When Does Your Car Insurance Go Down?

Your car insurance doesn’t stay the same forever—it can go down over time. Factors like clean driving records, increased experience, and smart policy adjustments all play a role in reducing your premiums. Understanding when and how your rates drop helps you save money and stay protected.

Key Takeaways

- Your driving record improves over time: A clean record with no accidents or tickets can lead to significant rate reductions after 3–5 years.

- Age and experience matter: Drivers typically see lower premiums once they reach age 25 and gain more driving experience.

- Vehicle depreciation affects coverage costs: As your car ages, comprehensive and collision coverage may become less expensive or optional.

- Discounts accumulate over time: Safe driver, low-mileage, and loyalty discounts can stack up, lowering your overall premium.

- Credit score improvements help: In most states, a better credit score can lead to lower insurance rates.

- Policy adjustments save money: Raising deductibles or dropping unnecessary coverage can reduce monthly payments.

- Shopping around pays off: Comparing quotes annually ensures you’re getting the best rate available.

📑 Table of Contents

- When Does Your Car Insurance Go Down?

- How Car Insurance Rates Are Determined

- Age and Experience: The Natural Rate Drop

- Driving Record Improvements: The Power of a Clean Slate

- Vehicle Depreciation and Coverage Adjustments

- Accumulating Discounts Over Time

- Credit Score Improvements and Rate Reductions

- Shopping Around: The Ultimate Rate Reset

- Conclusion: Take Control of Your Insurance Costs

When Does Your Car Insurance Go Down?

If you’ve been driving for a while, you’ve probably noticed that your car insurance bill doesn’t stay the same forever. In fact, it often goes down—sometimes significantly—over time. But when exactly does that happen? And what can you do to speed up the process?

Car insurance premiums aren’t set in stone. They’re based on a mix of factors including your age, driving history, location, vehicle type, credit score, and even how much you drive. As these factors change, so can your rates. The good news? Many of these changes work in your favor over time. Whether it’s gaining more experience behind the wheel, maintaining a clean record, or simply getting older, there are several natural milestones that can trigger a drop in your insurance costs.

Understanding when and why your car insurance goes down empowers you to take control of your expenses. It’s not just about waiting for time to pass—it’s about making smart choices that positively impact your risk profile in the eyes of insurers. In this guide, we’ll walk you through the key moments when your premiums are likely to decrease, what you can do to encourage those drops, and how to keep your coverage affordable without sacrificing protection.

How Car Insurance Rates Are Determined

Visual guide about When Does Your Car Insurance Go Down?

Image source: s3.amazonaws.com

Before we dive into when your car insurance goes down, it helps to understand how insurers calculate your premium in the first place. Insurance companies use complex algorithms to assess risk—the likelihood that you’ll file a claim. The higher the perceived risk, the higher your premium. Conversely, the lower the risk, the more likely your rates will drop.

Several core factors influence your rate:

- Age and driving experience: Younger drivers, especially teens and those under 25, are statistically more likely to be involved in accidents. That’s why their premiums are typically much higher. As you gain experience and age, your risk decreases.

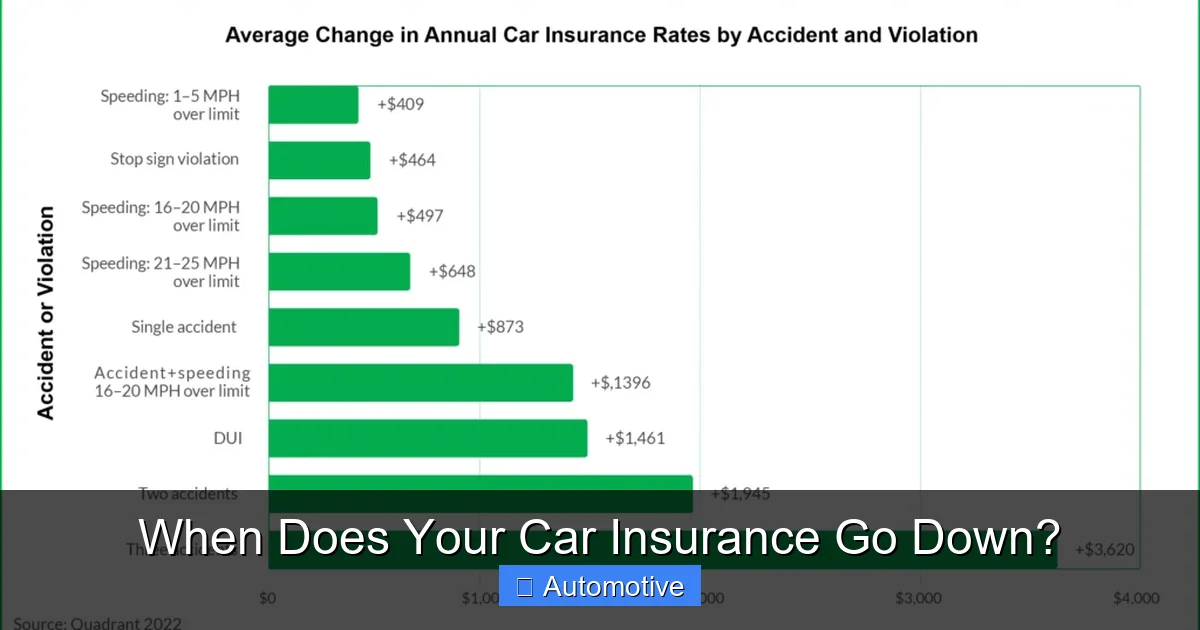

- Driving record: Accidents, speeding tickets, DUIs, and other violations signal higher risk. A clean record over time tells insurers you’re a safer bet.

- Vehicle type: Sports cars, luxury vehicles, and models with high repair costs usually cost more to insure. Older, less expensive cars often have lower premiums.

- Location: Urban areas with high traffic, theft rates, and accident frequency tend to have higher insurance costs than rural areas.

- Credit score: In most states, insurers use credit-based insurance scores to predict risk. Better credit often correlates with lower premiums.

- Mileage and usage: The more you drive, the greater your exposure to risk. Low-mileage drivers often qualify for discounts.

- Coverage level and deductible: Higher coverage limits and lower deductibles increase your premium. Adjusting these can lower costs.

These factors aren’t static. They evolve as your life changes. And that’s exactly why your car insurance can go down over time—because your risk profile improves.

Age and Experience: The Natural Rate Drop

Visual guide about When Does Your Car Insurance Go Down?

Image source: d2tez01fe91909.cloudfront.net

One of the most predictable times your car insurance goes down is when you reach certain age milestones—especially turning 25. Why 25? It’s not arbitrary. Insurance data consistently shows that drivers under 25 are involved in more accidents per mile driven than any other age group. Once you hit 25, you’re no longer in the highest-risk category, and insurers typically reward that with lower premiums.

But it’s not just about age—it’s about experience. A 25-year-old with five years of clean driving history is seen as much safer than a 25-year-old who just got their license. That’s why many insurers also consider the number of years you’ve been licensed. Some companies offer “experienced driver” discounts after you’ve held a license for 3, 5, or 10 years without major incidents.

Let’s look at an example: Sarah, 22, just got her license and is paying $2,400 a year for full coverage. She has a clean record but is still considered high-risk due to her age and lack of experience. By the time she turns 25 and has three accident-free years under her belt, her premium drops to $1,800. At 30, with a spotless record, she’s down to $1,400. That’s a $1,000 savings just from aging and gaining experience.

What You Can Do to Speed It Up

While you can’t rush time, you can make the most of it. Here’s how:

- Stay accident-free: Even one at-fault accident can delay rate reductions. Defensive driving courses can help you avoid collisions and may even earn you a discount.

- Maintain continuous coverage: Letting your policy lapse can increase your risk profile. Always keep your insurance active, even if you’re not driving much.

- Ask about experience-based discounts: Some insurers offer discounts for drivers with 5+ years of clean driving. Don’t assume you’ll be notified—ask your agent.

Driving Record Improvements: The Power of a Clean Slate

Visual guide about When Does Your Car Insurance Go Down?

Image source: rvandplaya.com

Your driving record is one of the most influential factors in your insurance rate. A single speeding ticket or fender bender can spike your premium by 20% or more. But the good news? Over time, those incidents fade in importance—especially if you maintain a clean record going forward.

Most insurers look at your driving history over the past 3 to 5 years. That means a ticket from six years ago likely won’t affect your rate at all. But a recent accident? That could keep your premiums high for several years.

Let’s say you got a speeding ticket two years ago. At the time, your insurer raised your rate by $300 per year. Now, two years later, you’ve had no other violations. As that ticket ages, its impact lessens. After three years, many insurers will no longer count it against you. That’s when your car insurance goes down—sometimes automatically, sometimes after a policy review.

How to Clean Up Your Record

If your record isn’t perfect, don’t panic. You can take steps to improve it:

- Take a defensive driving course: Many states allow you to remove a point from your license by completing an approved course. Some insurers also offer discounts for completing one.

- Contest unfair tickets: If you believe a ticket was issued in error, fight it in court. Winning can prevent it from appearing on your record.

- Drive safely and consistently: The best way to improve your record is to avoid future incidents. Use hands-free devices, obey speed limits, and stay alert.

Over time, a clean driving record signals reliability. And reliability equals lower risk—which means lower premiums.

Vehicle Depreciation and Coverage Adjustments

Your car’s value plays a big role in your insurance costs—especially for comprehensive and collision coverage. These coverages pay to repair or replace your vehicle if it’s damaged in an accident, stolen, or affected by weather, vandalism, or other non-collision events.

When your car is new, it’s expensive to repair or replace. That’s why comprehensive and collision premiums are higher. But as your car ages and depreciates, the cost to insure it drops. After 5–7 years, many cars are worth less than $5,000. At that point, the cost of comprehensive and collision coverage may exceed the car’s actual value.

This is a key moment when your car insurance can go down—if you adjust your coverage.

When to Drop Comprehensive and Collision

Consider dropping comprehensive and collision if:

- Your car is over 10 years old.

- The annual premium for these coverages is more than 10% of your car’s value.

- You have enough savings to cover a replacement out of pocket.

For example, if your 2015 sedan is worth $4,000 and you’re paying $600 a year for comprehensive and collision, that’s 15% of the car’s value. You’re paying more to insure it than it’s worth. Dropping those coverages could save you $50 a month—money you can put toward a future vehicle or emergency fund.

But be cautious. If you still have a car loan or lease, your lender likely requires full coverage. Also, if you drive in an area with high theft or severe weather, comprehensive coverage may still be worth it.

Other Coverage Adjustments

You can also lower your premium by:

- Raising your deductible: Increasing your deductible from $500 to $1,000 can reduce your premium by 15–30%. Just make sure you can afford the higher out-of-pocket cost if you need to file a claim.

- Reducing coverage limits: If you’re carrying more liability coverage than required by your state, consider lowering it—but only if you have other assets to protect. Liability coverage is cheap compared to the risk of a lawsuit.

- Removing unnecessary add-ons: Rental car reimbursement, roadside assistance, and glass coverage can add up. If you don’t need them, drop them.

These adjustments won’t affect your protection as much as they’ll reduce your monthly bill—making your car insurance go down without sacrificing essential coverage.

Accumulating Discounts Over Time

One of the most rewarding ways your car insurance goes down is through accumulating discounts. Many insurers offer a variety of savings opportunities, and the longer you stay with a company, the more discounts you may qualify for.

Here are some common discounts that can stack up over time:

- Safe driver discount: Awarded after 3–5 years of no accidents or violations.

- Loyalty discount: Given to customers who stay with the same insurer for several years.

- Low-mileage discount: For drivers who put fewer than 7,500–10,000 miles per year on their vehicle.

- Multi-policy discount: When you bundle auto insurance with home, renters, or life insurance.

- Good student discount: For full-time students with a B average or higher (often extends into early adulthood).

- Defensive driving course discount: For completing an approved safety course.

- Pay-in-full discount: For paying your annual premium upfront instead of monthly.

Let’s say you’re a 28-year-old with a clean record, drive 8,000 miles a year, bundle your auto and home insurance, and pay your premium annually. You could qualify for five or more discounts—adding up to 25–40% off your base rate.

How to Maximize Discounts

Don’t wait for discounts to appear. Take action:

- Ask your agent annually: “What discounts am I eligible for?” Policies and qualifications change.

- Track your mileage: Use a mileage tracker app to prove low usage.

- Bundle policies: If you rent or own a home, ask about multi-policy savings.

- Take a course: Even if you don’t have a ticket, a defensive driving course can earn you a discount.

Over time, these small savings add up—making your car insurance go down year after year.

Credit Score Improvements and Rate Reductions

In most states (except California, Hawaii, and Massachusetts), insurers use credit-based insurance scores to help determine your premium. The logic? Studies show a correlation between credit behavior and insurance risk. People with higher credit scores tend to file fewer claims.

If your credit score has improved—say, from 650 to 750—your car insurance may go down. A higher score signals financial responsibility, which insurers interpret as lower risk.

For example, a driver with a 620 credit score might pay $1,800 a year for full coverage. After improving their score to 740, they could see their premium drop to $1,400—a $400 annual savings.

How to Improve Your Credit Score

Improving your credit takes time, but it pays off in more ways than one:

- Pay bills on time: Payment history is the biggest factor in your credit score.

- Reduce credit card balances: Keep your credit utilization below 30%.

- Check your credit report: Look for errors and dispute them. You’re entitled to a free report from each bureau once a year at AnnualCreditReport.com.

- Avoid opening too many new accounts: Hard inquiries can temporarily lower your score.

Once your score improves, notify your insurer. Some companies automatically adjust rates, but others require a request. A quick call could save you hundreds.

Shopping Around: The Ultimate Rate Reset

Even if you’ve done everything right—maintained a clean record, improved your credit, and accumulated discounts—your current insurer might not be offering you the best rate. That’s why shopping around is one of the most effective ways to make your car insurance go down.

Insurance companies use different algorithms and risk models. What one company sees as high-risk, another might view as average. Plus, new customer incentives and promotional rates can make switching worthwhile.

Let’s say you’ve been with the same insurer for five years. You’ve earned loyalty discounts, but you haven’t compared quotes in years. When you finally shop around, you find a competitor offering the same coverage for $300 less per year. That’s a 20% savings—just for taking 30 minutes to compare.

When to Shop for New Insurance

Consider comparing quotes:

- Every 1–2 years, even if you’re happy with your current insurer.

- After major life changes (marriage, moving, buying a new car).

- When your policy is up for renewal.

- If you’ve improved your credit score or driving record.

Use online comparison tools or work with an independent agent who can check multiple companies. Be sure to compare apples to apples—same coverage limits, deductibles, and discounts.

Switching Without Lapses

When switching insurers, timing is key. Never cancel your current policy before the new one starts. A lapse in coverage can increase your rates with future insurers. Instead, schedule the new policy to begin the day your old one ends.

Also, ask your new insurer about a “proof of prior coverage” discount. Many companies offer this to customers who’ve maintained continuous insurance.

Conclusion: Take Control of Your Insurance Costs

Your car insurance doesn’t have to be a fixed expense. It can—and often does—go down over time. Whether it’s due to aging, a clean driving record, vehicle depreciation, accumulated discounts, credit improvements, or simply shopping around, there are many ways to reduce your premium.

The key is awareness and action. Don’t assume your insurer will automatically lower your rate when you qualify for a discount. Stay informed, review your policy annually, and take steps to improve your risk profile.

Remember, insurance is about protection—but it shouldn’t break the bank. By understanding when and why your car insurance goes down, you can save hundreds of dollars a year while still staying fully covered. So take control, make smart choices, and watch your premiums drop over time.

Frequently Asked Questions

When does car insurance typically go down for young drivers?

Car insurance usually goes down when young drivers turn 25, as they move out of the highest-risk age group. Rates may also decrease after 3–5 years of clean driving, regardless of age.

Can a clean driving record lower my insurance premium?

Yes, a clean driving record with no accidents or tickets can significantly reduce your premium over time. Most insurers review your record over the past 3–5 years.

Will my insurance go down if I improve my credit score?

In most states, yes. A higher credit score can lead to lower car insurance rates, as insurers view good credit as a sign of lower risk.

Should I drop comprehensive and collision coverage on an older car?

It may be worth considering if your car is over 10 years old and the cost of coverage exceeds 10% of its value. Just make sure you can afford to replace the car if needed.

How often should I shop around for car insurance?

It’s a good idea to compare quotes every 1–2 years or after major life changes. This ensures you’re getting the best rate available.

Do loyalty discounts really make a difference?

Yes, loyalty discounts can save you 5–15% or more over time. However, it’s still wise to compare rates periodically, as another insurer might offer a better deal.