How Much Is Gap Insurance Through Toyota?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is GAP Insurance and Why Do You Need It?

- 4 How Much Does GAP Insurance Cost Through Toyota?

- 5 How to Get GAP Insurance Through Toyota

- 6 Is Toyota GAP Insurance Worth It?

- 7 Alternatives to Toyota GAP Insurance

- 8 Real-Life Example: How GAP Insurance Saved a Toyota Owner

- 9 Tips for Buying GAP Insurance Through Toyota

- 10 Conclusion

- 11 Frequently Asked Questions

GAP insurance through Toyota helps cover the difference between your car’s actual cash value and your loan balance if your vehicle is totaled or stolen. Costs vary based on loan amount, vehicle type, and term length, typically ranging from $500 to $1,200, but can save you thousands in out-of-pocket expenses.

[FEATURED_IMAGE_PLACEHODELR]

So, you’ve just driven off the lot in a shiny new Toyota—or maybe a reliable certified pre-owned model—and you’re feeling great. But have you thought about what happens if your car is totaled in an accident or stolen? You might assume your regular auto insurance will cover everything, but here’s the catch: standard policies only pay the car’s *actual cash value* at the time of the loss. And because new cars lose value fast—sometimes 20% or more in the first year—you could end up owing more on your loan than the insurance company pays out. That’s where GAP insurance comes in.

GAP stands for “Guaranteed Asset Protection,” and it’s designed to bridge that financial gap. If your Toyota is declared a total loss, GAP insurance covers the difference between what your auto insurer pays and what you still owe on your loan or lease. Think of it as a safety net for your finances. And the good news? Toyota offers its own GAP insurance program through Toyota Financial Services (TFS), making it easy to add this protection when you finance your vehicle.

But how much does it actually cost? That’s the million-dollar question—or at least the few-thousand-dollar one. The price of GAP insurance through Toyota isn’t one-size-fits-all. It depends on several factors, including your loan amount, the type of vehicle, the length of your financing term, and even your credit profile. On average, you can expect to pay between $500 and $1,200 for Toyota GAP coverage. While that might sound like a lot upfront, it’s often rolled into your monthly car payment, so you don’t have to pay it all at once. And when you consider the potential financial protection it offers, many drivers find it’s a small price to pay for peace of mind.

Key Takeaways

- GAP insurance through Toyota covers the “gap” between your car’s depreciated value and your outstanding loan balance. This is crucial if your car is totaled or stolen and your auto insurance payout falls short.

- Costs typically range from $500 to $1,200, depending on loan amount, vehicle type, and financing term. It’s often rolled into your monthly car payment, making it easy to manage.

- Toyota offers GAP insurance for new, used, and certified pre-owned (CPO) vehicles financed through Toyota Financial Services (TFS). It’s available at the time of purchase or lease.

- The coverage is especially valuable for long-term loans (60+ months), low down payments, or vehicles that depreciate quickly. These factors increase the risk of being “upside-down” on your loan.

- GAP insurance is not automatically included—you must opt in when financing your vehicle. Be sure to ask your dealer or TFS representative about adding it.

- Claims are processed quickly through Toyota’s partnership with third-party administrators. If approved, the gap amount is paid directly to your lender.

- Consider alternatives like lender-offered GAP or standalone policies, but Toyota’s program offers convenience and seamless integration. Weigh cost, coverage, and ease of use before deciding.

📑 Table of Contents

- What Is GAP Insurance and Why Do You Need It?

- How Much Does GAP Insurance Cost Through Toyota?

- How to Get GAP Insurance Through Toyota

- Is Toyota GAP Insurance Worth It?

- Alternatives to Toyota GAP Insurance

- Real-Life Example: How GAP Insurance Saved a Toyota Owner

- Tips for Buying GAP Insurance Through Toyota

- Conclusion

What Is GAP Insurance and Why Do You Need It?

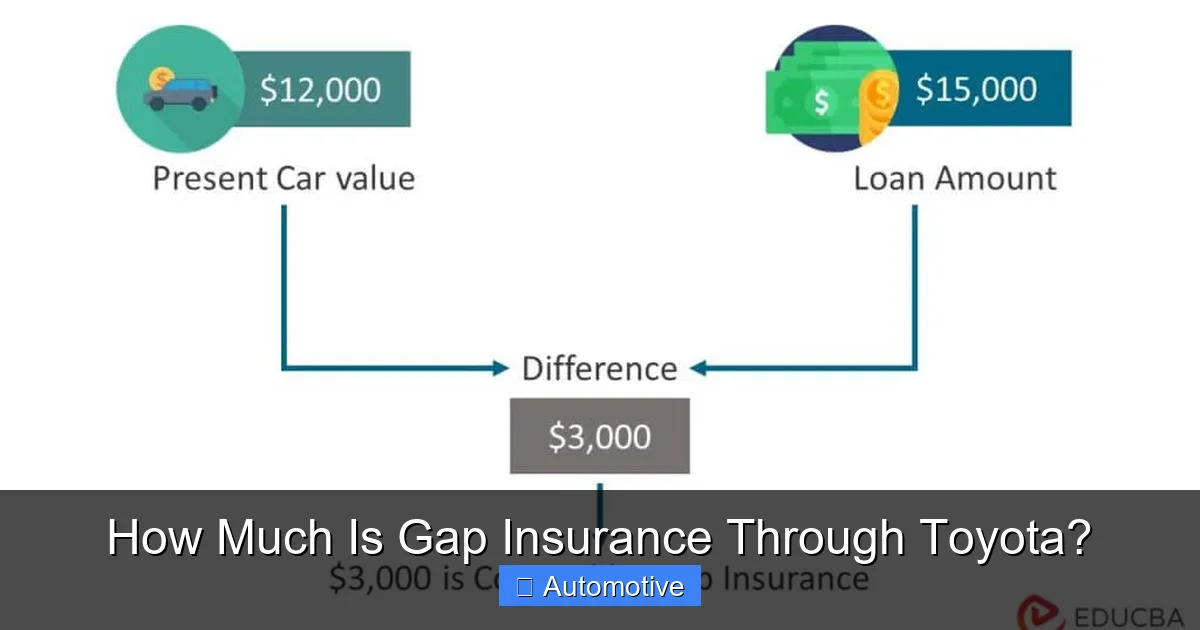

Let’s start with the basics. GAP insurance isn’t something you hear about every day—until you need it. And by then, it might be too late. So, what exactly is it? In simple terms, GAP insurance covers the difference between the amount you owe on your car loan or lease and the car’s current market value if it’s totaled or stolen. This “gap” can be significant, especially in the early years of ownership when depreciation is steep.

For example, imagine you buy a new Toyota RAV4 for $35,000 with a $5,000 down payment and a 6-year loan. That means you’re financing $30,000. But after just one year, the car’s value might drop to $25,000 due to depreciation. Now, if your RAV4 is totaled in an accident, your auto insurance will likely pay only $25,000—the actual cash value. But you still owe $27,500 on your loan. That leaves you with a $2,500 gap that you’d have to pay out of pocket. Ouch.

This is where GAP insurance saves the day. If you had Toyota’s GAP coverage, that $2,500 would be covered, and your loan would be paid off in full. You walk away with no debt and can use any remaining insurance payout (if applicable) toward a new vehicle.

Who Needs GAP Insurance?

Not every driver needs GAP insurance, but it’s especially valuable for certain situations. If you’re financing a new Toyota with little or no down payment, you’re more likely to owe more than the car is worth—especially in the first few years. The same goes for long-term loans (60 months or more), which increase the risk of being “upside-down” on your loan.

Leased vehicles are another common scenario. Since leases often require low or no down payments and have higher monthly payments, the gap risk is even greater. Plus, many lease agreements actually require GAP insurance, so it’s not optional.

Even if you put money down, some vehicles depreciate faster than others. Luxury models, high-mileage cars, and certain SUVs can lose value quickly. If you’re driving a Toyota that’s in high demand now but might not hold its value long-term, GAP insurance could be a smart move.

How GAP Insurance Works with Your Auto Policy

It’s important to understand that GAP insurance doesn’t replace your regular auto insurance—it works alongside it. When your Toyota is totaled or stolen, your primary auto insurer will first assess the damage and determine the actual cash value (ACV) of the vehicle. They’ll then issue a payout up to that amount, minus your deductible.

Once that’s done, GAP insurance kicks in. It reviews your loan or lease balance and pays the difference between the ACV and what you still owe. For example, if your insurance pays $22,000 and you owe $26,000, GAP covers the remaining $4,000. In some cases, if the insurance payout is higher than your loan balance, you may even receive a small refund.

The process is usually handled directly between Toyota Financial Services and the GAP administrator, so you don’t have to chase down payments. Claims are typically processed within a few weeks, and the funds go straight to your lender.

How Much Does GAP Insurance Cost Through Toyota?

Visual guide about How Much Is Gap Insurance Through Toyota?

Image source: gapinsurancequotes.org

Now for the big question: how much will it cost you? The price of GAP insurance through Toyota isn’t fixed—it varies based on several key factors. But on average, most buyers pay between $500 and $1,200 for coverage. That might seem steep, but remember: it’s often financed into your monthly car payment, so you’re not paying it all at once.

Let’s break down what influences the cost:

Loan Amount and Term Length

The bigger your loan and the longer your term, the higher the risk of a significant gap. For example, a $35,000 loan over 72 months will likely cost more for GAP insurance than a $20,000 loan over 48 months. This is because longer terms mean more time for depreciation to outpace loan repayment.

Vehicle Type and Age

Newer, more expensive vehicles tend to have higher GAP premiums because they depreciate faster. A brand-new Toyota Camry will cost more to insure with GAP than a 3-year-old Corolla. Similarly, luxury models like the Toyota Crown or high-end SUVs may come with higher rates.

Down Payment and Equity

If you put a large down payment (say, 20% or more), you’re less likely to be upside-down on your loan. As a result, your GAP insurance cost may be lower. Conversely, zero-down financing increases the risk and the price.

Credit and Financing Terms

While GAP insurance isn’t directly tied to your credit score, your overall financing package can influence the cost. Buyers with lower credit may face higher interest rates and longer terms, which can indirectly increase the GAP premium.

Example Cost Breakdown

Here’s a real-world example to put it in perspective:

– Vehicle: 2024 Toyota Highlander, MSRP $42,000

– Down payment: $3,000

– Loan amount: $39,000

– Term: 66 months

– GAP insurance cost: ~$850

This $850 would typically be added to your loan and paid off over the 66-month term, adding about $13 to your monthly payment. If the Highlander is totaled after two years, and your insurance pays $28,000 while you still owe $32,000, GAP covers the $4,000 difference.

How to Get GAP Insurance Through Toyota

Visual guide about How Much Is Gap Insurance Through Toyota?

Image source: shunins.com

Getting GAP insurance through Toyota is straightforward—if you know to ask for it. It’s not automatically included in your financing package, so you’ll need to request it when you’re signing your loan or lease agreement.

Step-by-Step Process

1. **Talk to Your Dealer or TFS Representative**: When you’re finalizing your financing, ask about adding GAP insurance. Most Toyota dealerships offer it through Toyota Financial Services.

2. **Review the Coverage Details**: Make sure you understand what’s covered. Toyota’s GAP insurance typically covers the difference between your loan balance and the ACV, up to the original loan amount. Some plans may also include a deductible waiver.

3. **Confirm the Cost**: Ask for a clear breakdown of the premium and how it will be paid—either as a lump sum or rolled into your monthly payment.

4. **Sign the Agreement**: Once you agree, the coverage is activated and tied to your loan.

5. **Keep Your Documentation**: Save a copy of your GAP insurance contract and any confirmation emails. You’ll need this if you ever file a claim.

Eligibility Requirements

To qualify for Toyota’s GAP insurance, your vehicle must be:

– A new, used, or certified pre-owned Toyota

– Financed or leased through Toyota Financial Services

– Covered by a comprehensive and collision auto insurance policy

The coverage must be purchased at the time of financing—retroactive purchases are generally not allowed.

Can You Cancel GAP Insurance?

Yes, in most cases you can cancel your GAP insurance, but the rules vary. Some plans allow cancellation after a certain period (e.g., 12–24 months), especially if you’ve built up enough equity in the vehicle. Others may offer a partial refund if you pay off your loan early.

Always check your contract or contact TFS to understand the cancellation policy. Keep in mind that if you sell or trade in your car, the GAP coverage typically ends, and you won’t receive a refund unless specified.

Is Toyota GAP Insurance Worth It?

Visual guide about How Much Is Gap Insurance Through Toyota?

Image source: cdn.educba.com

This is the million-dollar question—or at least the few-thousand-dollar one. Is GAP insurance through Toyota worth the cost? The answer depends on your financial situation, driving habits, and the type of vehicle you’re buying.

When It’s Worth It

GAP insurance makes the most sense if:

– You’re financing a new Toyota with little or no down payment

– You have a long loan term (60+ months)

– You’re leasing your vehicle

– You’re buying a model that depreciates quickly

– You’re concerned about financial risk in case of a total loss

For example, if you’re leasing a Toyota Prius Prime with a $0 down payment and a 36-month lease, GAP insurance is almost always a good idea. The same goes for someone financing a new Tundra with a 72-month loan and only $2,000 down.

When You Might Skip It

You might consider skipping GAP insurance if:

– You’ve made a large down payment (20% or more)

– You’re financing for a short term (36–48 months)

– You’re buying a used Toyota that’s already depreciated significantly

– You have strong emergency savings to cover a potential gap

For instance, if you buy a 3-year-old Toyota Camry for $18,000 with a $5,000 down payment and a 48-month loan, you’re less likely to be upside-down. In that case, GAP insurance might not be necessary.

Weighing the Cost vs. Benefit

At $500–$1,200, GAP insurance isn’t cheap. But compare that to the potential out-of-pocket cost of a $3,000–$5,000 gap. If your car is totaled, that’s money you’d have to pay from your savings, credit card, or another loan. For many people, the peace of mind is worth the premium.

Think of it like health insurance: you hope you never need it, but you’re glad it’s there if something goes wrong. GAP insurance is the same—it’s protection against a worst-case scenario that could otherwise derail your finances.

Alternatives to Toyota GAP Insurance

While Toyota’s GAP insurance is convenient, it’s not your only option. You might be able to find cheaper or more flexible coverage elsewhere.

Lender-Offered GAP Insurance

Some banks and credit unions offer their own GAP insurance programs. These may be less expensive than Toyota’s, especially if you’re financing through a third-party lender. However, they may not integrate as smoothly with your auto policy or offer the same level of customer service.

Standalone GAP Policies

Companies like Endurance, Protect My Car, and others sell standalone GAP insurance that can be used with any vehicle, regardless of financing source. These plans often offer more customization, such as higher coverage limits or additional benefits like tire protection.

However, standalone policies may require you to file claims independently and could have longer processing times. They also typically need to be purchased within a short window after buying the car.

Credit Card GAP Coverage

Some premium credit cards offer GAP protection as a benefit when you use the card to purchase your vehicle. For example, certain Visa or Mastercard offerings include GAP coverage for up to 12 months. This can be a cost-effective option if you pay for your car (or a large portion of it) with a qualifying card.

But be cautious: these benefits often have limits, exclusions, and strict requirements. Read the fine print carefully.

Comparing Your Options

When deciding between Toyota GAP and alternatives, consider:

– **Cost**: Which option is cheaper over the life of the loan?

– **Coverage**: Does it cover the full gap, including deductibles?

– **Ease of Use**: How simple is the claims process?

– **Flexibility**: Can you cancel or transfer the policy?

In many cases, Toyota’s GAP insurance offers the best balance of convenience, reliability, and integration—especially if you’re already financing through TFS.

Real-Life Example: How GAP Insurance Saved a Toyota Owner

Let’s look at a real-world scenario to see how GAP insurance works in practice.

Sarah bought a 2023 Toyota Sienna minivan for $45,000 with a $3,000 down payment and a 72-month loan. She financed $42,000 and added Toyota GAP insurance for $900, rolled into her monthly payment.

Two years later, Sarah was involved in a serious accident. The Sienna was declared a total loss. Her auto insurance company assessed the actual cash value at $28,000 and paid out that amount, minus her $500 deductible.

At the time of the accident, Sarah still owed $35,000 on her loan. Without GAP insurance, she would have been responsible for the $7,500 difference ($35,000 – $28,000 + $500 deductible).

But because she had Toyota GAP insurance, the $7,500 was covered. Her loan was paid off in full, and she walked away with no debt. She used the $28,000 insurance payout toward a new vehicle.

In this case, Sarah paid $900 for GAP insurance and avoided a $7,500 financial hit. That’s a net benefit of $6,600—proof that GAP insurance can be a lifesaver.

Tips for Buying GAP Insurance Through Toyota

If you’re considering GAP insurance, here are some practical tips to get the most value:

Ask Early in the Process

Don’t wait until the last minute. Bring up GAP insurance when you’re discussing financing options with your dealer or TFS representative. This gives you time to compare costs and understand the terms.

Compare Quotes

Even if you’re set on Toyota’s program, ask for a written quote. Then, check with your bank or credit union to see if they offer a cheaper alternative. Sometimes the difference is significant.

Read the Fine Print

Make sure you understand what’s covered and what’s not. For example, some GAP policies only cover the loan balance, while others also waive deductibles or cover lease-end fees.

Consider Your Loan Structure

If you can afford a larger down payment or a shorter loan term, you may reduce your need for GAP insurance. Even $2,000 more down can lower your risk significantly.

Don’t Assume It’s Included

Many buyers think GAP insurance comes automatically with financing. It doesn’t. You have to ask for it. Don’t let the dealer assume you don’t want it—speak up.

Keep Your Auto Insurance Active

GAP insurance only works if you have comprehensive and collision coverage. If your auto policy lapses, your GAP coverage may be voided.

Conclusion

So, how much is GAP insurance through Toyota? On average, between $500 and $1,200—depending on your loan, vehicle, and terms. While it’s an added expense, it can save you thousands if your car is totaled or stolen. For buyers with low down payments, long loan terms, or leased vehicles, it’s often a smart investment.

Toyota’s GAP insurance offers convenience, seamless integration with your financing, and reliable claims processing. It’s not the only option, but for many drivers, it’s the easiest and most trustworthy choice. Just remember: it’s not automatic. You have to ask for it when you’re signing your loan or lease.

At the end of the day, GAP insurance isn’t about the cost—it’s about protection. It’s about knowing that if the worst happens, you won’t be left paying for a car you no longer have. And in today’s world of fast-depreciating vehicles and long-term financing, that peace of mind is priceless.

Frequently Asked Questions

How much does GAP insurance cost through Toyota?

GAP insurance through Toyota typically costs between $500 and $1,200, depending on your loan amount, vehicle type, and financing term. The cost is often rolled into your monthly payment.

Is GAP insurance required when buying a Toyota?

No, GAP insurance is not required, but it’s highly recommended—especially if you have a low down payment, long loan term, or are leasing. Some lease agreements may require it.

Can I buy GAP insurance after purchasing my Toyota?

Generally, no. Toyota GAP insurance must be purchased at the time of financing. Retroactive purchases are not allowed, so be sure to ask when signing your loan or lease.

Does GAP insurance cover my deductible?

Some Toyota GAP plans include a deductible waiver, meaning they’ll cover your auto insurance deductible in addition to the loan gap. Check your policy details to confirm.

What happens if I pay off my loan early?

If you pay off your loan early, you may be eligible for a partial refund of your GAP insurance premium, depending on the terms. Contact Toyota Financial Services to inquire about cancellation and refunds.

Can I transfer GAP insurance if I sell my Toyota?

No, GAP insurance is tied to the original loan and cannot be transferred to a new owner. The coverage ends when the loan is paid off or the vehicle is sold.