How Much Is a Chrysler Pension?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is a Chrysler Pension? A Complete Guide for Employees and Retirees

- 4 Understanding Chrysler’s Pension Plans: A Historical Overview

- 5 How Chrysler Pension Benefits Are Calculated

- 6 Eligibility Requirements for a Chrysler Pension

- 7 Real-World Examples: How Much Do Chrysler Retirees Actually Receive?

- 8 Protecting Your Chrysler Pension: What Happens If the Company Struggles?

- 9 Tips for Maximizing Your Chrysler Pension

- 10 Conclusion: Planning for a Secure Retirement with a Chrysler Pension

- 11 Frequently Asked Questions

Understanding how much a Chrysler pension pays depends on several factors, including years of service, salary history, and retirement age. This guide breaks down the key elements of Chrysler’s pension plans, eligibility requirements, and real-world examples to help retirees and employees estimate their benefits.

Key Takeaways

- Chrysler pensions are based on a formula: Typically, benefits are calculated using years of service, average earnings, and a multiplier set by the plan.

- Eligibility requires meeting age and service thresholds: Most employees must be at least 55 years old with 10 years of service to qualify for full benefits.

- Pension amounts vary widely: Monthly payouts can range from a few hundred to over $3,000, depending on career length and salary.

- Early retirement reduces benefits: Retiring before the normal retirement age (usually 65) results in a permanent reduction in monthly payments.

- The Pension Benefit Guaranty Corporation (PBGC) provides protection: If Chrysler’s pension plan fails, PBGC may insure a portion of your benefits.

- Survivor benefits are available: Spouses and dependents may continue receiving payments after the retiree’s death, depending on the payout option chosen.

- Recent changes have affected new hires: Employees hired after certain dates may be enrolled in hybrid or 401(k)-style plans instead of traditional pensions.

📑 Table of Contents

- How Much Is a Chrysler Pension? A Complete Guide for Employees and Retirees

- Understanding Chrysler’s Pension Plans: A Historical Overview

- How Chrysler Pension Benefits Are Calculated

- Eligibility Requirements for a Chrysler Pension

- Real-World Examples: How Much Do Chrysler Retirees Actually Receive?

- Protecting Your Chrysler Pension: What Happens If the Company Struggles?

- Tips for Maximizing Your Chrysler Pension

- Conclusion: Planning for a Secure Retirement with a Chrysler Pension

How Much Is a Chrysler Pension? A Complete Guide for Employees and Retirees

If you’ve worked for Chrysler—or are currently employed by the automaker—you’ve probably asked yourself: How much is a Chrysler pension? It’s a fair and important question, especially when planning for retirement. Unlike a simple savings account, pension benefits aren’t just a fixed number. They’re calculated using a formula that takes into account your years of service, salary history, age at retirement, and the specific terms of the pension plan you’re enrolled in.

Chrysler, like many large manufacturers, has historically offered defined benefit pension plans to its employees. These plans promise a guaranteed monthly income for life after retirement, which can be a huge financial relief. But because the auto industry has undergone major changes—including bankruptcies, mergers, and shifts in labor contracts—the structure of Chrysler pensions has evolved over time. That means the answer to “how much is a Chrysler pension?” isn’t one-size-fits-all. It depends on when you were hired, your job classification, and the collective bargaining agreements in place during your employment.

In this guide, we’ll walk you through everything you need to know about Chrysler pensions. From how they’re calculated to who qualifies, and what to expect in monthly payouts, we’ll break it down in plain, easy-to-understand language. Whether you’re a long-time employee nearing retirement or just starting your career at Stellantis (the parent company formed after the Chrysler-Fiat merger), this article will help you understand your potential pension benefits and how to maximize them.

Understanding Chrysler’s Pension Plans: A Historical Overview

Visual guide about How Much Is a Chrysler Pension?

Image source: blackrock.com

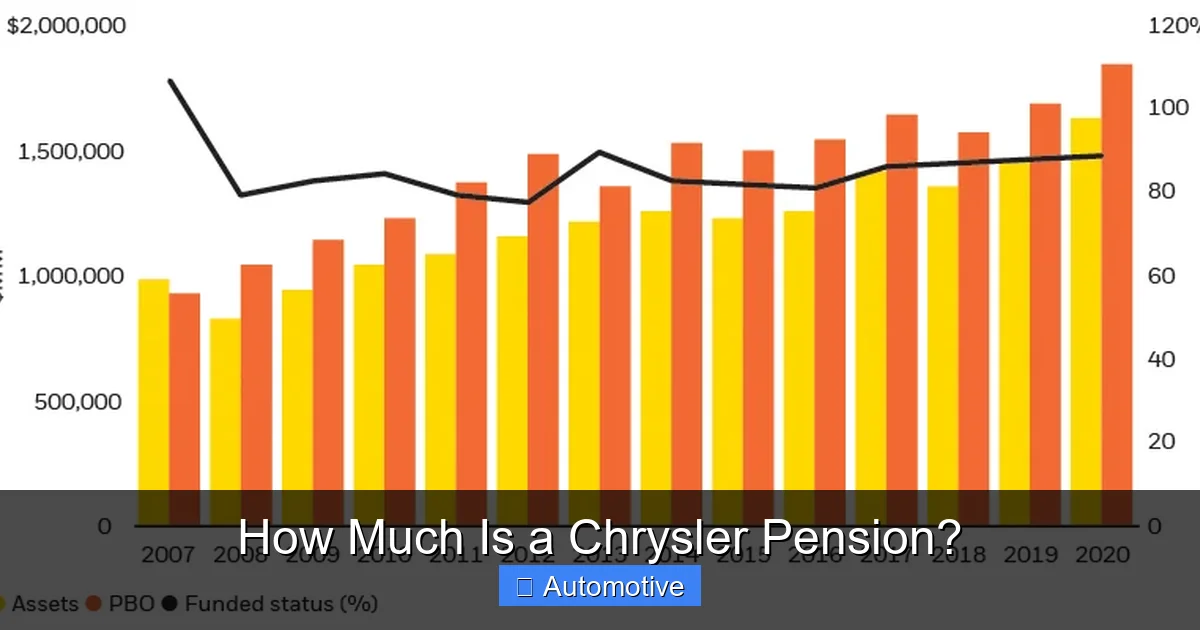

To truly grasp how much a Chrysler pension pays, it helps to understand the company’s pension history. Chrysler has offered pension benefits to its unionized workers—primarily through the United Auto Workers (UAW) union—for decades. These plans were designed to reward long-term employees with a stable retirement income, especially in an industry known for physically demanding jobs and early retirement incentives.

In the past, Chrysler’s traditional defined benefit pension plan was a cornerstone of employee compensation. Workers earned pension credits based on their years of service, and the final benefit was calculated using a formula that multiplied their average earnings (usually over the last few years of employment) by a set percentage. For example, a common formula might be: 1.5% × average salary × years of service. So, someone with 30 years of service and an average salary of $60,000 would receive an annual pension of $27,000, or $2,250 per month.

However, the landscape changed dramatically in the 2000s. The 2008 financial crisis hit the auto industry hard, leading to Chrysler’s bankruptcy and government bailout. As part of the restructuring, the company and the UAW renegotiated labor contracts to reduce long-term liabilities. One major change was the shift away from traditional pensions for newer employees. Starting around 2007 and accelerating after the 2009 bankruptcy, new hires were often placed into hybrid plans or defined contribution plans (like 401(k)s) instead of the classic pension.

Today, most Chrysler pension benefits are frozen for current retirees and long-term employees, meaning no new accruals are being added. But those who are already vested can still receive their full benefits upon retirement. The key takeaway? If you were hired before the mid-2000s, you likely have a traditional pension. If you were hired later, you may be in a different type of retirement plan.

The Role of the UAW in Pension Negotiations

The United Auto Workers union has played a central role in shaping Chrysler’s pension benefits. Through collective bargaining, the UAW has negotiated pension formulas, retirement ages, and cost-of-living adjustments (COLAs) for decades. These agreements are typically renewed every four years and can significantly impact how much a Chrysler pension pays.

For example, during the 2015 UAW-Chrysler contract negotiations, the union secured improvements in retirement benefits for certain groups, including enhanced early retirement options and better pension multipliers for skilled trades workers. However, the same contract also introduced a two-tier system that reduced benefits for newer hires, moving them into a cash balance plan—a type of hybrid pension that blends features of defined benefit and defined contribution plans.

Because of these negotiations, pension benefits can vary even among employees who worked at the same plant. Job classification, seniority, and the year you were hired all influence your final payout. That’s why it’s essential to review your individual pension statement and understand the specific terms of your plan.

Chrysler’s Transition to Stellantis and Its Impact on Pensions

In 2021, Chrysler’s parent company, Fiat Chrysler Automobiles (FCA), merged with PSA Group to form Stellantis. This merger created one of the world’s largest automakers, but it also raised questions about the future of employee benefits, including pensions.

So far, Stellantis has maintained existing pension obligations for current retirees and vested employees. The traditional defined benefit plans remain in place for those who qualify. However, the company has continued the trend of offering less generous retirement benefits to new hires. Today, most new employees at Stellantis are enrolled in a 401(k) plan with company matching, rather than a traditional pension.

This shift reflects a broader trend in the American workforce: the decline of defined benefit pensions in favor of defined contribution plans. While 401(k)s offer more portability and control, they also place more risk on the employee. With a pension, the employer guarantees a set income for life. With a 401(k), your retirement savings depend on market performance and your own investment choices.

For those asking, “How much is a Chrysler pension?” the answer is clearer for older employees: it’s likely a traditional pension with predictable payouts. For younger workers, the answer may be more complex, involving a mix of 401(k) savings and possibly a cash balance plan.

How Chrysler Pension Benefits Are Calculated

Visual guide about How Much Is a Chrysler Pension?

Image source: ncro.org

Now let’s get into the nitty-gritty: how exactly is a Chrysler pension calculated? The formula used depends on your employment date, job classification, and the specific pension plan you’re enrolled in. But for most long-term employees, the calculation follows a standard defined benefit formula.

The Standard Pension Formula

The most common formula for Chrysler pensions is:

Annual Pension = (Multiplier) × (Average Final Earnings) × (Years of Service)

Let’s break this down:

– Multiplier: This is a percentage set by the plan, typically between 1.25% and 1.75%. For example, if the multiplier is 1.5%, you earn 1.5% of your average salary for each year you work.

– Average Final Earnings: This is usually the average of your highest-paid consecutive years, often the last three to five years of employment. Some plans use a “career average” instead, but final earnings are more common in union contracts.

– Years of Service: This is the total number of years you’ve worked for Chrysler, including part-time and overtime, as defined by the plan.

Let’s look at a practical example:

Maria worked for Chrysler for 32 years. Her average final earnings (over her last three years) were $65,000. The pension multiplier for her plan is 1.6%. Her annual pension would be:

1.6% × $65,000 × 32 = $33,280 per year

That’s $2,773 per month for life.

Early Retirement and Benefit Reductions

One of the most important factors in determining how much a Chrysler pension pays is your age at retirement. The “normal retirement age” for most Chrysler plans is 65. If you retire at 65 or later, you receive 100% of your calculated benefit.

But many employees retire earlier—often in their late 50s or early 60s. Chrysler offers early retirement options, but they come with a catch: your monthly benefit is permanently reduced.

The reduction is typically actuarially calculated, meaning it accounts for the fact that you’ll receive payments for a longer period. For example, retiring at age 60 might reduce your benefit by 5% to 7% per year before age 65. So if your full benefit at 65 is $2,773, retiring at 60 could reduce it to around $2,100 per month.

Some plans offer “rule of 85” or “30-and-out” provisions, which allow full benefits if you meet certain age and service combinations. For instance, if you’re 55 and have 30 years of service, you might qualify for unreduced benefits. These rules vary by contract and are often negotiated during UAW talks.

Cost-of-Living Adjustments (COLAs)

Another factor that affects how much a Chrysler pension pays over time is whether your plan includes cost-of-living adjustments (COLAs). COLAs increase your monthly benefit each year to keep up with inflation.

Historically, some Chrysler pension plans included modest COLAs, especially for retirees who had been out of work for many years. However, in recent contracts, COLAs have been reduced or eliminated to help control costs. Many current retirees receive little to no annual increases, which means their purchasing power can erode over time.

For example, a retiree receiving $2,000 per month in 2010 would need over $2,800 per month today to maintain the same standard of living due to inflation. Without a COLA, that retiree is effectively losing ground each year.

Eligibility Requirements for a Chrysler Pension

Visual guide about How Much Is a Chrysler Pension?

Image source: vehq.com

Not everyone who works for Chrysler automatically qualifies for a pension. To receive benefits, you must meet specific eligibility criteria, which are outlined in your pension plan documents.

Vesting Requirements

The first step to earning a pension is “vesting.” Vesting means you’ve worked long enough to earn a right to your pension benefits, even if you leave the company before retiring.

For most Chrysler pension plans, the vesting period is five years. This means if you work for Chrysler for five years or more, you’re entitled to a pension when you reach retirement age—even if you quit or are laid off before then.

Some older plans had a 10-year vesting period, but the Employee Retirement Income Security Act (ERISA) now requires most private-sector pensions to vest within five years (or seven under a graded schedule).

Age and Service Requirements

In addition to vesting, you must meet age and service requirements to start receiving benefits. The most common thresholds are:

– Normal Retirement: Age 65 with at least five years of service.

– Early Retirement: Age 55 with 10 years of service (benefits reduced).

– Special Early Retirement: Age 50 with 25 years of service, or age 55 with 30 years (may offer unreduced benefits under certain contracts).

These rules can vary depending on your job classification and the year you were hired. For example, skilled trades workers (like electricians or machinists) often have more generous early retirement options than production workers.

Survivor Benefits and Payout Options

When you retire, you’ll also choose how your pension is paid out. The most common option is a single-life annuity, which provides the highest monthly payment but stops when you die. However, many retirees choose a joint-and-survivor option, which reduces the monthly amount but continues payments to a spouse or dependent after death.

For example, a 50% joint-and-survivor option might reduce your monthly benefit by 10–15%, but your spouse would receive half of that amount for life after you pass away. This can be a smart choice for married couples who want to ensure financial security for the surviving partner.

Some plans also offer a lump-sum option, allowing you to take your entire pension as a one-time payment. However, this is rare for traditional defined benefit plans and usually only available under specific circumstances.

Real-World Examples: How Much Do Chrysler Retirees Actually Receive?

To answer “how much is a Chrysler pension?” in practical terms, let’s look at a few real-world scenarios based on typical employee profiles.

Example 1: Long-Term Production Worker

John worked on the assembly line at a Chrysler plant for 35 years. He retired at age 62 with an average final salary of $58,000. His pension multiplier is 1.5%.

Calculation:

1.5% × $58,000 × 35 = $30,450 per year

Monthly: $2,537

Because he retired three years early, his benefit is reduced by about 6% per year (18% total).

Adjusted monthly benefit: $2,080

John also chose a 50% joint-and-survivor option, reducing his payment by 12%.

Final monthly pension: $1,830

Example 2: Skilled Trades Employee

Linda was a plant electrician for 28 years. She retired at age 60 with an average salary of $72,000. Her multiplier is 1.7%.

Calculation:

1.7% × $72,000 × 28 = $34,272 per year

Monthly: $2,856

She retired five years early, so her benefit is reduced by 30%.

Adjusted monthly: $1,999

She selected a single-life annuity (no survivor benefit), so no further reduction.

Final monthly pension: $1,999

Example 3: Manager or Salaried Employee

David was a mid-level manager for 25 years, retiring at 65 with an average salary of $85,000. His multiplier is 1.6%.

Calculation:

1.6% × $85,000 × 25 = $34,000 per year

Monthly: $2,833

He retired at normal retirement age, so no reduction.

Final monthly pension: $2,833

These examples show that Chrysler pensions can provide a solid foundation for retirement, especially for long-term employees. However, the amount varies widely based on salary, service length, and retirement choices.

Protecting Your Chrysler Pension: What Happens If the Company Struggles?

Given Chrysler’s financial troubles in the past, many retirees worry: “What if the company goes bankrupt again? Will I lose my pension?”

The good news is that most Chrysler pension benefits are protected by the Pension Benefit Guaranty Corporation (PBGC), a federal agency that insures private-sector defined benefit plans. If Chrysler’s pension plan were to fail, the PBGC would step in to pay benefits up to certain limits.

As of 2023, the PBGC guarantees up to about $6,750 per month for a 65-year-old retiree (the exact amount is adjusted annually). That means even if Chrysler couldn’t fund its pension, most retirees would still receive the majority of their benefits.

However, there are limits. High-income retirees may receive less than their full pension if their benefit exceeds the PBGC cap. Also, COLAs and certain early retirement subsidies are not fully protected.

To check the status of your pension and understand your protections, you can contact the PBGC or request a copy of your plan’s summary plan description (SPD) from HR or the UAW.

Tips for Maximizing Your Chrysler Pension

If you’re still working or planning for retirement, here are some practical tips to help you get the most from your Chrysler pension:

– Work as long as possible: Each additional year of service increases your benefit. Delaying retirement past age 65 may also increase your monthly payout in some plans.

– Understand your payout options: Compare single-life, joint-and-survivor, and lump-sum options to find the best fit for your family.

– Review your pension statement annually: Make sure your service years and salary history are accurate.

– Consider spousal benefits: If you’re married, a joint-and-survivor option can provide lifelong security for your partner.

– Supplement with savings: Even with a pension, it’s wise to contribute to a 401(k) or IRA to boost your retirement income.

Conclusion: Planning for a Secure Retirement with a Chrysler Pension

So, how much is a Chrysler pension? The answer isn’t a single number—it’s a personalized calculation based on your career, salary, and retirement choices. For many long-term employees, a Chrysler pension provides a reliable, lifelong income that can make retirement comfortable and stress-free.

But it’s important to understand the details: how your benefit is calculated, when you can retire, and what options are available to you and your family. With the right planning, your Chrysler pension can be a cornerstone of your financial future.

Whether you’re decades away from retirement or counting down the months, take the time to review your pension benefits, talk to a financial advisor, and make informed decisions. Your future self will thank you.

Frequently Asked Questions

How is a Chrysler pension calculated?

A Chrysler pension is typically calculated using a formula: (Multiplier) × (Average Final Earnings) × (Years of Service). The multiplier is usually between 1.25% and 1.75%, and average earnings are based on your highest-paid years.

Can I receive my Chrysler pension if I leave before retirement?

Yes, if you’re vested—usually after five years of service—you can receive your pension when you reach the eligible retirement age, even if you no longer work for Chrysler.

What happens to my pension if Chrysler goes bankrupt?

Most Chrysler pensions are insured by the PBGC, a federal agency. If the plan fails, the PBGC will pay benefits up to legal limits, protecting most retirees from total loss.

Do Chrysler pensions include cost-of-living adjustments?

Some older plans included modest COLAs, but recent contracts have reduced or eliminated them. Check your plan documents to see if your pension includes inflation protection.

Can I take my Chrysler pension as a lump sum?

Lump-sum options are rare for traditional defined benefit plans. Most retirees receive monthly payments for life, though some hybrid plans may offer lump-sum choices.

Are new Chrysler employees eligible for a pension?

Most new hires are enrolled in 401(k) plans or hybrid cash balance plans, not traditional pensions. Pension benefits are generally limited to employees hired before the mid-2000s.