can lead to lower insurance rates. Pay bills on time, reduce credit card balances, and check your credit report for errors.

Consider Usage-Based Insurance

Many insurers offer telematics programs that track your driving habits through a mobile app or device. If you drive safely—avoiding hard braking, speeding, and late-night trips—you could earn a discount of 10–20%.

Programs like Progressive’s Snapshot, Allstate’s Drivewise, and State Farm’s Drive Safe & Save are popular options.

Review Your Policy Annually

Your life changes—so should your insurance. Review your policy each year to ensure you’re not overpaying for coverage you don’t need. For example, if your car is older and has depreciated, you might drop collision coverage.

Top Car Insurance Companies in New York

Not all insurers are created equal. Some offer better rates, customer service, or discounts for New York drivers. Here are a few top performers:

GEICO

- Pros: Competitive rates, strong online tools, good customer service.

- Cons: Fewer local agents.

- Best for: Drivers looking for low rates and digital convenience.

State Farm

- Pros: Large agent network, excellent customer satisfaction, good discounts.

- Cons: Slightly higher rates in urban areas.

- Best for: Drivers who prefer in-person service and personalized support.

Progressive

- Pros: Name Your Price tool, strong usage-based programs, competitive pricing.

- Cons: Mixed customer service reviews.

- Best for: Tech-savvy drivers and those wanting flexible payment options.

Allstate

- Pros: Strong local presence, good discounts, accident forgiveness.

- Frequently Asked Questions

What is How Much Is Car Insurance in New York?

How Much Is Car Insurance in New York is an important topic with many practical applications.