How Much Is Car Insurance in Georgia?

Car insurance in Georgia costs an average of $1,800 to $2,500 per year for full coverage, but prices vary widely based on age, location, driving record, and credit score. This guide breaks down the real costs, factors affecting premiums, and smart ways to save.

If you’re driving in Georgia, you’ve probably asked yourself: *How much is car insurance in Georgia?* It’s a fair question—and one that doesn’t have a one-size-fits-all answer. Whether you’re a new driver in Savannah, a commuter in Atlanta, or a retiree cruising through Macon, your car insurance premium depends on a mix of personal factors, state laws, and even where you park your car at night.

Georgia is known for its Southern charm, peach orchards, and bustling highways—but it’s also one of the more expensive states for car insurance in the U.S. According to recent data from the National Association of Insurance Commissioners (NAIC), Georgia ranks among the top 15 states with the highest average auto insurance premiums. But why? And more importantly, what can you do about it?

In this guide, we’ll walk you through everything you need to know about car insurance costs in Georgia. From understanding state requirements to uncovering hidden discounts, we’ll help you make smart decisions that protect your wallet and keep you legal on the road. Whether you’re shopping for your first policy or looking to switch providers, this article will give you the clarity and confidence to find the best rate.

Key Takeaways

- Average annual premiums: Full coverage costs around $2,200/year; minimum liability averages $1,400/year.

- Location matters: Urban areas like Atlanta have higher rates due to traffic density and theft rates.

- Age and experience: Drivers under 25 pay significantly more, while safe drivers over 50 often see the lowest rates.

- Credit score impact: Georgia allows insurers to use credit-based insurance scores, which can raise or lower your premium.

- Required coverage: Georgia mandates liability, uninsured motorist, and PIP coverage—know the minimums to avoid fines.

- Discounts add up: Safe driver, multi-policy, good student, and low-mileage discounts can reduce costs by 10–30%.

- Shop every year: Rates change frequently—comparing quotes annually can save hundreds.

📑 Table of Contents

- What Does Car Insurance Cost in Georgia?

- Factors That Affect Your Car Insurance Rate in Georgia

- Georgia’s Minimum Car Insurance Requirements

- How to Save Money on Car Insurance in Georgia

- Frequently Asked Questions About Georgia Car Insurance

- Final Thoughts: Finding the Right Car Insurance in Georgia

What Does Car Insurance Cost in Georgia?

So, how much is car insurance in Georgia, really? Let’s cut to the chase: the average cost for full coverage auto insurance in Georgia is about $2,200 per year, or roughly $183 per month. For minimum liability coverage—the bare minimum required by law—the average drops to around $1,400 per year, or about $117 per month. But these are just averages. Your actual rate could be much higher or lower, depending on your unique situation.

To put this in perspective, Georgia’s average is slightly above the national average of $1,771 per year for full coverage. That might not sound like a huge difference, but over time, it adds up. For example, over five years, a Georgia driver could pay nearly $2,200 more than the national average—enough for a nice vacation or a significant car repair fund.

Why the higher cost? Several factors contribute. Georgia has a high rate of uninsured drivers—about 12.5%, according to the Insurance Research Council. That means more financial risk for insurers, which often gets passed on to policyholders. Additionally, the state has seen an increase in severe weather events, including hailstorms and tornadoes, which lead to more comprehensive claims.

But it’s not all bad news. Georgia also offers competitive insurance markets with dozens of providers, giving drivers plenty of options to shop around. And with the right strategy—like bundling policies or maintaining a clean driving record—you can still find affordable coverage that meets your needs.

Full Coverage vs. Minimum Liability: What’s the Difference?

When comparing car insurance costs, it’s important to understand the difference between full coverage and minimum liability. Minimum liability coverage is the least expensive option, but it also offers the least protection. In Georgia, this includes:

– $25,000 for bodily injury per person

– $50,000 for bodily injury per accident

– $25,000 for property damage

This coverage only pays for damage you cause to others—not for your own injuries or vehicle repairs. If you’re in a serious accident, these limits can be exhausted quickly, leaving you personally responsible for the rest.

Full coverage, on the other hand, includes liability plus collision and comprehensive insurance. Collision covers damage to your car from accidents, while comprehensive covers non-collision events like theft, vandalism, fire, or falling objects. Full coverage is typically required if you have a car loan or lease, and it’s highly recommended for newer or more valuable vehicles.

For example, let’s say you drive a 2022 Honda Accord valued at $28,000. If you only carry minimum liability and total your car in an accident, you’ll get nothing from your insurer for the vehicle itself. But with full coverage, you’d receive up to the car’s actual cash value (minus your deductible), helping you replace or repair it.

How Georgia Compares to Neighboring States

It’s helpful to see how Georgia stacks up against nearby states. Here’s a quick comparison of average annual full coverage premiums:

– Georgia: ~$2,200

– Florida: ~$2,700 (one of the highest in the nation)

– Alabama: ~$1,600

– Tennessee: ~$1,700

– South Carolina: ~$1,800

– North Carolina: ~$1,200 (lowest in the region)

As you can see, Georgia is on the higher end, especially compared to North Carolina, which has some of the lowest rates in the country due to strict regulation and a competitive market. Florida’s high costs are driven by no-fault laws, high litigation rates, and frequent hurricanes. Alabama and Tennessee offer more affordable options, partly due to lower population density and fewer uninsured drivers.

This comparison shows that where you live—even within a few hours’ drive—can make a big difference in your insurance bill. If you’re considering a move or frequently cross state lines, it’s worth checking how your premium might change.

Factors That Affect Your Car Insurance Rate in Georgia

Visual guide about How Much Is Car Insurance in Georgia?

Image source: carinsurance.org

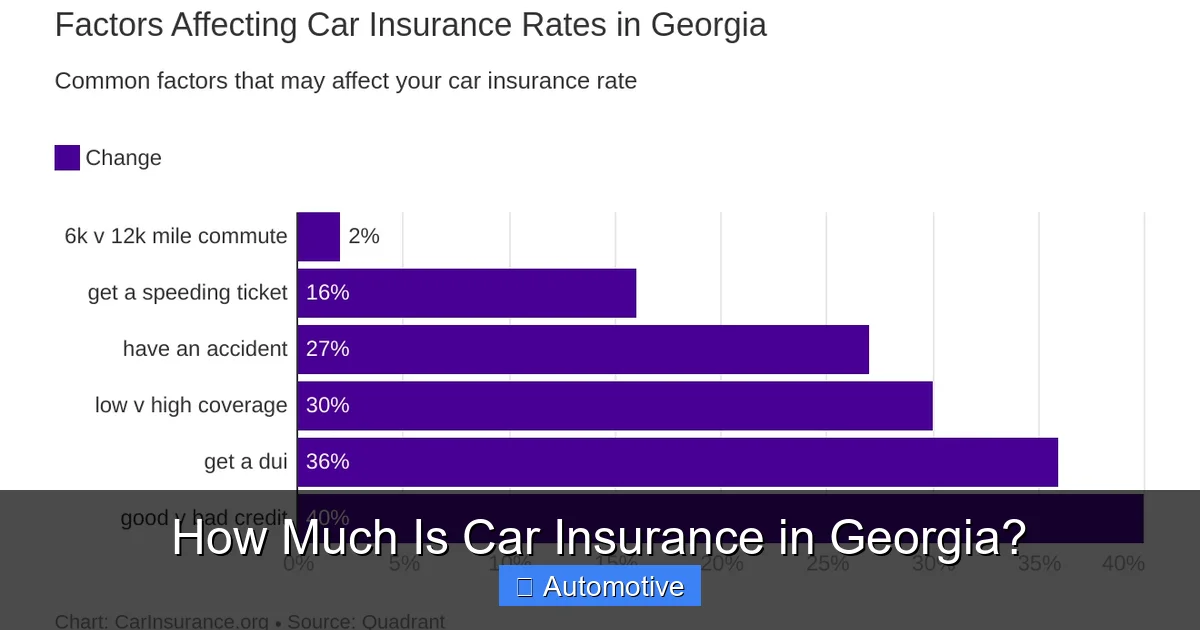

Now that you know the average cost, let’s dig into what actually determines how much you’ll pay. Car insurance companies in Georgia use a complex formula to calculate your premium, weighing dozens of factors. Some you can control, others you can’t—but understanding them all helps you make smarter choices.

1. Your Driving Record

Your driving history is one of the biggest factors in your rate. Insurers look at accidents, tickets, and DUIs over the past three to five years. A clean record can save you hundreds, while a single speeding ticket might increase your premium by 10–20%. For example, a 35-year-old driver with a clean record in Atlanta might pay $1,600/year for full coverage. Add a speeding ticket, and that jumps to $1,900. A DUI? That could double your rate.

Georgia also uses a point system for traffic violations. Accumulating too many points can lead to license suspension and higher insurance costs. The good news? You can reduce points by taking a defensive driving course, which many insurers also recognize with discounts.

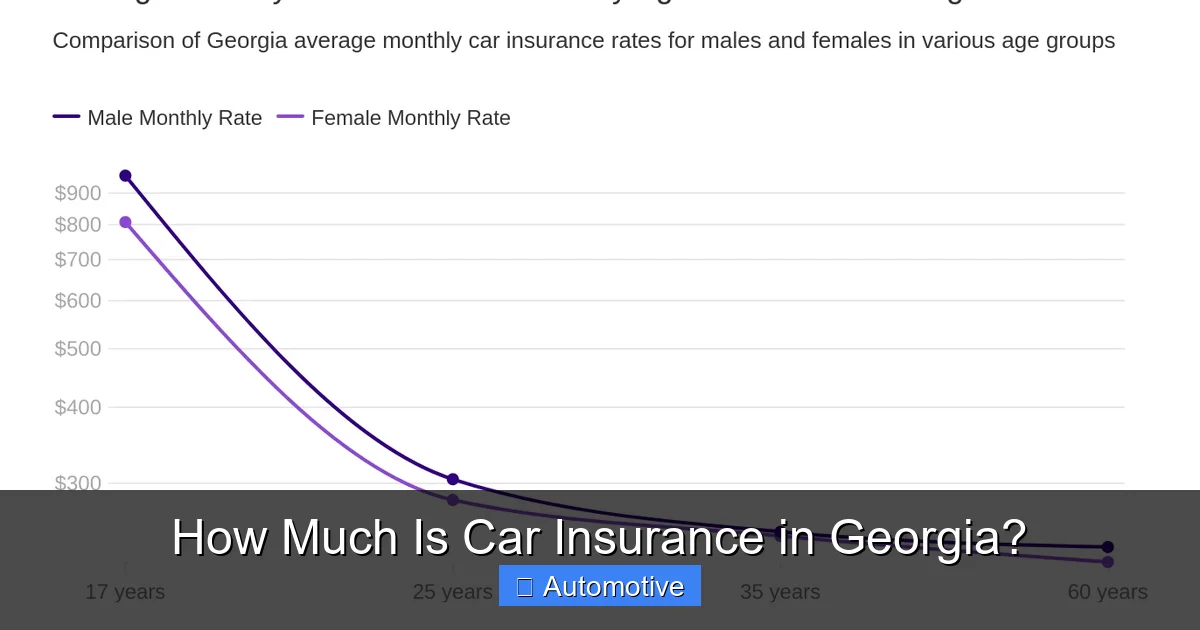

2. Age and Gender

Young drivers, especially those under 25, pay the highest rates. Why? Statistics show that teens and young adults are more likely to be involved in accidents. A 17-year-old male in Georgia might pay over $5,000/year for full coverage, while a 45-year-old female with the same car and record could pay less than $1,500.

Gender also plays a role, though it’s less significant than it used to be. Historically, young male drivers paid more due to higher accident rates, but the gap has narrowed in recent years. Still, in Georgia, a 20-year-old male might pay 15–20% more than a female of the same age.

As you get older and gain experience, your rates typically drop—especially after age 25. The biggest savings often come between ages 50 and 70, when drivers are considered low-risk.

3. Location, Location, Location

Where you live in Georgia has a major impact on your premium. Urban areas like Atlanta, Marietta, and Roswell have higher rates due to traffic congestion, higher accident rates, and increased theft and vandalism. For example, a driver in downtown Atlanta might pay $2,500/year, while someone in rural Tift County pays $1,700.

Even within the same city, ZIP codes matter. Areas with higher crime rates or more uninsured drivers will see higher premiums. Insurers use geolocation data to assess risk, so your exact address can make a difference.

4. Credit Score

This one surprises many people, but in Georgia, insurers can use your credit-based insurance score to set rates. Studies show a correlation between credit history and claim frequency—people with lower credit scores tend to file more claims. As a result, a poor credit score can increase your premium by 20–50%.

For example, a driver with excellent credit (750+) might pay $1,800/year, while someone with fair credit (600–650) could pay $2,400. If you’re working on improving your credit, paying bills on time and reducing debt can eventually lower your insurance costs.

5. Vehicle Type

The car you drive affects your rate more than you might think. High-performance vehicles, luxury cars, and models with high theft rates cost more to insure. For instance, insuring a Tesla Model 3 might cost 20–30% more than a Toyota Camry due to expensive parts and repair costs.

Safety features can help offset this. Cars with advanced driver assistance systems (ADAS) like automatic emergency braking, lane departure warnings, and adaptive cruise control may qualify for discounts. Georgia insurers often offer up to 10% off for vehicles with these features.

6. Annual Mileage

The more you drive, the higher your risk of an accident. Insurers ask for your annual mileage, and driving fewer miles can lead to lower rates. If you work from home or have a short commute, you might qualify for a low-mileage discount.

For example, driving 5,000 miles/year instead of 15,000 could save you $100–$200 annually. Some insurers even offer pay-per-mile programs, where your premium is based on actual miles driven—great for occasional drivers.

Georgia’s Minimum Car Insurance Requirements

Visual guide about How Much Is Car Insurance in Georgia?

Image source: carinsurance.org

Before you shop for quotes, it’s crucial to understand what coverage Georgia requires by law. Driving without insurance can result in fines, license suspension, and even jail time in extreme cases.

Georgia mandates three types of coverage:

1. **Bodily Injury Liability (BI):** Covers medical expenses for others if you’re at fault in an accident. Minimum: $25,000 per person / $50,000 per accident.

2. **Property Damage Liability (PD):** Covers damage to another person’s property. Minimum: $25,000 per accident.

3. **Uninsured/Underinsured Motorist Coverage (UM/UIM):** Protects you if you’re hit by a driver with no insurance or insufficient coverage. Minimum: $25,000 per person / $50,000 per accident.

4. **Personal Injury Protection (PIP):** Covers your medical expenses and lost wages, regardless of fault. Minimum: $5,000.

These are the legal minimums, but they may not be enough. For example, a serious accident could easily exceed $25,000 in medical bills. Many financial advisors recommend increasing your liability limits to $100,000/$300,000 or higher, especially if you have assets to protect.

Optional Coverage You Should Consider

Beyond the basics, consider adding these optional coverages:

– **Collision Coverage:** Pays for damage to your car from accidents.

– **Comprehensive Coverage:** Covers non-collision events like theft, fire, or weather damage.

– **Rental Reimbursement:** Pays for a rental car while yours is being repaired.

– **Roadside Assistance:** Covers towing, jump-starts, and lockout services.

– **Gap Insurance:** If you have a loan or lease, this covers the difference between your car’s value and what you owe if it’s totaled.

For example, if you’re financing a $30,000 car and it’s totaled in an accident, your insurer might only pay $22,000 (its depreciated value). Gap insurance would cover the remaining $8,000.

How to Save Money on Car Insurance in Georgia

Visual guide about How Much Is Car Insurance in Georgia?

Image source: general.com

Now that you know the costs and requirements, let’s talk about saving money. The good news? There are plenty of ways to lower your premium without sacrificing coverage.

1. Shop Around and Compare Quotes

This is the #1 way to save. Rates vary widely between insurers, even for the same driver profile. For example, one company might quote $1,800/year, while another offers $1,400 for identical coverage. Get at least three quotes from different providers, including national carriers (like State Farm, Geico, Progressive) and regional companies (like Auto-Owners or Georgia Farm Bureau).

Use online comparison tools or work with an independent agent who can access multiple insurers. Don’t forget to check customer service ratings and claims satisfaction—cheapest isn’t always best.

2. Take Advantage of Discounts

Most insurers offer a range of discounts. Common ones in Georgia include:

– **Safe Driver Discount:** For maintaining a clean record.

– **Multi-Policy Discount:** Bundling auto and home or renters insurance.

– **Good Student Discount:** For students with a B average or higher.

– **Defensive Driving Course:** Completing an approved course can reduce your rate.

– **Low Mileage Discount:** For driving under a certain number of miles per year.

– **Anti-Theft Device Discount:** For vehicles with alarms or tracking systems.

– **Pay-in-Full Discount:** Paying your annual premium upfront instead of monthly.

Stacking discounts can save you 15–30%. For example, a safe driver with a multi-policy bundle and low mileage might pay $1,200 instead of $1,800.

3. Raise Your Deductible

Your deductible is what you pay out of pocket before insurance kicks in. Raising it from $500 to $1,000 can lower your premium by 10–20%. Just make sure you can afford the higher deductible if you need to file a claim.

4. Improve Your Credit Score

Since credit affects your rate, taking steps to boost your score can lead to lower premiums. Pay bills on time, reduce credit card balances, and check your credit report for errors. Even a 50-point increase can make a difference.

5. Drive Safely and Avoid Claims

A clean driving record is your best asset. Avoiding accidents and tickets keeps your rates low and may qualify you for accident forgiveness programs. Some insurers also offer telematics programs (like Progressive’s Snapshot or State Farm’s Drive Safe & Save), which monitor your driving habits and reward safe behavior with discounts.

Frequently Asked Questions About Georgia Car Insurance

Can I drive without insurance in Georgia?

No. Georgia law requires all drivers to carry minimum liability, uninsured motorist, and PIP coverage. Driving without insurance can result in fines up to $1,000, license suspension, and vehicle impoundment.

Do I need full coverage if I own my car outright?

Not legally, but it’s wise if your car is newer or valuable. Full coverage protects your investment and gives you peace of mind. If your car is over 10 years old and worth less than $3,000, minimum liability might suffice.

How often should I review my car insurance policy?

Review your policy at least once a year, or whenever your life changes—like moving, getting married, or buying a new car. This ensures you’re not overpaying and have adequate coverage.

Does my credit score really affect my insurance rate?

Yes. In Georgia, insurers use credit-based insurance scores to assess risk. A higher score typically means lower premiums, while a lower score can increase costs.

Can I get car insurance with a suspended license?

It’s difficult, but possible. Some insurers offer non-owner policies for drivers with suspended licenses, but rates are high and coverage is limited. You’ll need to reinstate your license to get standard coverage.

What happens if I’m hit by an uninsured driver in Georgia?

Your uninsured motorist coverage will kick in, covering medical expenses and lost wages up to your policy limits. If you don’t have UM coverage, you may have to sue the at-fault driver or pay out of pocket.

Final Thoughts: Finding the Right Car Insurance in Georgia

So, how much is car insurance in Georgia? The answer depends on you—your age, driving history, location, and choices. While the state’s average rates are higher than the national norm, smart shopping and smart driving can help you find affordable, reliable coverage.

Start by understanding your state’s requirements and assessing your personal risk. Then, compare quotes from multiple insurers, ask about discounts, and consider raising your deductible if it fits your budget. Don’t forget to review your policy annually and adjust as your life changes.

Remember, the cheapest policy isn’t always the best. Look for a balance of cost, coverage, and customer service. A little effort now can save you hundreds—or even thousands—over the life of your policy.

Whether you’re cruising down I-75 or exploring the backroads of North Georgia, having the right car insurance gives you confidence and protection. So take control of your coverage, drive safely, and enjoy the open road—with peace of mind.

Frequently Asked Questions

How much is car insurance in Georgia for a new driver?

New drivers, especially teens, pay the highest rates due to lack of experience. A 16-year-old in Georgia might pay $4,000–$6,000/year for full coverage. Adding them to a parent’s policy can reduce costs.

Does Georgia require PIP coverage?

Yes. Georgia mandates Personal Injury Protection (PIP) coverage of at least $5,000 to cover medical expenses and lost wages, regardless of who caused the accident.

Can I lower my rate if I move to a rural area?

Yes. Rural areas typically have lower premiums due to less traffic and crime. Moving from Atlanta to a small town could save you $300–$500/year.

Do electric cars cost more to insure in Georgia?

Often, yes. Electric vehicles like Teslas have higher repair costs and expensive parts, leading to higher premiums—sometimes 20–30% more than gas-powered cars.

Is it illegal to let my insurance lapse in Georgia?

Yes. Letting your policy lapse can result in fines, license suspension, and higher future rates. Georgia requires continuous coverage.

How do I file a car insurance claim in Georgia?

Contact your insurer immediately after an accident. Provide details, photos, and witness info. Most companies offer online or app-based claims for faster processing.