Can I Pay More on My Car Loan?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Can I Pay More on My Car Loan?

- 4 Why Paying Extra on Your Car Loan Makes Sense

- 5 How to Pay Extra on Your Car Loan

- 6 When Paying Extra Might Not Be the Best Move

- 7 Real-Life Examples: How Extra Payments Make a Difference

- 8 Tips to Maximize Your Extra Payments

- 9 Can I Pay Off My Car Loan Early?

- 10 Should You Refinance After Paying Extra?

- 11 Final Thoughts: Is Paying Extra Right for You?

- 12 Frequently Asked Questions

Yes, you can pay more on your car loan—and it’s a smart financial move. Making extra payments reduces your principal balance, cuts interest costs, and helps you own your car outright sooner. With the right strategy, even small extra payments can make a big difference over time.

Key Takeaways

- You can pay more on your car loan: Most lenders allow extra payments without penalties, but always check your loan agreement first.

- Extra payments reduce interest: Paying down the principal early means less interest accrues over the life of the loan.

- Shorter loan term = faster ownership: Additional payments can shorten your repayment timeline significantly, sometimes by years.

- Specify where the extra money goes: Tell your lender to apply extra payments to the principal, not future interest.

- Automate for consistency: Set up automatic extra payments to build a habit and stay on track.

- Consider refinancing later: Once you’ve reduced your balance, refinancing to a lower rate may save even more.

- Balance with other financial goals: While paying off your car loan faster is great, don’t neglect high-interest debt or emergency savings.

📑 Table of Contents

- Can I Pay More on My Car Loan?

- Why Paying Extra on Your Car Loan Makes Sense

- How to Pay Extra on Your Car Loan

- When Paying Extra Might Not Be the Best Move

- Real-Life Examples: How Extra Payments Make a Difference

- Tips to Maximize Your Extra Payments

- Can I Pay Off My Car Loan Early?

- Should You Refinance After Paying Extra?

- Final Thoughts: Is Paying Extra Right for You?

Can I Pay More on My Car Loan?

If you’ve ever looked at your monthly car payment and thought, “I could pay a little more,” you’re not alone. Many car owners wonder whether they can—and should—pay extra on their auto loan. The short answer? Absolutely. In fact, paying more than your required monthly amount is one of the smartest financial moves you can make when it comes to car loans.

Car loans are typically amortizing loans, meaning each payment covers both interest and a portion of the principal (the original amount borrowed). Early in the loan term, a larger chunk of your payment goes toward interest, while the principal shrinks slowly. But as time goes on, more of your payment chips away at the principal. By paying extra, you jumpstart this process, reducing the principal faster and cutting down the total interest you’ll pay over the life of the loan.

But before you start writing bigger checks or adjusting your auto-pay settings, it’s important to understand how extra payments work, what to watch out for, and how to make the most of this strategy. This guide will walk you through everything you need to know—from the benefits of paying extra to practical tips for doing it right.

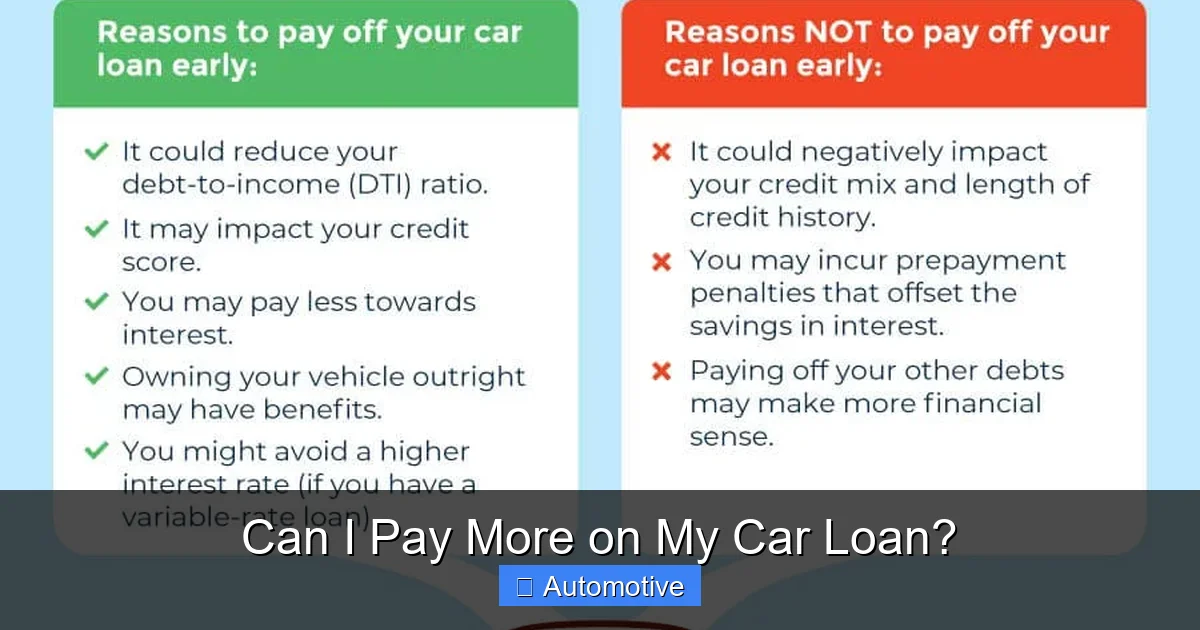

Why Paying Extra on Your Car Loan Makes Sense

Visual guide about Can I Pay More on My Car Loan?

Image source: images.ctfassets.net

Let’s be honest: car loans aren’t the most exciting part of car ownership. But they’re a necessary reality for most people. The average auto loan in the U.S. is around $40,000 for a new car and $28,000 for a used one, with terms ranging from 60 to 84 months. That’s a long time to be making payments—and a lot of interest to pay.

Paying extra on your car loan helps you break free from that financial commitment sooner. Here’s why it’s worth considering:

You Save on Interest

Interest is the cost of borrowing money, and it adds up fast. For example, let’s say you take out a $30,000 car loan at 5% interest over 6 years (72 months). Your monthly payment would be about $483. Over the life of the loan, you’d pay roughly $4,776 in interest.

Now, imagine you pay an extra $50 each month. That brings your monthly payment to $533. With that small change, you’d pay off the loan in about 60 months instead of 72—and save over $800 in interest. That’s a significant chunk of change, all from an extra $50 a month.

The reason this works is simple: every extra dollar you pay reduces the principal balance. Since interest is calculated on the remaining principal, a lower balance means less interest accrues each month. Over time, this snowballs into major savings.

You Own Your Car Sooner

One of the biggest perks of paying extra is that you’ll own your car outright much faster. Instead of making payments for six or seven years, you could be debt-free in four or five. That means more financial freedom and less stress about monthly obligations.

Plus, owning your car free and clear gives you more flexibility. You can sell it, trade it in, or keep it without worrying about being “upside down” on the loan (owing more than the car is worth). This is especially helpful if you plan to upgrade to a new vehicle in the future.

You Build Equity Faster

When you finance a car, it depreciates quickly—often losing 20% of its value the moment you drive it off the lot. If you’re only making minimum payments, you might find yourself owing more than the car is worth for a while. This is called being “underwater” or “upside down” on your loan.

Paying extra helps you build equity in your vehicle faster. Equity is the difference between what you owe and what the car is worth. The more equity you have, the less risky it is to keep the car long-term or sell it if needed.

It’s a Low-Risk Way to Invest

Think of paying extra on your car loan as a form of investment. The “return” you get is the interest you avoid paying. For example, if your loan has a 5% interest rate, every extra dollar you pay toward the principal effectively earns you a 5% return—guaranteed.

Compare that to putting money in a savings account, which might earn 0.5% or less. Or investing in the stock market, which comes with risk. Paying down debt is a safe, predictable way to improve your financial health.

How to Pay Extra on Your Car Loan

Visual guide about Can I Pay More on My Car Loan?

Image source: clicktodrive.ca

Now that you know why paying extra is beneficial, let’s talk about how to do it the right way. It’s not just about sending more money—it’s about making sure that money works as hard as possible for you.

Check Your Loan Agreement

Before you start paying extra, review your loan agreement. Most auto loans allow prepayments without penalties, but some lenders charge a prepayment penalty if you pay off the loan too early. These penalties are rare these days, but it’s always better to be safe than sorry.

Look for terms like “prepayment penalty,” “early payoff fee,” or “deferred interest.” If you see any of these, call your lender to clarify. In most cases, you’ll be fine, but it’s worth confirming.

Specify That Extra Payments Go to Principal

This is crucial. When you make an extra payment, you must tell your lender to apply it to the principal balance, not future interest.

Here’s why: if you just send extra money without instructions, some lenders may hold it as a “prepayment” and apply it to future payments. That means you’re still paying interest on the full balance, even though you’ve sent extra cash.

To avoid this, always include a note with your payment (or use your lender’s online portal) specifying that the extra amount should go toward the principal. For example, write: “Please apply $50 of this payment to the principal balance.”

Most online loan management systems have a field where you can indicate this. If you’re mailing a check, write it in the memo line.

Make Extra Payments Regularly

Consistency is key. One large extra payment is helpful, but regular smaller payments have a bigger long-term impact.

For example, paying an extra $25 every month is better than paying $300 once a year. Why? Because the $25 reduces your principal each month, which lowers the interest charged the following month. Over time, this compounding effect adds up.

Try to make extra payments part of your budget. Even $10 or $20 a month can make a difference. Set a goal—like paying an extra $50 per month—and stick to it.

Use Windfalls Wisely

Got a tax refund, bonus, or birthday cash? Consider putting it toward your car loan.

Lump-sum payments can dramatically reduce your balance and shorten your loan term. For instance, a $1,000 extra payment on a $25,000 loan could save you hundreds in interest and cut months off your repayment period.

Just remember to specify that the extra amount goes to the principal.

Automate Your Extra Payments

If you struggle to stay consistent, set up automatic extra payments through your lender’s website.

Many lenders allow you to schedule recurring payments in addition to your regular monthly payment. You can choose the amount and frequency—weekly, biweekly, or monthly.

Automation takes the guesswork out of paying extra and helps you build a habit. Plus, it ensures you don’t forget or skip a payment when life gets busy.

When Paying Extra Might Not Be the Best Move

Visual guide about Can I Pay More on My Car Loan?

Image source: images.ctfassets.net

While paying extra on your car loan is usually a smart idea, it’s not always the best choice for everyone. Here are a few situations where you might want to think twice:

You Have High-Interest Debt

If you’re carrying credit card debt with interest rates of 18% or higher, it usually makes more sense to pay that off first. The interest on credit cards is typically much higher than on car loans, so eliminating that debt gives you a better return on your money.

For example, paying $100 extra on a 20% credit card saves you $20 in interest over a year. Paying $100 extra on a 5% car loan saves you $5. The math is clear: tackle the highest-interest debt first.

You Don’t Have an Emergency Fund

Before aggressively paying down your car loan, make sure you have a solid emergency fund. Experts recommend saving three to six months’ worth of living expenses in a savings account.

If you don’t have this cushion, an unexpected expense—like a medical bill or car repair—could force you to rely on credit cards or loans, which could put you in a worse financial position.

So, if you’re choosing between building your emergency fund and paying extra on your car loan, prioritize the fund. Once it’s fully funded, you can shift focus to your car loan.

Your Car Loan Has a Very Low Interest Rate

If your car loan has an interest rate below 3% or 4%, the benefit of paying it off early is smaller. In this case, you might get a better return by investing the extra money in a retirement account or index fund.

For example, if your car loan is at 3% and the stock market averages 7% annual returns, investing could grow your wealth faster than paying off the loan early.

That said, some people prefer the peace of mind that comes with being debt-free, even if the financial return is lower. It’s a personal choice.

You’re Planning to Sell the Car Soon

If you’re planning to sell or trade in your car within the next year or two, paying extra might not be worth it. You’ll still owe money when you sell, and the extra payments won’t significantly reduce your balance in such a short time.

Instead, focus on maintaining the car’s value and saving for your next vehicle.

Real-Life Examples: How Extra Payments Make a Difference

Let’s look at a few real-world scenarios to see how paying extra can impact your loan.

Example 1: The $35,000 Loan at 6% Over 72 Months

– Loan amount: $35,000

– Interest rate: 6%

– Term: 6 years (72 months)

– Monthly payment: $581

– Total interest: $6,832

Now, let’s say you pay an extra $75 per month:

– New monthly payment: $656

– Payoff time: ~58 months (about 4.8 years)

– Total interest: $5,456

– Savings: $1,376 and 14 months off the loan

That’s a big win for just $75 extra per month.

Example 2: The $20,000 Loan at 4.5% Over 60 Months

– Loan amount: $20,000

– Interest rate: 4.5%

– Term: 5 years (60 months)

– Monthly payment: $373

– Total interest: $2,380

Add $50 extra per month:

– New monthly payment: $423

– Payoff time: ~52 months

– Total interest: $2,016

– Savings: $364 and 8 months off the loan

Even on a smaller loan, the savings add up.

Example 3: One-Time $2,000 Extra Payment

Let’s go back to the $35,000 loan at 6%. If you make one $2,000 extra payment in month 12:

– Payoff time: reduced by 8 months

– Total interest saved: ~$850

A single lump sum can still make a meaningful difference.

These examples show that whether you pay a little extra each month or make occasional lump sums, the impact is real.

Tips to Maximize Your Extra Payments

Ready to start paying more on your car loan? Here are some practical tips to get the most out of your efforts:

Round Up Your Payments

Instead of paying $483.27, round up to $500. That extra $16.73 might not seem like much, but over 60 months, it adds up to over $1,000 in extra payments.

Pay Biweekly Instead of Monthly

Instead of one monthly payment, split it in half and pay every two weeks. This results in 26 half-payments per year, which equals 13 full payments instead of 12.

That extra payment each year goes straight toward your principal and can shave months off your loan.

Use a Budgeting App

Apps like Mint, YNAB (You Need A Budget), or EveryDollar can help you track your car loan and plan extra payments. You can set goals, monitor progress, and see how much interest you’re saving.

Track Your Progress

Keep a simple spreadsheet or use your lender’s online portal to track your balance over time. Seeing your loan shrink can be incredibly motivating.

Reassess Annually

Review your loan once a year. If your income has increased or expenses have decreased, consider increasing your extra payment amount.

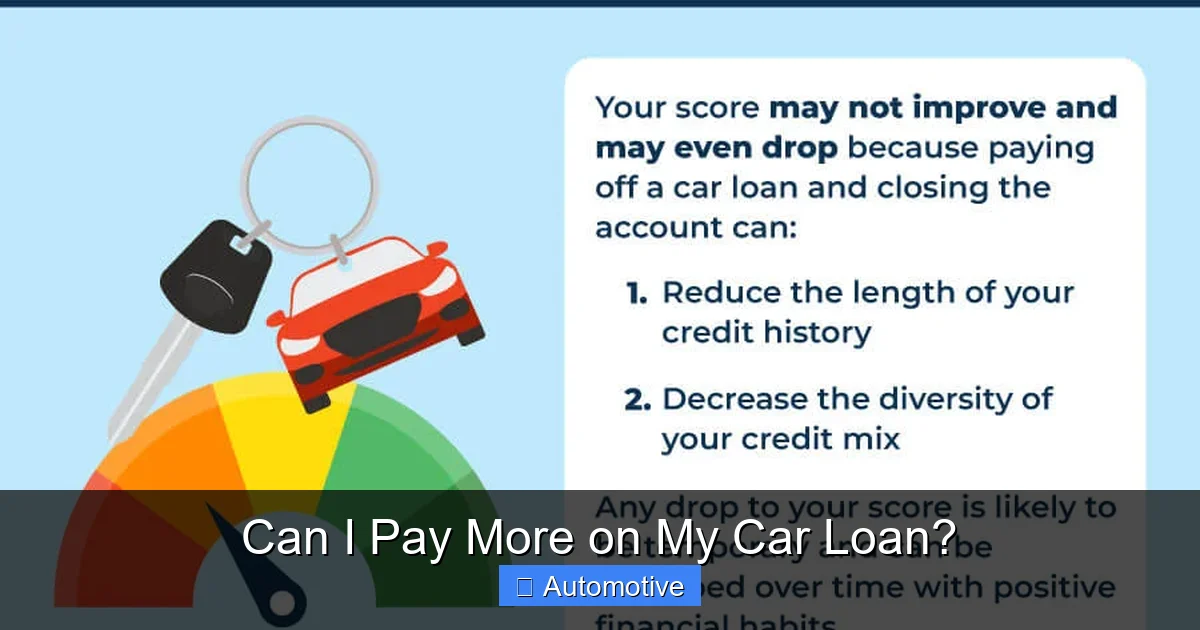

Can I Pay Off My Car Loan Early?

Yes—and many people do. Paying off your car loan early is the ultimate goal of making extra payments.

To pay off your loan early, continue making extra payments until the balance reaches zero. You can also make a large lump-sum payment if you come into money.

Once the loan is paid off, your lender will send you a payoff statement and release the lien on your car. You’ll receive the title (or it will be updated), and the car will be fully in your name.

Just make sure to contact your lender to confirm the exact payoff amount, which may include a small per-diem interest charge for the days between your last payment and the payoff date.

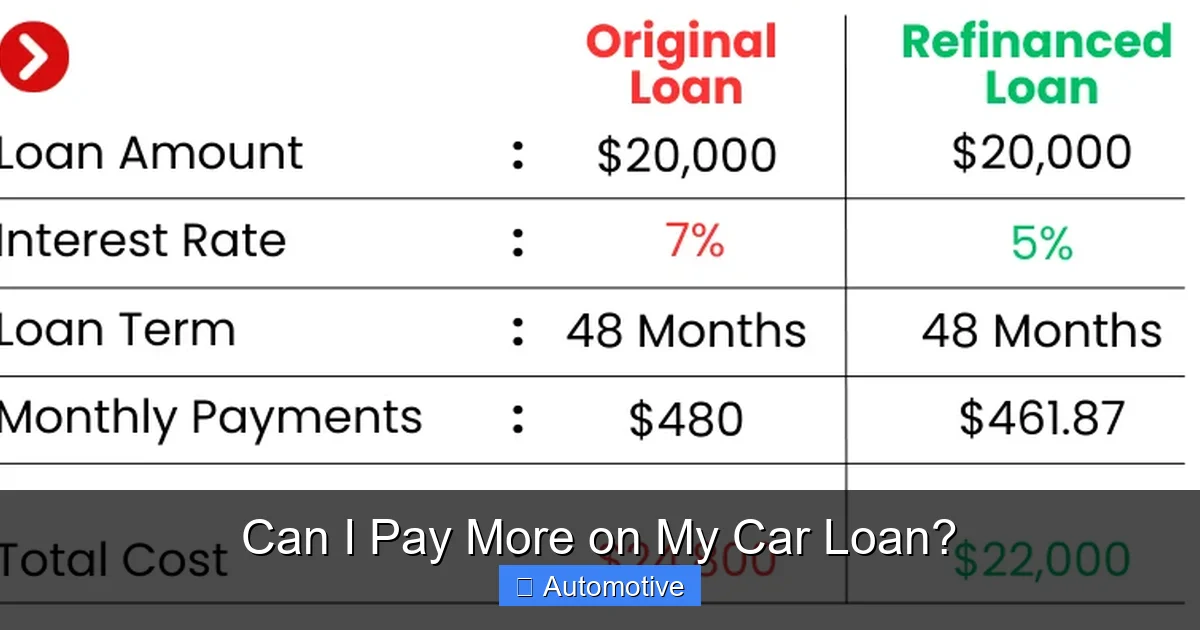

Should You Refinance After Paying Extra?

After making extra payments, you might qualify for a better interest rate if you refinance.

For example, if you started with a 7% loan and have since improved your credit score or reduced your loan-to-value ratio, you might now qualify for a 4% or 5% rate.

Refinancing could lower your monthly payment or shorten your term even further. Just be aware of any fees involved, such as origination fees or title transfer costs.

Use a refinance calculator to compare your current loan with potential new offers.

Final Thoughts: Is Paying Extra Right for You?

Paying more on your car loan is a powerful tool for saving money, building equity, and gaining financial freedom. For most people, it’s a smart move—especially if your loan has a moderate to high interest rate.

But it’s not a one-size-fits-all solution. Consider your overall financial picture: Do you have high-interest debt? An emergency fund? Other financial goals?

If the answer is yes to those, you might want to prioritize them first. But if your car loan is your biggest debt and you’re in a stable financial position, paying extra can make a big difference.

Start small if you need to. Even $10 or $20 extra per month can reduce your interest and shorten your loan term. The key is consistency and making sure your extra payments go toward the principal.

With a little planning and discipline, you can pay off your car loan faster, save hundreds (or thousands) in interest, and enjoy the peace of mind that comes with owning your car outright.

Frequently Asked Questions

Can I pay more on my car loan without penalties?

Yes, most car loans allow you to pay extra without penalties. However, always check your loan agreement to confirm there are no prepayment penalties.

Will paying extra reduce my monthly payment?

No, paying extra won’t lower your required monthly payment. Instead, it reduces the principal balance and shortens the loan term, helping you pay off the loan faster.

How do I make sure extra payments go to the principal?

When making an extra payment, specify in writing or through your lender’s online portal that the amount should be applied to the principal, not future interest.

Can I pay off my car loan early?

Yes, you can pay off your car loan early by making extra payments or a lump-sum payment. Contact your lender for the exact payoff amount.

Is it better to pay extra on my car loan or save the money?

It depends on your interest rate and financial goals. If your car loan has a high interest rate, paying extra saves more than most savings accounts earn. But prioritize high-interest debt and emergency savings first.

What happens when I pay off my car loan early?

Once paid off, your lender will release the lien on your car and send you the title. You’ll own the vehicle outright and no longer have monthly payments.