How to Renew Car Insurance

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How to Renew Car Insurance: A Complete Guide

- 4 Why Renewing Car Insurance Matters

- 5 When to Start the Renewal Process

- 6 Step-by-Step Guide to Renewing Your Car Insurance

- 7 Tips for Saving Money When You Renew

- 8 Common Mistakes to Avoid

- 9 Conclusion

- 10 Frequently Asked Questions

Renewing your car insurance doesn’t have to be stressful or confusing. With a little preparation and the right approach, you can keep your coverage active, save money, and even improve your policy. This guide walks you through every step—from reviewing your current plan to choosing the best renewal option—so you can drive with confidence.

Key Takeaways

- Start early: Begin the renewal process at least 30 days before your policy expires to avoid lapses and compare options.

- Review your coverage: Assess whether your current policy still meets your needs—especially after life changes like moving or buying a new car.

- Compare quotes: Get at least three quotes from different insurers to ensure you’re getting the best rate and value.

- Check for discounts: Ask about safe driver, multi-policy, low-mileage, and other discounts that could lower your premium.

- Understand renewal terms: Know whether your policy auto-renews or requires manual action to avoid unexpected changes.

- Keep documentation: Save confirmation emails, policy documents, and payment receipts for your records.

- Act promptly: Complete renewal before the expiration date to maintain continuous coverage and avoid penalties.

📑 Table of Contents

How to Renew Car Insurance: A Complete Guide

Let’s face it—car insurance isn’t the most exciting topic. But it’s one of those things you simply can’t ignore. Whether you’re a new driver or a seasoned road warrior, renewing your car insurance is a necessary task that comes around every 6 to 12 months. And while it might seem like a routine chore, doing it right can save you hundreds of dollars and give you peace of mind.

The good news? Renewing your car insurance doesn’t have to be complicated. With a little planning and the right information, you can breeze through the process—and maybe even end up with better coverage at a lower price. In this guide, we’ll walk you through everything you need to know about how to renew car insurance, from understanding your renewal notice to comparing quotes and finalizing your policy. Whether you’re sticking with your current insurer or shopping around, we’ve got you covered.

Why Renewing Car Insurance Matters

First things first—why does renewing your car insurance even matter? After all, isn’t it just a formality? Not quite. Letting your policy lapse, even for a day, can have serious consequences. In most states, driving without insurance is illegal and can result in fines, license suspension, or even vehicle impoundment. Plus, a lapse in coverage can lead to higher premiums when you do reinstate your policy, as insurers may see you as a higher-risk driver.

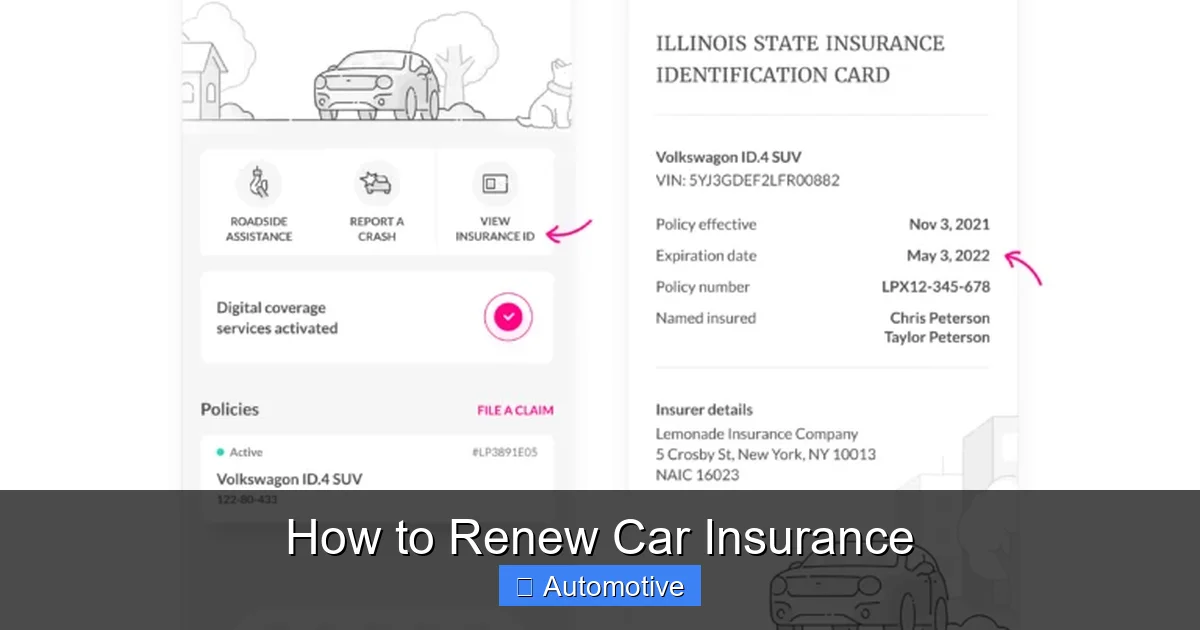

Visual guide about How to Renew Car Insurance

Image source: lemonade.com

Beyond the legal and financial risks, renewing your policy ensures you’re protected in case of an accident, theft, or natural disaster. Imagine getting into a fender bender and realizing your insurance expired last week—yikes! Renewing on time keeps your protection active and your mind at ease.

The Risks of Letting Your Policy Lapse

Even a short gap in coverage can trigger what’s called a “lapse penalty.” Insurers often charge higher rates to drivers who’ve had a break in coverage, regardless of the reason. This is because they assume you’ve been driving uninsured, which increases their risk. In some cases, you might even be forced to purchase high-risk or non-standard insurance, which comes with much steeper premiums.

Another risk? If you’re financing or leasing your car, your lender likely requires you to maintain full coverage. Letting your policy expire could violate your loan agreement, potentially leading to repossession. So, renewing isn’t just about staying legal—it’s about protecting your investment and maintaining financial stability.

Benefits of Timely Renewal

On the flip side, renewing your car insurance on time comes with several perks. For one, you maintain continuous coverage, which can help keep your premiums lower over time. Many insurers offer “loyalty discounts” or “continuous coverage discounts” to customers who renew without gaps.

Renewing also gives you a chance to reassess your needs. Maybe you’ve moved to a safer neighborhood, installed anti-theft devices, or started working from home—all of which could qualify you for discounts. Or perhaps you’ve had a clean driving record for years and deserve a lower rate. Renewal time is the perfect opportunity to make adjustments and optimize your policy.

When to Start the Renewal Process

Timing is everything when it comes to renewing your car insurance. Ideally, you should start the process at least 30 days before your policy expires. This gives you enough time to review your current coverage, shop around for better deals, and avoid last-minute stress.

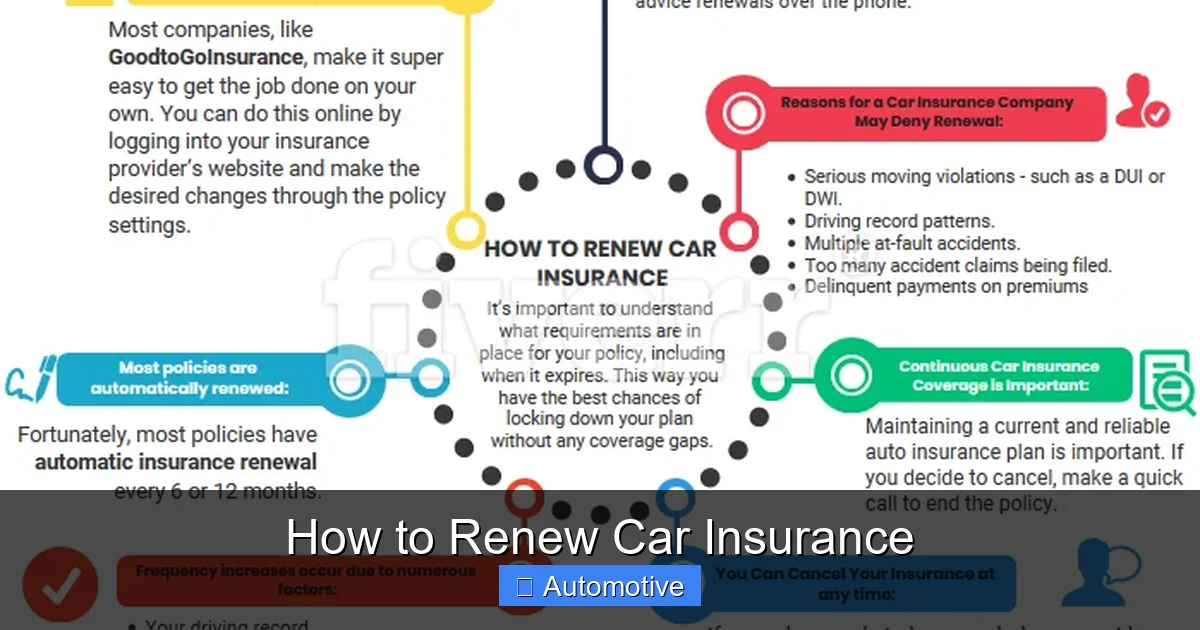

Visual guide about How to Renew Car Insurance

Image source: goodtogoinsurance.org

Most insurers send a renewal notice 30 to 60 days before your policy ends. This notice will include your renewal premium, coverage details, and instructions on how to proceed. Don’t ignore it! Even if you plan to stick with your current insurer, it’s smart to read the fine print. Sometimes, premiums increase at renewal without much explanation, and you might find a better deal elsewhere.

Signs It’s Time to Renew

How do you know when it’s time to renew? Here are a few telltale signs:

- You receive a renewal notice in the mail or via email.

- Your insurer sends a text or app notification about your upcoming expiration.

- You notice your policy end date approaching on your insurance ID card.

- Your bank or lender reminds you about maintaining coverage.

If you’re unsure when your policy expires, check your insurance card, log into your insurer’s website, or call customer service. It’s always better to be proactive than to wake up one morning to a canceled policy.

What Happens If You Miss the Deadline?

Life gets busy, and sometimes deadlines slip through the cracks. If you miss your renewal date, don’t panic—but act fast. Many insurers offer a grace period, usually 7 to 15 days, during which you can renew without losing coverage. However, this varies by company and state, so check your policy terms.

If your policy lapses, you’ll need to contact your insurer immediately to reinstate it. Be prepared for possible fees or a temporary increase in premiums. In some cases, you may need to file an SR-22 form (a certificate of financial responsibility) to prove you’re now insured, especially if you were caught driving uninsured.

Step-by-Step Guide to Renewing Your Car Insurance

Now that you understand why and when to renew, let’s dive into the actual process. Renewing your car insurance can be broken down into five simple steps. Follow them in order, and you’ll be back on the road with valid coverage in no time.

Visual guide about How to Renew Car Insurance

Image source: goodtogoinsurance.org

Step 1: Review Your Current Policy

Before you do anything else, take a close look at your current policy. Pull out your renewal notice or log into your insurer’s portal to review the details. Ask yourself:

- Are my coverage limits still adequate?

- Do I still need comprehensive and collision coverage?

- Has my deductible changed?

- Are there any new fees or surcharges?

For example, if you’ve paid off your car loan, you might no longer need collision coverage. Or if you’ve started driving more for work, you may need higher liability limits. This is also a good time to check for any errors—like an incorrect address or vehicle information—that could affect your premium.

Step 2: Assess Your Needs

Your life changes, and so should your insurance. Think about any major events since your last renewal:

- Did you move to a new city or state?

- Did you buy a new car or sell your old one?

- Did you get married, divorced, or add a teen driver to your policy?

- Did you install safety features like anti-lock brakes or a dashcam?

Each of these factors can impact your coverage needs and premium. For instance, moving to a rural area with lower traffic might qualify you for a lower rate, while adding a young driver could increase your costs. Be honest with yourself about what you need—don’t over-insure, but don’t under-insure either.

Step 3: Compare Quotes from Other Insurers

Even if you love your current insurer, it’s worth shopping around. Insurance rates vary widely between companies, and you could save hundreds by switching. Use online comparison tools or contact insurers directly to get quotes.

When comparing quotes, make sure you’re comparing apples to apples. Look at the same coverage types, limits, and deductibles. Don’t just focus on price—consider customer service ratings, claims process ease, and available discounts.

For example, let’s say your current policy costs $1,200 per year. You might find a similar policy from another company for $950. That’s $250 in savings—just for spending an hour comparing options!

Step 4: Check for Discounts

Don’t forget to ask about discounts! Many insurers offer a variety of ways to lower your premium. Common discounts include:

- Safe driver discount: For maintaining a clean record.

- Multi-policy discount: For bundling auto and home insurance.

- Low-mileage discount: For driving fewer than a certain number of miles per year.

- Good student discount: For students with high grades.

- Defensive driving course discount: For completing an approved course.

- Anti-theft device discount: For vehicles with alarms or tracking systems.

Some discounts are automatic, while others require you to request them. When you contact your insurer or a new company, ask specifically: “What discounts am I eligible for?” You might be surprised by how much you can save.

Step 5: Finalize Your Renewal

Once you’ve reviewed your policy, assessed your needs, compared quotes, and checked for discounts, it’s time to make a decision. If you’re staying with your current insurer, follow their renewal instructions—usually online, by phone, or through their app.

If you’re switching insurers, make sure your new policy starts before your old one ends. Provide your new insurer with your current policy details so they can coordinate the transition. You’ll typically receive a new insurance card and policy documents within a few days.

Finally, confirm that your renewal is complete. Check your email for a confirmation message, and verify that your payment has been processed. Keep a copy of your new policy for your records.

Tips for Saving Money When You Renew

Renewing your car insurance is a great opportunity to cut costs. Here are some proven strategies to keep more money in your pocket:

Raise Your Deductible

Your deductible is the amount you pay out of pocket before insurance kicks in. Raising it from $500 to $1,000 can lower your premium by 10% to 25%. Just make sure you can afford the higher deductible if you ever need to file a claim.

Maintain a Good Driving Record

Safe driving pays off—literally. Most insurers offer discounts for drivers with no accidents or violations in the past three to five years. Avoid speeding tickets, DUIs, and at-fault accidents to keep your rates low.

Bundle Your Policies

If you have home, renters, or life insurance, consider bundling them with your auto policy. Many insurers offer significant discounts for multiple policies—sometimes up to 20% off.

Pay Annually or Semi-Annually

Some insurers charge fees for monthly payments. Paying your premium in full once or twice a year can save you money on processing fees.

Take Advantage of Telematics Programs

Many insurers now offer usage-based insurance programs that track your driving habits through a mobile app or device. If you drive safely and infrequently, you could earn discounts of 10% to 30%.

Common Mistakes to Avoid

Even experienced drivers can make mistakes during the renewal process. Here are a few pitfalls to watch out for:

Auto-Renewal Without Review

Many policies auto-renew unless you cancel them. While convenient, this can lead to higher premiums or outdated coverage. Always review your renewal notice and consider your options.

Ignoring Small Print Changes

Insurers sometimes change terms, exclusions, or fees at renewal. Read the fine print to avoid surprises. If something doesn’t make sense, ask for clarification.

Not Updating Personal Information

Failing to update your address, vehicle details, or driving habits can result in incorrect premiums or denied claims. Keep your insurer informed of any changes.

Choosing the Cheapest Policy Without Considering Coverage

The lowest price isn’t always the best value. A cheap policy might have high deductibles, low limits, or poor customer service. Focus on getting the right coverage at a fair price.

Conclusion

Renewing your car insurance might not be the most thrilling task on your to-do list, but it’s one of the most important. By starting early, reviewing your coverage, comparing quotes, and taking advantage of discounts, you can keep your policy active, save money, and ensure you’re properly protected on the road.

Remember, insurance isn’t just a legal requirement—it’s a safety net. Whether you’re commuting to work, road-tripping with family, or just running errands, having the right coverage gives you peace of mind. So don’t wait until the last minute. Take control of your renewal process today, and drive with confidence knowing you’re covered.

Frequently Asked Questions

How far in advance should I renew my car insurance?

It’s best to start the renewal process at least 30 days before your policy expires. This gives you time to review your coverage, compare quotes, and avoid lapses in protection.

Can I renew my car insurance online?

Yes, most insurers allow you to renew online through their website or mobile app. You can also renew by phone or in person at a local office.

What happens if I miss my car insurance renewal date?

If you miss your renewal date, your policy may lapse, leading to fines, higher premiums, or legal issues. Contact your insurer immediately to reinstate coverage, and check if a grace period applies.

Will my premium increase when I renew?

Your premium may increase due to factors like inflation, claims history, or changes in your risk profile. However, you can often reduce costs by shopping around or qualifying for discounts.

Do I need to renew my car insurance if I’m not driving?

If your car is parked and not in use, you may be able to switch to a storage or non-owner policy. However, you still need some form of coverage if the vehicle is registered.

Can I switch insurers when I renew?

Absolutely! You can switch insurers at renewal time. Just make sure your new policy starts before your old one ends to avoid a coverage gap.