How Much Is Car Insurance for a Teenager?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Why Is Car Insurance So Expensive for Teenagers?

- 4 Average Cost of Car Insurance for a Teenager

- 5 Factors That Affect Teen Car Insurance Rates

- 6 Ways to Reduce Car Insurance Costs for Teen Drivers

- 7 Should You Buy a Separate Policy for Your Teen?

- 8 What Coverage Does a Teenager Need?

- 9 The Role of Parental Involvement in Lowering Costs

- 10 Long-Term Savings: How Rates Change as Teens Gain Experience

- 11 Conclusion

- 12 Frequently Asked Questions

Car insurance for a teenager typically costs between $5,000 and $10,000 per year—significantly more than for adult drivers. But with smart strategies like good student discounts, driver training, and choosing the right vehicle, families can reduce premiums by up to 30%.

Key Takeaways

- Teen drivers pay the highest insurance rates: Due to inexperience and higher accident risk, teens can pay 2–3 times more than adult drivers.

- Average annual cost ranges from $5,000 to $10,000: Exact pricing depends on location, vehicle type, coverage level, and driving record.

- Adding a teen to a parent’s policy is cheaper than a standalone plan: Most insurers offer multi-car and family discounts that lower overall costs.

- Good student and driver education discounts can save hundreds: Maintaining a B average or completing a certified driving course often qualifies for rate reductions.

- Vehicle choice matters: Older, safer, and less powerful cars typically cost less to insure than sports cars or luxury models.

- Usage-based insurance programs help monitor driving habits: Telematics apps can reward safe driving with lower premiums over time.

- Shop around annually: Rates vary widely between insurers, so comparing quotes each year ensures you’re getting the best deal.

📑 Table of Contents

- Why Is Car Insurance So Expensive for Teenagers?

- Average Cost of Car Insurance for a Teenager

- Factors That Affect Teen Car Insurance Rates

- Ways to Reduce Car Insurance Costs for Teen Drivers

- Should You Buy a Separate Policy for Your Teen?

- What Coverage Does a Teenager Need?

- The Role of Parental Involvement in Lowering Costs

- Long-Term Savings: How Rates Change as Teens Gain Experience

- Conclusion

Why Is Car Insurance So Expensive for Teenagers?

Let’s face it—adding your teenager to your car insurance policy is going to sting. You’ve probably seen the numbers: premiums can double or even triple when a 16-year-old gets behind the wheel. But why is car insurance for a teenager so expensive?

The short answer? Risk. Insurance companies base their rates on data, and the data shows that teen drivers are far more likely to be involved in accidents than any other age group. According to the Insurance Institute for Highway Safety (IIHS), drivers aged 16 to 19 are nearly three times more likely to be in a fatal crash than drivers over 20. This elevated risk translates directly into higher premiums.

But it’s not just about age. Inexperience plays a huge role. A 16-year-old may have passed their driving test, but they lack the real-world judgment that comes from years of navigating traffic, weather, and unexpected hazards. Combine that with distractions like smartphones, loud music, or peer passengers, and the risk skyrockets.

Another factor is the type of car teens often drive. Many start with older, high-mileage vehicles that may not have modern safety features like automatic emergency braking or lane departure warnings. While these cars are cheaper to buy, they can actually cost more to insure if they’re more prone to damage or theft.

And let’s not forget liability. If a teen causes an accident, the financial responsibility falls on the policyholder—usually the parents. Insurers know this and charge accordingly to cover potential claims.

So yes, car insurance for a teenager is expensive. But understanding why helps you make smarter decisions. The good news? There are proven ways to lower those costs without sacrificing coverage.

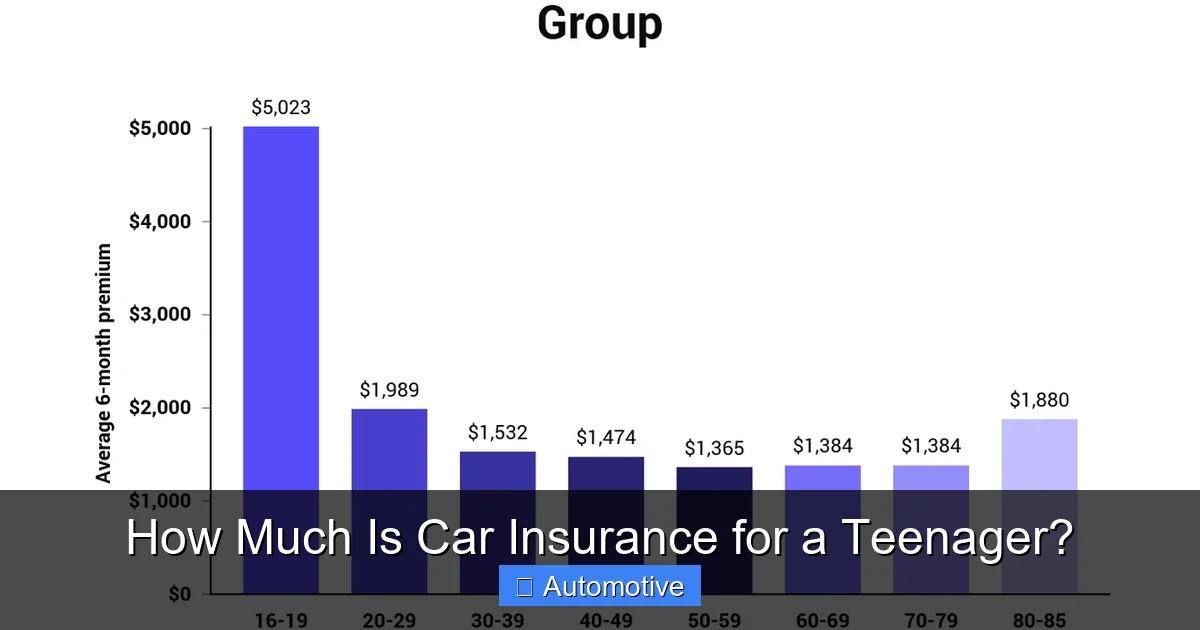

Average Cost of Car Insurance for a Teenager

Visual guide about How Much Is Car Insurance for a Teenager?

Image source: images.ctfassets.net

So, how much is car insurance for a teenager, exactly? The answer isn’t one-size-fits-all, but national averages give us a solid starting point.

On average, adding a teen driver to a parent’s policy increases annual premiums by $5,000 to $10,000. That’s a massive jump—especially when you consider that the average annual cost for an adult driver is around $1,500 to $2,500. In other words, a single teen can cost as much as four adult drivers combined.

But those numbers vary widely based on several factors. Let’s break it down.

Cost by Age and Gender

Age and gender still play a role in insurance pricing, though many states have started to limit or ban gender-based pricing due to fairness concerns.

For 16-year-old drivers, annual premiums can range from $6,000 to $12,000. By age 18, that often drops to $4,000–$7,000 as experience builds. Male teens typically pay 10–15% more than female teens of the same age, largely due to higher accident rates among young men.

For example, a 16-year-old boy in Texas might pay $8,500 per year for full coverage, while a 16-year-old girl in the same state might pay $7,200. By age 19, both might see rates drop to around $3,500–$4,000.

Cost by State

Where you live has a huge impact on insurance costs. States with high population density, strict liability laws, or expensive repair costs tend to have higher premiums.

For instance:

– In Michigan, a 16-year-old might pay over $15,000 per year due to the state’s no-fault insurance system and high medical coverage requirements.

– In Maine, the same teen might pay closer to $4,000 thanks to lower traffic density and lower repair costs.

– In California, rates are moderate—around $6,000–$8,000—but the state prohibits gender-based pricing, so boys and girls pay similar rates.

Urban areas like New York City or Los Angeles often have higher premiums than rural areas due to increased traffic, theft, and vandalism risks.

Cost by Coverage Level

The type of coverage you choose also affects the price.

– **Liability-only coverage** (minimum required in most states) is the cheapest option, often ranging from $2,000 to $4,000 per year for a teen.

– **Full coverage** (liability + collision + comprehensive) is much more expensive, typically $5,000 to $10,000 or more.

Full coverage is usually recommended for newer or financed vehicles, while liability-only might make sense for an older car with low market value.

Cost by Vehicle Type

The car your teen drives matters—a lot. Insurers consider safety ratings, repair costs, theft rates, and performance.

For example:

– A 2010 Honda Civic with good safety ratings might cost $5,500 per year to insure.

– A 2020 Ford Mustang GT could cost $9,000 or more due to high horsepower and theft risk.

– A 2015 Toyota Camry with advanced safety features might be around $6,200.

Choosing a safe, reliable, and modestly powered vehicle can save thousands over time.

Factors That Affect Teen Car Insurance Rates

Visual guide about How Much Is Car Insurance for a Teenager?

Image source: spendmenot.com

Now that you know the average costs, let’s dig into the factors that determine how much you’ll actually pay. Understanding these can help you make smarter choices and potentially lower your premiums.

Driving Record

This one’s a no-brainer: a clean driving record keeps rates low. But even a single speeding ticket or at-fault accident can spike premiums by 20–50%. For a teen, that could mean an extra $1,000 or more per year.

For example, a 17-year-old with a clean record might pay $6,000 annually. But if they get a speeding ticket, that could jump to $7,500. A DUI? That could double the cost or even lead to policy cancellation.

The good news? Many insurers offer accident forgiveness or rate reductions after a few years of safe driving. Some also allow teens to complete defensive driving courses to remove minor violations from their record.

Location

Where you live affects everything from traffic density to weather risks to theft rates.

– Urban areas: Higher traffic, more accidents, more theft → higher premiums.

– Rural areas: Less traffic, fewer claims → lower premiums.

– High-risk states: Michigan, Florida, and Louisiana have some of the highest average rates due to no-fault laws, hurricanes, or high litigation costs.

Even within a state, zip codes matter. Living in a safe suburban neighborhood with low crime and good schools can result in lower rates than a high-crime urban area.

Type of Vehicle

As mentioned earlier, the car your teen drives plays a major role. Insurers look at:

– **Safety ratings:** Cars with high IIHS or NHTSA ratings cost less to insure.

– **Repair costs:** Luxury and imported cars often have pricier parts and labor.

– **Theft rates:** Vehicles frequently targeted by thieves (like certain Honda or Toyota models) cost more to insure.

– **Performance:** High-horsepower cars are seen as riskier, especially for inexperienced drivers.

Tip: Before buying a car for your teen, get insurance quotes for a few models. You might be surprised by the difference.

Coverage Limits and Deductibles

Higher coverage limits mean higher premiums. But they also mean better protection in a serious accident.

Most states require minimum liability coverage (e.g., 25/50/25: $25,000 per person, $50,000 per accident, $25,000 for property damage). But experts recommend higher limits—like 100/300/100—especially for families with assets to protect.

Deductibles also affect cost. A higher deductible (e.g., $1,000 vs. $500) lowers your premium but means you pay more out of pocket if you file a claim. For teens, a $500 deductible is often a good balance.

Credit Score (Where Allowed)

In most states, insurers use credit-based insurance scores to predict risk. Teens usually don’t have credit histories, so parents’ scores are often used when adding them to a policy.

A poor credit score can increase premiums by 20–50%. Maintaining good credit as a family can help keep rates lower.

Note: California, Hawaii, and Massachusetts prohibit the use of credit scores in insurance pricing.

Discounts and Savings Opportunities

This is where you can really make a difference. Many insurers offer discounts specifically for teen drivers.

– **Good student discount:** Typically 10–25% off for maintaining a B average or higher.

– **Driver education discount:** Completing a certified course can save 5–15%.

– **Multi-car discount:** Adding a teen’s car to a family policy often reduces the per-car cost.

– **Safe driver monitoring:** Usage-based programs like Progressive’s Snapshot or Allstate’s Drivewise reward safe habits with discounts.

– **Low-mileage discount:** If your teen drives less than 7,500 miles per year, you might qualify.

Combining these can save hundreds—or even thousands—each year.

Ways to Reduce Car Insurance Costs for Teen Drivers

Now for the good part: how to lower those eye-watering premiums. With a few smart moves, you can cut your teen’s insurance costs by 20–30% or more.

Add Your Teen to Your Policy (Instead of a Separate One)

This is the single best way to save. Most insurers offer multi-car and family discounts when you add a teen to an existing policy. A standalone policy for a 16-year-old can cost $8,000–$12,000, while adding them to a parent’s policy might only increase the total by $5,000–$7,000.

Plus, you maintain control over coverage and can bundle home or renters insurance for even more savings.

Choose the Right Car

Avoid sports cars, luxury vehicles, and high-theft models. Instead, opt for:

– Sedans or small SUVs with top safety ratings

– Models with low repair costs and good fuel economy

– Cars with advanced safety features (automatic braking, blind-spot monitoring)

Examples of teen-friendly cars:

– Honda Civic

– Toyota Corolla

– Subaru Impreza

– Hyundai Elantra

These models are reliable, safe, and typically cost less to insure.

Encourage Good Grades

Many insurers offer good student discounts for teens with a B average or higher. This can save 10–25% on premiums.

Just provide a report card or transcript once a year. Some companies even accept honor roll status or participation in academic programs.

Enroll in a Driver Education Course

Completing a state-approved driver’s ed course can reduce premiums by 5–15%. These courses teach defensive driving, hazard recognition, and state laws.

Some insurers also offer discounts for online courses or behind-the-wheel training.

Use Telematics or Safe Driving Apps

Programs like:

– Progressive’s Snapshot

– State Farm’s Drive Safe & Save

– Allstate’s Drivewise

Track your teen’s driving habits (speed, braking, phone use) and reward safe behavior with discounts—sometimes up to 30%.

These apps also give parents peace of mind by providing real-time feedback and alerts.

Increase Deductibles (Carefully)

Raising your deductible from $500 to $1,000 can lower premiums by 10–15%. But make sure your family can afford the higher out-of-pocket cost if an accident occurs.

Limit Mileage

If your teen doesn’t drive much—say, only to school and part-time jobs—you might qualify for a low-mileage discount. Some insurers offer this for drivers under 7,500 miles per year.

Shop Around Annually

Insurance rates change every year. What was a great deal last year might not be the best now. Get quotes from at least three insurers annually.

Use comparison sites like NerdWallet, The Zebra, or Insurify to compare rates quickly.

Should You Buy a Separate Policy for Your Teen?

It’s a common question: should your teen have their own policy, or should they be added to yours?

In almost all cases, **adding them to your policy is cheaper and smarter**.

Here’s why:

– **Multi-car discounts:** Most insurers reduce the per-car cost when you have multiple vehicles.

– **Better rates:** Parent policies often have lower base rates due to the adult’s driving history and credit.

– **Easier management:** One policy means one bill, one renewal date, and one point of contact.

A standalone policy for a teen is usually only considered if:

– The teen owns their own car and lives independently (rare for minors).

– The parent’s policy doesn’t allow additional drivers.

– The teen has a poor driving record and would drastically increase the parent’s premium.

Even then, it’s worth comparing both options. In most cases, adding to the family policy saves money.

What Coverage Does a Teenager Need?

Now that you’re saving on premiums, don’t skimp on coverage. Teens need the same protection as adult drivers—maybe even more.

Liability Coverage

This is mandatory in every state. It covers:

– Bodily injury to others

– Property damage to others

Minimums vary, but experts recommend at least 100/300/100 for families with assets.

Collision Coverage

Pays for damage to your teen’s car after an accident, regardless of fault. Essential if the car is newer or financed.

Comprehensive Coverage

Covers non-collision events like theft, vandalism, fire, or weather damage. Important if the car has value or is parked in a high-risk area.

Uninsured/Underinsured Motorist Coverage

Protects your teen if they’re hit by a driver with no insurance or insufficient coverage. Highly recommended.

Medical Payments or PIP

Covers medical expenses for your teen and passengers, regardless of fault. Required in no-fault states.

Rental Reimbursement and Roadside Assistance

Optional but helpful. Rental reimbursement covers a rental car while yours is repaired. Roadside assistance helps with flat tires, towing, or lockouts.

Tip: If your teen drives an older car worth less than $4,000, you might skip collision and comprehensive to save money—but only if you can afford to replace the car out of pocket.

The Role of Parental Involvement in Lowering Costs

Parents aren’t just policyholders—they’re key to keeping their teen safe and insurance costs down.

Set Clear Rules

Create a parent-teen driving agreement that outlines:

– Curfews

– Passenger limits

– No phone use while driving

– Consequences for violations

Studies show that teens with clear rules are less likely to crash.

Monitor Driving Habits

Use apps like Life360 or built-in telematics to track location, speed, and driving behavior. Open communication helps teens understand the risks.

Lead by Example

Teens mimic adult behavior. If you speed, text while driving, or ignore seat belts, they will too. Practice safe driving yourself.

Stay Involved in Education

Attend driver’s ed with your teen. Practice driving in different conditions (rain, night, highways). The more experience, the safer they become—and the lower your premiums over time.

Long-Term Savings: How Rates Change as Teens Gain Experience

The good news? Car insurance for a teenager gets cheaper—fast.

Here’s how rates typically drop over time:

– **Age 16–17:** Highest rates, $6,000–$10,000+

– **Age 18–19:** Rates drop 20–30% with experience

– **Age 20–24:** Continue to decline, especially with clean records

– **Age 25+:** Rates stabilize and often match or fall below adult averages

For example, a 16-year-old paying $8,000 per year might pay $5,500 at 18, $4,000 at 20, and $2,500 at 25—assuming no accidents or tickets.

Maintaining a clean record, continuing education, and staying on the family policy can accelerate these savings.

Conclusion

So, how much is car insurance for a teenager? The answer is: a lot—but it doesn’t have to break the bank.

With average annual costs ranging from $5,000 to $10,000, teen drivers are the most expensive to insure. But by understanding the factors that affect pricing—and taking advantage of discounts, smart vehicle choices, and safe driving programs—you can reduce those costs significantly.

The key is to be proactive. Add your teen to your policy, choose a safe car, encourage good grades and driver education, and monitor their habits. Over time, as your teen gains experience and maintains a clean record, premiums will naturally decline.

Remember, insurance isn’t just about cost—it’s about protection. Investing in the right coverage now can save your family from financial disaster later.

And while the price tag may seem steep, think of it as an investment in your teen’s safety and your family’s peace of mind. With the right approach, you can keep both your wallet and your teen protected on the road.

Frequently Asked Questions

How much does it cost to add a 16-year-old to car insurance?

Adding a 16-year-old to a parent’s policy typically increases annual premiums by $5,000 to $10,000, depending on location, vehicle, and driving record. This is due to the high risk associated with inexperienced drivers.

Can I get a discount for my teen’s good grades?

Yes, most insurers offer a good student discount of 10–25% for teens who maintain a B average or higher. You’ll usually need to submit a report card or transcript once a year.

Is it cheaper to have my teen on my policy or their own?

Adding your teen to your existing policy is almost always cheaper than buying them a separate one. Multi-car and family discounts significantly reduce the overall cost.

What type of car is cheapest to insure for a teenager?

Sedans and small SUVs with high safety ratings, low repair costs, and modest engines—like the Honda Civic or Toyota Corolla—are typically the cheapest to insure for teens.

Do insurance rates go down when a teen turns 18?

Yes, rates usually drop by 20–30% when a teen turns 18, as they gain more driving experience. Continued safe driving can lead to further reductions over time.

Can telematics apps really lower my teen’s insurance cost?

Yes, usage-based programs like Progressive’s Snapshot or State Farm’s Drive Safe & Save can reward safe driving with discounts of up to 30%, based on speed, braking, and phone usage.