How Much Is Car Insurance in Illinois?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is the Average Cost of Car Insurance in Illinois?

- 4 Illinois Car Insurance Requirements: What You Must Have

- 5 Factors That Affect Car Insurance Rates in Illinois

- 6 How to Save Money on Car Insurance in Illinois

- 7 Best Car Insurance Companies in Illinois

- 8 What to Do If You’re Struggling to Afford Car Insurance

- 9 Final Thoughts: Making Smart Choices About Car Insurance in Illinois

- 10 Frequently Asked Questions

Car insurance in Illinois costs an average of $1,400 to $2,000 per year for full coverage, depending on your location, driving history, and coverage choices. While the state sets minimum requirements, most drivers pay more for better protection and peace of mind.

If you’re driving in Illinois, you’re required by law to carry car insurance—but that doesn’t mean you have to overpay. Whether you’re a new driver in Chicago, a family in Springfield, or a retiree in Peoria, understanding how much car insurance costs in Illinois can help you make smart financial decisions. The truth is, car insurance isn’t one-size-fits-all. Your premium depends on a mix of personal factors, location, and the type of coverage you choose.

So, how much is car insurance in Illinois, really? On average, Illinois drivers pay between $1,400 and $2,000 per year for full coverage, which includes liability, collision, and comprehensive protection. If you’re only meeting the state’s minimum requirements, you might pay closer to $500–$700 annually. But here’s the catch: minimum coverage often leaves you underinsured in serious accidents. That’s why most financial experts recommend going beyond the basics.

In this guide, we’ll break down the real cost of car insurance in Illinois, explore what affects your rates, and share practical tips to help you save. Whether you’re shopping for your first policy or looking to switch providers, this article will give you the clarity and confidence you need to get the best deal.

Key Takeaways

- Average annual cost: Full coverage car insurance in Illinois typically ranges from $1,400 to $2,000, with minimum liability coverage averaging around $500–$700 per year.

- State minimum requirements: Illinois requires 25/50/20 liability coverage—$25,000 for bodily injury per person, $50,000 per accident, and $20,000 for property damage.

- Location matters: Urban areas like Chicago have higher premiums due to traffic density, theft rates, and accident frequency compared to rural regions.

- Driver profile impacts rates: Age, credit score, driving record, and annual mileage all influence how much you’ll pay for car insurance in Illinois.

- Discounts can lower costs: Safe driver, multi-policy, good student, and low-mileage discounts help reduce premiums significantly.

- Shop around annually: Comparing quotes from at least three insurers can save hundreds of dollars each year.

- Consider usage-based programs: Telematics programs like Snapshot or Drivewise monitor driving habits and reward safe behavior with lower rates.

📑 Table of Contents

- What Is the Average Cost of Car Insurance in Illinois?

- Illinois Car Insurance Requirements: What You Must Have

- Factors That Affect Car Insurance Rates in Illinois

- How to Save Money on Car Insurance in Illinois

- Best Car Insurance Companies in Illinois

- What to Do If You’re Struggling to Afford Car Insurance

- Final Thoughts: Making Smart Choices About Car Insurance in Illinois

What Is the Average Cost of Car Insurance in Illinois?

When it comes to car insurance, Illinois sits somewhere in the middle compared to other states. It’s not the cheapest, but it’s also not among the most expensive. According to recent data from the National Association of Insurance Commissioners (NAIC) and industry reports, the average annual premium for full coverage in Illinois is around $1,650. For minimum liability coverage, the average drops to about $600 per year.

But averages only tell part of the story. Your actual rate could be much higher or lower depending on where you live, how you drive, and what kind of car you own. For example, a 35-year-old driver with a clean record in Rockford might pay $1,200 for full coverage, while a 22-year-old in downtown Chicago with a speeding ticket could pay over $3,000.

Full Coverage vs. Minimum Coverage

Full coverage typically includes liability, collision, and comprehensive insurance. It protects you financially if you cause an accident, damage your own vehicle, or face non-collision incidents like theft, vandalism, or weather damage. Minimum coverage, on the other hand, only meets Illinois’ legal requirements and covers damage you cause to others—not your own car.

Most insurers recommend full coverage if your car is worth more than $4,000. Why? Because if you total your vehicle in an accident, minimum coverage won’t help you replace it. For example, if you drive a 2020 Honda Civic valued at $18,000, paying an extra $800–$1,000 per year for full coverage could save you thousands out of pocket.

How Illinois Compares to Neighboring States

Let’s put Illinois in perspective. In Indiana, the average full coverage premium is about $1,300—lower than Illinois. In Wisconsin, it’s around $1,450. Meanwhile, Michigan’s no-fault system drives premiums much higher, averaging over $2,500. So while Illinois isn’t the cheapest, it’s more affordable than some nearby states.

One reason for this balance is Illinois’ mix of urban and rural areas. Cities like Chicago drive up average costs due to congestion and higher accident rates, but rural areas like southern Illinois keep the overall average in check.

Illinois Car Insurance Requirements: What You Must Have

Visual guide about How Much Is Car Insurance in Illinois?

Image source: illinoisdrivers.com

Before we dive deeper into costs, it’s important to understand what Illinois law requires. Driving without insurance isn’t just risky—it’s illegal. If you’re caught, you could face fines, license suspension, or even vehicle impoundment.

Minimum Liability Coverage

Illinois mandates that all drivers carry at least the following liability coverage:

– $25,000 for bodily injury per person

– $50,000 for bodily injury per accident

– $20,000 for property damage

This is often written as 25/50/20. It means your insurer will pay up to $25,000 for one person’s injuries in an accident you cause, up to $50,000 total for all injured parties, and up to $20,000 for damage to other people’s property (like their car or a fence).

But here’s a reality check: these numbers haven’t been updated since 1989. Medical costs and car repairs have skyrocketed since then. A single hospital visit can easily exceed $25,000. That’s why many experts recommend increasing your liability limits to at least 100/300/100—or even higher if you have significant assets to protect.

Uninsured/Underinsured Motorist Coverage

Illinois also requires uninsured motorist (UM) and underinsured motorist (UIM) coverage. This protects you if you’re hit by a driver who has no insurance or not enough to cover your damages. The minimum UM/UIM coverage matches your liability limits—so if you carry 25/50/20, your UM/UIM must also be 25/50/20.

This is a lifesaver. According to the Insurance Information Institute, about 13% of Illinois drivers are uninsured. Without UM coverage, you’d be stuck paying for your own medical bills and car repairs after an accident with an uninsured driver.

Proof of Insurance

You must carry proof of insurance in your vehicle at all times. This can be a physical card or a digital copy on your phone. Law enforcement officers can request it during traffic stops, and failure to provide it can result in fines and penalties.

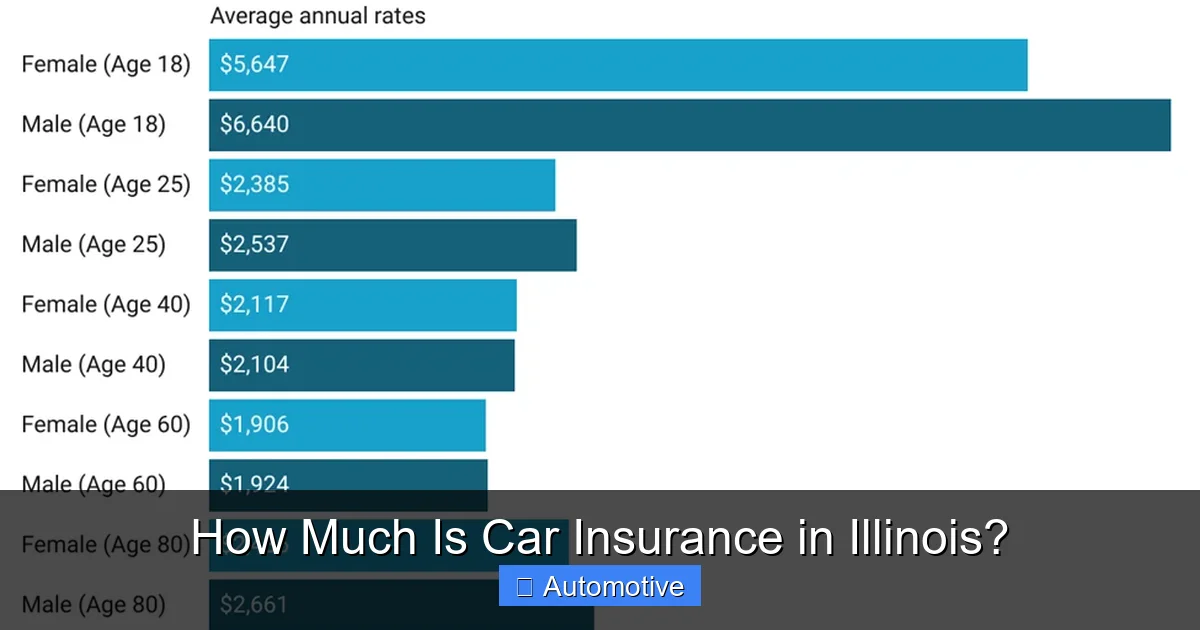

Factors That Affect Car Insurance Rates in Illinois

Visual guide about How Much Is Car Insurance in Illinois?

Image source: pdffiller.com

Now that you know the basics, let’s talk about what really drives your premium. Insurance companies use complex algorithms to calculate risk, and several key factors influence how much you’ll pay.

Location: Urban vs. Rural

Where you live in Illinois has a huge impact on your rate. Chicago, the state’s largest city, has the highest insurance premiums due to heavy traffic, higher accident rates, and increased theft and vandalism. Drivers in Chicago’s South or West sides often pay 30–50% more than those in suburban or rural areas.

For example, a 30-year-old driver with a clean record might pay $1,800 per year in Chicago but only $1,200 in Champaign or Carbondale. Even within Chicago, ZIP codes matter. A driver in the Loop might pay more than someone in Lincoln Park due to congestion and parking challenges.

Age and Driving Experience

Young drivers, especially those under 25, face the highest premiums. Insurance companies see them as higher risk due to inexperience and statistically higher accident rates. A 19-year-old male in Chicago could pay over $4,000 per year for full coverage.

On the flip side, older drivers (55–65) often enjoy lower rates due to years of safe driving. But once you hit 70, some insurers may start raising premiums again due to age-related risk factors.

Driving Record

Your driving history is one of the biggest predictors of your premium. A clean record can save you hundreds, while tickets, accidents, or DUIs can spike your rate significantly.

– One speeding ticket: +10–20%

– At-fault accident: +20–50%

– DUI: +80–150% or more

For example, a driver with a clean record paying $1,500 per year could see their premium jump to $2,250 after a DUI. Some insurers may even drop high-risk drivers, forcing them into the state’s assigned risk pool, which comes with much higher rates.

Credit Score

Illinois allows insurers to use credit-based insurance scores to determine premiums. Studies show a correlation between credit history and claim frequency, so drivers with poor credit often pay more.

A driver with excellent credit (750+) might pay $1,400 per year, while someone with poor credit (under 600) could pay $2,200 or more—even with the same car and driving record.

Vehicle Type

The make, model, and year of your car affect your premium. Sports cars, luxury vehicles, and models with high theft rates cost more to insure. For example, insuring a Toyota Camry will be cheaper than insuring a BMW 3 Series or a Ford Mustang.

Newer cars may also cost more due to higher repair costs, even if they have advanced safety features. However, some insurers offer discounts for vehicles with anti-theft systems, lane departure warnings, or automatic emergency braking.

Annual Mileage

The more you drive, the higher your risk of an accident. Drivers who commute long distances or use their car for work typically pay more than those who drive only occasionally.

If you work from home and drive less than 5,000 miles per year, you may qualify for a low-mileage discount. Some insurers offer usage-based programs that track your mileage and driving habits via a mobile app or device.

How to Save Money on Car Insurance in Illinois

Visual guide about How Much Is Car Insurance in Illinois?

Image source: thetechedvocate.org

The good news? There are many ways to reduce your car insurance costs without sacrificing coverage. A little effort can go a long way.

Shop Around and Compare Quotes

One of the easiest ways to save is by comparing quotes from multiple insurers. Rates can vary by hundreds of dollars between companies for the same coverage.

Start with national carriers like State Farm, GEICO, Progressive, and Allstate. Then check regional insurers like Country Financial or Illinois Farm Bureau, which may offer competitive rates for local drivers.

Use online comparison tools or work with an independent agent who can get quotes from several companies at once. Aim to compare at least three quotes before deciding.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Here are some common ones available in Illinois:

– **Safe driver discount:** For maintaining a clean record

– **Multi-policy discount:** Bundling auto and home insurance

– **Good student discount:** For students with a B average or higher

– **Low-mileage discount:** For driving under a certain number of miles per year

– **Defensive driving course discount:** After completing an approved course

– **Anti-theft device discount:** For vehicles with alarms or tracking systems

– **Pay-in-full discount:** For paying your annual premium upfront

For example, a family with two teen drivers could save $300–$500 per year by bundling policies and taking a defensive driving course.

Raise Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Raising it from $500 to $1,000 can lower your premium by 10–20%. Just make sure you can afford the higher deductible if you need to file a claim.

Improve Your Credit Score

Since credit affects your rate, improving your credit can lead to lower premiums. Pay bills on time, reduce credit card balances, and check your credit report for errors.

Consider Usage-Based Insurance

Telematics programs like Progressive’s Snapshot, State Farm’s Drive Safe & Save, or Allstate’s Drivewise monitor your driving habits—such as speed, braking, and mileage—and reward safe behavior with discounts.

These programs are especially helpful for young drivers or those with a few tickets. Some users report savings of 10–30% after six months of safe driving.

Drop Collision or Comprehensive on Older Cars

If your car is over 10 years old or worth less than $4,000, it may not be worth paying for collision and comprehensive coverage. The cost of the premium could exceed the car’s value.

For example, if your 2008 sedan is worth $3,000 and you’re paying $800 per year for full coverage, you might be better off dropping collision and comprehensive and setting aside that money in a repair fund.

Best Car Insurance Companies in Illinois

Not all insurers are created equal. Some offer better rates, customer service, or claims handling than others. Based on customer satisfaction, financial strength, and affordability, here are some top choices for Illinois drivers.

State Farm

State Farm is the largest auto insurer in the U.S. and a popular choice in Illinois. It offers competitive rates, especially for safe drivers and those who bundle policies. Their local agents provide personalized service, and their mobile app makes managing your policy easy.

GEICO

GEICO is known for low rates and a user-friendly online experience. It’s a great option for drivers with good credit and clean records. GEICO also offers a variety of discounts and a strong mobile app for claims and ID cards.

Progressive

Progressive stands out for its Name Your Price tool and Snapshot program. It’s ideal for drivers who want flexibility and usage-based savings. Progressive also offers competitive rates for high-risk drivers.

Allstate

Allstate provides strong customer service and a wide range of coverage options. Its Drivewise program rewards safe driving, and it offers accident forgiveness in some cases. Allstate is a solid choice for families and older drivers.

Country Financial

A regional insurer based in Illinois, Country Financial offers personalized service and competitive rates for local drivers. It’s especially popular in central and southern Illinois.

What to Do If You’re Struggling to Afford Car Insurance

Car insurance is a necessity, but it can be a financial burden—especially for low-income drivers. If you’re having trouble affording coverage, here are some options.

Look into the Illinois Assigned Risk Plan

If you’ve been denied coverage by multiple insurers, you may qualify for the Illinois Automobile Insurance Plan (IL AIP). This state-run program assigns high-risk drivers to insurers who must accept them. While rates are higher, it ensures you can meet legal requirements.

Apply for the Illinois Low-Income Car Insurance Program

Illinois doesn’t currently have a state-sponsored low-income insurance program, but some nonprofit organizations and community groups offer assistance or guidance. Check with local United Way chapters or consumer advocacy groups for resources.

Consider Pay-As-You-Go or Monthly Plans

Some insurers offer monthly payment plans or pay-as-you-go options that spread the cost over time. This can make insurance more manageable on a tight budget.

Final Thoughts: Making Smart Choices About Car Insurance in Illinois

So, how much is car insurance in Illinois? The answer depends on you—your driving habits, your car, your location, and your coverage needs. While the average cost is around $1,650 per year for full coverage, your actual rate could be higher or lower.

The key is to understand your options and make informed decisions. Don’t just go with the cheapest policy—make sure it provides the protection you need. And remember, shopping around, maintaining a clean record, and taking advantage of discounts can save you hundreds each year.

Car insurance isn’t just a legal requirement—it’s a smart investment in your financial security. Whether you’re driving down Lake Shore Drive or cruising through the cornfields of central Illinois, the right policy gives you peace of mind on every mile.

Frequently Asked Questions

What is the minimum car insurance required in Illinois?

Illinois requires drivers to carry at least 25/50/20 liability coverage: $25,000 for bodily injury per person, $50,000 per accident, and $20,000 for property damage. Uninsured motorist coverage matching these limits is also mandatory.

Why is car insurance so expensive in Chicago?

Chicago has higher insurance rates due to heavy traffic, frequent accidents, higher theft rates, and dense urban driving conditions. These factors increase the risk for insurers, leading to higher premiums.

Can I get car insurance with a bad driving record in Illinois?

Yes, but it will cost more. High-risk drivers can still get coverage through standard insurers or the Illinois Automobile Insurance Plan (IL AIP), though premiums will be significantly higher.

Does my credit score affect my car insurance rate in Illinois?

Yes, Illinois allows insurers to use credit-based insurance scores. Drivers with lower credit scores typically pay higher premiums due to statistical correlations between credit and claim frequency.

How often should I shop for car insurance in Illinois?

It’s a good idea to compare quotes at least once a year, especially when your policy renews. Rates change frequently, and you could save hundreds by switching insurers.

Are there discounts available for young drivers in Illinois?

Yes, many insurers offer good student discounts, defensive driving course discounts, and usage-based programs that can help reduce premiums for young or new drivers.