What Is Collision Coverage in Car Insurance?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is Collision Coverage in Car Insurance?

- 4 How Does Collision Coverage Work?

- 5 When Is Collision Coverage Required?

- 6 How Much Does Collision Coverage Cost?

- 7 Should You File a Collision Claim?

- 8 Collision Coverage vs. Other Types of Auto Insurance

- 9 Common Misconceptions About Collision Coverage

- 10 Final Thoughts: Is Collision Coverage Right for You?

- 11 Frequently Asked Questions

Bluetooth FM Transmitter

Car Neck Pillow

Car Battery Tester

Car Window Tint Film

Collision coverage pays for repairs to your car after a crash—whether you hit another vehicle, a tree, or a guardrail. It’s often required if you lease or finance your car and helps cover damage regardless of who’s at fault. This coverage is key to protecting your investment and staying financially secure on the road.

Key Takeaways

- Collision coverage pays for damage to your vehicle after an accident: It covers repairs when your car collides with another vehicle, object, or even flips over—regardless of fault.

- It’s different from liability and comprehensive coverage: Liability covers others’ damages; comprehensive handles non-collision events like theft or weather. Collision is specifically for crash-related damage.

- Often required for leased or financed vehicles: Lenders and leasing companies typically require collision coverage until the loan is paid off to protect their financial interest.

- You choose your deductible: Higher deductibles lower your premium, but you pay more out of pocket if you file a claim.

- Not always worth it for older or low-value cars: If repair costs exceed your car’s value minus the deductible, it may be smarter to drop the coverage.

- Can be combined with other coverages for full protection: Pairing collision with comprehensive and uninsured motorist coverage gives you well-rounded protection.

- Filing a claim may affect future premiums: Even if you’re not at fault, some insurers may raise rates after a collision claim, so weigh the cost before filing.

📑 Table of Contents

- What Is Collision Coverage in Car Insurance?

- How Does Collision Coverage Work?

- When Is Collision Coverage Required?

- How Much Does Collision Coverage Cost?

- Should You File a Collision Claim?

- Collision Coverage vs. Other Types of Auto Insurance

- Common Misconceptions About Collision Coverage

- Final Thoughts: Is Collision Coverage Right for You?

What Is Collision Coverage in Car Insurance?

Imagine you’re driving home from work on a rainy evening. You’re stopped at a red light, focused on the road ahead. Suddenly, the car behind you slams into your bumper. Your heart races. Your car is damaged. Now what?

This is where collision coverage in car insurance comes into play. It’s one of the most important—and often misunderstood—parts of your auto policy. While liability insurance covers damage you cause to others, collision coverage protects your own vehicle when you’re involved in a crash.

In simple terms, collision coverage pays to repair or replace your car if it’s damaged in an accident with another vehicle or object—like a tree, pole, or even a pothole. And here’s a key point: it doesn’t matter who’s at fault. Whether you rear-ended someone or were hit from behind, collision coverage steps in to help cover the cost of repairs.

But it’s not automatic. You have to add it to your policy, and it comes with a deductible—the amount you pay out of pocket before insurance kicks in. For example, if you have a $500 deductible and $3,000 in damage, you pay $500, and your insurer covers the remaining $2,500.

Collision coverage is especially valuable if you drive a newer or more expensive vehicle. Repairing or replacing a modern car can cost thousands of dollars, and without this coverage, you’d be on the hook for the full amount. Even if you’re not at fault, the other driver’s insurance might take time to respond—or they might be uninsured. Collision coverage gives you peace of mind and faster access to repairs.

How Does Collision Coverage Work?

Visual guide about What Is Collision Coverage in Car Insurance?

Image source: carinsurance.org

So, how exactly does collision coverage function when you need it most? Let’s break it down step by step.

When you’re in an accident—whether it’s a fender bender in a parking lot or a more serious collision on the highway—your first step is to contact your insurance company. Most insurers have 24/7 claims lines, so you can report the incident right away.

Once you file a claim, an adjuster will be assigned to assess the damage. They’ll inspect your vehicle, either in person or through photos and estimates from a repair shop. Based on their evaluation, they’ll determine the cost of repairs.

Here’s where your deductible comes into play. Let’s say your car has $4,000 in damage and your deductible is $1,000. You pay the first $1,000, and your insurer covers the remaining $3,000. The insurance company will typically send a check to the repair shop or directly to you, depending on your policy and the shop’s requirements.

It’s important to note that collision coverage only pays up to the actual cash value (ACV) of your car at the time of the accident. ACV factors in depreciation—so if your car is five years old, it’s worth less than when it was new. If the cost to repair your car exceeds its ACV minus your deductible, the insurer may declare it a total loss and pay you the car’s market value instead.

For example, if your car is worth $8,000 and the repair estimate is $7,500 with a $1,000 deductible, the insurer might total the car and give you $7,000 ($8,000 minus $1,000). You could then use that money to buy a replacement vehicle.

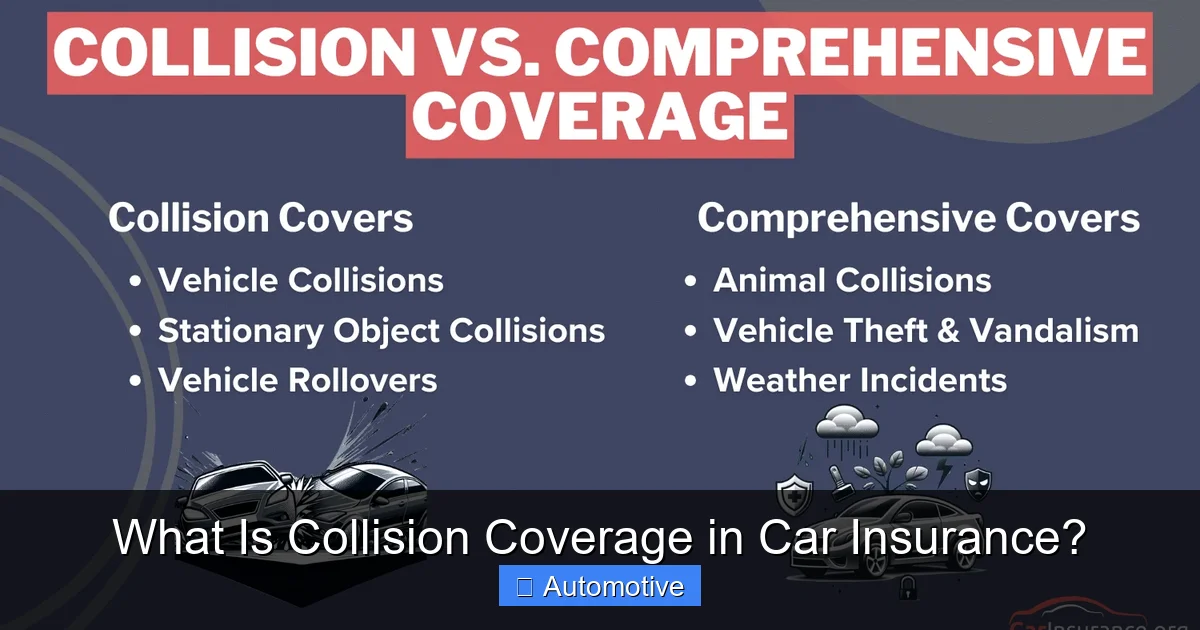

What Types of Accidents Are Covered?

Collision coverage is designed to handle a wide range of accidents. Here are some common scenarios where it applies:

- Hitting another vehicle: Whether you rear-end someone at a stoplight or get T-boned at an intersection, collision coverage pays for your car’s damage.

- Hitting a stationary object: Crashing into a tree, fence, mailbox, or guardrail? Covered.

- Rolling your car: If your vehicle flips over due to a collision, collision coverage applies.

- Single-vehicle accidents: Even if no other car is involved—like sliding off the road in icy conditions—your collision coverage still kicks in.

It’s worth noting that collision coverage does not cover damage from non-collision events. For example, if a hailstorm dents your roof or a thief breaks your window, that’s where comprehensive coverage comes in. But if you swerve to avoid a deer and hit a curb, damaging your suspension, that’s a collision—and it’s covered.

Is Collision Coverage the Same as Comprehensive?

This is a common point of confusion. While both collision and comprehensive are optional coverages that protect your vehicle, they cover very different types of incidents.

Collision coverage is all about crashes—your car hitting something or being hit. Comprehensive coverage, on the other hand, handles “other-than-collision” events. This includes:

- Theft or vandalism

- Fire or explosion

- Falling objects (like tree branches)

- Weather-related damage (hail, flooding, wind)

- Animal collisions (hitting a deer or dog)

So, if a tree falls on your car during a storm, comprehensive pays. If you hit the tree while driving, collision pays. They work together to give you full protection, but they’re not interchangeable.

Many drivers choose to bundle both coverages for complete peace of mind. This combination is often referred to as “full coverage,” though that’s not an official insurance term—it just means you have more than just liability.

When Is Collision Coverage Required?

Visual guide about What Is Collision Coverage in Car Insurance?

Image source: carinsurance.org

You might be wondering: do I really need collision coverage? The answer depends on your situation.

Leased or Financed Vehicles

If you’re leasing or financing your car, the answer is almost always yes. Lenders and leasing companies require collision (and usually comprehensive) coverage to protect their financial interest in the vehicle. If your car is damaged or totaled, they want to ensure it can be repaired or replaced so the loan can be repaid.

For example, if you have a $20,000 loan on a car and it’s totaled in an accident, the insurance payout helps cover that debt. Without collision coverage, you’d still owe the lender money—even if you no longer have the car.

Most lenders require you to maintain this coverage until the loan is fully paid off. If you drop it, they may add it back to your policy and charge you for it—often at a higher rate.

Owners of Newer or High-Value Cars

Even if you own your car outright, collision coverage makes sense if your vehicle is relatively new or has a high market value. Repairing a modern car with advanced safety features, sensors, and electronics can be extremely expensive. A single accident could cost thousands—money you might not have on hand.

For instance, replacing a damaged bumper on a luxury SUV might cost $2,500 or more. Without collision coverage, that’s coming straight out of your pocket.

Older or Low-Value Vehicles

On the flip side, if you drive an older car with low market value—say, a 15-year-old sedan worth $3,000—collision coverage might not be worth the cost. Insurance premiums for collision can be $200–$500 per year or more, depending on your deductible and location.

If your car is only worth $3,000 and you have a $1,000 deductible, the maximum payout in a total loss would be $2,000. Over five years, you could pay $1,000–$2,500 in premiums just to potentially recover $2,000. In this case, it might make more financial sense to drop collision and self-insure—meaning you’d pay for any repairs yourself.

A good rule of thumb: if your annual collision premium is more than 10% of your car’s value, it may be time to reconsider.

How Much Does Collision Coverage Cost?

Visual guide about What Is Collision Coverage in Car Insurance?

Image source: westsidecollision.com

The cost of collision coverage varies widely based on several factors. Understanding these can help you make an informed decision and possibly save money.

Factors That Affect Premiums

- Vehicle make and model: Sports cars and luxury vehicles cost more to insure because they’re expensive to repair and more likely to be involved in accidents.

- Your driving record: Safe drivers with no accidents or tickets typically pay less. A history of collisions or violations can significantly increase your rate.

- Location: Urban areas with heavy traffic and higher accident rates tend to have higher premiums than rural areas.

- Age and experience: Younger, less experienced drivers often pay more due to higher risk.

- Deductible amount: Choosing a higher deductible (e.g., $1,000 instead of $500) lowers your premium, but increases your out-of-pocket cost if you file a claim.

- Coverage limits: While collision doesn’t have a “limit” like liability, the payout is capped at your car’s actual cash value.

On average, collision coverage adds $200–$600 per year to your premium. But in high-risk areas or for expensive cars, it could be much more.

Tips to Save on Collision Coverage

- Raise your deductible: If you have savings to cover a higher out-of-pocket cost, increasing your deductible can reduce your premium by 15–30%.

- Bundle policies: Many insurers offer discounts if you bundle auto with home or renters insurance.

- Maintain a clean driving record: Safe driving can lead to discounts and lower rates over time.

- Ask about discounts: Good student, low mileage, anti-theft device, and defensive driving course discounts can all help.

- Shop around annually: Rates change, so comparing quotes from multiple insurers can save you hundreds.

Should You File a Collision Claim?

Deciding whether to file a claim can be tricky. While collision coverage is there to help, filing a claim isn’t always the best move—especially for minor damage.

When to File a Claim

- Significant damage: If repairs cost more than your deductible, it usually makes sense to file.

- Safety concerns: If the damage affects your car’s safety (brakes, steering, airbags), get it fixed immediately.

- You’re not at fault: If the other driver is clearly responsible and their insurance is slow to respond, your collision coverage can get you back on the road faster.

When to Pay Out of Pocket

- Minor damage under your deductible: If the repair costs $400 and your deductible is $500, filing a claim won’t help—you’d pay the full amount anyway.

- Risk of rate increases: Some insurers raise rates after any claim, even if you’re not at fault. Check your policy or ask your agent.

- Older car with low value: If your car isn’t worth much, a claim might not be worth the hassle or potential premium hike.

A good strategy: get a repair estimate first. Compare it to your deductible and consider the long-term impact on your insurance rates before deciding.

Collision Coverage vs. Other Types of Auto Insurance

To fully understand collision coverage, it helps to see how it fits into the bigger picture of auto insurance.

Liability Coverage

This is the foundation of every auto policy and is required in almost every state. It covers damage and injuries you cause to others in an accident. For example, if you run a red light and hit another car, liability pays for their car repairs and medical bills—but not yours.

Collision coverage, in contrast, protects your own vehicle. You can have liability without collision, but not the other way around (in most cases).

Comprehensive Coverage

As mentioned earlier, comprehensive covers non-collision events. Think of it as “everything else” that can damage your car. While collision handles crashes, comprehensive handles nature, theft, and vandalism.

Uninsured/Underinsured Motorist Coverage

This protects you if you’re hit by a driver with no insurance or insufficient coverage. It can pay for your medical bills and sometimes vehicle damage—depending on your state.

Personal Injury Protection (PIP)

Available in some states, PIP covers medical expenses for you and your passengers, regardless of fault. It’s often paired with collision for full protection.

Gap Insurance

If you have a loan or lease, gap insurance covers the “gap” between what your car is worth and what you owe if it’s totaled. Collision pays the car’s value, but gap insurance covers the rest of your loan.

For example, if your car is worth $15,000 but you owe $20,000, collision pays $15,000. Gap insurance covers the remaining $5,000.

Common Misconceptions About Collision Coverage

Despite its importance, collision coverage is often misunderstood. Let’s clear up some common myths.

Myth 1: “I Don’t Need Collision If I’m a Good Driver”

Even the safest drivers can be involved in accidents—especially if someone else is at fault. Collision coverage protects you from others’ mistakes, not just your own.

Myth 2: “My Insurance Will Always Pay for Repairs”

Insurance only pays up to your car’s actual cash value minus your deductible. If repairs exceed that amount, your car may be declared a total loss.

Myth 3: “Collision Coverage Pays for Everything”

It doesn’t cover mechanical failures, normal wear and tear, or damage from non-collision events. Those fall under comprehensive or warranty coverage.

Myth 4: “I Can’t Drop Collision Once I Add It”

You can drop collision coverage at any time—unless you have a loan or lease that requires it. Just be sure it makes financial sense.

Myth 5: “Filing a Claim Always Raises My Rates”

Not necessarily. Some insurers offer accident forgiveness or don’t raise rates for not-at-fault claims. Check with your provider.

Final Thoughts: Is Collision Coverage Right for You?

Collision coverage in car insurance is a powerful tool for protecting your vehicle and your wallet. It gives you the freedom to drive with confidence, knowing that if the unexpected happens, you’re not left paying the full cost of repairs.

But it’s not a one-size-fits-all solution. If you drive a newer car, have a loan, or live in a high-risk area, collision coverage is likely a smart investment. On the other hand, if your car is old and low-value, the cost may outweigh the benefit.

The key is to evaluate your personal situation: your car’s value, your financial cushion, your driving habits, and your risk tolerance. Talk to your insurance agent, compare quotes, and don’t be afraid to adjust your coverage as your needs change.

Remember, insurance isn’t just about meeting legal requirements—it’s about peace of mind. And when it comes to something as important as your car, that peace of mind is priceless.

Frequently Asked Questions

Do I need collision coverage if I own my car outright?

Not necessarily. If your car is older or has low market value, the cost of collision coverage may exceed the potential payout. Evaluate your car’s worth and your ability to pay for repairs out of pocket.

Does collision coverage cover rental cars?

Generally, no. Collision coverage applies to your insured vehicle. If you rent a car, you’d need separate rental reimbursement coverage or rely on your credit card’s rental insurance benefits.

Can I add collision coverage after an accident?

No. Insurance only covers future incidents, not past ones. You must have collision coverage in place before an accident occurs to file a claim.

Will my rates go up if I file a collision claim?

It depends on your insurer and whether you were at fault. Some companies offer accident forgiveness or don’t raise rates for not-at-fault claims. Ask your agent about their policy.

What happens if my car is totaled?

Your insurer will pay the actual cash value of your car minus your deductible. If you have a loan, the payout goes to the lender first. Gap insurance can cover any remaining balance.

Is collision coverage worth it for a used car?

It depends on the car’s value and your deductible. If your annual premium is more than 10% of your car’s worth, it may not be cost-effective. Consider your financial situation and risk tolerance.