What Is a Declaration Page for Car Insurance

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is a Declaration Page for Car Insurance?

- 4 Why the Declaration Page Matters

- 5 Key Information Found on a Declaration Page

- 6 How to Access Your Declaration Page

- 7 When Should You Review Your Declaration Page?

- 8 Common Mistakes to Avoid

- 9 How to Use Your Declaration Page in Real-Life Situations

- 10 Tips for Managing Your Declaration Page

- 11 Conclusion

- 12 Frequently Asked Questions

A declaration page for car insurance is your policy’s summary sheet, listing essential details like coverage types, limits, deductibles, and vehicle information. It’s a crucial document for understanding your protection and proving coverage when needed.

Key Takeaways

- What It Is: The declaration page is the first page of your car insurance policy, summarizing key coverage details in one place.

- Why It Matters: It proves you have insurance, helps you understand your coverage, and is required for vehicle registration and accidents.

- Key Information Included: Your name, vehicle details, policy number, coverage types, limits, deductibles, and effective dates.

- How to Access It: You can find it in your insurance binder, online account, or mobile app—usually the first page after logging in.

- When to Review It: Check it at renewal, after changes, or before buying a new car to ensure your coverage fits your needs.

- Common Mistakes to Avoid: Ignoring updates, misunderstanding coverage limits, or failing to verify driver listings can lead to gaps in protection.

- Pro Tip: Keep a digital and printed copy handy—especially when driving, renting a car, or filing a claim.

📑 Table of Contents

- What Is a Declaration Page for Car Insurance?

- Why the Declaration Page Matters

- Key Information Found on a Declaration Page

- How to Access Your Declaration Page

- When Should You Review Your Declaration Page?

- Common Mistakes to Avoid

- How to Use Your Declaration Page in Real-Life Situations

- Tips for Managing Your Declaration Page

- Conclusion

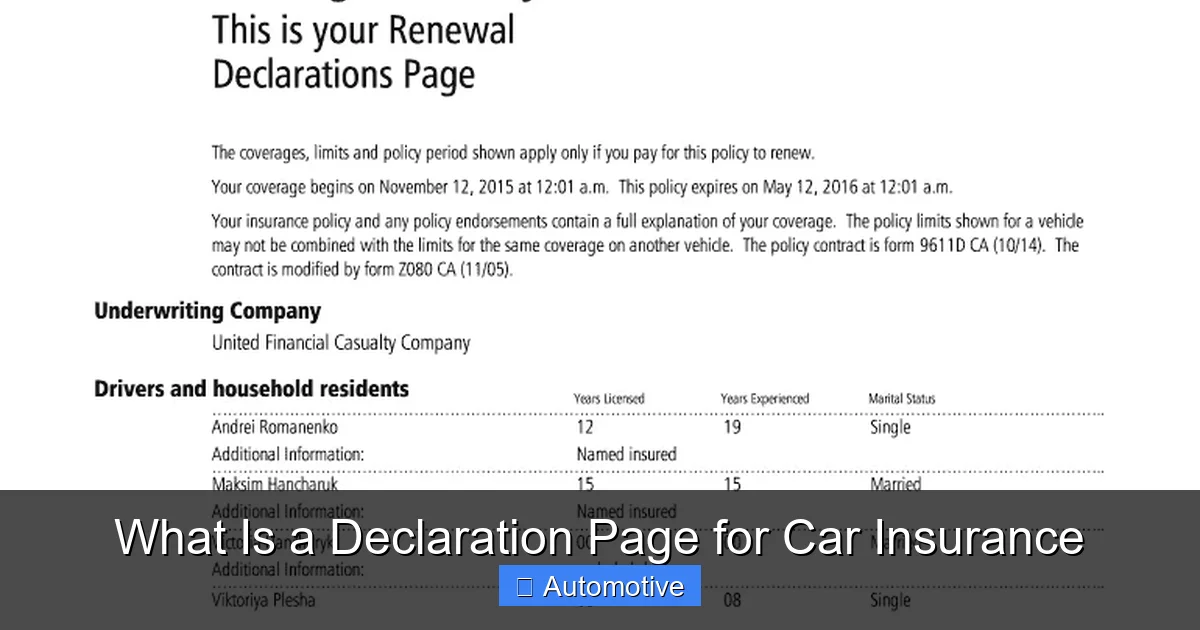

What Is a Declaration Page for Car Insurance?

If you’ve ever looked through your car insurance documents, you’ve probably seen a page titled “Declarations” or “Declarations Page.” It might look like a simple summary, but this one page holds the key to understanding your entire auto insurance policy. Think of it as your insurance ID card—but with way more detail.

The declaration page for car insurance is essentially the front page of your policy. It’s where your insurer lists all the important facts about your coverage in a clear, easy-to-read format. Whether you’re filing a claim, registering your car, or just trying to figure out how much you’re actually protected for, this page is your go-to resource.

Unlike the long, legal-heavy policy documents that can run dozens of pages, the declaration page cuts through the jargon. It gives you the essentials: who’s covered, what vehicles are included, what types of coverage you have, how much you’re paying, and when your policy starts and ends. It’s designed to be practical, not overwhelming.

Why the Declaration Page Matters

Visual guide about What Is a Declaration Page for Car Insurance

Image source: i.pinimg.com

You might be thinking, “I have my insurance card—why do I need this?” Great question. While your insurance card proves you have coverage at a glance, the declaration page tells the full story. It’s the difference between knowing you have a phone and knowing how to use all its features.

First, it’s your proof of insurance—but with depth. When you get pulled over, involved in an accident, or register your vehicle, authorities often ask for more than just the card. They may want to see the declaration page to verify coverage types and limits. Without it, you might face delays or even fines.

Second, it helps you understand what you’re actually paying for. Many drivers don’t realize they’re underinsured until it’s too late. The declaration page lays out your liability limits, collision and comprehensive deductibles, and optional add-ons like roadside assistance or rental reimbursement. This clarity helps you make informed decisions about your coverage.

Third, it’s essential during claims. When you file a claim, the adjuster will refer to your declaration page to determine what’s covered and how much you’re entitled to. If there’s a dispute about coverage, this page is the starting point for resolution.

Finally, it’s a tool for financial planning. By reviewing your declaration page regularly, you can spot changes in premiums, identify unnecessary coverage, or adjust your policy to better fit your lifestyle—like lowering coverage on an older car or adding protection for a new teen driver.

Key Information Found on a Declaration Page

Visual guide about What Is a Declaration Page for Car Insurance

Image source: signnow.com

Now that you know why it’s important, let’s break down what you’ll typically find on a declaration page for car insurance. While formats can vary slightly between insurers, the core elements remain consistent.

Policyholder Information

At the top of the page, you’ll see your name, address, and contact details. This confirms that the policy is issued to you. If you’re married or have a co-signer, their name may also appear here. It’s important to double-check this information—especially after a move or name change—to avoid issues during claims or renewals.

Policy Number and Effective Dates

Your policy number is a unique identifier used by your insurer to track your account. You’ll need it for every interaction, from filing a claim to updating your coverage. The effective dates show when your policy starts and ends. Most policies run for six or twelve months, so keep an eye on the expiration date to avoid lapses in coverage.

Vehicle Details

This section lists every vehicle covered under the policy. For each car, you’ll see the year, make, model, and vehicle identification number (VIN). Some insurers also include the vehicle’s usage (e.g., personal, business, or commuting) and annual mileage estimate. This helps determine your risk profile and premium.

Coverage Types and Limits

This is the heart of the declaration page. It outlines the types of coverage you’ve purchased and the maximum amounts your insurer will pay. Common coverage types include:

- Liability Coverage: Covers bodily injury and property damage you cause to others. Limits are usually shown as three numbers (e.g., 100/300/100), meaning $100,000 per person for injury, $300,000 per accident for injury, and $100,000 for property damage.

- Collision Coverage: Pays for damage to your car from a crash, regardless of fault. You’ll see the deductible amount (e.g., $500), which is what you pay out of pocket before insurance kicks in.

- Comprehensive Coverage: Covers non-collision incidents like theft, vandalism, fire, or weather damage. Also includes a deductible.

- Personal Injury Protection (PIP) or Medical Payments: Helps cover medical expenses for you and your passengers, regardless of fault. Required in some states.

- Uninsured/Underinsured Motorist Coverage: Protects you if you’re hit by a driver with no insurance or insufficient coverage.

Premium Breakdown

This section shows how much you’re paying for each type of coverage. It may be broken down by vehicle or listed as a total. Some insurers also show discounts applied, such as for safe driving, multi-car policies, or anti-theft devices. Understanding this breakdown helps you see where your money is going and identify opportunities to save.

Named Insured and Additional Drivers

The declaration page lists all drivers covered under the policy. This includes you (the named insured) and any other household members or frequent drivers. If someone isn’t listed, they may not be covered—even if they live with you. It’s important to add or remove drivers as your household changes to avoid coverage gaps or unexpected premiums.

How to Access Your Declaration Page

Visual guide about What Is a Declaration Page for Car Insurance

Image source: i2.wp.com

Gone are the days when you had to wait for a paper copy in the mail. Today, most insurers offer easy ways to access your declaration page.

Online Account or Mobile App

The fastest way to get your declaration page is through your insurer’s website or mobile app. After logging in, look for a section labeled “Policy Documents,” “My Coverage,” or “Documents.” The declaration page is usually the first document listed. You can view, download, or print it instantly.

Many apps also allow you to save a digital copy to your phone’s wallet or cloud storage. This is especially handy when you’re on the road and need to show proof of insurance.

Insurance Binder

When you first purchase a policy or make significant changes, your insurer may send an insurance binder—a temporary document that includes your declaration page. It’s valid until your official policy documents arrive. Keep this binder in your glove compartment until you receive the full policy.

Customer Service

If you can’t find your declaration page online, call your insurer’s customer service line. They can email or mail you a copy right away. Be ready to verify your identity with your policy number, driver’s license, or other personal information.

Email or Mail

Some insurers automatically email your declaration page at renewal or after updates. Others may send it by mail. If you prefer digital copies, make sure your email address is up to date in your account settings.

When Should You Review Your Declaration Page?

Your declaration page isn’t a “set it and forget it” document. It should be reviewed regularly to ensure it reflects your current needs and circumstances.

At Policy Renewal

Every time your policy renews—typically every six or twelve months—take a few minutes to review your declaration page. Look for changes in premiums, coverage limits, or deductibles. Ask yourself: Are my limits still adequate? Have my driving habits changed? Do I still need all the coverage I’m paying for?

For example, if you’ve paid off your car loan, you might consider dropping collision and comprehensive coverage on an older vehicle. Or if you’ve started driving more for work, you may need higher liability limits.

After Life Changes

Major life events can impact your insurance needs. Review your declaration page after:

- Buying or selling a car

- Moving to a new state or city

- Adding or removing a driver (e.g., a teen getting a license)

- Getting married or divorced

- Changing jobs or commuting distance

Each of these can affect your risk profile and coverage requirements. For instance, adding a young driver will likely increase your premium, so you may want to shop around or adjust coverage to manage costs.

Before Filing a Claim

If you’re involved in an accident or experience damage, check your declaration page before calling your insurer. It will help you understand what’s covered and what your out-of-pocket costs might be. For example, if you have a $1,000 deductible and the repair estimate is $800, it may not make sense to file a claim.

When Renting a Car

If you’re renting a car, your personal auto insurance may extend to the rental vehicle—but only if your policy includes collision and comprehensive coverage. Check your declaration page to confirm. Some credit cards also offer rental car insurance, but it often has limitations.

Common Mistakes to Avoid

Even experienced drivers can make errors when it comes to their declaration page. Here are some common pitfalls and how to avoid them.

Ignoring Updates

Your insurer may send updated declaration pages after changes to your policy. Don’t toss them in a drawer. Review them to ensure the changes are correct. For example, if you requested a lower deductible but the page still shows the old amount, contact your agent right away.

Misunderstanding Coverage Limits

Many drivers assume “full coverage” means they’re protected for everything. But “full coverage” typically refers to having liability, collision, and comprehensive—not unlimited protection. Your limits still apply. If you cause an accident with $500,000 in damages but only have $100,000 in liability, you could be personally responsible for the difference.

Failing to Add New Drivers

If your teen gets their license or a family member starts driving your car regularly, they should be added to your policy. Driving without being listed can result in a denied claim or policy cancellation. Even occasional drivers should be disclosed if they live in your household.

Overlooking Discounts

Your declaration page shows which discounts you’re receiving. If you’ve installed anti-theft devices, completed a defensive driving course, or bundled home and auto insurance, make sure those discounts are applied. If not, ask your insurer why.

Keeping Outdated Information

If you’ve moved, changed your name, or sold a car, update your policy immediately. Outdated information can delay claims or cause coverage issues. Most insurers allow you to make changes online or over the phone.

How to Use Your Declaration Page in Real-Life Situations

Let’s look at a few practical examples of how the declaration page can help you in everyday scenarios.

Getting Pulled Over

Imagine you’re driving and get pulled over for a broken taillight. The officer asks for proof of insurance. You hand over your insurance card—but they also ask to see your declaration page to verify coverage types and limits. Having a digital copy on your phone saves time and avoids confusion.

Filing a Claim After an Accident

You’re rear-ended at a stoplight. The other driver is at fault, but their insurance is slow to respond. You check your declaration page and see you have uninsured motorist coverage with a $250 deductible. You file a claim with your own insurer, who covers the repairs minus the deductible. Without that coverage, you’d be stuck paying out of pocket.

Buying a New Car

You just bought a new SUV and want to make sure it’s covered. You check your declaration page and see that your policy includes a “newly acquired vehicle” clause, which provides temporary coverage for 14–30 days. You contact your insurer to add the new car permanently, using the VIN and details from the declaration page.

Renting a Car on Vacation

You’re heading on a road trip and need to rent a car. You check your declaration page and confirm you have collision and comprehensive coverage. You decline the rental company’s insurance, saving $25 per day. But you also note your deductible is $1,000, so you consider buying a damage waiver for peace of mind.

Tips for Managing Your Declaration Page

To get the most out of your declaration page, follow these best practices:

- Store it securely: Keep a printed copy in your glove compartment and a digital copy in your phone or cloud storage.

- Review it annually: Make it a habit to check your declaration page at least once a year, especially before renewal.

- Share with family: If other drivers in your household use your car, make sure they understand the coverage limits and deductibles.

- Ask questions: If something on the page is unclear, don’t guess—call your agent or insurer for clarification.

- Update promptly: Notify your insurer of any changes to your vehicle, address, or drivers as soon as they happen.

Conclusion

The declaration page for car insurance may seem like just another piece of paperwork, but it’s one of the most important documents in your vehicle. It’s your policy’s summary, your proof of coverage, and your guide to understanding what you’re paying for. By taking the time to read, review, and understand it, you can avoid costly mistakes, make smarter insurance decisions, and drive with confidence.

Whether you’re a new driver or a seasoned pro, don’t underestimate the power of this single page. Keep it accessible, keep it updated, and use it as a tool to protect yourself, your family, and your vehicle. After all, insurance isn’t just about meeting legal requirements—it’s about peace of mind on every mile of the road.

Frequently Asked Questions

What is a declaration page for car insurance?

A declaration page is the summary sheet of your car insurance policy. It lists key details like your name, vehicle information, coverage types, limits, deductibles, and policy dates. It’s often the first page of your policy documents.

Do I need to carry my declaration page in my car?

While most states only require an insurance card, having your declaration page handy can be helpful during traffic stops, accidents, or vehicle registration. A digital copy on your phone is a smart backup.

Can I get a copy of my declaration page online?

Yes, most insurers allow you to download or view your declaration page through their website or mobile app. Log in to your account and look under “Policy Documents” or “My Coverage.”

How often should I review my declaration page?

Review it at least once a year, especially at renewal. Also check it after major life changes like buying a car, moving, or adding a driver to ensure your coverage is up to date.

What if my declaration page has incorrect information?

Contact your insurance agent or customer service immediately. Errors in your name, vehicle details, or coverage can lead to claim denials or legal issues. Most insurers can correct mistakes quickly.

Does the declaration page show my deductible?

Yes, it lists the deductible amounts for collision and comprehensive coverage. This is the amount you pay out of pocket before your insurance covers the rest of a claim.