What Does Full Coverage Car Insurance Cover

Full coverage car insurance combines liability, collision, and comprehensive coverage to protect you financially in most driving scenarios. It’s not a single policy but a bundle that covers damage to your vehicle, others’ property, and medical costs—offering peace of mind on the road.

Key Takeaways

- Full coverage includes liability, collision, and comprehensive insurance: This trio forms the core of most “full coverage” policies, protecting you from a wide range of risks.

- It covers damage to your own vehicle: Unlike basic liability insurance, full coverage pays for repairs to your car after accidents, theft, or natural disasters.

- It protects against non-collision events: Comprehensive coverage handles incidents like vandalism, falling objects, fire, and animal collisions.

- It’s often required by lenders: If you’re financing or leasing a car, your lender will likely require full coverage to protect their investment.

- Deductibles affect your out-of-pocket costs: Choosing a higher deductible lowers your premium but increases what you pay when filing a claim.

- It doesn’t cover everything: Personal belongings, mechanical breakdowns, and normal wear and tear are typically excluded.

- You can customize with add-ons: Options like roadside assistance, rental reimbursement, and gap insurance enhance your protection.

📑 Table of Contents

What Does Full Coverage Car Insurance Cover?

When you hear the term “full coverage car insurance,” it sounds like a one-size-fits-all solution that protects you from every possible driving mishap. But the truth is, there’s no official policy called “full coverage” in the insurance world. Instead, it’s a commonly used phrase that refers to a combination of several types of coverage that together offer much broader protection than the minimum required by law.

Most drivers think of full coverage as the gold standard—something that shields them from financial disaster whether they crash into another car, hit a deer, or wake up to find their vehicle stolen. And they’re not entirely wrong. When properly configured, a full coverage policy can be incredibly comprehensive, covering not just damage to other people’s property and medical bills (which basic liability covers), but also damage to your own vehicle and a wide range of unexpected events.

But here’s the catch: “full coverage” isn’t a magic shield. It doesn’t cover every possible scenario, and it certainly doesn’t eliminate all out-of-pocket costs. Understanding exactly what it includes—and what it leaves out—is crucial for making smart decisions about your auto insurance. Whether you’re buying your first car, refinancing an existing loan, or just reviewing your current policy, knowing the ins and outs of full coverage can save you thousands in the long run.

The Core Components of Full Coverage Insurance

Visual guide about What Does Full Coverage Car Insurance Cover

Image source: assets-us-01.kc-usercontent.com

At its heart, full coverage car insurance is built on three main pillars: liability insurance, collision coverage, and comprehensive coverage. Together, these form the foundation of most robust auto insurance policies. Let’s break down each one and see how they work in real-life situations.

Liability Insurance: Protecting Others

Liability insurance is the only type of coverage required by law in almost every state. It’s designed to protect you financially if you’re at fault in an accident that causes injury to others or damages their property. There are two parts to liability coverage:

– **Bodily Injury Liability**: This pays for medical expenses, lost wages, and even legal fees if someone is injured in an accident you caused. For example, if you rear-end another driver and they need physical therapy, your bodily injury liability kicks in to cover those costs—up to your policy limits.

– **Property Damage Liability**: This covers the cost of repairing or replacing another person’s vehicle or property. If you crash into someone’s fence or damage a parked car, this part of your policy handles the repairs.

While liability insurance is essential, it doesn’t protect your own vehicle or health. That’s where the other two components come in.

Collision Coverage: When You Crash Your Car

Collision coverage pays to repair or replace your vehicle if it’s damaged in a collision—regardless of who’s at fault. This includes accidents with other cars, single-vehicle crashes (like hitting a tree or guardrail), or even rolling your car.

Let’s say you’re driving in the rain, lose control, and slide into a concrete barrier. Your car’s front end is smashed, and the airbags deployed. Without collision coverage, you’d be on the hook for all repair costs. But with it, your insurance company covers the repairs (minus your deductible), getting you back on the road faster.

Collision coverage is especially valuable for newer or more expensive vehicles, where repair costs can run into the thousands. It’s also typically required if you’re financing or leasing your car, since the lender wants to protect their investment.

Comprehensive Coverage: Beyond Collisions

While collision handles accidents involving impact, comprehensive coverage steps in for everything else. Think of it as your “non-collision” safety net. It protects your vehicle from a wide range of unexpected events, including:

– Theft

– Vandalism (like broken windows or keyed paint)

– Fire

– Natural disasters (hurricanes, floods, hail)

– Falling objects (tree branches, construction debris)

– Animal collisions (hitting a deer or raccoon)

For example, imagine you park your car overnight and wake up to find it covered in graffiti and a shattered windshield. Comprehensive coverage would pay for the cleanup and repairs. Or if a hailstorm dents your roof and hood, your insurer handles the bodywork—again, after you pay your deductible.

This coverage is particularly important if you live in areas prone to severe weather, high crime rates, or wildlife crossings. It’s also commonly required by lenders, just like collision coverage.

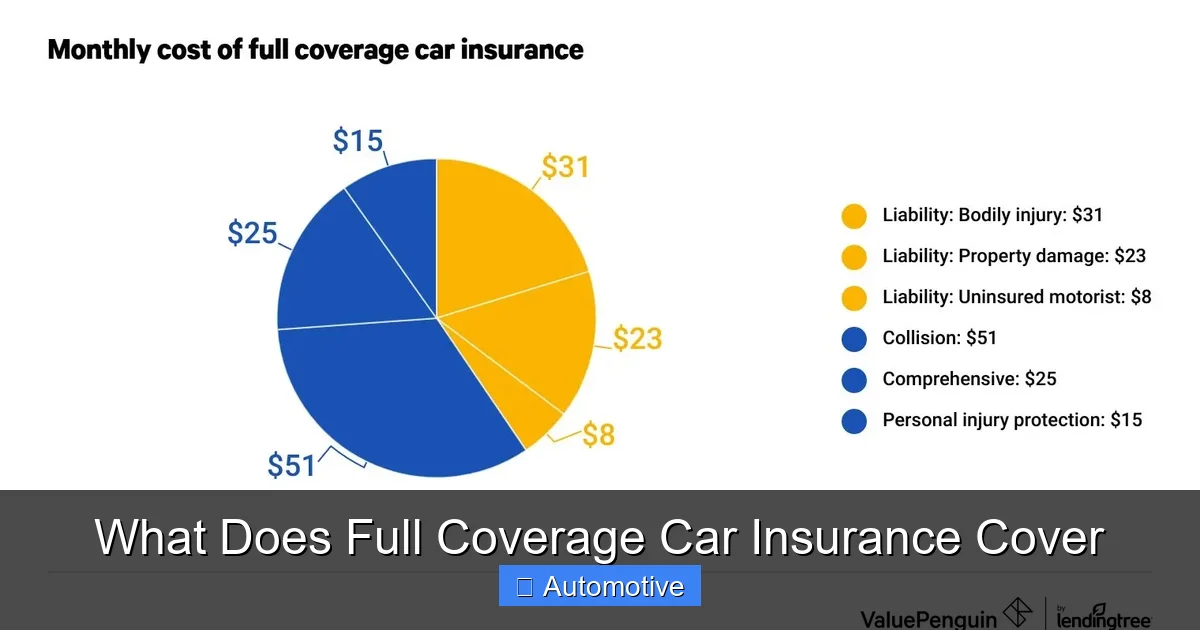

What Full Coverage Doesn’t Cover

Visual guide about What Does Full Coverage Car Insurance Cover

Image source: cdn.howmuch.net

Now that we’ve covered what full protection includes, it’s just as important to understand its limits. Despite the name, full coverage doesn’t mean “covers everything.” There are several common scenarios and items that fall outside its scope.

Personal Belongings in Your Car

If your laptop, phone, or gym bag is stolen from your vehicle, don’t expect your auto insurance to reimburse you. Comprehensive coverage only protects the vehicle itself—not the personal items inside. For that, you’d need to file a claim under your homeowner’s or renter’s insurance policy, which typically includes off-premises coverage for personal property.

Mechanical Breakdowns and Wear and Tear

Full coverage won’t pay for routine maintenance, oil changes, brake pad replacements, or engine failures due to age or poor upkeep. These are considered normal wear and tear—part of owning a car. If your transmission fails because it’s old, that’s on you. However, if it’s damaged in an accident or by a covered event like flooding, then comprehensive or collision might apply.

Your Own Medical Bills (Without PIP or MedPay)

Liability coverage pays for the other driver’s injuries—not yours. If you’re hurt in an accident, your medical expenses won’t be covered unless you have Personal Injury Protection (PIP) or Medical Payments (MedPay) coverage. These are optional add-ons in most states (though required in some no-fault states) and help cover your medical costs regardless of fault.

Rental Cars and Lost Income

If your car is in the shop after an accident, full coverage won’t automatically pay for a rental—unless you’ve added rental reimbursement coverage. Similarly, if you miss work due to injuries, your auto policy won’t replace your lost wages. Again, PIP or disability insurance would handle that.

Intentional Damage or Illegal Activity

Insurance doesn’t cover deliberate acts. If you intentionally crash your car or use it in a crime, your claim will be denied. The same goes for driving under the influence—most policies exclude coverage for accidents that occur while intoxicated.

Why Lenders Require Full Coverage

Visual guide about What Does Full Coverage Car Insurance Cover

Image source: res.cloudinary.com

If you’re financing or leasing a vehicle, your lender will almost always require you to carry full coverage insurance. This isn’t just a suggestion—it’s a contractual obligation. Here’s why.

Protecting the Lender’s Investment

When you take out a car loan, the lender technically owns the vehicle until you pay off the loan. If your car is totaled in an accident and you only have liability insurance, the insurer won’t pay to replace it. That leaves the lender with a big loss—and you still owe the remaining balance on the loan.

Full coverage ensures that if the car is damaged or destroyed, the insurance payout can be used to repair it or pay off the loan. This protects both you and the lender.

Gap Insurance: The Missing Piece

Even with full coverage, there’s a gap—literally. Cars depreciate quickly. If your vehicle is totaled early in the loan term, the insurance payout might be less than what you still owe. For example, you might owe $25,000 on a car that’s now worth only $20,000. That $5,000 difference is your responsibility—unless you have gap insurance.

Gap insurance covers the “gap” between the car’s actual cash value and the remaining loan balance. It’s often included in leases or can be purchased separately. While not part of standard full coverage, it’s a smart add-on for anyone financing a new car.

Customizing Your Full Coverage Policy

One of the biggest advantages of full coverage is its flexibility. You’re not stuck with a rigid package—you can tailor your policy to fit your lifestyle, budget, and risk tolerance.

Choosing Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. For collision and comprehensive claims, you’ll choose a deductible—common options are $250, $500, or $1,000.

– A **higher deductible** means lower monthly premiums but more cost if you file a claim.

– A **lower deductible** means higher premiums but less stress at claim time.

If you have a good emergency fund and drive cautiously, a higher deductible can save you money over time. But if you’re on a tight budget or live in a high-risk area, a lower deductible might be worth the extra premium.

Adding Optional Coverages

Beyond the core trio, there are several valuable add-ons you can include:

– **Rental Reimbursement**: Pays for a rental car while yours is being repaired after a covered claim.

– **Roadside Assistance**: Covers towing, jump-starts, flat tires, and lockout services.

– **New Car Replacement**: If your new car is totaled within the first year, this replaces it with a brand-new model of the same kind.

– **Accident Forgiveness**: Prevents your premium from increasing after your first at-fault accident (available from some insurers).

– **Uninsured/Underinsured Motorist Coverage**: Protects you if you’re hit by a driver with no or insufficient insurance.

These extras can significantly enhance your protection, especially if you rely heavily on your vehicle or live in areas with high rates of uninsured drivers.

Reviewing Your Coverage Limits

It’s not enough to just have full coverage—you also need the right amount. Many drivers make the mistake of choosing the minimum liability limits required by their state, which can leave them exposed in serious accidents.

For example, if your liability limit is $25,000 per person for bodily injury, but the other driver’s medical bills total $100,000, you could be sued for the difference. That’s why experts recommend higher limits—like 100/300/100 (meaning $100,000 per person, $300,000 per accident for injuries, and $100,000 for property damage).

Similarly, make sure your collision and comprehensive coverage reflects your car’s current value. If your vehicle is older and worth less than your deductible, it might not be worth carrying those coverages anymore.

When Is Full Coverage Worth It?

Full coverage isn’t always necessary—or cost-effective. Whether you should carry it depends on several factors.

Age and Value of Your Vehicle

If you drive a brand-new or high-end car, full coverage is almost always worth it. The cost of repairs or replacement is high, and the peace of mind is invaluable.

But if your car is over 10 years old and worth less than $4,000, you might consider dropping collision and comprehensive. The annual premium could exceed the car’s value, making it a poor financial decision. In that case, liability-only coverage might suffice—especially if you have savings to cover repairs.

Your Financial Situation

If you can’t afford to replace your car out of pocket, full coverage is a smart choice. It acts as a financial safety net, protecting your assets and credit.

On the other hand, if you have a solid emergency fund and can handle unexpected repair costs, you might opt for a higher deductible or even drop full coverage on an older vehicle.

Where You Live and Drive

Your location plays a big role. If you live in a city with high traffic, crime, or severe weather, full coverage offers essential protection. Rural drivers might face fewer risks but could still benefit from comprehensive coverage due to wildlife or isolated roads.

Tips for Getting the Most Out of Your Policy

Once you’ve chosen full coverage, make sure you’re using it wisely. Here are some practical tips to maximize your protection and minimize costs.

Shop Around Annually

Insurance rates change frequently. What was a great deal last year might be overpriced now. Compare quotes from at least three insurers each year—you could save hundreds.

Bundle Your Policies

Many insurers offer discounts if you bundle auto with home, renters, or life insurance. This can reduce your overall premium by 10–25%.

Maintain a Clean Driving Record

Safe driving doesn’t just keep you safe—it keeps your premiums low. Avoid speeding tickets, accidents, and DUIs to qualify for safe driver discounts.

Ask About Discounts

Insurers offer a variety of discounts, including:

– Good student discounts

– Military or veteran discounts

– Low-mileage discounts

– Anti-theft device discounts

– Paperless billing or auto-pay discounts

Don’t assume you’re getting all the savings you deserve—ask your agent.

Review Your Policy After Major Life Changes

Marriage, moving, buying a new car, or adding a teen driver can all affect your coverage needs. Update your policy to reflect these changes and avoid gaps in protection.

Conclusion

Full coverage car insurance isn’t a single product—it’s a smart combination of liability, collision, and comprehensive coverage that offers broad protection for you, your vehicle, and others on the road. While it doesn’t cover every possible scenario, it significantly reduces your financial risk in most driving situations.

Whether you’re required to carry it by a lender or choosing it for peace of mind, understanding what full coverage includes—and what it excludes—helps you make informed decisions. By customizing your policy, choosing the right deductibles, and taking advantage of discounts, you can get the protection you need at a price you can afford.

Remember, the goal isn’t just to meet legal requirements—it’s to drive with confidence, knowing you’re prepared for the unexpected. So take the time to review your policy, ask questions, and ensure your coverage truly matches your needs. Your future self will thank you.

Frequently Asked Questions

Is full coverage car insurance required by law?

No, full coverage is not legally required in most states. However, if you’re financing or leasing a vehicle, your lender will typically require it to protect their investment.

Does full coverage include rental car reimbursement?

Not automatically. Rental reimbursement is an optional add-on that pays for a rental car while your vehicle is being repaired after a covered claim. You’ll need to add it to your policy.

Will full coverage pay for my medical bills if I’m injured in an accident?

Only if you have Personal Injury Protection (PIP) or Medical Payments (MedPay) coverage. Standard full coverage includes liability, collision, and comprehensive—but not medical coverage for you.

Can I drop full coverage on an older car?

Yes, if your car’s value is low and you can afford to repair or replace it out of pocket. Dropping collision and comprehensive on older vehicles can save money, but weigh the risks carefully.

What happens if my car is totaled and I owe more than it’s worth?

Your insurance will pay the car’s actual cash value, not the loan balance. If there’s a gap, you’ll owe the difference—unless you have gap insurance, which covers that shortfall.

Does full coverage protect against uninsured drivers?

Only if you add uninsured/underinsured motorist coverage. This optional protection pays for your damages if you’re hit by a driver with no or insufficient insurance.