How to Buy a Repossessed Car

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How to Buy a Repossessed Car: A Step-by-Step Guide

- 4 What Is a Repossessed Car?

- 5 Where to Find Repossessed Cars for Sale

- 6 How to Inspect a Repossessed Car Before Buying

- 7 Financing a Repossessed Car

- 8 Common Pitfalls and How to Avoid Them

- 9 Tips for Getting the Best Deal

- 10 Conclusion

- 11 Frequently Asked Questions

Buying a repossessed car can save you up to 50% off market value, but it requires research, caution, and smart timing. This guide walks you through every step—from finding repo listings to inspecting the vehicle and closing the deal—so you can drive away with a reliable ride at a fraction of the cost.

Key Takeaways

- Repossessed cars are often priced below market value: Banks and lenders sell repossessed vehicles quickly, which means lower prices for buyers.

- You can find repo cars through banks, auctions, and government sites: Major lenders like Chase, Wells Fargo, and the U.S. Treasury list repossessed vehicles online.

- Always inspect the car before buying: Many repo cars are sold “as-is,” so a pre-purchase inspection is essential to avoid hidden problems.

- Timing matters—buy at the right time for the best deals: End-of-month, end-of-quarter, and year-end sales often feature deeper discounts.

- Financing may be trickier but is possible: While some buyers pay cash, you can still get financing through credit unions or online lenders.

- Watch out for hidden fees and paperwork issues: Repossessed vehicles may have liens, back taxes, or title complications that need resolving.

- Private repo sales can offer better deals than auctions: Some lenders sell directly to the public, cutting out auction middlemen and lowering costs.

📑 Table of Contents

How to Buy a Repossessed Car: A Step-by-Step Guide

If you’re looking to save serious money on your next vehicle, buying a repossessed car might be one of the smartest moves you can make. Repossessed vehicles—also known as “repo cars”—are cars that lenders have taken back from owners who failed to make payments. These cars are often sold quickly and at steep discounts, sometimes up to 50% below market value. That means a $20,000 sedan could go for $10,000 or less.

But here’s the catch: buying a repossessed car isn’t as simple as walking into a dealership and driving off in a shiny new ride. These vehicles come with risks. They may have been neglected, driven hard, or even damaged. Plus, the buying process can be more complex than a standard car purchase. You might deal with banks, auctions, or government agencies, and each has its own rules.

That’s why it’s crucial to go in with a plan. In this guide, we’ll walk you through everything you need to know—from where to find repossessed cars, how to inspect them, and how to avoid common pitfalls. Whether you’re a first-time buyer or a seasoned car shopper, this guide will help you navigate the repo car market with confidence.

What Is a Repossessed Car?

Visual guide about How to Buy a Repossessed Car

Image source: thepanda.co.za

A repossessed car is a vehicle that has been taken back by a lender—usually a bank, credit union, or finance company—because the owner defaulted on their loan payments. When someone stops making payments, the lender has the legal right to reclaim the vehicle under the terms of the loan agreement. This process is called repossession.

Once the car is repossessed, the lender’s goal is to recover as much of the outstanding loan balance as possible. To do this quickly, they often sell the car at a discount. That’s where you come in. Because these vehicles are sold fast, they’re frequently priced well below what you’d pay at a dealership.

But not all repossessed cars are created equal. Some may have been well-maintained and only repossessed due to financial hardship. Others might have been driven hard, neglected, or even damaged during the repossession process. That’s why it’s so important to do your homework before handing over any cash.

Why Do Lenders Repossess Cars?

Lenders repossess cars primarily to minimize their financial losses. When a borrower stops making payments, the lender risks losing thousands of dollars. By reclaiming the vehicle, they can sell it and recoup some of that money.

Common reasons for repossession include:

- Missed or late payments over several months

- Defaulting on the loan agreement

- Filing for bankruptcy

- Failing to maintain required insurance

In most cases, repossession happens without warning. A repo agent may tow the car from your driveway, workplace, or even a parking lot. Once the car is in the lender’s possession, they’ll typically send a notice to the former owner and begin the process of selling it.

Types of Repossessed Vehicles

Repossessed cars come in all shapes and sizes. You might find everything from compact sedans and SUVs to trucks, minivans, and even luxury vehicles. The type of car available depends on what people were driving before they defaulted on their loans.

Some common categories include:

- Economy cars: Like Honda Civics, Toyota Corollas, and Ford Focuses—often well-maintained and fuel-efficient.

- SUVs and crossovers: Such as Toyota RAV4s, Honda CR-Vs, and Ford Explorers—popular with families and often in good condition.

- Trucks: Like Ford F-150s, Chevrolet Silverados, and Ram 1500s—frequently used for work and may show wear.

- Luxury vehicles: Including BMWs, Mercedes-Benz, and Audis—can be high-mileage or have mechanical issues.

Keep in mind that while luxury cars might look appealing, they often come with higher maintenance costs. A repossessed BMW might save you $10,000 upfront, but a single repair could cost $2,000 or more.

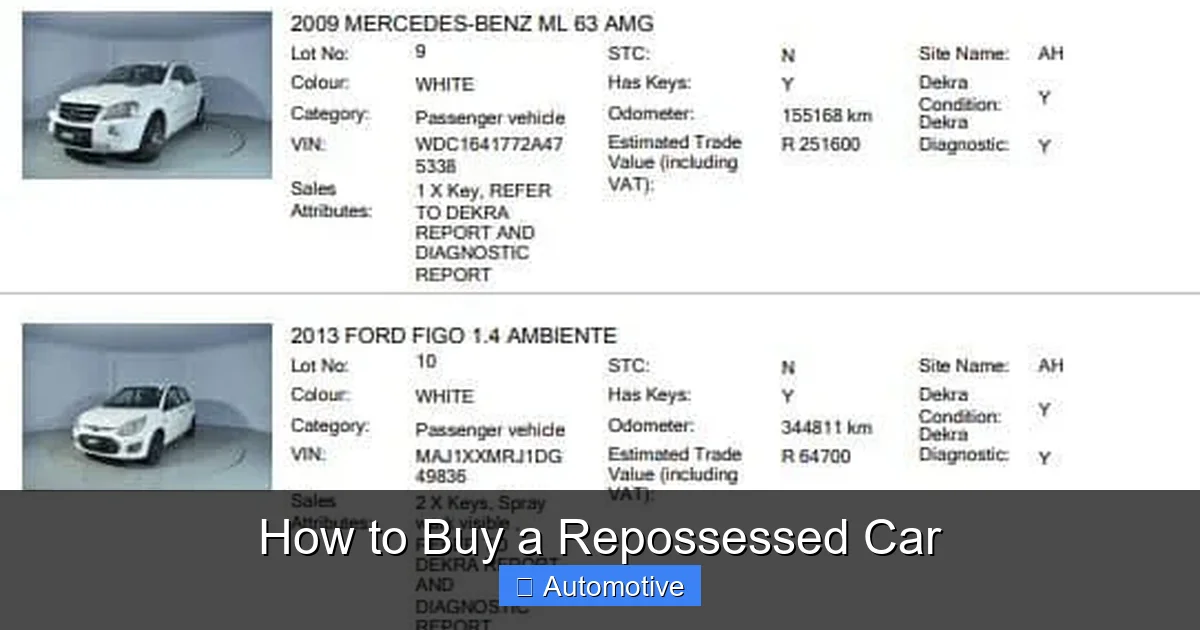

Where to Find Repossessed Cars for Sale

Visual guide about How to Buy a Repossessed Car

Image source: uturnrepossessedcarsource.co.za

Now that you know what a repossessed car is, the next step is finding one to buy. The good news is that there are several reliable sources where you can search for repo vehicles. The key is knowing where to look and how to access these listings.

Banks and Credit Unions

Many major banks and credit unions sell repossessed vehicles directly to the public. These institutions often list their available cars on their websites or through third-party platforms. Some even host online auctions.

Examples include:

- Chase Bank: Offers repossessed vehicles through its “Chase Auto” portal. You can filter by make, model, price, and location.

- Wells Fargo: Lists repossessed cars on its website, with options to search by ZIP code.

- Bank of America: Sells repossessed vehicles through local branches and online listings.

- Local credit unions: Often have smaller inventories but may offer better deals due to lower overhead.

One advantage of buying from a bank is transparency. These institutions usually provide basic vehicle history reports and may allow test drives. However, they often sell cars “as-is,” meaning no warranties or guarantees.

Government Auctions

The U.S. government also sells repossessed vehicles, especially those seized by law enforcement or federal agencies. These cars are often well-maintained and come from agencies like the IRS, FBI, or Department of Defense.

You can find government repossessed cars through:

- GovDeals: A popular online auction site that lists vehicles from federal, state, and local agencies.

- USPS Auctions: The U.S. Postal Service sells repossessed vehicles on its official auction site.

- Treasury Auctions: The U.S. Department of the Treasury auctions off seized and repossessed assets, including cars.

Government auctions can be competitive, but they often feature high-quality vehicles at low prices. For example, a former police cruiser might sell for half its original value. Just be aware that bidding can get intense, and you’ll need to register in advance.

Public Auctions

Private auction houses also sell repossessed cars. These auctions are often held in person, though many now offer online bidding as well. Companies like Manheim, ADESA, and Copart specialize in vehicle auctions, including repossessed models.

Public auctions are great for finding a wide variety of vehicles, but they come with risks:

- You usually can’t test drive the car before bidding.

- Inspections may be limited or require a fee.

- Cars are sold “as-is,” with no return policy.

To increase your chances of success, arrive early, inspect the vehicle thoroughly, and set a strict budget. It’s also wise to bring a mechanic or use the auction’s inspection service.

Online Marketplaces

Websites like eBay Motors, CarGurus, and Cars.com sometimes list repossessed vehicles. These platforms allow you to filter searches by “repossessed,” “bank-owned,” or “repo” to find relevant listings.

While convenient, online marketplaces can be hit-or-miss. Some sellers may exaggerate the condition of the car or hide mechanical issues. Always request a vehicle history report (like Carfax or AutoCheck) and, if possible, arrange for an independent inspection.

How to Inspect a Repossessed Car Before Buying

Visual guide about How to Buy a Repossessed Car

Image source: shopatcarauctions.co.za

One of the biggest risks of buying a repossessed car is that it may have hidden problems. Since these vehicles are often sold “as-is,” you won’t get a warranty or return policy. That makes a thorough inspection absolutely essential.

Start with a Vehicle History Report

Before you even see the car in person, pull a vehicle history report. This document will tell you:

- Whether the car has been in any accidents

- If it has a salvage or rebuilt title

- How many previous owners it had

- Odometer readings over time

- Service and maintenance records (if available)

Services like Carfax and AutoCheck charge around $30–$40 per report, but it’s money well spent. A clean history report doesn’t guarantee the car is in perfect condition, but it helps rule out major red flags.

Conduct a Visual Inspection

When you arrive to inspect the car, bring a flashlight, notepad, and camera. Look for signs of damage, wear, or neglect.

Check the exterior for:

- Dents, scratches, or rust

- Mismatched paint (a sign of past repairs)

- Uneven tire wear (could indicate alignment issues)

- Cracked or cloudy headlights

Inside, look for:

- Stains, tears, or odors in the upholstery

- Warning lights on the dashboard

- Worn pedals or steering wheel (signs of high mileage)

- Functioning electronics (radio, AC, windows, locks)

Don’t forget to pop the hood. Check the engine for leaks, corrosion, or unusual noises. Look at the oil—dark, gritty oil could mean poor maintenance.

Take It for a Test Drive

If allowed, take the car for a test drive. Pay attention to:

- How the engine starts and idles

- Smoothness of the transmission

- Brake responsiveness

- Steering and suspension feel

- Unusual noises (knocking, squealing, grinding)

Drive on different road types—city streets, highways, and hills—to get a full sense of the car’s performance.

Get a Pre-Purchase Inspection

Even if the car looks good, always get a pre-purchase inspection (PPI) from a trusted mechanic. This typically costs $100–$150 but can save you thousands in repairs.

A good mechanic will:

- Check the engine, transmission, and drivetrain

- Inspect the suspension and brakes

- Test the electrical systems

- Look for signs of flood damage or frame issues

If the mechanic finds major problems, you can walk away or use the report to negotiate a lower price.

Financing a Repossessed Car

Many buyers assume they need to pay cash for a repossessed car, but that’s not always true. While some auctions and private sales require full payment upfront, there are financing options available.

Can You Finance a Repossessed Car?

Yes, you can finance a repossessed car, but it may be more challenging than financing a new or certified pre-owned vehicle. Lenders view repo cars as higher risk, so they may charge higher interest rates or require a larger down payment.

However, several options exist:

- Credit unions: Often offer competitive rates for used cars, including repossessed models.

- Online lenders: Companies like LightStream, Upstart, and LendingTree may finance repo cars.

- Dealer financing: Some banks and credit unions partner with auction houses to offer financing at the point of sale.

To improve your chances of approval, have a good credit score (650 or higher), a stable income, and a reasonable debt-to-income ratio.

Tips for Getting Approved

- Get pre-approved: Apply for financing before you start shopping. This gives you a clear budget and strengthens your negotiating position.

- Put down a larger down payment: A 20–30% down payment reduces the lender’s risk and may lower your interest rate.

- Choose a shorter loan term: While monthly payments will be higher, you’ll pay less in interest overall.

- Consider a co-signer: If your credit is weak, a co-signer with good credit can help you qualify.

Remember, even if you finance the car, you’ll still need to pay for taxes, registration, and insurance—so budget accordingly.

Common Pitfalls and How to Avoid Them

Buying a repossessed car can be a great deal, but it’s not without risks. Here are some common pitfalls and how to avoid them.

Buying Without an Inspection

One of the biggest mistakes buyers make is skipping the inspection. Just because a car looks clean doesn’t mean it’s mechanically sound. A $100 inspection could save you $5,000 in repairs.

Overbidding at Auction

Auctions can be exciting, but it’s easy to get caught up in the moment and overbid. Set a firm budget before you go and stick to it. Remember, you’re not just paying for the car—you’ll also need to cover towing, repairs, and registration.

Ignoring Title and Lien Issues

Some repossessed cars may still have liens, back taxes, or title problems. Always verify the title is clear before buying. Ask for a copy of the title and check it against the VIN. If there are liens, the seller must resolve them before you can register the car.

Not Researching the Market Value

Just because a car is cheap doesn’t mean it’s a good deal. Use tools like Kelley Blue Book (KBB) or Edmunds to check the fair market value. If a repossessed car is priced too low, there’s probably a reason—like high mileage or damage.

Forgetting About Hidden Costs

Beyond the purchase price, you’ll need to budget for:

- Sales tax (varies by state)

- Registration and title fees

- Insurance

- Repairs and maintenance

- Towing (if the car doesn’t run)

Add up these costs before you buy to avoid surprises.

Tips for Getting the Best Deal

With the right strategy, you can score an incredible deal on a repossessed car. Here are some proven tips to help you save even more.

Buy at the Right Time

Lenders and auction houses often offer deeper discounts at certain times of the year:

- End of the month: Sales teams may be trying to meet quotas.

- End of the quarter: Banks may want to clear inventory.

- End of the year: New models arrive, so older cars get discounted.

Shopping during these periods can give you more negotiating power.

Negotiate the Price

Even at auctions, you can sometimes negotiate—especially if the car has been sitting for a while. If you’re buying directly from a bank, ask if they’re willing to lower the price. They may say no, but it never hurts to ask.

Look for Low-Mileage Vehicles

Some repossessed cars have surprisingly low mileage, especially if the previous owner didn’t drive much. These vehicles can be excellent buys, as they’ve had less wear and tear.

Consider Fleet or Rental Cars

Many repossessed cars come from rental companies or corporate fleets. These vehicles are often well-maintained and serviced regularly. While they may have higher mileage, they’re usually in good condition.

Be Patient

The best deals don’t always come quickly. It may take weeks or even months to find the right car at the right price. But patience pays off—literally.

Conclusion

Buying a repossessed car can be a smart financial move, offering significant savings compared to traditional dealerships. With prices often 30–50% below market value, you can drive away in a reliable vehicle without breaking the bank.

But success doesn’t come automatically. It requires research, caution, and a clear plan. Start by knowing where to look—banks, government auctions, and online marketplaces are all great sources. Always inspect the car thoroughly, get a pre-purchase inspection, and verify the title is clean.

Financing is possible, even for repo cars, especially if you have good credit. And while there are risks—like hidden damage or title issues—they can be managed with the right precautions.

By following the steps in this guide, you’ll be well-equipped to navigate the world of repossessed cars and find a great deal. So don’t let the stigma of “repo” scare you away. With the right approach, that repossessed car could be the best purchase you’ve ever made.

Frequently Asked Questions

Are repossessed cars reliable?

Repossessed cars can be reliable, but it depends on their history and condition. Many are well-maintained, while others may have been neglected. Always inspect the vehicle and get a history report before buying.

Can I test drive a repossessed car?

It depends on the seller. Banks and private sellers may allow test drives, but auction houses often do not. If a test drive isn’t possible, a pre-purchase inspection is even more important.

Do repossessed cars come with a warranty?

Most repossessed cars are sold “as-is,” meaning no warranty. Some banks or dealers may offer limited warranties, but this is rare. Be prepared to cover any repairs yourself.

How do I know if a repossessed car has a clean title?

Ask for a copy of the title and verify it matches the VIN. You can also check for liens using your state’s DMV website or a service like Carfax. Avoid cars with salvage or rebuilt titles unless you’re prepared for extra paperwork.

Can I finance a repossessed car with bad credit?

It’s possible, but harder. You may need a co-signer, a larger down payment, or to work with a subprime lender. Credit unions and online lenders are good places to start.

Where can I find repossessed cars near me?

Check bank websites, government auction sites like GovDeals, and local auction houses. You can also search online marketplaces and filter for “repossessed” or “bank-owned” vehicles.