How Much Is Car Insurance for a 16-year-old per Month

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance for a 16-Year-Old per Month?

- 4 Why Is Car Insurance So Expensive for 16-Year-Olds?

- 5 Average Monthly Costs by State and Scenario

- 6 Factors That Affect Car Insurance Rates for Teens

- 7 How to Reduce Car Insurance Costs for a 16-Year-Old

- 8 State-Specific Considerations

- 9 Common Mistakes to Avoid

- 10 Final Thoughts: Is It Worth It?

- 11 Conclusion

- 12 Frequently Asked Questions

Car Shampoo Concentrate

Side Window Sunshade

Microfiber Car Cleaning Cloth

LED Emergency Road Flares

Car insurance for a 16-year-old typically costs between $200 and $500 per month, depending on location, vehicle, and coverage. While expensive, smart choices like adding your teen to your policy and choosing safe cars can help reduce costs.

[FEATURED_IMAGE_PLACEOLDER]

Key Takeaways

- High premiums are normal: 16-year-old drivers face the highest insurance rates due to lack of experience and higher accident risk.

- Monthly costs range widely: Expect to pay $200–$500 per month, with some areas exceeding $600 depending on state and insurer.

- Adding to a parent’s policy is cheaper: It’s almost always more affordable than a standalone policy for a teen.

- Vehicle choice matters: Safe, low-powered cars with high safety ratings cost less to insure than sports cars or luxury vehicles.

- Discounts can help: Good student, driver training, and telematics programs can reduce premiums by 10–25%.

- State laws affect pricing: Minimum coverage requirements and no-fault laws influence how much you’ll pay.

- Shop around annually: Comparing quotes from multiple insurers can lead to significant savings over time.

📑 Table of Contents

- How Much Is Car Insurance for a 16-Year-Old per Month?

- Why Is Car Insurance So Expensive for 16-Year-Olds?

- Average Monthly Costs by State and Scenario

- Factors That Affect Car Insurance Rates for Teens

- How to Reduce Car Insurance Costs for a 16-Year-Old

- State-Specific Considerations

- Common Mistakes to Avoid

- Final Thoughts: Is It Worth It?

- Conclusion

How Much Is Car Insurance for a 16-Year-Old per Month?

Getting your 16-year-old behind the wheel is a big milestone—but it comes with a hefty price tag. One of the biggest questions parents ask is: How much is car insurance for a 16-year-old per month? The short answer? It’s expensive. But the long answer? It depends on a lot of factors, and there are ways to manage the cost.

On average, insuring a 16-year-old driver costs between $200 and $500 per month. In some high-risk areas or with certain vehicles, that number can climb above $600. That’s a steep bill, especially when you’re already covering your own insurance, car payments, gas, and maintenance. But understanding what drives these costs—and how to reduce them—can make a big difference.

The good news? You’re not powerless. By choosing the right car, taking advantage of discounts, and making smart policy decisions, you can keep premiums more manageable. This guide will walk you through everything you need to know about car insurance for 16-year-olds, from average costs to money-saving tips and real-world examples.

Why Is Car Insurance So Expensive for 16-Year-Olds?

Visual guide about How Much Is Car Insurance for a 16-year-old per Month

Image source: res.cloudinary.com

Let’s be honest: 16-year-old drivers are risky. Insurance companies base their rates on data, and the data shows that teen drivers—especially 16-year-olds—are far more likely to get into accidents than any other age group.

According to the Insurance Institute for Highway Safety (IIHS), drivers aged 16 to 19 have crash rates nearly three times higher than drivers aged 20 and older. And 16-year-olds? They’re at the top of that risk pile. In fact, the fatal crash rate per mile driven is nearly twice as high for 16-year-olds as it is for 18- and 19-year-olds.

Lack of Driving Experience

At 16, most teens have only been driving for a few months. They’re still learning how to judge speed, distance, and reaction times. They’re more likely to be distracted by passengers, phones, or music. And they’re less likely to recognize dangerous situations before it’s too late.

Insurance companies see this inexperience as a major liability. Even if your teen is responsible and cautious, the statistics don’t lie—new drivers are more likely to make mistakes that lead to claims.

Higher Likelihood of Risky Behavior

Teen drivers are also more prone to risky behaviors like speeding, not wearing seat belts, and driving under the influence. According to the CDC, teens are less likely than adults to wear seat belts, and male teen drivers are twice as likely to be involved in a fatal crash involving alcohol.

These behaviors increase the chance of severe accidents, which means higher payouts for insurers—and higher premiums for you.

Gender and Age Play a Role

Believe it or not, gender still affects insurance rates—especially for teens. Statistically, 16-year-old male drivers are involved in more accidents than 16-year-old female drivers. As a result, insurance companies often charge young men higher premiums.

For example, a 16-year-old boy might pay $50 more per month than a 16-year-old girl with the same driving record, vehicle, and location. This gap narrows as drivers get older and gain experience.

Location Matters

Where you live has a huge impact on insurance costs. Urban areas with heavy traffic, high accident rates, and expensive repair costs tend to have higher premiums. States with no-fault insurance laws or high minimum coverage requirements also drive up prices.

For instance, a 16-year-old in Michigan might pay over $600 per month due to the state’s unlimited personal injury protection (PIP) coverage. Meanwhile, a teen in Maine or Ohio might pay closer to $250.

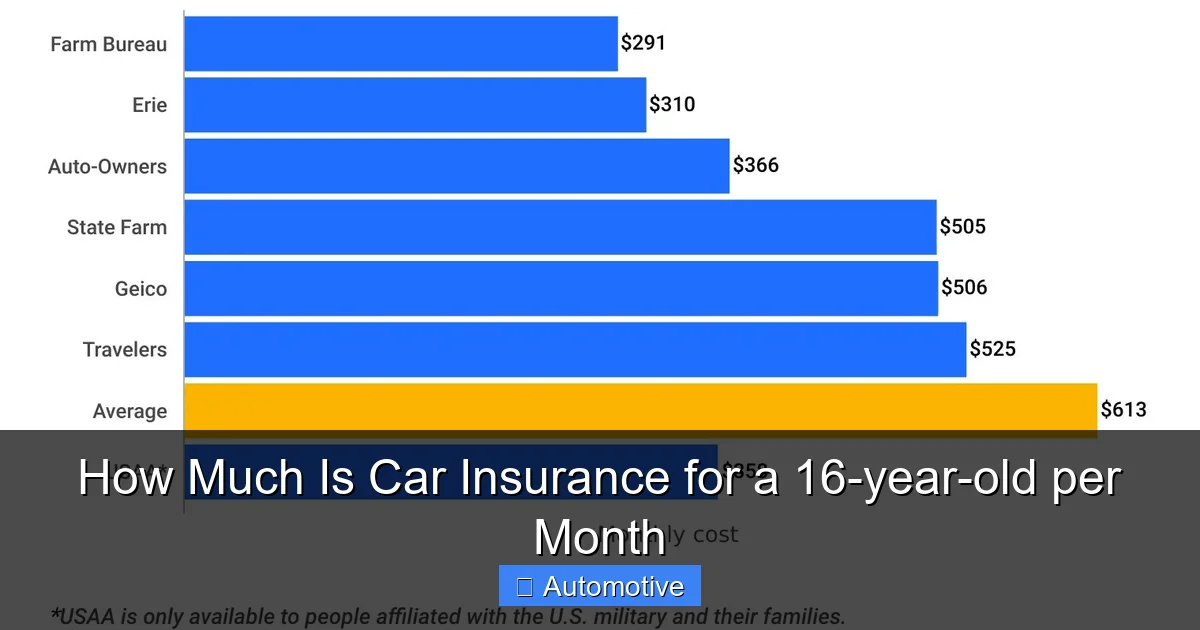

Average Monthly Costs by State and Scenario

Visual guide about How Much Is Car Insurance for a 16-year-old per Month

Image source: doubxab0r1mke.cloudfront.net

So, how much is car insurance for a 16-year-old per month in real terms? Let’s break it down with some realistic examples.

National Average

Across the U.S., the average monthly cost to insure a 16-year-old driver ranges from $200 to $500. This assumes the teen is added to a parent’s policy, drives a modest vehicle, and has a clean record.

But averages don’t tell the whole story. Costs can vary dramatically based on where you live.

High-Cost States

In states like Michigan, Florida, and Louisiana, monthly premiums for a 16-year-old can exceed $600. Michigan tops the list due to its unique no-fault system and unlimited PIP coverage. Even with a clean record and a safe car, a 16-year-old in Detroit might pay $700 or more per month.

Florida follows closely, with high rates driven by traffic congestion, weather-related damage, and a large number of uninsured drivers.

Low-Cost States

On the other end of the spectrum, states like Maine, Ohio, and Wisconsin offer more affordable rates. In Maine, a 16-year-old might pay as little as $180 per month when added to a parent’s policy. That’s because the state has lower population density, fewer accidents, and lower repair costs.

Real-World Example: Adding a Teen to a Parent’s Policy

Let’s say you live in Texas, drive a 2018 Honda CR-V, and have a clean driving record. You add your 16-year-old daughter to your policy.

– Your current premium: $120/month

– Premium after adding teen: $320/month

– Increase: $200/month

That’s a big jump—but it’s still far cheaper than buying a separate policy for your teen, which could cost $400–$600/month on its own.

Standalone Policy vs. Adding to Parent’s Policy

Some parents consider getting their teen their own insurance policy. But this is almost always a bad idea.

A standalone policy for a 16-year-old can cost $400–$800 per month, depending on the state and coverage. That’s because the insurer sees the teen as the primary driver—and a high-risk one at that.

Adding your teen to your policy spreads the risk across the household and often qualifies you for multi-car and multi-driver discounts. It’s almost always the more affordable option.

Factors That Affect Car Insurance Rates for Teens

Visual guide about How Much Is Car Insurance for a 16-year-old per Month

Image source: kuonilopez.com

Now that you know the average costs, let’s look at what actually determines how much you’ll pay. Understanding these factors can help you make smarter decisions and potentially lower your premium.

1. Type of Vehicle

The car your teen drives has a huge impact on insurance costs. Insurers look at:

– **Safety ratings:** Cars with high safety scores (like those from the IIHS or NHTSA) cost less to insure.

– **Repair costs:** Luxury and imported cars are more expensive to fix.

– **Theft rates:** Vehicles that are frequently stolen (like certain Honda models) have higher premiums.

– **Performance:** High-horsepower cars, especially sports cars, are seen as riskier.

For example, insuring a 16-year-old in a Toyota Corolla or Honda Civic will cost significantly less than insuring them in a Ford Mustang or BMW 3 Series.

2. Coverage Level

The more coverage you buy, the higher your premium. Most states require minimum liability coverage, but many parents opt for full coverage (including collision and comprehensive) to protect their investment.

– **Minimum liability:** Covers damage you cause to others. Cheapest option, but offers no protection for your own car.

– **Full coverage:** Includes collision (damage from accidents) and comprehensive (theft, vandalism, weather). More expensive, but recommended if the car is worth more than $4,000.

For a 16-year-old, full coverage is often worth it—especially if the car is new or financed.

3. Driving Record

Even at 16, a clean driving record matters. If your teen gets a speeding ticket or causes an accident, premiums can increase by 20–50%.

Conversely, maintaining a clean record for a year or two can lead to lower rates as they gain experience.

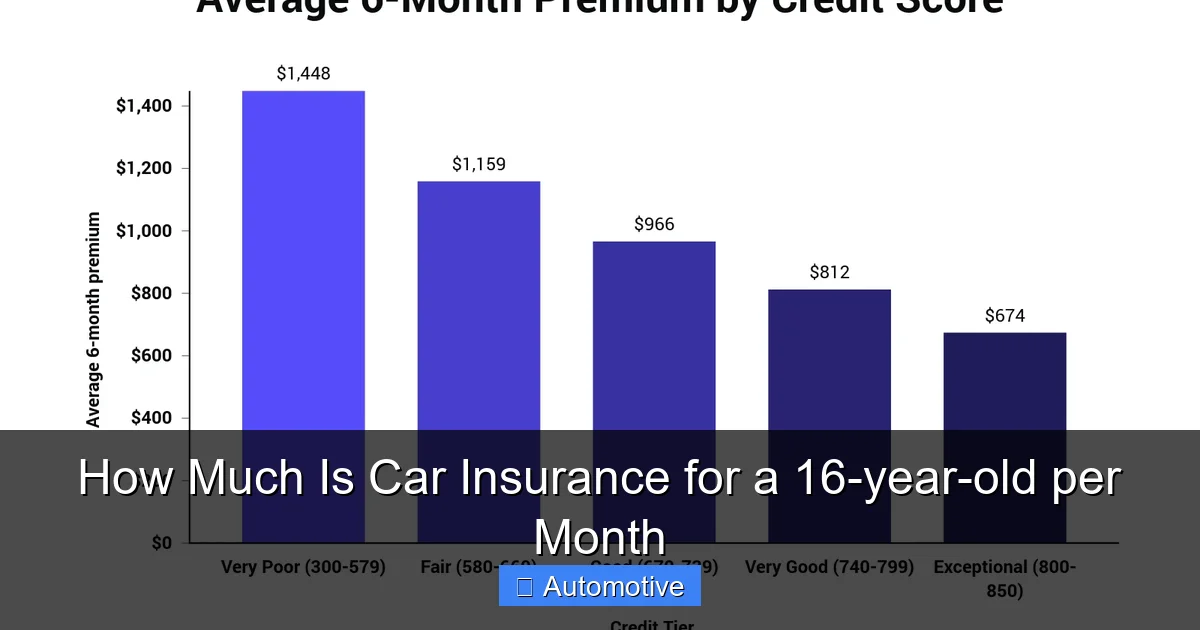

4. Credit Score (in Most States)

In most states (except California, Hawaii, and Massachusetts), insurers use credit-based insurance scores to set rates. Teens don’t have credit histories, so the parent’s credit score is used when adding them to a policy.

Good credit can lead to lower premiums, while poor credit can increase costs by 20% or more.

5. Annual Mileage

The more your teen drives, the higher the risk. If they’re only driving to school and back (say, 500 miles per month), you might qualify for a low-mileage discount.

But if they’re commuting long distances or driving for work, expect higher rates.

6. School Performance

Many insurers offer a “good student discount” for teens who maintain a B average or higher. This can save 10–25% on premiums.

Some companies also offer discounts for completing a driver’s education course or defensive driving program.

How to Reduce Car Insurance Costs for a 16-Year-Old

Yes, insuring a 16-year-old is expensive—but you don’t have to pay full price. Here are proven strategies to lower your monthly bill.

1. Add Your Teen to Your Policy

As mentioned earlier, this is almost always cheaper than a standalone policy. You’ll benefit from family discounts and shared risk.

2. Choose a Safe, Affordable Car

Avoid sports cars, luxury vehicles, and high-theft models. Instead, opt for:

– Midsize sedans (e.g., Toyota Camry, Honda Accord)

– Compact SUVs (e.g., Honda CR-V, Toyota RAV4)

– Cars with top safety ratings

These vehicles are cheaper to insure and safer in crashes.

3. Take Advantage of Discounts

Look for these common teen discounts:

– **Good student discount:** For maintaining a B average or higher.

– **Driver training discount:** For completing a state-approved driver’s ed course.

– **Telematics program:** Use a driving app or device (like Progressive’s Snapshot or State Farm’s Drive Safe & Save) to earn discounts for safe driving.

– **Multi-car discount:** If you insure multiple vehicles with the same company.

– **Paperless billing or auto-pay discount:** Small but helpful savings.

Some insurers also offer discounts for low annual mileage or for having anti-theft devices.

4. Increase Your Deductible

Raising your collision and comprehensive deductible from $500 to $1,000 can lower your premium by 10–20%. Just make sure you can afford to pay the deductible if you need to file a claim.

5. Consider Usage-Based Insurance

Telematics programs monitor your teen’s driving habits—like speed, braking, and mileage. Safe drivers can earn significant discounts, sometimes up to 30%.

These programs are especially helpful for proving that your teen is a responsible driver, even if they’re young.

6. Shop Around Annually

Insurance companies change their rates and discounts frequently. What was the cheapest option last year might not be this year.

Get quotes from at least three insurers every 12 months. Compare not just price, but also customer service, claims process, and coverage options.

7. Keep Your Teen on Your Policy as Long as Possible

Once your teen turns 18 or 19, they may be eligible for their own policy—but that doesn’t mean they should get one. Staying on your policy often remains cheaper, especially if you have a good driving record and multiple vehicles.

State-Specific Considerations

Insurance regulations vary by state, and these differences can affect how much you pay.

No-Fault States

In no-fault states (like Florida, Michigan, and New York), drivers must carry personal injury protection (PIP) coverage. This pays for medical expenses regardless of who caused the accident.

PIP coverage is expensive, especially for high-risk drivers like teens. That’s why Michigan has some of the highest teen insurance rates in the country.

Minimum Coverage Requirements

Each state sets minimum liability limits. For example:

– California: 15/30/5 ($15,000 bodily injury per person, $30,000 per accident, $5,000 property damage)

– Texas: 30/60/25

– New York: 25/50/10

Meeting only the minimum can save money, but it leaves you underinsured. Consider higher limits or an umbrella policy for better protection.

Teen Licensing Laws

Some states have graduated driver licensing (GDL) programs that restrict teen driving (e.g., no nighttime driving or passenger limits). These laws reduce accident rates, which can indirectly lower insurance costs over time.

Common Mistakes to Avoid

When insuring a 16-year-old, it’s easy to make costly mistakes. Here’s what to avoid:

1. Buying a Standalone Policy

As discussed, this is almost always more expensive. Only consider it if your teen owns the car outright and you’re not the primary driver.

2. Choosing the Cheapest Car Without Considering Insurance

A used sports car might seem affordable, but insurance could cost more than the car payment. Always check insurance quotes before buying.

3. Skipping Full Coverage on a Newer Car

If the car is worth more than $4,000, full coverage is usually worth it. Otherwise, you could lose thousands in an accident.

4. Not Updating the Policy

If your teen moves out, goes to college, or stops driving, update your policy. You might qualify for a “distant student” discount or lower mileage rates.

5. Ignoring Discounts

Many parents don’t realize discounts exist. Always ask your insurer about available savings.

Final Thoughts: Is It Worth It?

Yes—insuring your 16-year-old is worth it. While the cost is high, the protection is essential. A single accident could result in tens of thousands of dollars in damages, medical bills, or legal fees. Without insurance, you’d be on the hook for all of it.

The key is to balance cost and coverage. Don’t over-insure, but don’t under-insure either. Use discounts, choose wisely, and shop around.

Remember, your teen’s rates will improve with time. After a year or two of safe driving, you’ll likely see a significant drop in premiums. And by then, they’ll have the experience to be a safer, more confident driver.

Conclusion

So, how much is car insurance for a 16-year-old per month? On average, $200 to $500—but it depends on where you live, what you drive, and how you manage your policy.

While the cost is high, it’s a necessary investment in your teen’s safety and your financial security. By understanding the factors that affect pricing and taking advantage of every discount available, you can make insuring your 16-year-old more affordable.

Start by adding your teen to your policy, choosing a safe vehicle, and enrolling in driver training and telematics programs. Then, shop around annually to ensure you’re getting the best deal.

With the right approach, you can protect your teen—and your wallet—while they learn to drive responsibly.

Frequently Asked Questions

How much does it cost to insure a 16-year-old per month?

The average monthly cost ranges from $200 to $500, depending on location, vehicle, and coverage. In high-cost states like Michigan or Florida, it can exceed $600.

Is it cheaper to add a teen to my policy or get them their own?

Adding your teen to your policy is almost always cheaper than a standalone policy, which can cost $400–$800 per month.

What kind of car is cheapest to insure for a 16-year-old?

Safe, reliable cars like the Honda Civic, Toyota Corolla, or Honda CR-V are cheapest to insure due to low repair costs and high safety ratings.

Can my teen get a discount for good grades?

Yes, most insurers offer a good student discount for maintaining a B average or higher, which can save 10–25% on premiums.

Do I need full coverage for my 16-year-old’s car?

If the car is worth more than $4,000 or is financed, full coverage (including collision and comprehensive) is usually recommended.

Will my rates go down as my teen gets older?

Yes, insurance rates typically decrease significantly after age 18–19, especially with a clean driving record and more experience.