How Much Is Car Insurance in California

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance in California?

- 4 What Determines Your Car Insurance Rate in California?

- 5 Average Car Insurance Costs by California City

- 6 California’s Minimum Car Insurance Requirements

- 7 How to Save Money on Car Insurance in California

- 8 Special Considerations for California Drivers

- 9 Conclusion: Finding the Right Car Insurance in California

- 10 Frequently Asked Questions

Car insurance in California costs an average of $1,800 to $2,400 per year for full coverage, but rates vary widely based on location, driving history, and coverage choices. Understanding what impacts your premium can help you find affordable, reliable protection.

Key Takeaways

- Average annual cost: Full coverage car insurance in California typically ranges from $1,800 to $2,400, while minimum liability coverage costs around $600 to $900.

- Location matters: Urban areas like Los Angeles and San Francisco have higher premiums due to traffic density, theft rates, and accident frequency.

- Driving record is key: A clean driving history can lower your rates, while accidents, tickets, or DUIs can significantly increase them.

- Age and experience count: Young drivers under 25 often pay much more, while older, experienced drivers usually enjoy lower premiums.

- Vehicle type affects cost: Luxury, sports, and high-theft vehicles cost more to insure than safe, economical models.

- Credit score influences rates: California allows insurers to use credit-based insurance scores, so better credit can mean lower premiums.

- Shop around annually: Comparing quotes from multiple insurers can save you hundreds of dollars each year.

📑 Table of Contents

- How Much Is Car Insurance in California?

- What Determines Your Car Insurance Rate in California?

- Average Car Insurance Costs by California City

- California’s Minimum Car Insurance Requirements

- How to Save Money on Car Insurance in California

- Special Considerations for California Drivers

- Conclusion: Finding the Right Car Insurance in California

How Much Is Car Insurance in California?

If you’re driving in California, you’re not just cruising down scenic highways—you’re also navigating one of the most expensive states for car insurance in the U.S. Whether you’re a new driver in San Diego, a commuter in the Bay Area, or a family in Sacramento, understanding how much car insurance costs in California is essential for budgeting and staying compliant with state law.

Car insurance isn’t just a legal requirement—it’s a financial safety net. In California, drivers must carry at least the minimum liability coverage, but many opt for full coverage to protect against theft, vandalism, and collisions. The cost of that protection varies widely depending on where you live, how you drive, and what kind of car you drive. On average, California drivers pay between $1,800 and $2,400 per year for full coverage, while minimum liability coverage runs about $600 to $900 annually. That’s higher than the national average, but it’s not without reason.

California’s high population density, traffic congestion, and frequent natural disasters like wildfires and earthquakes contribute to elevated insurance costs. Additionally, the state’s strict regulations and high cost of living play a role. But don’t let the numbers scare you. With the right knowledge and a bit of research, you can find affordable, high-quality car insurance that fits your needs and your budget.

What Determines Your Car Insurance Rate in California?

Visual guide about How Much Is Car Insurance in California

Image source: res.cloudinary.com

Your car insurance premium isn’t just a random number—it’s calculated based on a mix of personal, geographic, and vehicle-related factors. Insurance companies use complex algorithms to assess risk, and the higher the risk you pose, the more you’ll pay. Let’s break down the biggest factors that influence how much you’ll pay for car insurance in California.

Your Driving Record

One of the most significant factors is your driving history. If you have a clean record with no accidents, tickets, or DUIs, you’re likely to qualify for lower rates. On the flip side, even a single speeding ticket can increase your premium by 10% to 20%. A DUI conviction? That could double your rates or more. For example, a 35-year-old driver with a clean record might pay $1,600 a year for full coverage, while the same driver with a DUI could pay over $3,000.

Where You Live

Location is a major player in California. Urban areas like Los Angeles, San Francisco, and Oakland have higher premiums due to traffic congestion, higher accident rates, and increased vehicle theft. In contrast, rural areas like Redding or Eureka tend to have lower rates. For instance, a driver in downtown LA might pay $2,800 a year, while someone in a small Central Valley town might pay just $1,400 for the same coverage.

Your Age and Driving Experience

Young drivers, especially those under 25, face the highest premiums. A 19-year-old male in California might pay $4,000 or more annually for full coverage due to higher accident rates among teens. As you gain experience and reach your 30s and 40s, rates typically drop. Married drivers and those with advanced degrees may also see slight discounts.

The Type of Car You Drive

Your vehicle’s make, model, age, and safety features all affect your premium. High-performance cars like BMWs, Audis, or Mustangs cost more to insure because they’re more expensive to repair and more likely to be involved in speeding-related accidents. Electric vehicles like Teslas can also be pricey due to costly repairs and specialized parts. On the other hand, safe, reliable cars like Honda Accords or Toyota Camrys often come with lower premiums.

Your Credit Score

California allows insurers to use credit-based insurance scores when setting rates. While the state limits how much weight credit can carry, a poor credit score can still increase your premium by 20% to 50%. For example, a driver with excellent credit might pay $1,700 a year, while someone with poor credit could pay $2,500 for the same policy.

Coverage Level and Deductible

The more coverage you buy, the higher your premium. Minimum liability coverage is the cheapest but offers the least protection. Full coverage, which includes collision and comprehensive, is more expensive but provides peace of mind. Your deductible—the amount you pay out of pocket before insurance kicks in—also matters. A $1,000 deductible can lower your premium by 15% to 30% compared to a $500 deductible.

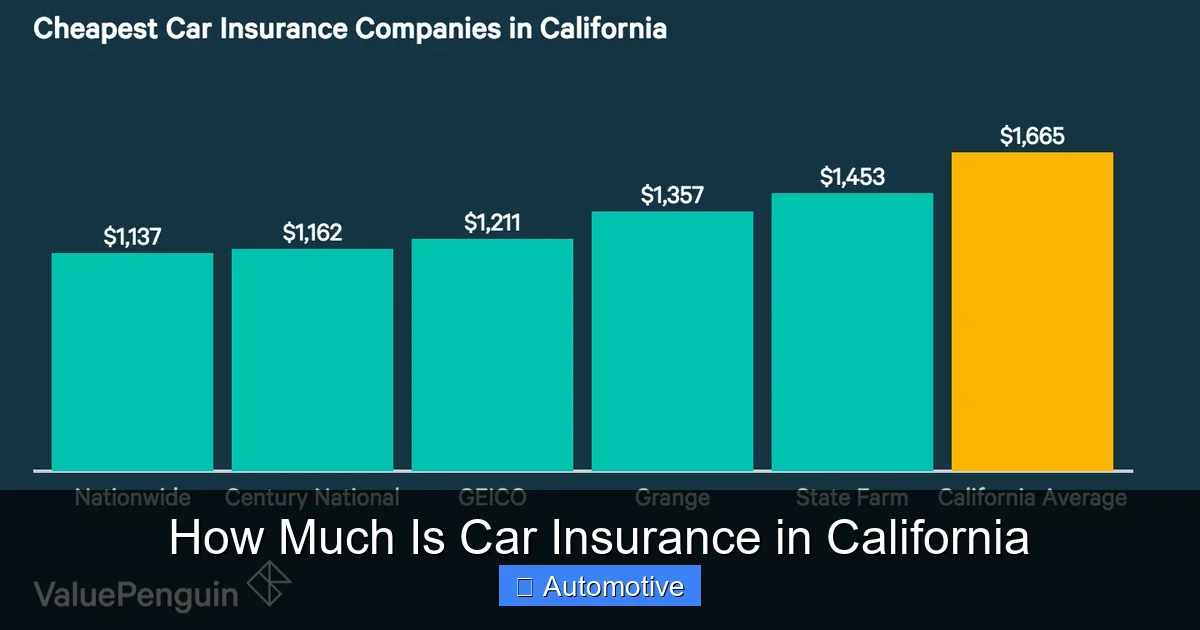

Average Car Insurance Costs by California City

Visual guide about How Much Is Car Insurance in California

Image source: busconomico.us

One of the most eye-opening aspects of car insurance in California is how much rates can vary from one city to another. Even neighboring cities can have dramatically different premiums due to local crime rates, traffic patterns, and population density. Let’s look at some real-world examples to give you a clearer picture.

Los Angeles

As the largest city in California, Los Angeles has some of the highest insurance rates in the state. The average annual premium for full coverage is around $2,600, with minimum liability averaging $850. High traffic, frequent accidents, and a high rate of vehicle theft contribute to these elevated costs. For example, a 30-year-old driver with a clean record might pay $2,400 a year, while someone with a speeding ticket could see that jump to $2,900.

San Francisco

San Francisco isn’t far behind LA in terms of cost. The average full coverage premium here is about $2,500 per year, with minimum liability around $800. The city’s steep hills, narrow streets, and high population density make driving riskier, which insurers reflect in their pricing. Parking in SF is also notoriously difficult, increasing the risk of fender benders and vandalism.

San Diego

San Diego offers slightly more affordable rates, with full coverage averaging $2,100 annually and minimum liability at about $700. The city’s milder traffic and lower crime rates compared to LA and SF help keep premiums in check. A safe driver in San Diego might pay $1,900 a year, while a teen driver could pay over $4,000.

Sacramento

The state capital has moderate insurance costs. Full coverage averages $1,900 per year, with minimum liability around $650. Sacramento’s mix of urban and suburban areas means rates are higher than rural towns but lower than major metros. A 40-year-old driver with good credit might pay $1,700, while someone with a DUI could pay $3,200.

Fresno

In the Central Valley, Fresno offers more budget-friendly options. Full coverage averages $1,700 annually, with minimum liability at $600. Lower population density and fewer traffic jams help reduce risk, making insurance more affordable. A clean-record driver might pay $1,500, while a high-risk driver could pay $2,800.

Rural Areas (e.g., Redding, Eureka)

In smaller, rural communities, insurance is significantly cheaper. Full coverage averages $1,400 per year, with minimum liability around $500. With less traffic, fewer accidents, and lower theft rates, insurers charge less. A 35-year-old driver might pay just $1,200 a year for full coverage.

California’s Minimum Car Insurance Requirements

Before you even think about how much car insurance costs, you need to know what the law requires. California has strict minimum coverage requirements that all drivers must meet. Driving without insurance can result in fines, license suspension, and even vehicle impoundment.

Liability Coverage Basics

California requires drivers to carry liability insurance to cover damages and injuries you cause to others in an accident. The state’s minimum limits are:

– $15,000 for injury or death to one person

– $30,000 for injury or death to more than one person

– $5,000 for property damage

This is often written as 15/30/5. While this meets legal requirements, it’s often not enough to cover serious accidents. For example, a single emergency room visit can cost over $20,000, leaving you personally liable for the difference.

Why Minimum Coverage Isn’t Enough

Many drivers opt for higher limits or full coverage to protect their assets. If you’re at fault in a major accident, the other party could sue you for medical bills, lost wages, and pain and suffering. Without sufficient coverage, your savings, home, or future income could be at risk. For instance, a driver with only 15/30/5 coverage who causes a multi-car pileup could face hundreds of thousands in damages—far beyond their policy limits.

Uninsured/Underinsured Motorist Coverage

California also requires uninsured/underinsured motorist (UM/UIM) coverage unless you explicitly reject it in writing. This protects you if you’re hit by a driver with no insurance or insufficient coverage. The minimum UM/UIM limits match your liability limits (15/30/5), but many experts recommend higher amounts.

Additional Coverage Options

Beyond the basics, you can add:

– Collision coverage: Pays for damage to your car from accidents, regardless of fault.

– Comprehensive coverage: Covers non-collision events like theft, vandalism, fire, and natural disasters.

– Medical payments (MedPay): Covers your medical expenses after an accident.

– Rental reimbursement: Pays for a rental car while your vehicle is being repaired.

These add-ons increase your premium but provide valuable protection.

How to Save Money on Car Insurance in California

Car insurance in California doesn’t have to break the bank. With smart strategies, you can reduce your premium without sacrificing coverage. Here are proven ways to save.

Shop Around and Compare Quotes

One of the easiest ways to save is by comparing quotes from at least three different insurers. Rates can vary by hundreds of dollars for the same coverage. Use online comparison tools or work with an independent agent to find the best deal. For example, a driver in Sacramento might get a quote of $1,900 from State Farm, $1,700 from Geico, and $1,500 from Progressive—just by shopping around.

Maintain a Clean Driving Record

Safe driving is the best way to keep your rates low. Avoid speeding, distracted driving, and DUIs. Many insurers offer accident forgiveness or safe driver discounts after a few years of clean driving. For instance, Allstate’s Safe Driving Bonus gives you a discount every six months you don’t file a claim.

Improve Your Credit Score

Since California allows credit-based pricing, improving your credit can lower your premium. Pay bills on time, reduce debt, and check your credit report for errors. A jump from “fair” to “good” credit could save you $200 or more per year.

Choose a Higher Deductible

Raising your deductible from $500 to $1,000 can reduce your premium by 15% to 30%. Just make sure you can afford the out-of-pocket cost if you need to file a claim. For example, a $1,800 policy might drop to $1,400 with a higher deductible.

Take Advantage of Discounts

Many insurers offer discounts for:

– Good students (B average or higher)

– Defensive driving courses

– Multi-car policies

– Bundling home and auto insurance

– Low mileage

– Safety features (anti-lock brakes, airbags, anti-theft systems)

Ask your insurer about available discounts—you might save 5% to 25%.

Drive a Safer, Less Expensive Car

Choose a vehicle with high safety ratings and low theft rates. Avoid luxury or high-performance models unless you’re prepared for higher premiums. For example, insuring a Honda Civic might cost $1,600 a year, while a BMW 3 Series could cost $2,800.

Consider Usage-Based Insurance

Some insurers offer programs that track your driving habits via a mobile app or device. Safe drivers can earn discounts based on mileage, braking, and speed. For example, Progressive’s Snapshot program can save you up to 30%.

Special Considerations for California Drivers

California’s unique landscape and regulations create special challenges and opportunities for drivers. Here are a few things to keep in mind.

Wildfire and Natural Disaster Risks

California is prone to wildfires, earthquakes, and mudslides. Comprehensive coverage is essential to protect your vehicle from fire, falling debris, or flooding. Without it, you could be left paying thousands out of pocket. For example, a driver in Sonoma County whose car is damaged in a wildfire would need comprehensive coverage to file a claim.

High Rates of Uninsured Drivers

Despite mandatory insurance laws, about 15% of California drivers are uninsured. That’s why UM/UIM coverage is so important. If you’re hit by an uninsured driver, this coverage pays for your medical bills and car repairs.

Strict Emissions and Smog Checks

California has strict environmental regulations, including smog checks every two years for most vehicles. While this doesn’t directly affect insurance, it reflects the state’s focus on safety and compliance—values that insurers also prioritize.

Rideshare and Delivery Driver Insurance

If you drive for Uber, Lyft, DoorDash, or similar services, your personal policy may not cover you during work. You’ll need a commercial or rideshare endorsement. For example, a DoorDash driver in LA might pay an extra $200 a year for coverage while delivering.

Conclusion: Finding the Right Car Insurance in California

So, how much is car insurance in California? The answer isn’t one-size-fits-all. While the average driver pays between $1,800 and $2,400 per year for full coverage, your actual cost depends on your location, driving history, vehicle, and coverage choices. Urban areas like LA and San Francisco are more expensive, while rural towns offer lower rates. Young drivers, high-risk vehicles, and poor credit can all drive up premiums.

But here’s the good news: you have control. By maintaining a clean driving record, improving your credit, shopping around, and taking advantage of discounts, you can find affordable, reliable coverage. Don’t just accept the first quote you get—compare options, ask questions, and tailor your policy to your needs.

Remember, car insurance isn’t just about meeting legal requirements. It’s about protecting yourself, your family, and your financial future. Whether you’re commuting to work, road-tripping up the coast, or just running errands, the right policy gives you peace of mind on every mile.

So take the time to understand your options, evaluate your risks, and choose wisely. With the right approach, you can drive confidently through the Golden State—without overpaying for protection.

Frequently Asked Questions

How much is car insurance per month in California?

The average monthly cost for full coverage car insurance in California is between $150 and $200, while minimum liability coverage costs around $50 to $75 per month. Actual rates depend on your profile and location.

Is car insurance cheaper in California than other states?

No, car insurance in California is generally more expensive than the national average. Factors like high population density, traffic, and strict regulations contribute to higher premiums compared to states like Maine or Ohio.

Can I get car insurance with a suspended license in California?

It’s difficult but possible. Some insurers offer SR-22 policies for high-risk drivers, including those with suspended licenses. These policies are more expensive and require proof of financial responsibility.

Do I need full coverage if I lease or finance my car?

Yes, most lenders and leasing companies require full coverage (collision and comprehensive) to protect their financial interest in the vehicle. Minimum liability alone won’t meet their requirements.

How does a DUI affect car insurance in California?

A DUI conviction can double or even triple your insurance premium. You’ll also need to file an SR-22 form, which signals to the state that you’re high-risk. Rates may remain elevated for 3 to 5 years.

Can I switch car insurance companies anytime in California?

Yes, you can switch insurers at any time. Just make sure there’s no lapse in coverage. Most companies allow you to cancel without penalty, but check your policy for any fees.