Can I Get a Car Loan with a 500 Credit Score?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Can I Get a Car Loan with a 500 Credit Score?

- 4 Understanding Credit Scores and Car Loans

- 5 Types of Lenders That May Approve a 500 Credit Score

- 6 Strategies to Improve Your Chances of Approval

- 7 What to Expect: Loan Terms and Costs with a 500 Credit Score

- 8 Tips to Avoid Predatory Lending and Scams

- 9 How to Use Your Car Loan to Rebuild Credit

- 10 Conclusion

- 11 Frequently Asked Questions

Getting a car loan with a 500 credit score is possible, but it comes with challenges like higher interest rates and stricter terms. With the right preparation—such as saving for a larger down payment, finding a co-signer, or working with subprime lenders—you can still secure financing and rebuild your credit in the process.

Key Takeaways

- Yes, it’s possible: Many lenders specialize in working with borrowers who have poor credit, including those with a 500 credit score.

- Expect higher interest rates: With a low credit score, you’ll likely face APRs well above 15%, increasing your total loan cost.

- Down payment matters: A larger down payment (10–20%) can improve your approval odds and reduce monthly payments.

- Consider a co-signer: A trusted person with better credit can help you qualify and secure better loan terms.

- Shop around carefully: Not all subprime lenders are reputable—research and compare offers to avoid predatory practices.

- Rebuild your credit over time: Making on-time payments on your car loan can gradually improve your credit score.

- Choose an affordable vehicle: Opt for a reliable used car to keep loan amounts and insurance costs manageable.

📑 Table of Contents

- Can I Get a Car Loan with a 500 Credit Score?

- Understanding Credit Scores and Car Loans

- Types of Lenders That May Approve a 500 Credit Score

- Strategies to Improve Your Chances of Approval

- What to Expect: Loan Terms and Costs with a 500 Credit Score

- Tips to Avoid Predatory Lending and Scams

- How to Use Your Car Loan to Rebuild Credit

- Conclusion

Can I Get a Car Loan with a 500 Credit Score?

If you’ve got a credit score of 500, you’re likely wondering: “Can I really get a car loan?” The short answer is yes—but it’s not going to be easy, and it definitely won’t be cheap. A 500 credit score falls into the “poor” category on most scoring models, which means traditional banks and credit unions may turn you down. However, that doesn’t mean you’re out of options.

The good news? There are lenders who specialize in working with people who have bad credit. These are often called subprime lenders, and they’re willing to take on higher-risk borrowers—like those with a 500 credit score—in exchange for higher interest rates and stricter terms. While this might sound discouraging, it’s still a pathway to car ownership, especially if you need reliable transportation for work, school, or family responsibilities.

But before you jump into the first loan offer you see, it’s important to understand what you’re up against. Lenders view a 500 credit score as a red flag. It suggests you’ve had trouble managing debt in the past—maybe missed payments, defaulted on loans, or maxed out credit cards. Because of this, they’ll want to minimize their risk, which usually means charging you more and requiring extra safeguards like a co-signer or a large down payment.

The key is to go in prepared. With the right strategy, you can not only qualify for a car loan but also use it as a stepping stone to rebuild your credit. In this guide, we’ll walk you through everything you need to know—from understanding how your credit score affects your loan options to practical tips for getting approved and saving money in the long run.

Understanding Credit Scores and Car Loans

Visual guide about Can I Get a Car Loan with a 500 Credit Score?

Image source: balanceprocess.com

Before diving into loan options, it helps to understand how credit scores work and why they matter so much when financing a car. Your credit score is a three-digit number that summarizes your creditworthiness—basically, how likely you are to repay borrowed money. The most common scoring model is FICO, which ranges from 300 to 850.

Here’s a quick breakdown of FICO score ranges:

– 800–850: Exceptional

– 740–799: Very Good

– 670–739: Good

– 580–669: Fair

– 300–579: Poor

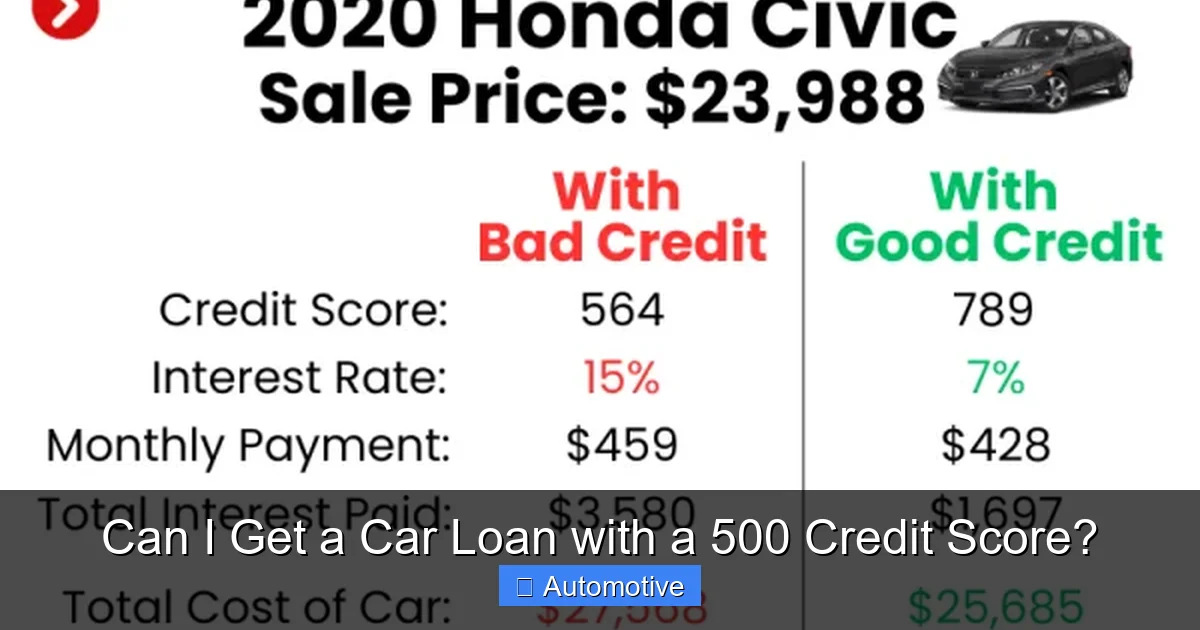

A score of 500 lands you firmly in the “poor” category. This means you’ve likely had significant credit issues in the past—such as late payments, collections, charge-offs, or even bankruptcy. Lenders use this score to assess risk. The lower your score, the higher the risk you pose, and the less likely traditional lenders are to approve your application.

When it comes to car loans, your credit score directly affects:

– Whether you’re approved

– The interest rate you’re offered

– The size of your down payment

– The loan term (length of repayment)

For example, someone with a 750 credit score might qualify for a 5% APR on a $20,000 loan, while someone with a 500 score could be offered 18% or higher. Over a 60-month term, that difference could cost thousands of extra dollars in interest.

But here’s the silver lining: your credit score isn’t the only factor lenders consider. Income, employment history, debt-to-income ratio, and down payment size also play big roles. So even with a 500 score, you can still improve your chances by strengthening these other areas.

How Lenders Evaluate Risk

Lenders don’t just look at your credit score—they look at your entire financial picture. Here’s what they typically consider:

– Credit history: How long you’ve had credit, your payment history, and any negative marks.

– Debt-to-income ratio (DTI): The percentage of your monthly income that goes toward debt payments. A lower DTI is better.

– Employment stability: Lenders prefer borrowers with steady jobs and consistent income.

– Down payment: A larger down payment reduces the lender’s risk and shows financial responsibility.

– Loan-to-value ratio (LTV): This compares the loan amount to the car’s value. A lower LTV (thanks to a bigger down payment) is more favorable.

Even with a low credit score, improving these factors can help you qualify. For instance, if you have a stable job, low monthly debts, and can put down 15–20% on a car, some lenders may be more willing to work with you.

Types of Lenders That May Approve a 500 Credit Score

Visual guide about Can I Get a Car Loan with a 500 Credit Score?

Image source: fcatadvantage-com.cdn-convertus.com

Not all lenders are created equal—especially when it comes to bad credit car loans. While major banks and credit unions often have strict credit requirements, other types of lenders are more flexible. Here are the most common options for borrowers with a 500 credit score:

Subprime Lenders

Subprime lenders specialize in loans for people with poor credit. They’re often the go-to option for those with scores below 580. These lenders understand that life happens—job loss, medical bills, unexpected expenses—and they’re willing to take on higher-risk borrowers.

However, this flexibility comes at a cost. Subprime loans typically come with:

– High interest rates (often 15% to 25% APR)

– Shorter loan terms (to reduce risk)

– Strict repayment terms

– Possible prepayment penalties

Examples of subprime lenders include Santander Consumer USA, Capital One Auto Finance (for certain applicants), and online lenders like LendingTree or MyAutoLoan, which connect you with multiple lenders.

Buy-Here-Pay-Here (BHPH) Dealerships

These are dealerships that finance car purchases directly, without involving a third-party lender. They’re often willing to work with people who have bad credit or no credit history.

The pros? Fast approval, no need for a bank, and sometimes no credit check. The cons? Higher prices, older or high-mileage vehicles, and weekly or biweekly payment requirements (often collected in person).

BHPH dealers can be a lifeline in a pinch, but they’re also known for predatory practices. Some install GPS trackers or starter interrupters that disable the car if you miss a payment. Always read the fine print and avoid dealers that pressure you or refuse to show you the contract.

Credit Unions

Some credit unions offer second-chance auto loans for members with poor credit. Because they’re nonprofit organizations, they may be more flexible than banks. They often consider your overall relationship with the credit union, not just your credit score.

To qualify, you may need to:

– Be a member for a certain period

– Have direct deposit set up

– Provide proof of income and residence

– Agree to financial counseling

While approval isn’t guaranteed, credit unions can offer lower rates than subprime lenders—sometimes 10–15% APR—making them a better long-term option if you can qualify.

Online Lenders and Loan Matching Services

Websites like AutoCreditExpress, CarsDirect, or RoadLoans allow you to fill out one application and get matched with multiple lenders. This saves time and lets you compare offers.

These platforms often work with subprime lenders, so they can be a good starting point. Just be cautious—some sites may charge fees or sell your information to third parties. Always check reviews and avoid paying upfront fees.

Strategies to Improve Your Chances of Approval

Visual guide about Can I Get a Car Loan with a 500 Credit Score?

Image source: i.pinimg.com

Even with a 500 credit score, you’re not powerless. There are several steps you can take to boost your chances of getting approved—and possibly even secure better loan terms.

Save for a Larger Down Payment

One of the most effective ways to improve your odds is to put more money down. A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk.

Aim for at least 10–20% of the car’s purchase price. For a $15,000 car, that’s $1,500 to $3,000. This not only helps with approval but also reduces your monthly payment and total interest paid.

If you can’t afford 20%, start saving now. Cut unnecessary expenses, sell unused items, or take on a side gig. Even an extra $500 can make a difference.

Get a Co-Signer

A co-signer is someone with good credit who agrees to take responsibility for the loan if you can’t make payments. This gives lenders extra confidence and can help you qualify for a lower interest rate.

Choose a co-signer wisely—preferably someone with a strong credit history and stable income. And remember: if you miss payments, it affects both your credit and theirs. Be honest with your co-signer about the risks and your commitment to repaying the loan.

Improve Your Debt-to-Income Ratio

Lenders want to see that you can afford the monthly payment. If your debts are too high relative to your income, you may be denied.

Calculate your DTI by adding up all monthly debt payments (credit cards, student loans, rent, etc.) and dividing by your gross monthly income. Aim for a DTI below 40%—lower is better.

To improve your DTI:

– Pay down credit card balances

– Avoid taking on new debt

– Increase your income if possible

Even small improvements can make a big difference in your application.

Choose an Affordable, Reliable Used Car

Lenders are more likely to approve loans for used cars than new ones—especially for borrowers with poor credit. New cars depreciate quickly, and lenders see them as riskier investments.

Instead, look for a reliable used car in the $8,000–$15,000 range. Focus on models known for longevity and low maintenance costs, such as:

– Honda Civic or Accord

– Toyota Corolla or Camry

– Ford Focus (pre-2018 models)

– Hyundai Elantra

Avoid luxury brands, high-mileage vehicles, or cars with a history of mechanical issues. A well-maintained used car can save you money on the loan, insurance, and repairs.

Check Your Credit Report for Errors

Before applying, pull your free credit reports from AnnualCreditReport.com. Look for errors—like accounts you didn’t open, incorrect balances, or outdated negative marks.

If you find mistakes, dispute them with the credit bureau. Correcting errors can boost your score by 20–50 points, which might push you into a better loan tier.

Even if your score doesn’t jump to 600, fixing errors shows lenders you’re proactive about your credit—a positive signal.

What to Expect: Loan Terms and Costs with a 500 Credit Score

If you’re approved for a car loan with a 500 credit score, here’s what you can typically expect:

High Interest Rates

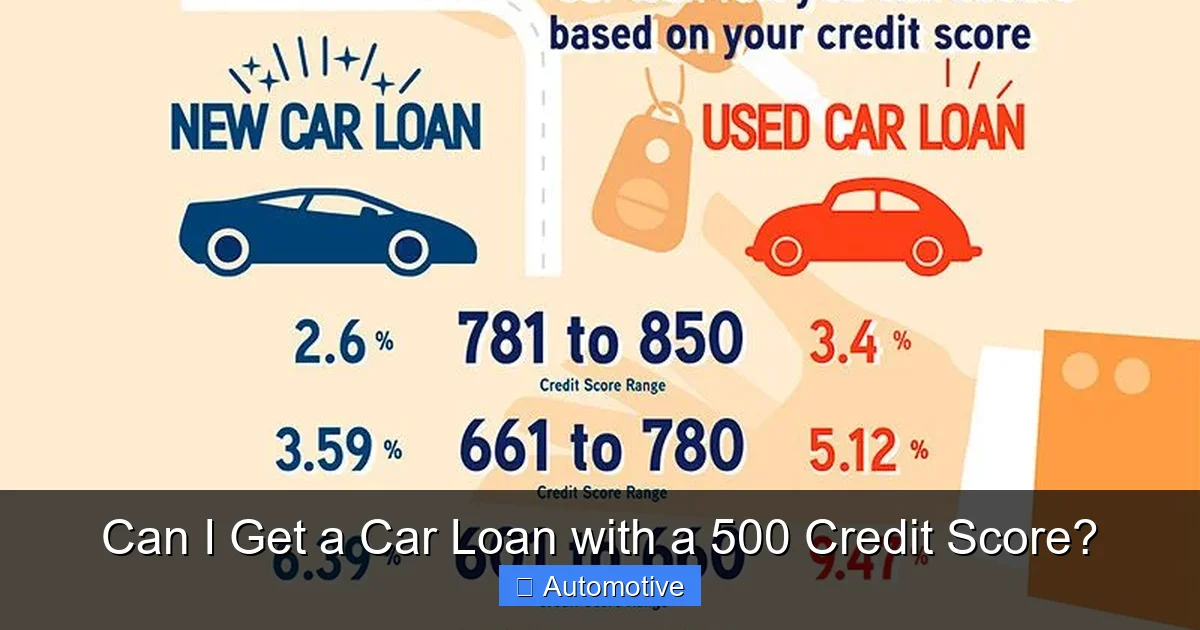

Interest rates for borrowers with poor credit are significantly higher than average. While the national average auto loan rate hovers around 5–7% for good credit, someone with a 500 score might see rates between 15% and 25%.

For example:

– A $15,000 loan at 6% over 60 months = $289/month, $2,340 in total interest

– The same loan at 20% = $396/month, $8,760 in total interest

That’s over $6,000 more in interest—just because of the rate difference.

Shorter Loan Terms

Subprime lenders often offer shorter repayment periods (36 to 60 months) to reduce their risk. While this means higher monthly payments, it also means you’ll pay less interest over time and own the car sooner.

Avoid stretching the loan beyond 60 months if possible. Longer terms may lower your monthly payment, but they increase total interest and the risk of being “upside down” (owing more than the car is worth).

Strict Payment Requirements

Some lenders require:

– Automatic payments from your bank account

– Proof of income and residence

– GPS tracking or starter interrupters (especially with BHPH dealers)

– Weekly or biweekly payment schedules

These measures help ensure repayment but can feel invasive. Make sure you understand all terms before signing.

Higher Insurance Costs

Lenders require full coverage insurance (comprehensive and collision) on financed vehicles. With a low credit score, your insurance premiums may also be higher, as some insurers use credit-based insurance scores to set rates.

Shop around for insurance quotes and consider raising your deductible to lower monthly costs—just make sure you can afford it if you need to file a claim.

Tips to Avoid Predatory Lending and Scams

Unfortunately, the bad credit car loan market attracts unscrupulous lenders. Protect yourself with these tips:

Read the Fine Print

Never sign a loan agreement without reading every word. Look for:

– Hidden fees (origination, documentation, prepayment penalties)

– Balloon payments (large final payment)

– Variable interest rates (can increase over time)

– Mandatory add-ons (extended warranties, GAP insurance)

If something seems unclear or too good to be true, ask questions or walk away.

Avoid “No Credit Check” Loans

Legitimate lenders always check your credit—even if they say they don’t. “No credit check” offers are often scams or BHPH dealers with extremely high rates.

If a lender refuses to show you your credit report or won’t explain how they evaluate applicants, it’s a red flag.

Don’t Pay Upfront Fees

Reputable lenders don’t ask for money before approving your loan. If someone demands a fee to “hold” a car or “process” your application, it’s likely a scam.

Legitimate lenders deduct fees from the loan amount or roll them into the financing.

Get Everything in Writing

Verbal promises aren’t binding. Make sure all terms—interest rate, monthly payment, loan term, fees—are clearly stated in the contract.

If the dealer or lender changes terms at the last minute, don’t sign. Walk away and find a more transparent option.

Use the “Cooling-Off” Rule

In most states, you have a short window (usually 3 days) to cancel a car purchase without penalty. Use this time to review the contract, compare offers, and make sure you’re comfortable with the terms.

How to Use Your Car Loan to Rebuild Credit

Getting a car loan with a 500 credit score isn’t just about transportation—it’s also an opportunity to improve your financial future. Here’s how to turn your loan into a credit-building tool:

Make On-Time Payments

Payment history is the biggest factor in your credit score (35% of your FICO score). Even one late payment can hurt your score, so set up automatic payments or calendar reminders.

If you’re struggling to pay, contact your lender immediately. Many offer hardship programs or payment deferrals.

Pay More Than the Minimum

Paying extra each month reduces your principal faster, saves on interest, and shows lenders you’re responsible. Even $20 extra can make a difference over time.

Monitor Your Credit

Use free services like Credit Karma, Experian, or your bank’s credit monitoring tool to track your score. You’ll see how your on-time payments are helping—and catch any errors early.

Keep the Loan Open

Closing the account too soon can shorten your credit history and hurt your score. Keep the loan active until it’s paid off, then let it remain on your report as a positive mark.

Avoid New Debt

While rebuilding credit, avoid opening new credit cards or taking on other loans. Focus on managing your car payment and existing debts.

Conclusion

Yes, you can get a car loan with a 500 credit score—but it requires careful planning, realistic expectations, and a commitment to responsible borrowing. While the process is tougher and more expensive than for borrowers with good credit, it’s not impossible.

By saving for a down payment, finding a co-signer, choosing an affordable used car, and working with reputable lenders, you can secure financing and start rebuilding your credit. Just remember: the goal isn’t just to get a car—it’s to use this loan as a stepping stone toward better financial health.

Take your time, shop around, and never rush into a deal that doesn’t feel right. With patience and persistence, you can drive away in a reliable vehicle and move closer to a brighter financial future.

Frequently Asked Questions

Can I get a car loan with a 500 credit score?

Yes, it’s possible to get a car loan with a 500 credit score, but you’ll likely need to work with subprime lenders or buy-here-pay-here dealerships. Expect higher interest rates and stricter terms.

What interest rate can I expect with a 500 credit score?

Interest rates for a 500 credit score typically range from 15% to 25% APR, depending on the lender, your income, and down payment. This is significantly higher than rates for borrowers with good credit.

Do I need a down payment with a 500 credit score?

While not always required, a down payment of 10–20% greatly improves your chances of approval and can lower your monthly payment. Lenders see it as a sign of financial responsibility.

Can a co-signer help me get approved?

Yes, a co-signer with good credit can increase your approval odds and help you secure a lower interest rate. Just remember, they’re equally responsible for the loan if you miss payments.

Will a car loan help improve my credit score?

Yes, making on-time payments on your car loan can gradually improve your credit score. Payment history is the largest factor in your credit score, so consistency is key.

Are buy-here-pay-here dealerships safe?

Some BHPH dealers are legitimate, but others use predatory practices like high markups, GPS tracking, or starter interrupters. Always read the contract carefully and avoid dealers who pressure you or refuse transparency.