How Much Is Car Insurance in Hawaii?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance in Hawaii? A Complete Guide

- 4 Average Car Insurance Costs in Hawaii

- 5 Factors That Affect Car Insurance Rates in Hawaii

- 6 Hawaii’s No-Fault Insurance System Explained

- 7 Required Car Insurance Coverage in Hawaii

- 8 How to Save Money on Car Insurance in Hawaii

- 9 Top Car Insurance Companies in Hawaii

- 10 Final Thoughts: Is Car Insurance Expensive in Hawaii?

- 11 Frequently Asked Questions

Car insurance in Hawaii costs an average of $1,400 to $1,800 per year for full coverage, which is slightly below the national average. Rates vary based on location, driving record, vehicle type, and coverage choices, but Hawaii’s no-fault insurance system and low accident rates help keep premiums manageable.

Key Takeaways

- Average annual cost: Full coverage car insurance in Hawaii typically ranges from $1,400 to $1,800, while minimum liability coverage costs around $500 to $700 per year.

- No-fault insurance system: Hawaii operates under a no-fault insurance model, meaning your own insurer covers medical expenses after an accident, regardless of who caused it.

- State-mandated coverage: All drivers must carry at least $10,000 in personal injury protection (PIP), $10,000 in property damage liability, and $20,000/$40,000 in bodily injury liability.

- Factors affecting rates: Age, driving history, credit score (in most cases), vehicle type, and location (urban vs. rural) all influence your premium.

- Discounts available: Safe driver, multi-car, good student, and anti-theft device discounts can significantly lower your monthly payments.

- Shopping around pays off: Comparing quotes from at least three insurers can save you hundreds of dollars annually.

- Electric and hybrid vehicles may cost less: Some insurers offer green vehicle discounts, and lower repair costs can reduce premiums.

📑 Table of Contents

- How Much Is Car Insurance in Hawaii? A Complete Guide

- Average Car Insurance Costs in Hawaii

- Factors That Affect Car Insurance Rates in Hawaii

- Hawaii’s No-Fault Insurance System Explained

- Required Car Insurance Coverage in Hawaii

- How to Save Money on Car Insurance in Hawaii

- Top Car Insurance Companies in Hawaii

- Final Thoughts: Is Car Insurance Expensive in Hawaii?

How Much Is Car Insurance in Hawaii? A Complete Guide

If you’re living in or moving to Hawaii, one of the first things you’ll need to figure out is how much car insurance will cost. Whether you’re cruising down the scenic roads of Maui, navigating Honolulu traffic, or exploring the quiet towns of the Big Island, having the right auto insurance is not just a legal requirement—it’s a smart financial move.

Hawaii is known for its stunning beaches, tropical climate, and laid-back lifestyle, but when it comes to car insurance, the state has some unique rules and cost structures. Unlike many other states, Hawaii uses a no-fault insurance system, which affects how claims are handled and what coverage you’re required to carry. This system, combined with the state’s relatively low population density and fewer major highways, helps keep insurance costs lower than in many mainland states.

But don’t let the island charm fool you—car insurance in Hawaii isn’t free, and prices can vary widely depending on where you live, what you drive, and your personal driving history. In this guide, we’ll break down everything you need to know about car insurance costs in Hawaii, from average premiums to factors that influence your rate, and tips to help you save money without sacrificing protection.

Average Car Insurance Costs in Hawaii

Visual guide about How Much Is Car Insurance in Hawaii?

Image source: thegeneral.com

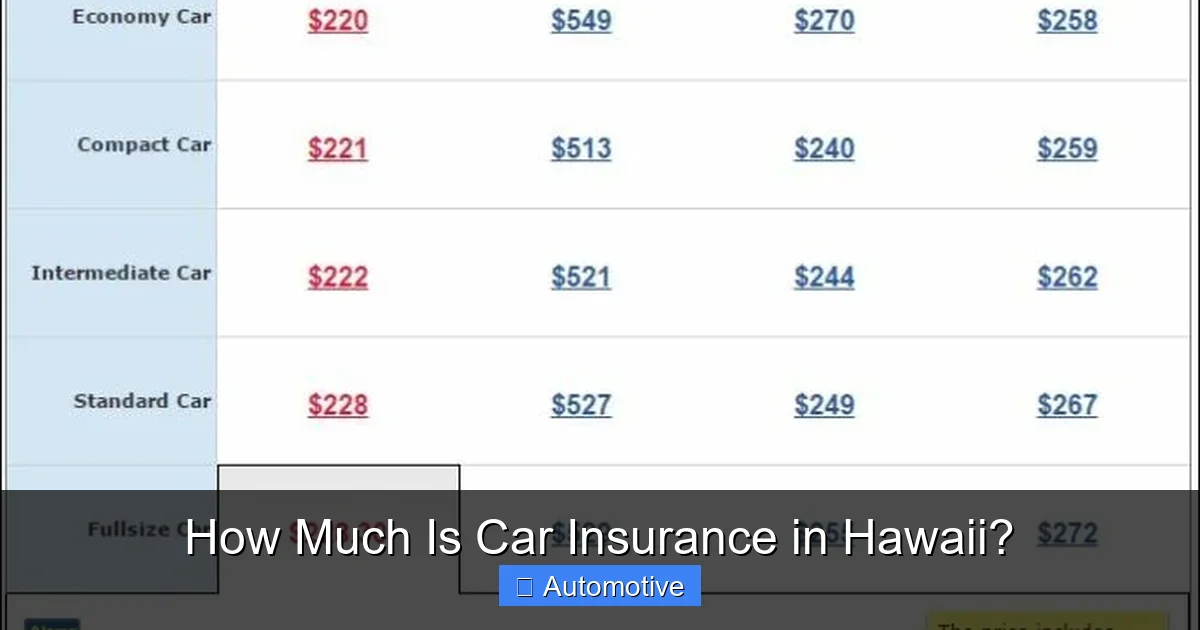

So, how much is car insurance in Hawaii, exactly? On average, drivers in the Aloha State pay between $1,400 and $1,800 per year for full coverage auto insurance. That includes liability, collision, comprehensive, and personal injury protection (PIP). For minimum coverage—just the state-required liability and PIP—the average cost drops to around $500 to $700 annually.

To put that in perspective, the national average for full coverage is about $1,700 per year, so Hawaii is actually slightly more affordable than many other states. This is partly due to lower traffic congestion, fewer severe weather events (like snowstorms or tornadoes), and a strong emphasis on safe driving culture.

Let’s look at some real-world examples. A 35-year-old driver with a clean record, driving a 2020 Honda Civic in Honolulu, might pay around $1,500 per year for full coverage. The same driver in a rural area like Kauai or the North Shore of the Big Island could see rates as low as $1,300. On the flip side, a young driver under 25 or someone with a recent accident or ticket might pay closer to $2,200 or more.

It’s also worth noting that Hawaii has one of the lowest rates of uninsured drivers in the country—under 5%—which helps keep overall premiums lower for everyone. When fewer people drive without insurance, the risk pool improves, and insurers can offer more competitive rates.

Minimum vs. Full Coverage: What’s the Difference?

When shopping for car insurance in Hawaii, you’ll quickly notice two main tiers: minimum coverage and full coverage. Understanding the difference is crucial to making the right choice for your needs and budget.

Minimum coverage meets Hawaii’s legal requirements but offers very limited protection. It includes:

– $10,000 in Personal Injury Protection (PIP)

– $10,000 in Property Damage Liability (PDL)

– $20,000 per person / $40,000 per accident in Bodily Injury Liability (BIL)

This coverage pays for medical expenses for you and your passengers (PIP), damage you cause to other people’s property (PDL), and injuries you cause to others in an accident (BIL). However, it does not cover damage to your own vehicle or theft, vandalism, or natural disasters.

Full coverage, on the other hand, includes everything in minimum coverage plus:

– Collision coverage (pays for damage to your car from accidents)

– Comprehensive coverage (covers non-collision events like theft, fire, or falling objects)

For most drivers—especially those with newer or financed vehicles—full coverage is the smarter choice. While it costs more upfront, it provides peace of mind and financial protection in case of a serious accident or unexpected event.

Factors That Affect Car Insurance Rates in Hawaii

Visual guide about How Much Is Car Insurance in Hawaii?

Image source: cdn.wallethub.com

Just like anywhere else, your car insurance premium in Hawaii isn’t set in stone. Several key factors determine how much you’ll pay, and understanding them can help you find ways to lower your costs.

1. Your Driving Record

Your driving history is one of the biggest factors insurers consider. A clean record with no accidents, tickets, or DUIs will earn you the best rates. On the other hand, even a single speeding ticket can increase your premium by 10% to 20%, while an at-fault accident could raise it by 30% or more.

For example, a driver with a recent DUI might pay over $3,000 per year for full coverage in Honolulu, compared to $1,500 for someone with a spotless record. That’s why maintaining safe driving habits isn’t just good for your safety—it’s good for your wallet.

2. Age and Experience

Younger drivers, especially those under 25, typically face higher insurance rates due to their lack of experience and higher accident rates. In Hawaii, a 19-year-old driver might pay nearly double what a 40-year-old with the same car and record would pay.

However, rates tend to stabilize around age 25 and continue to decrease with age and experience. Senior drivers (65+) may see slight increases due to slower reaction times, but many insurers offer mature driver discounts to offset this.

3. Location Within Hawaii

Where you live in Hawaii makes a big difference. Urban areas like Honolulu on Oahu have higher traffic density, more accidents, and greater risk of theft or vandalism, leading to higher premiums. Rural areas like Hana on Maui or Waimea on the Big Island tend to have lower rates due to less congestion and fewer claims.

For instance, a driver in downtown Honolulu might pay $1,700 for full coverage, while someone in a small town on Kauai could pay $1,300 for the same policy. Even within the same island, ZIP code can impact your rate.

4. Vehicle Type and Value

The car you drive directly affects your insurance cost. High-performance vehicles, luxury cars, and models with high repair costs or theft rates will come with higher premiums. Conversely, safe, reliable, and fuel-efficient cars—especially those with advanced safety features—often qualify for discounts.

For example, insuring a 2023 Tesla Model 3 in Hawaii might cost more than a 2020 Toyota Camry due to the Tesla’s higher value and repair costs. However, some insurers offer discounts for electric vehicles (EVs) due to their lower environmental impact and reduced risk of certain types of damage.

5. Credit Score (With Exceptions)

In most states, insurers use credit-based insurance scores to help determine rates. Hawaii allows this practice, but with a major exception: as of 2022, insurers cannot use credit scores to set rates for drivers who are 65 or older. This protects older residents from being penalized for financial history that may not reflect current risk.

For younger drivers, a good credit score (typically 670 or higher) can lead to lower premiums, while poor credit may result in higher costs. Improving your credit over time can gradually reduce your insurance expenses.

6. Coverage Limits and Deductibles

The amount of coverage you choose and your deductible (the amount you pay out of pocket before insurance kicks in) also affect your premium. Higher coverage limits and lower deductibles mean more protection but higher monthly payments.

For example, choosing a $500 deductible instead of $1,000 can increase your premium by $100 to $200 per year. But if you’re in an accident, you’ll save $500 out of pocket. It’s a trade-off between upfront cost and potential savings later.

Hawaii’s No-Fault Insurance System Explained

Visual guide about How Much Is Car Insurance in Hawaii?

Image source: trendingsimple.com

One of the most important things to understand about car insurance in Hawaii is that the state operates under a no-fault system. This means that after an accident, each driver’s own insurance company pays for their medical expenses and lost wages, regardless of who caused the crash.

This system is designed to reduce lawsuits and speed up claim settlements. Instead of waiting months or years to determine fault and recover costs, injured parties can get medical treatment quickly through their Personal Injury Protection (PIP) coverage.

How No-Fault Works in Practice

Let’s say you’re rear-ended by another driver in Honolulu. Even if they’re clearly at fault, your own insurance will cover your medical bills up to your PIP limit ($10,000 minimum). The other driver’s insurance will cover your vehicle damage and any additional medical costs if your injuries exceed your PIP limit.

You can still sue the at-fault driver in Hawaii, but only if your injuries meet certain thresholds—such as significant disfigurement, permanent injury, or medical expenses exceeding $5,000. This threshold helps prevent frivolous lawsuits while still allowing compensation for serious harm.

Benefits and Drawbacks

The no-fault system has pros and cons. On the plus side, it ensures faster access to medical care and reduces legal battles. It also helps keep premiums lower by minimizing costly litigation.

However, some drivers feel limited by the $10,000 PIP cap, especially if they have serious injuries. That’s why many opt to increase their PIP coverage or add optional medical payments (MedPay) coverage for extra protection.

Required Car Insurance Coverage in Hawaii

Hawaii law requires all drivers to carry a minimum amount of auto insurance. Failing to do so can result in fines, license suspension, or even vehicle impoundment.

Here’s what you must have:

- Personal Injury Protection (PIP): $10,000 minimum. Covers medical expenses, lost wages, and other costs for you and your passengers.

- Bodily Injury Liability (BIL): $20,000 per person / $40,000 per accident. Pays for injuries you cause to others.

- Property Damage Liability (PDL): $10,000 minimum. Covers damage you cause to someone else’s property, like their car or fence.

These are the bare minimums. While they meet legal requirements, they may not provide enough protection in a serious accident. For example, $10,000 in PIP might cover a minor fender bender, but it won’t go far in a major collision requiring surgery or long-term care.

That’s why many financial experts recommend increasing your coverage limits. Upgrading to $100,000/$300,000 in bodily injury liability and $50,000 in property damage can offer much better protection—and often costs only $50 to $100 more per year.

Optional Coverage to Consider

Beyond the basics, you may want to add optional coverages for extra peace of mind:

- Collision Coverage: Pays for damage to your car from accidents, regardless of fault.

- Comprehensive Coverage: Covers non-collision events like theft, fire, vandalism, or falling objects (like a coconut from a tree!).

- Uninsured/Underinsured Motorist Coverage: Protects you if you’re hit by a driver with no insurance or insufficient coverage.

- Rental Reimbursement: Pays for a rental car while your vehicle is being repaired after a covered claim.

- Roadside Assistance: Covers towing, jump-starts, and other emergency services.

These add-ons can make a big difference in your overall protection, especially if you rely heavily on your vehicle or live in an area with higher risks.

How to Save Money on Car Insurance in Hawaii

Car insurance doesn’t have to break the bank. With a few smart strategies, you can reduce your premiums without sacrificing coverage.

Shop Around and Compare Quotes

One of the easiest ways to save is by comparing quotes from multiple insurers. Rates can vary significantly between companies, even for the same driver and vehicle. Use online comparison tools or work with an independent agent to get quotes from at least three different providers.

For example, you might find that Geico offers a lower rate for your Honda Accord, while State Farm has a better deal for your teenage driver. Taking the time to compare can save you $200 or more per year.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Common ones in Hawaii include:

- Safe Driver Discount: For maintaining a clean record over several years.

- Multi-Car Discount: When you insure more than one vehicle with the same company.

- Good Student Discount: For full-time students with a B average or higher.

- Anti-Theft Device Discount: For vehicles equipped with alarms or tracking systems.

- Low Mileage Discount: If you drive fewer than 7,500 miles per year.

- Defensive Driving Course Discount: Completing an approved course can reduce your premium.

Be sure to ask your insurer about all available discounts—you might be surprised by how much you qualify for.

Raise Your Deductible

Increasing your deductible from $500 to $1,000 can lower your premium by 10% to 20%. Just make sure you have enough savings to cover the higher out-of-pocket cost if you need to file a claim.

Maintain a Good Credit Score

As mentioned earlier, credit scores affect your rate in Hawaii (except for drivers 65+). Paying bills on time, reducing debt, and monitoring your credit report can help improve your score and lower your insurance costs over time.

Consider Pay-in-Full or Automatic Payments

Some insurers offer discounts if you pay your premium in full rather than monthly. Others give a small discount for setting up automatic payments. These may seem minor, but they add up.

Top Car Insurance Companies in Hawaii

Not all insurers are created equal. Some companies offer better rates, customer service, or coverage options in Hawaii. Based on customer satisfaction, financial strength, and local presence, here are a few top choices:

- State Farm: Known for excellent customer service and a wide range of discounts. Popular among families and young drivers.

- Geico: Offers competitive rates and a user-friendly online experience. Great for tech-savvy drivers.

- Progressive: Known for flexible coverage options and the Name Your Price tool, which helps you find a policy within your budget.

- Liberty Mutual: Offers strong coverage for high-risk drivers and customizable policies.

- Island Insurance: A local Hawaii-based company with deep knowledge of the state’s unique needs and regulations.

Local insurers like Island Insurance may have an edge when it comes to understanding island-specific risks, such as tropical storms or remote road conditions.

Final Thoughts: Is Car Insurance Expensive in Hawaii?

So, is car insurance expensive in Hawaii? The short answer is no—especially when compared to many mainland states. With average full coverage costs around $1,500 per year, Hawaii offers relatively affordable auto insurance, thanks to its no-fault system, low uninsured driver rates, and favorable driving conditions.

However, “affordable” doesn’t mean “cheap.” Your actual cost will depend on your personal circumstances, including your age, driving history, vehicle, and where you live. The good news is that there are plenty of ways to keep your premiums low, from shopping around to taking advantage of discounts.

Ultimately, the best car insurance policy is one that offers the right balance of coverage, cost, and customer service. Don’t just go for the cheapest option—make sure it meets your needs and gives you confidence on the road.

Whether you’re a lifelong resident or new to the islands, understanding how much car insurance costs in Hawaii—and how to get the best deal—is a crucial part of responsible car ownership. With the right information and a little effort, you can drive safely, legally, and affordably through paradise.

Frequently Asked Questions

What is the average cost of car insurance in Hawaii?

The average cost of full coverage car insurance in Hawaii is between $1,400 and $1,800 per year. Minimum coverage typically costs $500 to $700 annually, which is slightly below the national average.

Is car insurance required in Hawaii?

Yes, all drivers in Hawaii must carry at least $10,000 in PIP, $20,000/$40,000 in bodily injury liability, and $10,000 in property damage liability. Driving without insurance can result in fines and license suspension.

Does Hawaii use a no-fault insurance system?

Yes, Hawaii is a no-fault state. This means your own insurance covers your medical expenses after an accident, regardless of who caused it, up to your PIP limit.

Can I lower my car insurance premium in Hawaii?

Yes, you can save by shopping around, raising your deductible, maintaining a clean driving record, and taking advantage of discounts like safe driver, multi-car, or good student discounts.

Do credit scores affect car insurance rates in Hawaii?

Yes, but only for drivers under 65. Insurers can use credit-based insurance scores to set rates, though drivers aged 65 and older are protected from credit-based pricing.

What happens if I’m in an accident with an uninsured driver in Hawaii?

If you have uninsured motorist coverage, your insurer will cover your injuries and damages. Without it, you may have to pursue the at-fault driver personally, which can be difficult if they lack assets or insurance.