Does Virginia Require Car Insurance?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Understanding Virginia’s Unique Car Insurance Laws

- 4 The Risks of Going Uninsured in Virginia

- 5 When Might the UMV Fee Make Sense?

- 6 How to Choose the Right Insurance Policy in Virginia

- 7 What Happens If You’re Caught Driving Without Insurance?

- 8 The Bottom Line: Is Car Insurance Worth It in Virginia?

- 9 Frequently Asked Questions

Virginia does not require traditional car insurance, but drivers must meet financial responsibility requirements through insurance or an uninsured motor vehicle (UMV) fee. Understanding your options and the risks involved is crucial to staying compliant and protected on the road.

If you’re a driver in Virginia, you might have heard something surprising: the state doesn’t technically require you to carry car insurance. That’s right—Virginia is one of only a handful of states in the U.S. that allows drivers to legally operate a vehicle without traditional auto insurance. But before you celebrate and cancel your policy, there’s a big catch. While insurance isn’t mandatory in the conventional sense, Virginia still enforces strict financial responsibility laws. This means you must prove you can pay for damages or injuries you might cause in an accident—whether through insurance or another approved method.

So, what does this really mean for you as a driver? It means you have a choice, but it’s a choice with serious consequences. You can either purchase a standard auto insurance policy that meets the state’s minimum coverage requirements, or you can pay an Uninsured Motor Vehicle (UMV) fee to the Virginia Department of Motor Vehicles (DMV). Sounds simple, right? But here’s the catch: paying the UMV fee does not give you any insurance coverage. It simply allows you to register your vehicle without a policy. If you cause an accident, you’re on the hook for all costs—medical bills, vehicle repairs, legal fees, and more—out of your own pocket.

This unique approach to car insurance in Virginia was designed to give drivers more flexibility, but it also places a heavy burden of responsibility on individuals. Most financial advisors, legal experts, and insurance professionals strongly recommend that drivers in Virginia still purchase full coverage insurance. The risks of going uninsured—even legally—are simply too high. In this article, we’ll break down everything you need to know about Virginia’s car insurance requirements, the pros and cons of each option, and how to make the smartest decision for your safety and financial security.

Key Takeaways

- Understanding Does Virginia Require Car Insurance?: Provides essential knowledge

📑 Table of Contents

Understanding Virginia’s Unique Car Insurance Laws

Virginia’s car insurance laws stand out from the rest of the country. While nearly every other state mandates that drivers carry at least a minimum amount of liability insurance, Virginia takes a different approach. Instead of requiring insurance, the state requires drivers to demonstrate “financial responsibility.” This means you must be able to cover the costs of damages or injuries you might cause in a car accident.

There are two main ways to meet this requirement:

1. Purchase a standard auto insurance policy that meets Virginia’s minimum coverage limits.

2. Pay the Uninsured Motor Vehicle (UMV) fee to the DMV and self-insure.

Let’s look at each option in more detail.

Option 1: Traditional Auto Insurance

This is the most common and widely recommended path. When you buy auto insurance in Virginia, your policy must include at least the following minimum coverages:

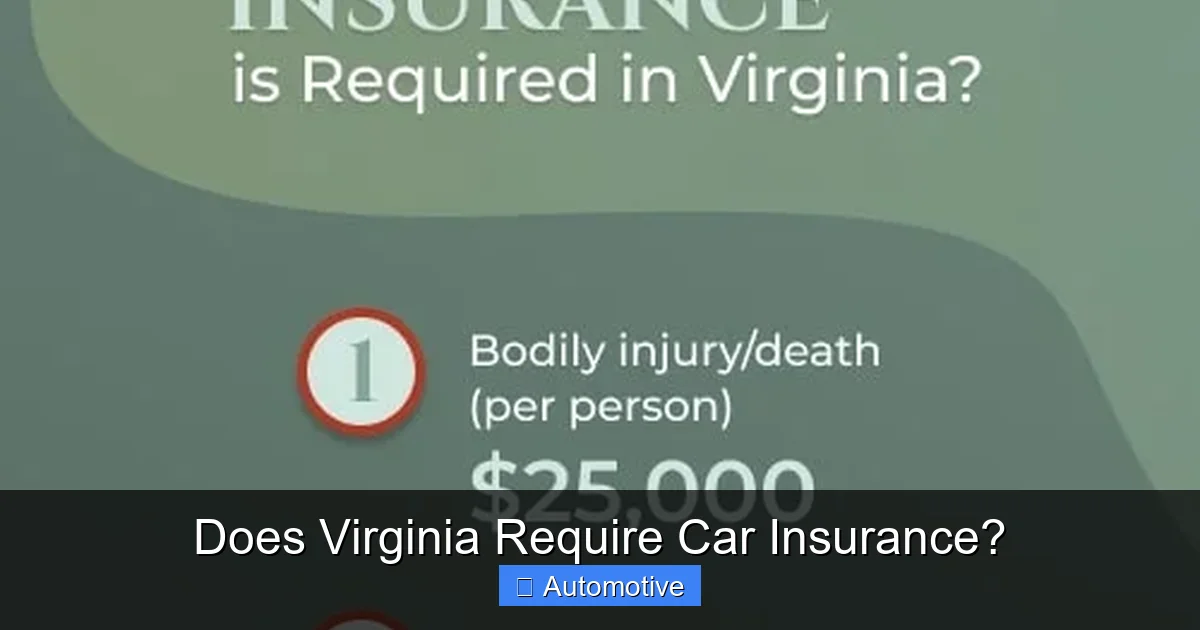

– Bodily Injury Liability: $25,000 per person, $50,000 per accident

– Property Damage Liability: $20,000 per accident

These limits are designed to cover the costs if you’re at fault in an accident. For example, if you rear-end another driver and cause $15,000 in vehicle damage and $30,000 in medical bills for the other person, your insurance would cover those costs up to your policy limits. If the damages exceed your coverage, you could be sued for the difference.

Many drivers choose to purchase additional coverage, such as:

– Collision coverage (for damage to your own vehicle)

– Comprehensive coverage (for theft, vandalism, or weather damage)

– Uninsured/underinsured motorist coverage (if the other driver has no or insufficient insurance)

– Medical payments coverage (for your own medical expenses)

These extras can provide peace of mind and protect your assets in the event of a serious accident.

Option 2: Paying the Uninsured Motor Vehicle (UMV) Fee

The UMV fee is a one-time payment of $500 that you make to the Virginia DMV when registering your vehicle. By paying this fee, you’re essentially telling the state: “I accept full financial responsibility for any damages I cause.” It’s a legal way to register your car without buying insurance.

But here’s the critical point: this fee does not provide any insurance coverage. It’s not a policy. It’s not protection. It’s simply a way to comply with the law while going uninsured.

If you cause an accident, you’ll have to pay for all damages yourself. That includes repairing or replacing the other person’s car, covering their medical bills, and potentially facing a lawsuit if the costs exceed what you can afford. And if you’re injured in an accident caused by someone else, you won’t have uninsured motorist coverage to help with your own medical expenses.

The Risks of Going Uninsured in Virginia

Visual guide about Does Virginia Require Car Insurance?

Image source: motorbiscuit.com

Choosing to pay the UMV fee instead of buying insurance might seem like a smart financial move—especially if you’re on a tight budget or drive an older car. But the risks far outweigh the short-term savings. Let’s explore why going uninsured in Virginia is a risky gamble.

Personal Financial Liability

When you drive without insurance, you’re personally responsible for every dollar of damage you cause. Imagine you’re at fault in a multi-car accident. The other drivers’ vehicles are totaled, and several people are injured. Medical bills could easily run into the tens of thousands—or even hundreds of thousands—of dollars. Without insurance, you’d have to pay all of that out of pocket.

Even a minor fender bender can cost thousands in repairs. If the other driver’s car is newer or more expensive than yours, the repair costs could be staggering. And if you can’t pay, the other party can sue you. A court judgment could lead to wage garnishment, liens on your property, or even bankruptcy.

No Coverage for Your Own Injuries or Vehicle

Another major downside of going uninsured is that you have no protection for yourself. If you’re injured in an accident—even one caused by another driver—you won’t have medical payments coverage or uninsured motorist benefits to help with your bills. You’ll have to rely on your health insurance, pay out of pocket, or go without care.

Similarly, if your car is damaged in a collision, theft, or natural disaster, you won’t have collision or comprehensive coverage to help with repairs or replacement. You’ll be stuck paying for everything yourself.

Legal and Registration Consequences

While paying the UMV fee allows you to register your vehicle legally, there are still risks. If you’re caught driving without meeting financial responsibility—whether through insurance or the UMV fee—you could face serious penalties. These include:

– Fines up to $1,125

– License suspension for up to one year

– Vehicle registration revocation

– Requirement to file an SR-22 form (proof of future insurance) for up to three years

And if you cause an accident while uninsured, the penalties can be even harsher. You could be charged with a misdemeanor, face higher fines, and be required to reimburse the state for any payments made to injured parties through the Virginia Uninsured Motorist Fund.

Difficulty Getting Insurance Later

Driving uninsured can also make it harder and more expensive to get insurance in the future. Insurance companies view uninsured drivers as high-risk, which can lead to higher premiums. And if you’re required to file an SR-22 after a violation, your rates could skyrocket.

When Might the UMV Fee Make Sense?

Visual guide about Does Virginia Require Car Insurance?

Image source: riverrunlaw.com

Despite the risks, there are a few scenarios where paying the UMV fee might seem tempting. But even in these cases, the decision should be made with extreme caution.

Older or Low-Value Vehicles

If you drive an older car that’s not worth much—say, under $2,000—you might think insurance isn’t worth the cost. After all, if the car is totaled, you won’t get much from a claim anyway. In this case, some drivers choose to pay the UMV fee and self-insure.

But remember: liability coverage isn’t just about protecting your own car. It’s about protecting you from the financial fallout of damaging someone else’s property or injuring another person. Even if your car is old, the other driver’s vehicle might be brand new. The medical bills could be enormous. The UMV fee doesn’t protect you from that.

Financial Hardship

If you’re truly unable to afford insurance, the UMV fee might seem like a lifeline. But before you go this route, explore other options. Many insurance companies offer low-cost policies for drivers with limited budgets. You might also qualify for discounts based on your driving record, vehicle type, or safety features.

Additionally, some nonprofit organizations and state programs offer assistance to low-income drivers. It’s worth researching these resources before deciding to go uninsured.

Short-Term Use

If you only plan to drive occasionally—for example, using a classic car for weekend trips—you might consider the UMV fee. But even then, the risk remains. A single accident could wipe out your savings. And if you ever decide to insure the vehicle later, you may face higher premiums due to the gap in coverage.

How to Choose the Right Insurance Policy in Virginia

Visual guide about Does Virginia Require Car Insurance?

Image source: quartzmountain.org

If you decide to purchase insurance—which is strongly recommended—here’s how to find the right policy for your needs.

Assess Your Coverage Needs

Start by evaluating your financial situation and driving habits. Ask yourself:

– How much can I afford to pay out of pocket if I cause an accident?

– What’s the value of my vehicle?

– Do I drive frequently or only occasionally?

– Do I have savings to cover unexpected expenses?

If you have significant assets—like a home, savings, or investments—you’ll want higher liability limits to protect them from lawsuits. Most experts recommend at least $100,000 per person/$300,000 per accident in bodily injury coverage and $100,000 in property damage coverage.

Compare Quotes from Multiple Insurers

Insurance rates can vary widely between companies, so it pays to shop around. Get quotes from at least three different insurers. Look beyond just the premium—consider the deductible, coverage options, customer service, and claims process.

Some top-rated insurance companies in Virginia include:

– State Farm

– GEICO

– Progressive

– Allstate

– USAA (for military members and families)

Take Advantage of Discounts

Many insurers offer discounts that can lower your premium. Common discounts include:

– Safe driver discount

– Multi-car discount

– Good student discount

– Anti-theft device discount

– Low-mileage discount

Be sure to ask about available discounts when getting quotes.

Review Your Policy Annually

Your insurance needs can change over time. Review your policy each year to make sure it still meets your needs. If you’ve paid off your car, moved to a safer area, or improved your driving record, you might qualify for lower rates.

What Happens If You’re Caught Driving Without Insurance?

Even though Virginia allows the UMV fee, driving without meeting financial responsibility is still a serious offense. If you’re pulled over or involved in an accident and can’t prove you’re insured or have paid the UMV fee, you could face:

– A fine of up to $1,125

– License suspension for up to one year

– Vehicle registration revocation

– Requirement to file an SR-22 form for three years

– Possible jail time (in extreme cases)

And if you cause an accident while uninsured, the consequences are even more severe. You could be sued for damages, face criminal charges, and be required to reimburse the state for any payments made to injured parties.

The Bottom Line: Is Car Insurance Worth It in Virginia?

So, does Virginia require car insurance? Technically, no—but it does require financial responsibility. While you can legally drive without insurance by paying the UMV fee, doing so leaves you exposed to enormous financial and legal risks.

For most drivers, the smart choice is to purchase a comprehensive auto insurance policy. The peace of mind, asset protection, and legal compliance it provides far outweigh the cost. Insurance isn’t just a legal requirement—it’s a crucial part of responsible driving.

If you’re unsure about your options, talk to an insurance agent or financial advisor. They can help you find a policy that fits your budget and protects your future. Remember: a few hundred dollars in premiums could save you tens of thousands in the event of an accident.

In the end, driving without insurance in Virginia isn’t just risky—it’s a gamble with your financial future. Don’t roll the dice. Get covered, stay safe, and drive with confidence.

Frequently Asked Questions

Does Virginia require car insurance?

Virginia does not require traditional car insurance, but drivers must meet financial responsibility requirements. This can be done by purchasing an insurance policy or paying the Uninsured Motor Vehicle (UMV) fee.

What is the Uninsured Motor Vehicle (UMV) fee?

The UMV fee is a $500 payment to the Virginia DMV that allows you to register your vehicle without buying insurance. However, it does not provide any coverage or protection in case of an accident.

What happens if I cause an accident without insurance in Virginia?

If you cause an accident and don’t have insurance, you’re personally responsible for all damages, injuries, and legal costs. You could face lawsuits, wage garnishment, or even bankruptcy.

Can I lose my license for not having insurance in Virginia?

Yes. If you’re caught driving without meeting financial responsibility—either through insurance or the UMV fee—your license can be suspended, and your vehicle registration revoked.

Do I need an SR-22 in Virginia?

An SR-22 may be required if you’re convicted of certain violations, such as driving without insurance, DUI, or reckless driving. It proves to the state that you have insurance coverage.

Is it cheaper to pay the UMV fee than buy insurance?

While the UMV fee is a one-time $500 payment, it offers no protection. Insurance premiums may be higher, but they provide valuable coverage that can save you thousands in the event of an accident.