Can a 17-year-old Get Car Insurance in Their Name

Yes, a 17-year-old can get car insurance in their own name, but it’s rarely the most cost-effective or practical option. Most teens are better off being added to a parent’s policy, which offers lower rates and broader coverage. However, in certain situations—like owning a car outright or living independently—getting individual coverage may be necessary.

Key Takeaways

- Legal eligibility: In most U.S. states, a 17-year-old can legally purchase car insurance in their name once they have a valid driver’s license.

- Higher premiums: Teen drivers, especially males under 18, face significantly higher insurance rates due to lack of driving experience and statistical risk.

- Parental policies are cheaper: Adding a teen to a parent’s existing policy is almost always more affordable than a standalone plan.

- Ownership matters: If the teen owns the car outright (not co-signed by a parent), insurers may require them to be the primary policyholder.

- State laws vary: Some states have specific rules about who can be listed as a policyholder, so check local regulations.

- Discounts are available: Good student discounts, driver training credits, and telematics programs can help reduce costs for young drivers.

- Independent living exception: Teens who are legally emancipated or financially independent may need their own policy for compliance and protection.

📑 Table of Contents

Can a 17-Year-Old Legally Get Car Insurance in Their Name?

If you’re a 17-year-old who just got your driver’s license—or you’re a parent helping your teen navigate the world of driving—you might be wondering: *Can a 17-year-old actually get car insurance in their own name?* The short answer is yes, but the long answer involves a mix of legal allowances, financial realities, and practical considerations.

In most states across the U.S., there’s no law that explicitly prohibits a 17-year-old from purchasing their own car insurance policy. As long as the teen has a valid driver’s license and is legally allowed to enter into a contract (which varies slightly by state), they can technically apply for coverage. However, insurance companies often treat minors differently when it comes to policy ownership. Many insurers require a parent or guardian to co-sign or be listed as a responsible party on the policy, especially if the teen is still under 18.

That said, the ability to get insurance isn’t the same as the *wisdom* of doing so. While it’s legally possible, getting your own policy at 17 usually comes with steep premiums, limited options, and fewer discounts compared to being added to a family plan. So while the door is open, most experts recommend walking through it only when absolutely necessary.

Why Most 17-Year-Olds Shouldn’t Get Their Own Policy

Visual guide about Can a 17-year-old Get Car Insurance in Their Name

Image source: forbes.com

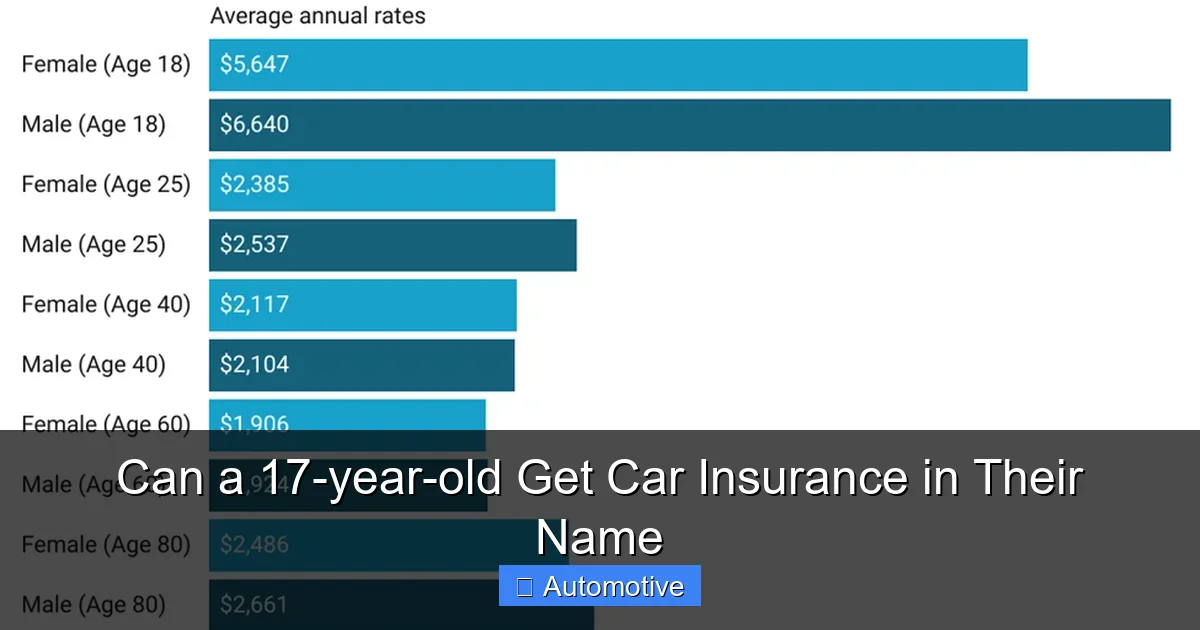

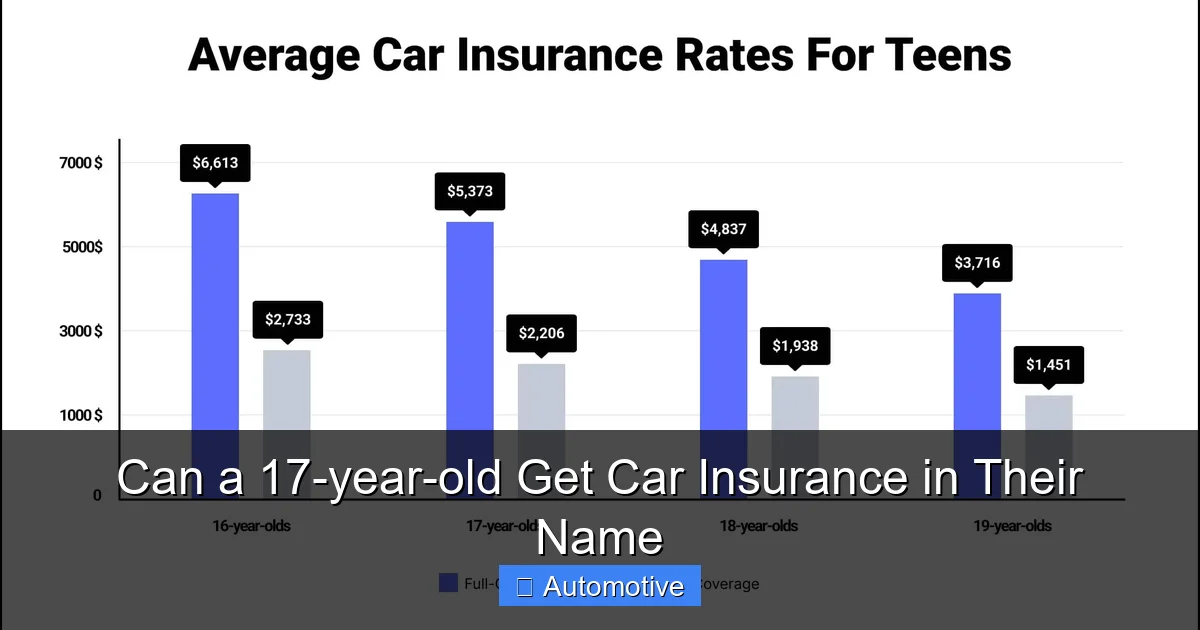

Let’s be real: car insurance for teens is expensive. According to the Insurance Information Institute, adding a 16- or 17-year-old to a parent’s policy can increase premiums by an average of 80% to 150%. That’s a huge jump—but even with that increase, it’s still almost always cheaper than buying a standalone policy for the teen.

Why? Because insurance companies base rates on risk. And statistically, teen drivers are among the highest-risk groups on the road. The Centers for Disease Control and Prevention (CDC) reports that drivers aged 16 to 19 are nearly three times more likely than drivers aged 20 and older to be in a fatal crash per mile driven. This elevated risk translates directly into higher premiums.

When a teen gets their own policy, they’re being rated as an individual with zero or minimal driving history. There’s no credit history (which some states use in pricing), no proven track record of safe driving, and often no discounts for multi-car or multi-policy bundles. All of this adds up to a very expensive monthly bill—often $300 to $600 or more per month for basic coverage.

In contrast, when a teen is added to a parent’s policy, the insurer considers the entire household’s risk profile. Parents typically have years of driving experience, established credit, and a history of claims (or lack thereof). This lowers the overall risk assessment, which helps keep premiums more manageable—even with a high-risk driver added.

Example: Standalone vs. Family Policy

Let’s say Maria, a 17-year-old in Texas, just bought her first car—a used 2015 Honda Civic. She wants to be independent and insists on having her own insurance policy.

– **Standalone policy:** After shopping around, Maria finds a basic liability-only policy for $450 per month. That’s $5,400 per year just for minimum coverage.

– **Added to parent’s policy:** Her parents’ current premium is $1,200 per year. Adding Maria increases it to $2,100 per year—an extra $900 annually, or $75 per month.

Even though Maria’s addition causes a 75% increase in her parents’ premium, she’s still paying far less than she would on her own. And she gets the benefit of being covered under a more comprehensive plan, often with higher liability limits and additional protections like uninsured motorist coverage.

This example shows why, in most cases, teens are better off being listed as a driver on a parent’s policy rather than trying to go it alone.

When Might a 17-Year-Old Need Their Own Insurance Policy?

Visual guide about Can a 17-year-old Get Car Insurance in Their Name

Image source: agilerates.com

While adding a teen to a parent’s policy is usually the best move, there are situations where a 17-year-old might need—or even be required—to get their own car insurance in their name.

1. The Teen Owns the Car Outright

If a 17-year-old purchases a car with their own money (perhaps from savings, a job, or a gift), and the title is solely in their name, insurers may require them to be the primary policyholder. This is because the person who owns the vehicle is typically responsible for insuring it.

For example, if Jake buys a used truck with money he earned working part-time, and the title lists only his name, the insurance company will likely insist that he be the named insured on the policy. In this case, his parents can still be listed as additional drivers or co-signers, but Jake would be the primary policyholder.

2. The Teen Lives Independently

If a 17-year-old is legally emancipated, married, or living away from home (such as in a college dorm or their own apartment), they may no longer be considered a dependent. In these cases, they might not qualify to be added to a parent’s policy, especially if they’re not listed as a resident at the same address.

Insurance companies require that all listed drivers live at the same household as the policyholder. If a teen moves out, even temporarily, they may need their own policy to maintain continuous coverage.

3. Parental Policy Excludes Teen Drivers

Some older or more restrictive insurance policies may exclude drivers under a certain age—especially if the parents have a history of claims or high-risk factors. In rare cases, an insurer might refuse to add a 17-year-old to an existing policy, forcing the teen to seek coverage elsewhere.

Additionally, if the parents’ policy has lapsed or been canceled, the teen may need to secure their own insurance to legally drive.

4. State-Specific Requirements

While most states allow minors to purchase insurance, a few have unique rules. For instance, in some states, a parent or guardian must be listed as a co-insured or sign the application on behalf of the minor. In others, the teen must be legally emancipated to enter into a binding contract.

It’s important to check with your state’s Department of Motor Vehicles (DMV) or insurance commissioner’s office to understand local regulations.

How to Get Car Insurance as a 17-Year-Old

Visual guide about Can a 17-year-old Get Car Insurance in Their Name

Image source: eireinsure.org

If you’ve determined that getting your own policy is the right choice, here’s how to go about it—step by step.

Step 1: Get Your Driver’s License

Before you can insure a car, you need a valid driver’s license. Most states allow teens to get a learner’s permit at 15 or 16 and a full license at 16 or 17, depending on completion of driver’s education and supervised driving hours.

Make sure your license is current and unrestricted. Some insurers may hesitate to cover drivers with provisional or restricted licenses, though it’s not impossible.

Step 2: Choose the Right Car

The type of car you drive has a big impact on insurance costs. Insurers consider factors like:

– **Safety ratings:** Cars with high crash-test scores and advanced safety features (like automatic emergency braking) are cheaper to insure.

– **Repair costs:** Luxury and sports cars cost more to repair, leading to higher premiums.

– **Theft rates:** Vehicles that are frequently stolen (like certain Honda or Toyota models) may have higher comprehensive coverage costs.

For a 17-year-old, a reliable, mid-size sedan like a Toyota Corolla, Honda Civic, or Ford Focus is usually the best bet. Avoid high-performance vehicles, large SUVs, or cars with turbocharged engines—they’ll spike your rates.

Step 3: Shop Around for Quotes

Don’t just go with the first quote you get. Insurance pricing varies widely between companies, even for the same driver and car. Get quotes from at least three to five insurers, including:

– National carriers (State Farm, Geico, Progressive, Allstate)

– Regional insurers (like Auto-Owners or Erie Insurance)

– Online-only companies (like Root or Lemonade)

Use online comparison tools or work with an independent insurance agent who can shop multiple companies for you.

When requesting quotes, be honest about your age, driving history, and intended use of the vehicle. Lying on an application can lead to denial of claims or policy cancellation.

Step 4: Consider Coverage Options

As a young driver, it’s tempting to go with the minimum required coverage to save money. But this can be a dangerous mistake.

Most states require liability insurance, which covers damage or injuries you cause to others. But it doesn’t cover your own car or medical expenses. For a 17-year-old, we recommend:

– **Higher liability limits:** Instead of the state minimum (e.g., 25/50/25), consider 100/300/100. This means $100,000 per person for bodily injury, $300,000 per accident, and $100,000 for property damage.

– **Comprehensive and collision:** These cover damage to your own car from accidents, theft, vandalism, or weather. If your car is worth more than $4,000, this is usually worth the cost.

– **Uninsured/underinsured motorist coverage:** Protects you if you’re hit by a driver with no or insufficient insurance.

– **Medical payments or PIP:** Covers medical bills for you and your passengers, regardless of fault.

Step 5: Look for Discounts

Even as a teen, you may qualify for discounts that can lower your premium. Common ones include:

– **Good student discount:** Maintain a B average or higher (usually requires a transcript).

– **Driver training discount:** Complete a state-approved driver’s education or defensive driving course.

– **Telematics programs:** Use a driving app or device (like Progressive’s Snapshot or Allstate’s Drivewise) to prove safe driving habits.

– **Low-mileage discount:** If you don’t drive often, you may qualify for a reduced rate.

– **Multi-policy discount:** If you have another type of insurance (like renters or life), bundling can save money.

Ask each insurer what discounts they offer and how to qualify.

Tips for Reducing Insurance Costs as a Young Driver

Even if you’re stuck with higher premiums, there are smart ways to keep costs down.

Stay on Your Parents’ Policy (If Possible)

This is the number one tip. As we’ve discussed, being added to a parent’s policy is almost always cheaper. Even if you own the car, you can often be listed as the primary driver while your parent remains the policyholder—just make sure the insurer knows the truth about who drives the car most.

Maintain Good Grades

Many insurers offer a good student discount for teens with a 3.0 GPA or higher. This can save 10% to 25% on your premium. Keep your grades up—it pays in more ways than one.

Take a Defensive Driving Course

Completing an approved course can not only make you a safer driver but also qualify you for a discount. Some states even reduce license restrictions after completing such a course.

Drive Safely

One speeding ticket or at-fault accident can double your insurance rate. Avoid distractions, follow speed limits, and never drive under the influence. Safe driving now builds a clean record that will help lower your rates in the future.

Consider a Usage-Based Insurance Plan

Telematics programs monitor your driving habits—like hard braking, rapid acceleration, and nighttime driving. If you drive safely, you can earn significant discounts. These programs are especially helpful for teens who want to prove they’re responsible drivers.

Review Your Policy Annually

As you gain more driving experience, your rates should gradually decrease. Review your policy each year and shop around to make sure you’re still getting the best deal. You might find a better rate with a different company.

The Bottom Line: Is It Worth It?

So, can a 17-year-old get car insurance in their name? Yes. Should they? Usually, no—unless there’s a compelling reason.

For most teens, the financial and practical benefits of being added to a parent’s policy far outweigh the desire for independence. You’ll pay less, get better coverage, and have the support of a more experienced driver on your side.

But if you own your car, live independently, or can’t be added to a family policy, getting your own insurance is not only possible—it’s necessary. Just be prepared for higher costs, and take advantage of every discount and safety program available.

Ultimately, the goal isn’t just to get insured—it’s to drive safely, responsibly, and affordably. Whether you’re on your own policy or your parents’, the habits you build now will shape your driving future for years to come.

Frequently Asked Questions

Can a 17-year-old legally buy car insurance in their own name?

Yes, in most U.S. states, a 17-year-old with a valid driver’s license can legally purchase car insurance in their name. However, some insurers may require a parent or guardian to co-sign the policy.

Is it cheaper for a 17-year-old to get their own policy or be added to a parent’s?

It’s almost always cheaper to be added to a parent’s policy. Standalone policies for teens are significantly more expensive due to high risk and lack of driving history.

What if the 17-year-old owns the car?

If the teen owns the car outright and the title is in their name, insurers may require them to be the primary policyholder, even if a parent helps with payments.

Do all insurance companies allow minors to have their own policies?

No. Some insurers have age restrictions or require a parent to be listed as a co-insured. It’s best to shop around and ask directly about their policies for minors.

Can a 17-year-old get full coverage insurance?

Yes, a 17-year-old can get full coverage (liability, collision, and comprehensive) in their name, but it will be more expensive than basic liability-only plans.

What discounts are available for teen drivers?

Common discounts include good student discounts, driver training credits, telematics programs, and low-mileage discounts. These can help reduce premiums significantly.