How Much Can I Afford for a Car?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Can I Afford for a Car? A Smart Buyer’s Guide

- 4 Step 1: Know Your Financial Situation

- 5 Step 2: Use the 20/4/10 Rule

- 6 Step 3: Calculate the True Cost of Ownership

- 7 Step 4: Check Your Credit and Shop for Financing

- 8 Step 5: Choose the Right Car for Your Budget

- 9 Step 6: Stick to Your Budget—No Matter What

- 10 Final Thoughts: Drive Happy, Not Broke

- 11 Frequently Asked Questions

Buying a car is exciting, but overspending can lead to financial stress. Knowing how much you can afford for a car means looking beyond the sticker price and factoring in insurance, fuel, maintenance, and monthly payments. With smart planning, you can drive away happy—without hurting your wallet.

Key Takeaways

- Use the 20/4/10 rule: Put down 20%, finance for no more than 4 years, and keep total car expenses under 10% of your gross income.

- Calculate your true monthly cost: Include loan payments, insurance, fuel, maintenance, and parking to avoid surprises.

- Check your credit score first: A higher score means lower interest rates and better loan terms.

- Consider total cost of ownership: Some cars cost more to insure, repair, or fuel—even if the purchase price is low.

- Shop around for financing: Compare rates from banks, credit unions, and dealerships to save hundreds over the loan term.

- Test drive your budget: Use online calculators to simulate payments before visiting a dealership.

- Avoid emotional decisions: Stick to your budget, even when tempted by flashy features or sales pressure.

📑 Table of Contents

- How Much Can I Afford for a Car? A Smart Buyer’s Guide

- Step 1: Know Your Financial Situation

- Step 2: Use the 20/4/10 Rule

- Step 3: Calculate the True Cost of Ownership

- Step 4: Check Your Credit and Shop for Financing

- Step 5: Choose the Right Car for Your Budget

- Step 6: Stick to Your Budget—No Matter What

- Final Thoughts: Drive Happy, Not Broke

How Much Can I Afford for a Car? A Smart Buyer’s Guide

So you’re thinking about buying a car. Maybe you’re tired of public transit, your old ride just gave up the ghost, or you finally feel ready to upgrade. Whatever the reason, one question looms large: *How much can I afford for a car?*

It’s easy to get swept up in the excitement—shiny paint, leather seats, a sunroof that opens with the touch of a button. But before you fall in love with a vehicle that’s stretching your budget to the breaking point, take a step back. The real key to a smart car purchase isn’t just finding the right model—it’s finding one that fits your financial life.

Many people focus only on the monthly payment, but that’s just one piece of the puzzle. The true cost of owning a car includes insurance, fuel, maintenance, repairs, registration, and depreciation. If you don’t plan for these, you could end up paying far more than you expected—or worse, struggling to make payments when unexpected expenses pop up.

The good news? With a little planning and some honest number-crunching, you can figure out exactly how much car you can afford—and feel confident in your decision. This guide will walk you through the steps, from assessing your income and expenses to comparing loan options and choosing the right vehicle. Let’s get started.

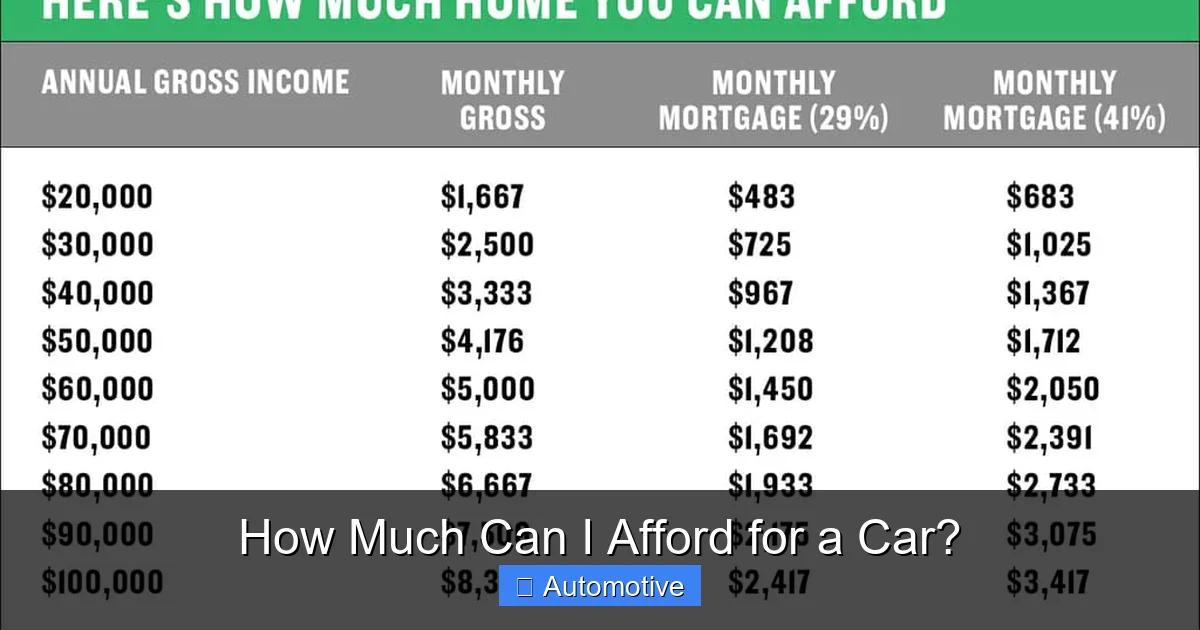

Step 1: Know Your Financial Situation

Visual guide about How Much Can I Afford for a Car?

Image source: notwaitingtolive.com

Before you even look at car listings, take a hard look at your finances. This isn’t about shame or guilt—it’s about clarity. You need to understand your income, expenses, debts, and savings to make a smart decision.

Calculate Your Monthly Take-Home Pay

Start with your net income—the amount you actually bring home after taxes and deductions. If you’re salaried, this is straightforward. If you’re hourly or freelance, average your last three to six months of income to get a realistic number.

For example, if you earn $4,000 per month after taxes, that’s your starting point. Don’t use your gross income (before taxes), because that number is misleading. You can’t spend money you don’t actually receive.

List Your Monthly Expenses

Next, write down all your regular monthly expenses. This includes:

– Rent or mortgage

– Utilities (electric, water, gas, internet)

– Groceries

– Transportation (gas, public transit, current car payments)

– Insurance (health, renters, etc.)

– Debt payments (credit cards, student loans, personal loans)

– Savings and investments

– Entertainment, dining out, subscriptions

Be honest. If you spend $200 a month on coffee and takeout, include it. These small expenses add up and affect how much you can comfortably spend on a car.

Determine Your Disposable Income

Subtract your total monthly expenses from your net income. The result is your disposable income—the amount you have left for non-essential spending, like a new car payment.

For example:

– Net income: $4,000

– Total expenses: $2,800

– Disposable income: $1,200

This $1,200 is what you can use for a car payment, insurance, fuel, and maintenance—without going into debt or skipping rent.

Factor in Emergency Savings

Before committing to a car payment, make sure you have an emergency fund. Experts recommend saving three to six months’ worth of living expenses. If you don’t have that yet, consider delaying your purchase or choosing a cheaper car so you can build savings while making payments.

A car breakdown or unexpected repair can cost hundreds—or even thousands. Without savings, you might have to put repairs on a credit card, which can lead to high-interest debt.

Step 2: Use the 20/4/10 Rule

Visual guide about How Much Can I Afford for a Car?

Image source: notwaitingtolive.com

One of the most trusted guidelines for car affordability is the 20/4/10 rule. It’s simple, practical, and backed by financial experts.

What Is the 20/4/10 Rule?

The rule breaks down like this:

– **20% down payment:** Put at least 20% of the car’s price down upfront.

– **4-year loan term:** Finance the car for no more than 4 years (48 months).

– **10% of income:** Keep your total car expenses (payment + insurance + fuel + maintenance) under 10% of your gross monthly income.

Let’s see how this works in practice.

Say you earn $50,000 per year, which is about $4,167 per month gross. Ten percent of that is $417. So your total monthly car costs should not exceed $417.

If you follow the 20/4/10 rule, you’re less likely to be “upside down” on your loan (owing more than the car is worth) and more likely to afford ongoing expenses.

Why This Rule Works

– **20% down payment:** Reduces the loan amount, lowers monthly payments, and builds equity faster. It also shows lenders you’re financially responsible, which can help you get better loan terms.

– **4-year loan term:** Shorter terms mean less interest paid over time. A 6- or 7-year loan might have lower monthly payments, but you’ll pay significantly more in interest—and risk owing more than the car is worth.

– **10% of income:** Keeps car ownership affordable. If your car costs more than 10% of your income, you may struggle to cover other essentials or save for the future.

Example: Applying the 20/4/10 Rule

Let’s say you want to buy a $25,000 car.

– 20% down payment = $5,000

– Loan amount = $20,000

– 4-year loan at 5% interest = about $460 per month

Now add insurance ($120), fuel ($100), and maintenance ($50). Total monthly cost: $730.

If your gross monthly income is $4,167, 10% is $417. $730 is way over that limit.

So what can you afford? Let’s work backward.

If your max car budget is $417 per month, and insurance, fuel, and maintenance cost about $270, that leaves $147 for the loan payment.

At 5% interest over 4 years, a $147 payment gets you a loan of about $6,400. Add a $1,600 down payment (20%), and you can afford a car around $8,000.

That might sound low, but it’s realistic. Many reliable used cars—like a Honda Civic, Toyota Corolla, or Mazda3—fall in this range and can last for years with proper care.

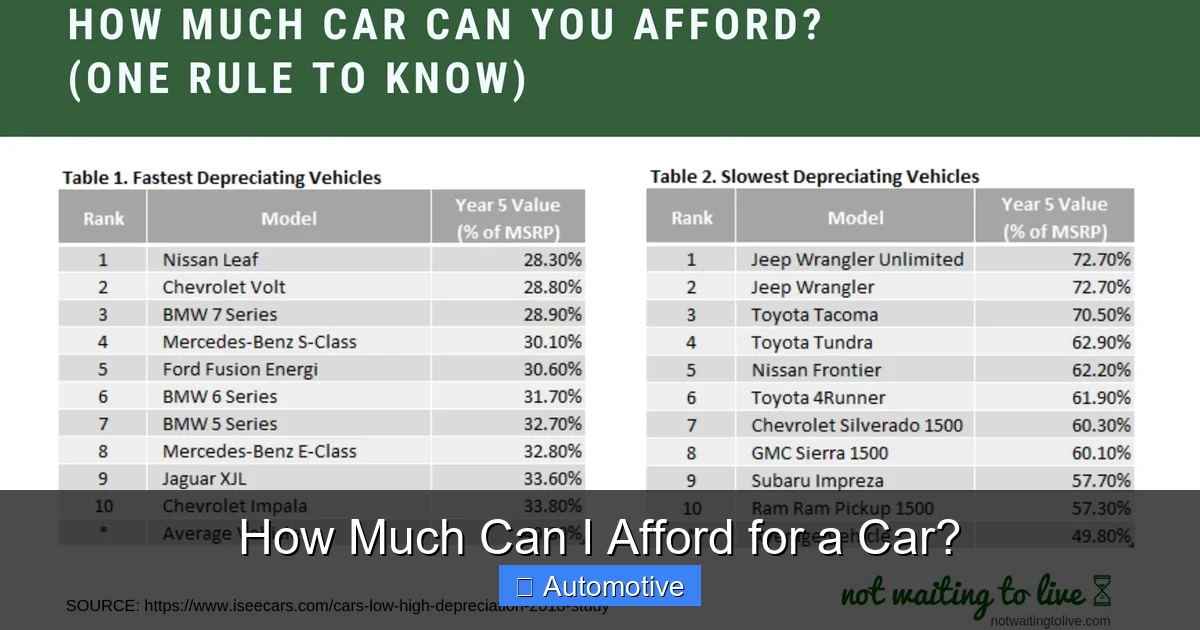

Step 3: Calculate the True Cost of Ownership

Visual guide about How Much Can I Afford for a Car?

Image source: gajizmo.com

The sticker price of a car is just the beginning. To truly understand how much you can afford, you need to consider the total cost of ownership.

Loan Payments

This is the most obvious cost. Use an online auto loan calculator to estimate your monthly payment based on the car price, down payment, interest rate, and loan term.

For example:

– Car price: $20,000

– Down payment: $4,000

– Loan amount: $16,000

– Interest rate: 6%

– Loan term: 5 years (60 months)

– Monthly payment: ~$305

But remember: longer terms mean more interest. A 6-year loan at 6% would drop the payment to ~$254—but you’d pay over $1,200 more in interest.

Insurance

Insurance can vary wildly based on the car, your age, driving record, and location. A sports car or luxury vehicle will cost more to insure than a compact sedan.

Get quotes for the models you’re considering. For example:

– 2020 Honda Civic: $110/month

– 2020 BMW 3 Series: $220/month

That’s a $110 difference every month—over $1,300 per year.

Fuel Costs

Fuel efficiency matters. A car that gets 30 mpg will cost less to drive than one that gets 20 mpg.

Let’s say you drive 12,000 miles per year and gas costs $3.50 per gallon.

– 30 mpg: 400 gallons × $3.50 = $1,400/year ($117/month)

– 20 mpg: 600 gallons × $3.50 = $2,100/year ($175/month)

That’s a $58 monthly difference—over $700 per year.

Maintenance and Repairs

New cars come with warranties, but used cars can need repairs sooner. Luxury brands and high-performance vehicles often have higher maintenance costs.

On average, drivers spend $500–$1,000 per year on maintenance. But some cars cost much more. For example:

– Toyota Camry: ~$400/year

– Mercedes-Benz C-Class: ~$1,200/year

Set aside $50–$100 per month for maintenance, even if your car is new. This helps you avoid financial stress when something breaks.

Depreciation

Cars lose value the moment you drive them off the lot. A new car can lose 20% of its value in the first year and 50% in three years.

While you can’t avoid depreciation, you can minimize its impact by:

– Buying a used car that’s 2–3 years old (most depreciation has already happened)

– Choosing a model with strong resale value (Toyota, Honda, Subaru)

– Keeping the car well-maintained

Registration, Taxes, and Fees

Don’t forget one-time costs like:

– Sales tax (varies by state, often 5–10%)

– Registration fees ($50–$300)

– Title fees ($20–$100)

– Documentation fees (sometimes called “doc fees,” can be $200–$800)

These can add $1,000 or more to your upfront cost.

Step 4: Check Your Credit and Shop for Financing

Your credit score has a big impact on how much you’ll pay for a car loan. The higher your score, the lower your interest rate.

Know Your Credit Score

Check your credit score for free through sites like Credit Karma, Experian, or your bank. Scores range from 300 to 850.

– 720–850: Excellent (best rates)

– 690–719: Good

– 630–689: Fair

– 300–629: Poor

If your score is below 690, consider improving it before applying for a loan. Pay down credit card balances, make on-time payments, and avoid new credit applications.

Get Pre-Approved

Before visiting a dealership, get pre-approved for a loan from a bank or credit union. This gives you a clear budget and negotiating power.

Compare offers from at least three lenders. For example:

– Bank A: 5.5% APR, $300/month

– Credit Union B: 4.9% APR, $290/month

– Dealership: 6.2% APR, $315/month

Even a 0.5% difference can save you hundreds over the life of the loan.

Watch Out for Dealer Financing Traps

Dealerships often offer “special financing” with low monthly payments—but longer terms or hidden fees. They may also roll in add-ons like extended warranties, paint protection, or VIN etching, which can add $1,000 or more.

Always read the fine print. Ask for a breakdown of all costs. And never feel pressured to sign on the spot.

Step 5: Choose the Right Car for Your Budget

Now that you know your budget, it’s time to pick a car that fits.

New vs. Used

New cars come with warranties, the latest features, and peace of mind—but they depreciate fast. Used cars cost less and depreciate slower, but may need repairs sooner.

A smart middle ground? Certified pre-owned (CPO) vehicles. These are used cars that have been inspected, refurbished, and backed by a warranty from the manufacturer.

Reliability and Resale Value

Some cars cost less to own over time. Brands like Toyota, Honda, and Subaru are known for reliability and strong resale value.

Check reliability ratings from sources like Consumer Reports or J.D. Power. Avoid models with a history of expensive repairs.

Fuel Efficiency and Features

Choose a car that matches your lifestyle. If you commute 50 miles a day, fuel efficiency is key. If you have a family, safety and cargo space matter.

But don’t overspend on features you won’t use. A sunroof or premium sound system might sound nice, but they add to the price—and may not be worth it.

Test Drive and Inspect

Always test drive a car before buying. Pay attention to comfort, visibility, and how it handles.

For used cars, get a pre-purchase inspection from a trusted mechanic. It costs $100–$150 but can save you thousands in repairs.

Step 6: Stick to Your Budget—No Matter What

It’s easy to get tempted at the dealership. Salespeople are trained to upsell, and shiny cars can cloud your judgment.

Bring a Cheat Sheet

Before you go, write down:

– Your max monthly payment

– Your total budget (including insurance, fuel, etc.)

– The car models you’re considering

– Your pre-approved loan terms

Stick to it. If a salesperson pushes a more expensive car, politely say, “That’s over my budget. I’m looking for something around $X.”

Walk Away if Needed

There are plenty of cars—and dealerships—out there. If you feel pressured or uncomfortable, leave. You’re in control.

Celebrate Smart Choices

Buying a car within your means isn’t boring—it’s smart. You’ll sleep better, stress less, and have more money for things that matter, like travel, savings, or your next adventure.

Final Thoughts: Drive Happy, Not Broke

So, how much can you afford for a car? The answer isn’t just about the price tag—it’s about your entire financial picture.

By knowing your income, using the 20/4/10 rule, calculating total ownership costs, and shopping smart, you can find a car that fits your life—and your budget.

Remember: a car is a tool, not a status symbol. The best car is one that gets you where you need to go without breaking the bank.

Take your time. Do your homework. And when you drive off the lot, do it with confidence—and a clear conscience.

Frequently Asked Questions

How much should I spend on a car if I make $60,000 a year?

If you earn $60,000 per year, your gross monthly income is about $5,000. Following the 10% rule, your total car expenses should not exceed $500 per month. This includes loan payments, insurance, fuel, and maintenance. A car priced around $20,000 with a 20% down payment and 4-year loan could fit this budget.

Is it better to lease or buy a car?

Buying is usually better if you plan to keep the car long-term and want to build equity. Leasing offers lower monthly payments and the chance to drive a new car every few years, but you don’t own the vehicle and face mileage limits. Consider your driving habits and financial goals before deciding.

Can I afford a car on a tight budget?

Yes—many reliable used cars are available under $10,000. Focus on fuel-efficient, low-maintenance models like a Honda Fit, Toyota Yaris, or Hyundai Accent. Save for a larger down payment to reduce monthly costs, and always factor in insurance and fuel.

What if my credit score is low?

A low credit score means higher interest rates, but you can still get a loan. Consider a co-signer, improve your credit before applying, or shop at buy-here-pay-here dealerships (though these often have high rates). Aim to refinance later when your score improves.

Should I pay cash for a car?

Paying cash avoids interest and simplifies the process, but it can deplete your savings. Only pay cash if you have enough left for emergencies and other goals. Otherwise, a low-interest loan with a manageable payment may be smarter.

How do I avoid being upside down on my car loan?

To avoid owing more than your car is worth, make a larger down payment (20% or more), choose a shorter loan term (4 years or less), and buy a car with strong resale value. Avoid rolling negative equity from a previous loan into a new one.