Do All States Require Car Insurance?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Do All States Require Car Insurance?

- 4 Understanding Financial Responsibility Laws

- 5 States That Require Car Insurance

- 6 Exceptions: States Without Mandatory Insurance

- 7 Penalties for Driving Without Insurance

- 8 Tips for Staying Compliant and Protected

- 9 Conclusion

- 10 Frequently Asked Questions

Most U.S. states require drivers to carry car insurance, but a few offer alternatives like cash deposits or self-insurance. Driving without required coverage can lead to fines, license suspension, or even vehicle impoundment.

Key Takeaways

- 48 states require liability car insurance: Only New Hampshire and Virginia do not mandate traditional auto insurance for all drivers under certain conditions.

- Financial responsibility laws apply everywhere: Even in states without mandatory insurance, drivers must prove they can cover damages in an accident.

- Virginia allows uninsured motorist fees: Drivers can pay a $500 annual fee to legally drive without insurance, but they remain personally liable for accidents.

- New Hampshire has unique rules: Insurance is only required if you cause an accident or are convicted of certain traffic violations.

- Minimum coverage varies by state: Each state sets its own liability limits, so what’s enough in one state may not be sufficient in another.

- Driving uninsured carries serious penalties: Fines, license suspension, vehicle registration revocation, and even jail time are possible in some cases.

- Non-owner policies exist for occasional drivers: If you don’t own a car but drive regularly, a non-owner policy can provide liability protection.

📑 Table of Contents

Do All States Require Car Insurance?

When you get behind the wheel, you’re not just responsible for your own safety—you’re also accountable for the safety of others on the road. That’s why nearly every state in the U.S. has laws requiring drivers to carry some form of financial protection in case they cause an accident. But here’s the twist: not all states require traditional car insurance. So, do all states require car insurance? The short answer is no—but almost all do, with a couple of notable exceptions and alternative options.

Most people assume that auto insurance is a universal requirement, and for good reason. In 48 states, having at least minimum liability coverage is the law. This insurance helps pay for injuries and property damage you might cause to others in a crash. It doesn’t cover your own vehicle, but it protects you from being personally sued for thousands—or even millions—of dollars in damages. However, two states, New Hampshire and Virginia, have different approaches. They don’t require every driver to carry standard auto insurance, but they do enforce strict financial responsibility laws. That means even if you don’t have an insurance policy, you must still prove you can pay for damages if you’re at fault in an accident.

Understanding these nuances is crucial, especially if you’re moving to a new state, renting a car, or lending your vehicle to a friend. The rules aren’t just bureaucratic red tape—they’re designed to protect everyone on the road and ensure that victims of accidents aren’t left footing the bill. In this article, we’ll break down the insurance requirements across the U.S., explore the exceptions, and explain what happens if you drive without coverage. Whether you’re a new driver or a seasoned road warrior, knowing your state’s laws can save you money, stress, and legal trouble down the line.

Understanding Financial Responsibility Laws

Visual guide about Do All States Require Car Insurance?

Image source: autostartransport.com

At the heart of every state’s approach to auto coverage is the concept of financial responsibility. Even in states that don’t mandate traditional car insurance, drivers must still demonstrate that they can cover the costs of an accident they cause. This principle ensures that if you hit someone’s car or injure a pedestrian, there’s a way to compensate the victim—whether through insurance, cash, or other approved methods.

Financial responsibility laws vary by state, but they generally require drivers to show proof of their ability to pay for bodily injury and property damage. In most cases, this is done by purchasing liability insurance that meets the state’s minimum coverage requirements. For example, California requires drivers to carry at least $15,000 for injury to one person, $30,000 for injury to multiple people, and $5,000 for property damage (often written as 15/30/5). Other states have higher or lower limits, but the idea is the same: you must be able to cover basic damages.

But what if you don’t want to buy insurance? Some states allow alternatives. You might be able to post a cash bond, deposit money with the state, or qualify as a self-insurer if you meet certain financial criteria. These options are rare and often impractical for the average driver, but they exist. For instance, in Arizona, you can avoid buying insurance if you deposit $40,000 with the state treasurer and maintain it for three years. That’s a steep price for most people, which is why the vast majority opt for traditional insurance instead.

The key takeaway? Even if your state doesn’t require car insurance, you’re still legally responsible for covering damages you cause. Failing to do so can result in severe penalties, including fines, license suspension, and even lawsuits. So while the term “financial responsibility” might sound dry, it’s really about accountability—and protecting both yourself and others on the road.

How Financial Responsibility Works in Practice

Let’s say you live in a state like New Hampshire, where insurance isn’t mandatory unless you’ve been in an accident or received certain traffic violations. If you cause a crash, you must immediately report it to the state and prove you can pay for the damages. If you can’t, the state may suspend your license until you do. This system puts the burden squarely on the driver, which is why many New Hampshire residents still choose to buy insurance—even though it’s not required.

In Virginia, the rules are slightly different. You can legally drive without insurance if you pay a $500 Uninsured Motor Vehicle (UMV) fee to the state. But here’s the catch: that fee doesn’t provide any coverage. If you cause an accident, you’re still on the hook for all medical bills, vehicle repairs, and other costs. That $500 might seem like a bargain compared to annual insurance premiums, but one serious accident could cost tens of thousands of dollars—far more than the fee.

These examples show that financial responsibility isn’t just a legal formality. It’s a real-world safeguard that ensures victims aren’t left with unpaid bills. And while some drivers may try to skirt the rules, the risks often outweigh the savings. That’s why most experts recommend carrying at least the minimum required insurance, even in states where it’s not mandatory.

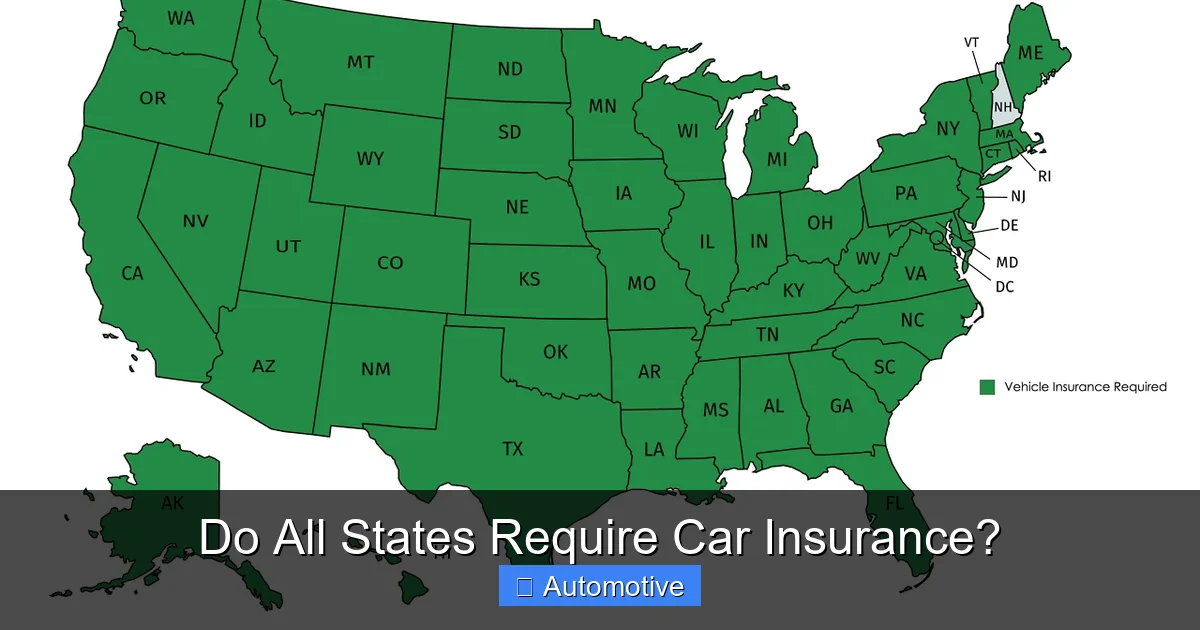

States That Require Car Insurance

Visual guide about Do All States Require Car Insurance?

Image source: 64.media.tumblr.com

The vast majority of U.S. states—48 out of 50—require drivers to carry at least minimum liability car insurance. These laws are designed to protect both drivers and the public by ensuring that anyone who causes an accident has the means to cover the resulting damages. The specifics of these requirements vary from state to state, but the core idea remains consistent: if you drive, you must have financial protection.

Liability insurance typically covers two main areas: bodily injury and property damage. Bodily injury coverage pays for medical expenses, lost wages, and pain and suffering for people injured in an accident you cause. Property damage coverage pays for repairs to other vehicles, buildings, fences, or other property damaged in the crash. Most states set minimum dollar amounts for each type of coverage, and drivers must carry policies that meet or exceed those limits.

For example, in Texas, drivers must carry at least $30,000 for bodily injury per person, $60,000 for bodily injury per accident, and $25,000 for property damage (written as 30/60/25). In contrast, Florida requires only $10,000 in property damage liability and $10,000 in personal injury protection (PIP), but no bodily injury liability—making it one of the few no-fault states with unique requirements. These differences highlight why it’s important to know your state’s specific rules, especially if you travel or move frequently.

Minimum Coverage Requirements by State

While we won’t list every state’s exact limits here (they change occasionally), it’s helpful to understand the range. Some states, like Maine and Alaska, have relatively high minimums—$50,000 for bodily injury per person and $100,000 per accident. Others, like California and New York, have lower minimums but higher population densities, which can increase the risk of costly accidents.

Most states fall somewhere in the middle, with minimums ranging from $15,000 to $30,000 for bodily injury per person and $5,000 to $25,000 for property damage. However, these minimums are often criticized as being too low to cover serious accidents. A single night in the hospital can easily exceed $50,000, and a totaled luxury car can cost even more. That’s why many financial advisors recommend carrying higher limits—or even umbrella policies—for added protection.

It’s also worth noting that some states require additional coverage beyond liability. For instance, Michigan requires unlimited personal injury protection (PIP), while New Jersey offers both standard and basic policies with different levels of coverage. These variations reflect each state’s approach to balancing affordability with protection.

Proof of Insurance and Enforcement

In states that require car insurance, drivers must carry proof of coverage at all times. This usually comes in the form of an insurance card provided by your insurer, which lists your policy number, effective dates, and coverage details. Police officers may ask to see this card during traffic stops, and failure to provide it can result in fines or other penalties.

Many states also use electronic verification systems to check whether a vehicle is insured. When you register your car or renew your registration, the Department of Motor Vehicles (DMV) may cross-reference your information with insurance databases. If your policy lapses or you cancel it without replacing it, the state can suspend your registration or even impound your vehicle.

Some states take enforcement a step further. In California, for example, first-time offenders caught driving without insurance face fines of up to $400 and possible license suspension. Repeat offenders may pay even more and could have their vehicle impounded. These strict measures are designed to encourage compliance and reduce the number of uninsured drivers on the road.

Exceptions: States Without Mandatory Insurance

Visual guide about Do All States Require Car Insurance?

Image source: slideteam.net

While most states require car insurance, two stand out as exceptions: New Hampshire and Virginia. These states don’t mandate traditional auto insurance for all drivers, but they do enforce financial responsibility laws that require drivers to cover damages if they cause an accident. Understanding how these states work is key to knowing whether you need insurance—and what your options are.

New Hampshire: The “Live Free or Die” Approach

New Hampshire is famous for its motto, “Live Free or Die,” and its approach to auto insurance reflects that independent spirit. The state does not require drivers to carry liability insurance—unless they’ve been involved in an accident, received a DUI, or been convicted of certain traffic violations. In those cases, the state may require you to file an SR-22 form, which proves you have insurance, and maintain it for a set period.

If you’re a safe driver with a clean record, you can legally drive in New Hampshire without insurance. However, if you cause an accident, you must immediately report it to the state and prove you can pay for the damages. If you can’t, your license may be suspended until you do. This system puts the onus on the driver to be financially prepared, which is why many New Hampshire residents still choose to buy insurance—even though it’s not required.

One practical tip: if you’re moving to New Hampshire from another state, your current insurance policy may still be valid, but it’s wise to check with your insurer and the DMV. Some insurers may not offer policies in New Hampshire due to the unique regulations, so you might need to shop around.

Virginia: The $500 Uninsured Motorist Fee

Virginia offers a unique alternative to traditional insurance: the Uninsured Motor Vehicle (UMV) fee. Drivers can pay $500 annually to the state and legally drive without insurance. This fee is not insurance—it doesn’t provide any coverage. Instead, it’s a way to comply with the state’s financial responsibility law without buying a policy.

The catch? If you cause an accident, you’re still personally liable for all damages. That means you could be sued for medical bills, vehicle repairs, lost wages, and pain and suffering. For many drivers, the risk of a single serious accident far outweighs the $500 savings. That’s why most Virginians choose to buy insurance anyway.

It’s also important to note that the UMV fee doesn’t protect you if you’re injured in an accident caused by someone else. Without uninsured motorist coverage, you may have to rely on your own health insurance or pay out of pocket. This can be a significant financial burden, especially if you don’t have robust health coverage.

Other Alternatives to Traditional Insurance

In a few other states, drivers may qualify for alternatives to standard insurance. For example, in Arizona, you can avoid buying insurance if you deposit $40,000 with the state treasurer and maintain it for three years. In Oklahoma, self-insurers—typically large companies or government entities—can be exempt from buying policies if they meet certain financial criteria.

These options are rare and often impractical for individual drivers. Most people don’t have $40,000 to lock away for years, and self-insurance requires significant assets and administrative effort. As a result, the vast majority of drivers opt for traditional insurance, even in states where it’s not strictly required.

Penalties for Driving Without Insurance

Driving without required car insurance is a serious offense in most states, and the penalties can be severe. These consequences are designed to deter uninsured driving and protect other road users from financial harm. Whether you’re caught during a traffic stop, involved in an accident, or simply let your policy lapse, the fallout can affect your wallet, your driving privileges, and even your freedom.

Common Penalties Across States

The most common penalty for driving without insurance is a fine. These can range from $100 to over $1,000, depending on the state and whether it’s a first or repeat offense. For example, in Texas, first-time offenders face fines of up to $350, while repeat offenders can pay up to $1,000. In New York, fines start at $150 and can go up to $1,500 for subsequent violations.

In addition to fines, many states suspend your driver’s license and vehicle registration. In California, a first offense results in a 30-day license suspension and a $100 reinstatement fee. In Florida, uninsured drivers may face a four-month license suspension and a $500 fine. Some states also require you to file an SR-22 form—a certificate of financial responsibility—after a suspension, which can increase your insurance costs for years.

Vehicle Impoundment and Jail Time

In extreme cases, driving without insurance can lead to vehicle impoundment or even jail time. In Arizona, for instance, a third offense can result in a 30-day jail sentence and a $750 fine. In Illinois, repeat offenders may face up to six months in jail. These harsh penalties underscore the seriousness of the offense and the state’s commitment to road safety.

Even if you avoid jail, the financial impact can be devastating. If you cause an accident while uninsured, you may be sued for damages that exceed your ability to pay. This can lead to wage garnishment, liens on your property, or even bankruptcy. And if you’re injured in an accident caused by an uninsured driver, you may have limited options for compensation—especially if you don’t have uninsured motorist coverage.

How to Reinstate Your Driving Privileges

If your license or registration is suspended due to lack of insurance, you’ll need to take specific steps to get back on the road. This usually involves paying all fines, reinstating your registration, and providing proof of insurance. In some states, you may also need to file an SR-22 form and maintain it for one to three years.

It’s important to act quickly. The longer your license is suspended, the harder it may be to find affordable insurance—and the more you’ll pay when you do. Some insurers specialize in high-risk drivers, but their rates can be significantly higher than standard policies.

Tips for Staying Compliant and Protected

Staying compliant with your state’s insurance requirements doesn’t have to be complicated—but it does require attention and planning. Whether you’re a new driver or a seasoned pro, a few smart habits can help you avoid legal trouble and ensure you’re protected on the road.

Know Your State’s Requirements

The first step is understanding what your state requires. Visit your state’s DMV website or contact them directly to find the minimum coverage limits and any additional requirements. If you’re unsure, ask your insurance agent—they should be familiar with local laws and can help you choose the right policy.

Keep in mind that requirements can change. Some states periodically update their minimums to reflect inflation or rising medical costs. Staying informed ensures you’re always compliant.

Carry Proof of Insurance

Always keep your insurance card in your vehicle. Most insurers provide a physical card, but many also offer digital versions through their apps. Make sure your card is up to date and clearly displays your policy number, effective dates, and coverage details.

If you’re pulled over, having proof of insurance can prevent unnecessary fines or delays. It also helps first responders and other drivers in the event of an accident.

Consider Higher Coverage Limits

While minimum coverage keeps you legal, it may not protect you financially. Consider increasing your liability limits or adding optional coverages like uninsured motorist protection, collision, and comprehensive. These can provide peace of mind and protect your assets in case of a serious accident.

For example, if you own a home or have savings, higher liability limits can shield you from lawsuits. And if you drive an older car, comprehensive coverage can help pay for theft, vandalism, or weather damage.

Review Your Policy Regularly

Life changes—and so should your insurance. Review your policy annually or after major life events like buying a new car, moving, or getting married. Make sure your coverage still meets your needs and complies with state laws.

If you’re unsure, schedule a consultation with your agent. They can help you adjust your policy and find discounts you may qualify for, such as safe driver or multi-car discounts.

Use Technology to Stay on Track

Many insurers offer tools to help you manage your policy, pay bills, and track your coverage. Use these resources to set reminders for renewals, monitor your driving habits, and receive alerts if your policy is about to lapse.

Some states also offer online portals where you can verify your insurance status or report changes. Taking advantage of these tools can help you stay compliant with minimal effort.

Conclusion

So, do all states require car insurance? The answer is almost—but not quite. While 48 states mandate liability insurance, New Hampshire and Virginia offer alternatives that allow some drivers to go without traditional coverage. However, even in these states, financial responsibility laws ensure that drivers can cover damages if they cause an accident.

The bottom line? Driving without insurance—whether required or not—is a risky move. The potential penalties, from fines and license suspension to lawsuits and jail time, far outweigh the savings. And in the event of an accident, being uninsured can leave you financially vulnerable.

For most drivers, the smart choice is to carry at least the minimum required insurance—and ideally more. It’s not just about following the law; it’s about protecting yourself, your passengers, and everyone else on the road. By understanding your state’s requirements, staying informed, and choosing the right coverage, you can drive with confidence and peace of mind.

Frequently Asked Questions

Is car insurance required in all 50 states?

No, car insurance is not required in all 50 states. Only New Hampshire and Virginia do not mandate traditional auto insurance for all drivers, though both enforce financial responsibility laws.

What happens if I drive without insurance in a state that requires it?

Driving without insurance can result in fines, license suspension, vehicle registration revocation, and in some cases, jail time. You may also be required to file an SR-22 form to reinstate your driving privileges.

Can I legally drive in Virginia without car insurance?

Yes, but only if you pay a $500 Uninsured Motor Vehicle fee. This fee does not provide any coverage, and you remain personally liable for any damages you cause in an accident.

Do I need insurance in New Hampshire?

Insurance is not required unless you’ve been in an accident, received a DUI, or been convicted of certain traffic violations. However, you must still prove financial responsibility if you cause damage.

What is financial responsibility in auto insurance?

Financial responsibility means proving you can cover damages if you cause an accident. This is typically done through insurance, but some states allow cash deposits or self-insurance as alternatives.

Can I use my health insurance if I’m in an accident and don’t have car insurance?

Your health insurance may cover medical expenses, but it won’t pay for vehicle damage or liability to others. Without car insurance, you could still be sued for additional costs.