How Much Is Car Insurance in Texas

Car insurance in Texas costs more than the national average, with drivers paying around $1,800 to $2,500 per year. Rates vary based on location, driving record, age, and coverage level, but smart shopping and discounts can help you save.

If you live in Texas, you already know the state loves its cars. From long commutes on I-35 to weekend road trips through the Hill Country, driving is a way of life. But with that freedom comes responsibility—and one of the biggest responsibilities is car insurance. So, how much is car insurance in Texas? The short answer? It depends. But on average, Texas drivers pay more than most Americans for coverage.

Unlike some states with no-fault insurance laws, Texas follows a traditional “at-fault” system. That means if you cause an accident, your insurance pays for the other party’s damages. Because of this, insurers in Texas take on more financial risk, which can drive up premiums. Add in the state’s high traffic volume, urban congestion, and weather-related risks like hailstorms and flooding, and it’s easy to see why insurance costs are higher here.

But don’t let that scare you. With the right knowledge and a little effort, you can find affordable, reliable coverage that fits your budget and protects your wallet. In this guide, we’ll break down everything you need to know about car insurance costs in Texas—from average rates to what affects your premium and how to save money.

Key Takeaways

- Average annual cost: Texas drivers pay between $1,800 and $2,500 for full coverage, higher than the U.S. average.

- Minimum coverage is cheaper: State-minimum liability insurance costs around $700–$1,200 per year, but offers limited protection.

- Location matters: Urban areas like Houston and Dallas have higher rates due to traffic, theft, and accident risks.

- Your driving record impacts price: Accidents, tickets, and DUIs can increase premiums by 20% or more.

- Age and experience count: Young drivers under 25 often pay significantly more than older, experienced drivers.

- Shop around: Comparing quotes from at least three insurers can save you hundreds per year.

- Discounts help: Safe driver, multi-policy, and good student discounts can lower your bill.

📑 Table of Contents

What Is the Average Cost of Car Insurance in Texas?

When it comes to car insurance in Texas, the average cost is a moving target. But recent data gives us a solid ballpark. According to industry reports from 2023 and 2024, the average annual premium for full coverage car insurance in Texas is about $2,200. That’s roughly $183 per month. For minimum liability coverage—just the state-required basics—the average drops to around $900 per year, or about $75 per month.

To put that in perspective, the national average for full coverage is closer to $1,700 per year. So yes, Texas is on the higher end. But why? Several factors contribute, including population density, accident rates, and the state’s unique insurance regulations.

Let’s look at a real-world example. Imagine two drivers: Sarah, a 35-year-old with a clean record living in Austin, and Mike, a 22-year-old college student in Houston with a speeding ticket. Sarah might pay around $1,600 per year for full coverage, while Mike could be looking at $3,000 or more. That’s a big difference, and it shows how personal factors play a huge role.

It’s also worth noting that these averages include a mix of urban, suburban, and rural drivers. Rural areas like Lubbock or Amarillo tend to have lower rates due to less traffic and fewer claims. But in cities like Dallas, Houston, and San Antonio, where congestion and crime rates are higher, premiums climb.

Minimum vs. Full Coverage: What’s the Difference?

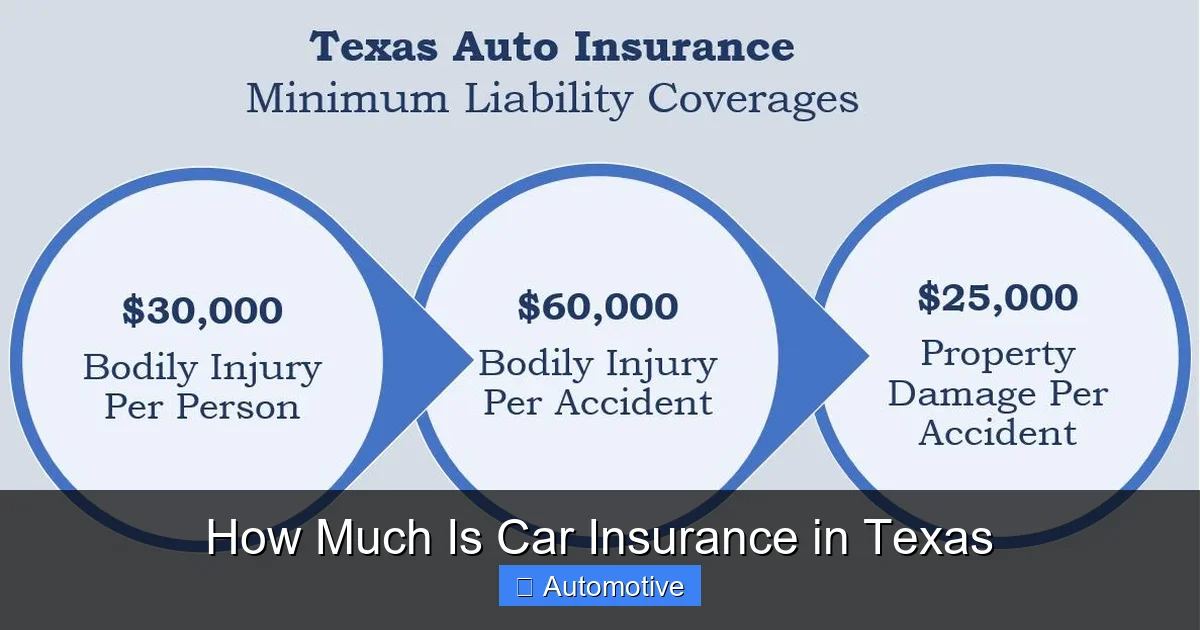

One of the biggest decisions you’ll make is whether to go with minimum coverage or full coverage. In Texas, the law requires all drivers to carry at least 30/60/25 liability insurance. That means:

– $30,000 for bodily injury per person

– $60,000 for bodily injury per accident

– $25,000 for property damage

This is the bare minimum, and it only covers damages you cause to others—not your own vehicle or medical bills. If you’re in a serious accident, $25,000 might not even cover the other driver’s car repairs, let alone medical costs.

Full coverage, on the other hand, includes liability plus collision and comprehensive insurance. Collision covers damage to your car from accidents, while comprehensive handles non-collision events like theft, vandalism, hail, or hitting a deer. Full coverage also often includes uninsured/underinsured motorist protection, which is crucial in Texas—nearly 15% of drivers are uninsured, one of the highest rates in the country.

Because full coverage offers much broader protection, it costs more. But for most drivers, especially those with newer or financed vehicles, it’s worth the investment. Lenders typically require full coverage if you have a car loan or lease.

How Texas Compares to Other States

So how does Texas stack up against other states? According to the National Association of Insurance Commissioners (NAIC), Texas ranks among the top 10 most expensive states for car insurance. States like Michigan, Louisiana, and Florida are even pricier, largely due to no-fault laws, high medical costs, or severe weather risks.

But compared to neighbors like Oklahoma ($1,400 average) or New Mexico ($1,500), Texas is noticeably more expensive. Even California, with its high population and strict regulations, has a lower average premium than Texas.

Why the difference? One reason is Texas’s large urban centers. Cities like Houston and Dallas have some of the highest traffic densities in the nation, leading to more accidents and claims. Additionally, Texas has a high rate of uninsured drivers, which increases costs for everyone else. Insurers pass some of that risk onto policyholders through higher premiums.

Factors That Affect Your Car Insurance Rate in Texas

Visual guide about How Much Is Car Insurance in Texas

Image source: a-abana.com

Now that you know the average cost, let’s dig into what actually determines your rate. Insurance companies use a complex formula based on risk. The higher the risk you pose, the more you’ll pay. Here are the biggest factors that influence how much you’ll pay for car insurance in Texas.

1. Your Driving Record

This is one of the most important factors. If you have a clean record—no accidents, tickets, or DUIs—you’ll likely get the best rates. But even one incident can spike your premium.

For example, a single at-fault accident can increase your rate by 20% to 40%. A speeding ticket might add 10% to 20%. And a DUI? That could double your premium or more. In Texas, a DUI stays on your record for up to 10 years, and insurers will see it every time you apply for coverage.

Let’s say you’re paying $1,800 per year with a clean record. After a DUI, that could jump to $3,600 or higher. That’s why safe driving isn’t just about safety—it’s also about saving money.

2. Age and Driving Experience

Young drivers, especially those under 25, pay significantly more for car insurance. Why? Statistics show that teens and young adults are more likely to be involved in accidents. Inexperience, risk-taking behavior, and distractions like phones all play a role.

A 16-year-old driver in Texas might pay $4,000 or more per year for full coverage. By age 25, that number typically drops by 30% to 50%, assuming a clean record. After 30, rates continue to decline slowly, with the lowest premiums often going to drivers in their 50s and 60s.

Gender also plays a role, though less so than in the past. Historically, young male drivers paid more than young females because of higher accident rates. But many insurers are moving away from gender-based pricing due to regulatory and social pressure.

3. Where You Live

Your ZIP code can have a huge impact on your premium. Urban areas like Houston, Dallas, San Antonio, and Austin have higher rates due to:

– More traffic and congestion

– Higher accident rates

– Increased risk of theft and vandalism

– Greater likelihood of severe weather (hail, flooding)

For example, a driver in downtown Houston might pay $2,800 per year, while someone in a rural town like Fredericksburg pays $1,400 for the same coverage. That’s a $1,400 difference just based on location.

Even within a city, rates can vary. Neighborhoods with higher crime rates or more traffic accidents will see higher premiums. Insurers use detailed geographic data to assess risk, so moving just a few miles can sometimes lower your rate.

4. Your Vehicle

The car you drive affects your insurance cost more than you might think. Insurers look at:

– Make and model

– Age of the vehicle

– Safety features

– Repair costs

– Theft rates

Sports cars, luxury vehicles, and high-performance models typically cost more to insure because they’re more expensive to repair and more likely to be involved in accidents. For example, insuring a BMW or a Dodge Charger will cost more than a Toyota Camry or Honda Civic.

Newer cars also tend to have higher premiums because they’re more valuable. But they may qualify for safety discounts if they have features like automatic emergency braking, lane departure warnings, or adaptive cruise control.

On the flip side, older cars may be cheaper to insure, but if they lack modern safety features, you might miss out on discounts. And if your car is very old, some insurers may not offer comprehensive coverage.

5. Your Credit Score

In Texas, insurers can use your credit-based insurance score to help determine your rate. This isn’t the same as your FICO score, but it’s based on similar factors: payment history, credit utilization, length of credit history, and types of credit.

Studies show that people with lower credit scores are more likely to file claims, so insurers charge them more. In Texas, a poor credit score can increase your premium by 50% or more compared to someone with excellent credit.

For example, a driver with a credit score of 600 might pay $2,500 per year, while someone with a 750 score pays $1,600 for the same coverage. That’s a $900 difference just based on credit.

If your credit isn’t great, don’t panic. You can improve it over time by paying bills on time, reducing debt, and checking your credit report for errors.

6. Coverage Level and Deductible

The more coverage you buy, the more you’ll pay. But you also have control over your deductible—the amount you pay out of pocket before insurance kicks in.

A higher deductible means lower premiums. For example, raising your collision deductible from $500 to $1,000 could save you $100 to $200 per year. But make sure you can afford to pay that amount if you need to file a claim.

Similarly, adding extras like roadside assistance, rental reimbursement, or gap insurance will increase your cost. Only add what you truly need.

How to Save Money on Car Insurance in Texas

Now that you know what drives up your premium, let’s talk about how to bring it down. The good news? There are plenty of ways to save on car insurance in Texas without sacrificing coverage.

Shop Around and Compare Quotes

This is the single most effective way to save. Insurance companies price risk differently, so the same driver can get wildly different quotes from different insurers.

For example, one company might offer you $1,800 per year, while another quotes $2,400 for the same coverage. That’s a $600 difference—just for doing a little research.

Experts recommend getting quotes from at least three to five insurers. You can do this online, through an independent agent, or by calling companies directly. Be sure to compare apples to apples—same coverage limits, deductibles, and discounts.

Some top insurers in Texas include State Farm, GEICO, Progressive, Allstate, and USAA (for military members and families). Each has strengths and weaknesses, so don’t assume the biggest name is the cheapest.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Here are some common ones in Texas:

– **Safe driver discount:** For maintaining a clean record over several years

– **Multi-policy discount:** Bundling auto and home or renters insurance

– **Good student discount:** For students with a B average or higher

– **Defensive driving course discount:** Completing an approved course (can also remove points from your license)

– **Low mileage discount:** Driving fewer than 7,500–10,000 miles per year

– **Anti-theft device discount:** For vehicles with alarms or tracking systems

– **Pay-in-full discount:** Paying your annual premium upfront instead of monthly

Some discounts can save you 10% to 25% or more. For example, a multi-policy discount might knock $300 off your annual premium. Over time, that adds up.

Improve Your Credit Score

Since credit affects your rate, improving your score can lead to lower premiums. Start by checking your credit report for free at AnnualCreditReport.com. Look for errors, like accounts you didn’t open or incorrect late payments, and dispute them.

Then, focus on paying bills on time, keeping credit card balances low, and avoiding new debt. Even a 50-point increase in your score can make a noticeable difference in your insurance rate.

Consider Usage-Based Insurance

Also known as telematics, usage-based insurance programs track your driving habits through a mobile app or device plugged into your car. Safe behaviors—like smooth braking, low speeds, and limited nighttime driving—can earn you discounts.

Programs like Progressive’s Snapshot, Allstate’s Drivewise, and State Farm’s Drive Safe & Save are popular in Texas. Some drivers save up to 30% with these programs.

Just be aware that if you drive aggressively or rack up a lot of miles, your rate could go up. So only enroll if you’re a safe, low-mileage driver.

Reassess Your Coverage Annually

Your insurance needs change over time. If you’ve paid off your car loan, you might not need collision coverage anymore—especially if your car is older and not worth much. Similarly, if your kids have moved out, you might not need as much liability coverage.

Review your policy every year during renewal. Ask yourself:

– Do I still need full coverage?

– Can I afford a higher deductible?

– Am I missing any discounts?

A quick check could save you hundreds.

Understanding Texas Car Insurance Laws

Before you sign up for a policy, it’s important to understand Texas’s insurance requirements. Driving without insurance is illegal and can result in fines, license suspension, and even vehicle impoundment.

Minimum Coverage Requirements

As mentioned earlier, Texas requires 30/60/25 liability coverage. But that’s the bare minimum. Many financial experts recommend higher limits—like 100/300/100—to protect your assets in case of a serious accident.

For example, if you cause an accident that results in $150,000 in medical bills, your 30/60 policy won’t cover it. You’d be personally responsible for the difference. Higher limits give you peace of mind.

Proof of Insurance

In Texas, you must carry proof of insurance in your vehicle at all times. This can be a physical card or a digital copy on your phone. Police officers can request it during traffic stops.

If you’re caught without insurance, penalties include:

– First offense: $175–$350 fine

– Second offense: Up to $1,000 fine, 2-year license suspension, and possible vehicle registration hold

– SR-22 requirement: You may need to file an SR-22 form (proof of financial responsibility) to reinstate your license

No-Fault vs. At-Fault

Texas is an at-fault state, meaning the driver responsible for the accident pays for damages. This is different from no-fault states, where each driver’s insurance covers their own injuries regardless of who caused the crash.

In Texas, you can sue the at-fault driver for additional damages if your injuries are severe. This system encourages careful driving but also means higher liability risks—and higher premiums.

Tips for First-Time Car Buyers in Texas

If you’re buying your first car in Texas, insurance should be part of your budget from day one. Here are some tips to help you get started:

– **Get quotes before you buy:** Insurance costs vary by vehicle, so compare models before making a decision.

– **Consider a used car:** Older, safer models are often cheaper to insure than new or high-performance vehicles.

– **Ask about discounts:** Many insurers offer good student, defensive driving, and low-mileage discounts for new drivers.

– **Start with higher coverage:** As a new driver, you’re at higher risk, so full coverage is wise—even if it costs more.

– **Stay on your parents’ policy:** If possible, stay on your parents’ policy as a listed driver. It’s usually cheaper than getting your own.

Final Thoughts: Is Car Insurance in Texas Worth It?

Yes—absolutely. While car insurance in Texas may cost more than in other states, it’s a necessary investment. Accidents happen, and without coverage, a single crash could wipe out your savings or even lead to lawsuits.

The key is to find the right balance between cost and protection. Don’t just go for the cheapest policy. Look for one that offers solid coverage, good customer service, and fair claims handling.

And remember: your rate isn’t set in stone. By driving safely, maintaining good credit, shopping around, and taking advantage of discounts, you can keep your premiums manageable.

So, how much is car insurance in Texas? On average, $1,800 to $2,500 per year for full coverage. But with the right approach, you can pay less—and drive with confidence.

Frequently Asked Questions

How much is car insurance in Texas per month?

On average, Texas drivers pay between $150 and $200 per month for full coverage car insurance. Minimum liability coverage costs around $60 to $100 per month.

Why is car insurance so expensive in Texas?

Car insurance is expensive in Texas due to high traffic density, urban congestion, a large number of uninsured drivers, and frequent weather-related claims like hail and flooding.

Can I drive without car insurance in Texas?

No, it’s illegal to drive without insurance in Texas. You must carry at least 30/60/25 liability coverage. Driving uninsured can result in fines, license suspension, and vehicle impoundment.

What is the cheapest car insurance in Texas?

The cheapest car insurance varies by driver, but GEICO, State Farm, and Progressive often offer competitive rates. Comparing quotes is the best way to find the lowest price.

Do I need full coverage in Texas?

Full coverage isn’t required by law, but it’s recommended—especially if you have a newer car, a loan, or lease. It protects your vehicle and offers broader financial protection.

How can I lower my car insurance in Texas?

You can lower your premium by shopping around, improving your credit score, taking a defensive driving course, raising your deductible, and asking about available discounts.