Do I Need Gap Insurance on a Used Car

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Do I Need Gap Insurance on a Used Car?

- 4 What Is Gap Insurance and How Does It Work?

- 5 When Does Gap Insurance Make Sense for a Used Car?

- 6 When Might You NOT Need Gap Insurance on a Used Car?

- 7 How Much Does Gap Insurance Cost?

- 8 How to Buy Gap Insurance for a Used Car

- 9 Common Misconceptions About Gap Insurance

- 10 Final Thoughts: Should You Get Gap Insurance on a Used Car?

- 11 Frequently Asked Questions

Gap insurance covers the difference between what you owe on your car loan and the car’s actual cash value if it’s totaled or stolen. While not always necessary for used cars, it can be a smart financial safety net—especially if you have a long loan term, low down payment, or rapid depreciation.

Key Takeaways

- Gap insurance protects against negative equity: If your used car is totaled, your auto insurance pays the current market value—not what you still owe. Gap insurance covers the gap.

- It’s most useful with long loan terms: Loans over 60 months increase the risk of owing more than the car is worth, making gap insurance more valuable.

- Low down payments increase your need: Putting little or nothing down means you start with negative equity, so gap coverage can prevent out-of-pocket losses.

- Not all used cars depreciate quickly: Some models hold their value well. Research your car’s depreciation rate before deciding.

- Gap insurance isn’t always available: Some lenders or insurers don’t offer it on older used cars. Check availability early.

- It’s usually cheaper at the dealership: Buying gap coverage when you sign your loan is often more affordable than adding it later.

- You may not need it if you have strong equity: If you’ve paid down your loan significantly or made a large down payment, gap insurance may be unnecessary.

📑 Table of Contents

- Do I Need Gap Insurance on a Used Car?

- What Is Gap Insurance and How Does It Work?

- When Does Gap Insurance Make Sense for a Used Car?

- When Might You NOT Need Gap Insurance on a Used Car?

- How Much Does Gap Insurance Cost?

- How to Buy Gap Insurance for a Used Car

- Common Misconceptions About Gap Insurance

- Final Thoughts: Should You Get Gap Insurance on a Used Car?

Do I Need Gap Insurance on a Used Car?

Buying a used car can be a smart financial move. You avoid the steepest part of depreciation, often get lower insurance rates, and still enjoy reliable transportation. But once you drive off the lot, one big question remains: Do I need gap insurance on a used car?

It’s a fair question—and one that many buyers overlook. Gap insurance isn’t required by law, and it’s not always pushed hard by salespeople. But in the right situation, it can save you thousands of dollars if your car is totaled or stolen. On the flip side, if you’re in a strong financial position with your loan, it might be an unnecessary expense.

So how do you decide? The answer depends on several factors: your loan terms, down payment, the car’s depreciation rate, and your personal risk tolerance. In this guide, we’ll walk you through everything you need to know about gap insurance for used cars—what it is, when it makes sense, and how to make the best choice for your situation.

What Is Gap Insurance and How Does It Work?

Visual guide about Do I Need Gap Insurance on a Used Car

Image source: moneyabcs.uta.edu

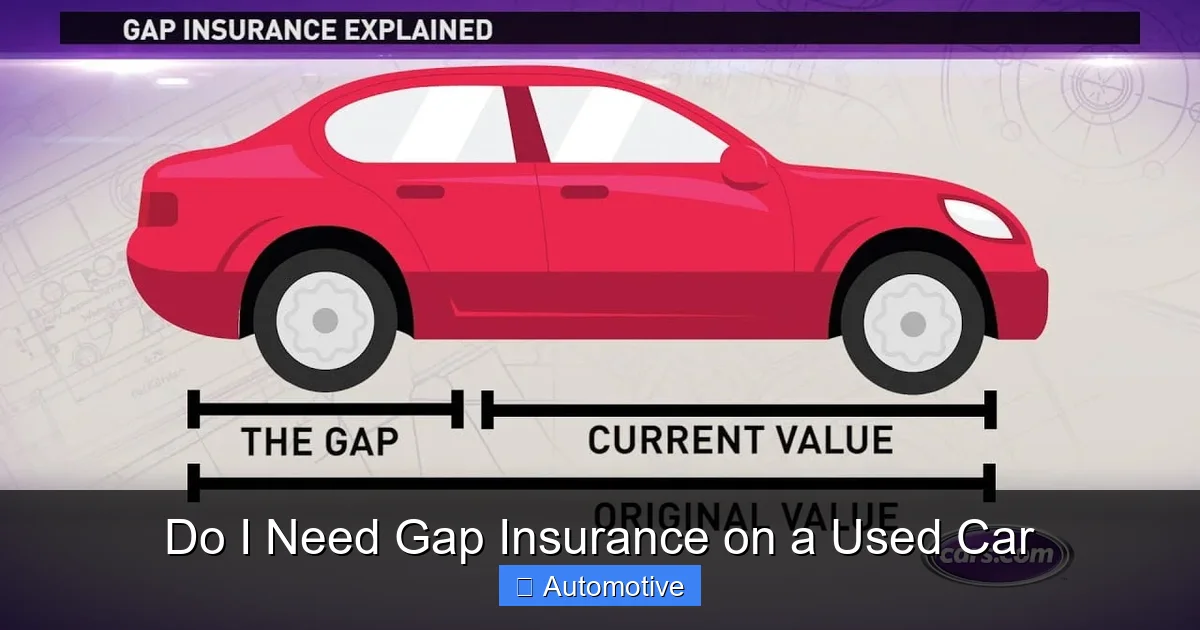

Let’s start with the basics. Gap insurance—short for “guaranteed asset protection” insurance—is designed to cover the difference between what you owe on your car loan and what your car is actually worth at the time of a total loss.

Here’s how it works: If your used car is involved in a serious accident or stolen and declared a total loss by your insurance company, your standard auto insurance policy will pay out the car’s actual cash value (ACV). That’s the market value of the car right before the incident, based on factors like age, mileage, condition, and local demand.

But here’s the catch: cars lose value fast. Even used cars can depreciate significantly in the first few years of ownership. If you financed most of the purchase price with a long-term loan, you might owe more than the car is worth. This is called being “upside down” or having “negative equity.”

That’s where gap insurance steps in. If you have a claim, your regular insurance pays the ACV, and gap insurance covers the remaining balance on your loan—up to a certain limit, usually the original loan amount or a percentage of the car’s value.

For example, let’s say you bought a used SUV for $25,000 with a $2,000 down payment and financed $23,000 over 72 months. Two years in, the car is totaled in an accident. At that point, the car’s actual cash value is $18,000, but you still owe $19,500 on the loan.

Your auto insurance pays $18,000. Without gap insurance, you’re on the hook for the remaining $1,500. But with gap insurance, that $1,500 is covered, and you walk away debt-free.

How Gap Insurance Differs from Regular Auto Insurance

It’s important to understand that gap insurance is not a replacement for collision or comprehensive coverage. You still need those to protect your vehicle. Gap insurance is an add-on that works alongside your existing policy.

Think of it this way:

– Collision and comprehensive insurance pay to repair or replace your car based on its current market value.

– Gap insurance pays the difference between that value and what you still owe.

They serve different purposes, and both can be valuable depending on your financial situation.

Types of Gap Insurance

Not all gap insurance is the same. There are two main types:

1. Regular Gap Insurance: This covers the difference between your loan balance and the car’s ACV. It’s the most common type and works well for most buyers.

2. Return to Invoice (RTI) or Full Gap Insurance: This more comprehensive version may also cover your deductible, finance charges, and sometimes even the cost of a replacement vehicle up to a certain amount. It’s more expensive but offers greater protection.

Some lenders offer their own gap products, while others allow you to purchase it through third-party insurers. Always read the fine print to understand what’s covered and what’s not.

When Does Gap Insurance Make Sense for a Used Car?

Visual guide about Do I Need Gap Insurance on a Used Car

Image source: thumbor.forbes.com

Now that you understand what gap insurance does, let’s talk about when it actually makes financial sense—especially for used cars.

Used cars don’t depreciate as quickly as new ones, but they still lose value over time. And if you’re financing a large portion of the purchase price, you could still end up owing more than the car is worth.

Here are the key scenarios where gap insurance is worth considering:

You Have a Long Loan Term (60+ Months)

The longer your loan term, the more time your car has to depreciate while you’re still paying it off. A 72- or 84-month loan might seem manageable with low monthly payments, but it increases the risk of negative equity.

For example, a used car that costs $20,000 today might be worth only $12,000 in three years. If you’re still paying off a 72-month loan, you could easily owe $14,000 or more at that point. That’s a $2,000 gap—money you’d have to pay out of pocket if the car is totaled.

Gap insurance eliminates that risk.

You Made a Small or No Down Payment

If you financed 90% or more of the car’s value, you started with little to no equity. Even a small drop in value can put you underwater on your loan.

Let’s say you bought a used sedan for $18,000 with no down payment and a 60-month loan. After one year, the car is worth $15,000, but you still owe $16,500. That’s a $1,500 gap.

Without gap insurance, you’d have to pay that difference if the car is totaled. With it, you’re protected.

You’re Leasing the Used Car

Leased vehicles often come with gap insurance built into the contract, but if you’re leasing a used car privately or through a non-traditional lender, you may need to purchase it separately.

Leases are especially vulnerable to negative equity because you’re paying for the car’s depreciation during the lease term. If the car is totaled early in the lease, you could owe far more than its current value.

The Car Has a High Depreciation Rate

Not all used cars lose value at the same rate. Luxury brands, certain SUVs, and vehicles with high mileage or poor reliability ratings tend to depreciate faster.

For example, a used BMW or Mercedes might lose 40–50% of its value in the first three years, even if it’s well-maintained. If you’re financing such a vehicle, gap insurance could be a smart hedge against rapid depreciation.

On the other hand, Toyota, Honda, and Subaru models often hold their value well. If you’re buying a used Camry or CR-V with a strong resale history, you may be less likely to owe more than the car is worth.

You Can’t Afford an Unexpected Out-of-Pocket Expense

Even a $1,000 or $2,000 gap might be manageable for some people, but for others, it could mean financial hardship. If you’re living paycheck to paycheck or don’t have an emergency fund, gap insurance can provide peace of mind.

It’s essentially insurance for your loan—protecting you from a worst-case scenario that could otherwise derail your finances.

When Might You NOT Need Gap Insurance on a Used Car?

Visual guide about Do I Need Gap Insurance on a Used Car

Image source: money.madenginer.com

Gap insurance isn’t always necessary. In fact, for some buyers, it’s an unnecessary expense. Here’s when you might skip it:

You Have Significant Equity in the Car

If you made a large down payment—say, 20% or more—or have already paid down a big portion of the loan, you’re less likely to owe more than the car is worth.

For example, if you put $5,000 down on a $20,000 used car and have already paid off $8,000 in principal, you owe $7,000. If the car is now worth $12,000, you have $5,000 in equity. In this case, gap insurance isn’t needed.

Your Loan Term Is Short (48 Months or Less)

Shorter loan terms mean you pay off the principal faster and build equity more quickly. With a 36- or 48-month loan, you’re less likely to be upside down, especially if you made a decent down payment.

The Car Holds Its Value Well

As mentioned earlier, some used cars depreciate slowly. If you’re driving a Toyota, Honda, or Subaru with a strong resale market, the gap between what you owe and what the car is worth may never materialize.

Check resources like Kelley Blue Book or Edmunds to see how your specific make and model holds value over time.

You Plan to Pay Off the Loan Early

If you’re making extra payments or plan to pay off your loan in a few years, you’ll reduce your balance faster than the car depreciates. This reduces the risk of negative equity.

Just remember: if you pay off the loan early, you may be able to cancel gap insurance, but check your policy terms first.

You Have Other Financial Protections

Some people have emergency savings, disability insurance, or other financial cushions that could cover a small gap. If you’re confident you could handle a $1,000–$2,000 loss without major hardship, gap insurance might not be worth the cost.

How Much Does Gap Insurance Cost?

The cost of gap insurance varies, but it’s generally affordable—especially when compared to the potential financial risk it mitigates.

On average, gap insurance costs between $200 and $700 for the life of the loan, depending on the lender, the car’s value, and the type of coverage.

Here’s a breakdown:

– Dealership-purchased gap insurance: Often the most convenient and sometimes the cheapest option. It’s typically rolled into your loan, so you pay interest on it, but the upfront cost is low.

– Third-party gap insurance: Can be purchased from insurers like Progressive, Geico, or standalone gap providers. May offer more flexibility but could be slightly more expensive.

– Bank or credit union gap products: Some lenders offer their own gap coverage as part of the financing package.

For example, a $400 gap policy on a $20,000 used car loan might cost less than $10 per month if financed over 60 months. That’s a small price to pay for protection against a $2,000–$5,000 loss.

Is It Worth the Cost?

To decide if gap insurance is worth it, consider the potential payout versus the cost.

Let’s say your gap policy costs $500 and covers up to $10,000 in negative equity. If there’s a 5% chance your car is totaled in the next three years, the expected value of the insurance is $500 (5% of $10,000). That’s break-even.

But if the risk is higher—due to driving conditions, location, or the car’s age—the insurance becomes more valuable. And if you can’t afford to pay a gap out of pocket, even a small chance of loss makes the insurance worthwhile.

How to Buy Gap Insurance for a Used Car

If you decide gap insurance is right for you, here’s how to get it:

Buy It at the Time of Purchase

The best time to buy gap insurance is when you sign your loan or lease agreement. Most dealerships offer it as an add-on, and it’s often cheaper when bundled with financing.

You can usually roll the cost into your loan, so you don’t pay upfront. Just be aware that you’ll pay interest on the gap premium over the life of the loan.

Check with Your Auto Insurer

Some major insurers offer gap coverage as an endorsement to your existing policy. Call your agent to see if it’s available and how much it costs.

This can be a good option if you’re buying a used car privately and not using dealership financing.

Compare Third-Party Providers

Companies like Endurance, Protect My Car, and others offer standalone gap insurance. These can be more flexible but may require more paperwork.

Always compare quotes and read reviews before choosing a provider.

Understand the Terms and Conditions

Not all gap policies are created equal. Before buying, ask:

– What’s the maximum coverage amount?

– Does it cover the deductible?

– Are there exclusions (e.g., certain types of accidents or modifications)?

– Can you cancel it early if you pay off the loan?

Make sure the policy matches your needs and loan terms.

Common Misconceptions About Gap Insurance

There are a few myths about gap insurance that can lead to confusion. Let’s clear them up:

“Gap insurance pays for a new car.”

No—it pays the difference between your loan balance and the car’s current value. It doesn’t buy you a replacement vehicle. Some enhanced policies (like RTI) may offer a replacement benefit, but standard gap insurance does not.

“I don’t need it because my car is used.”

Used cars can still depreciate and leave you with negative equity, especially with long loans and low down payments. Age doesn’t eliminate the risk.

“My regular insurance will cover the gap.”

Standard auto insurance only pays the actual cash value. It does not cover loan balances. You need gap insurance for that.

“Gap insurance is required by law.”

It’s not required anywhere in the U.S. It’s optional, though some lenders may require it for certain loans.

Final Thoughts: Should You Get Gap Insurance on a Used Car?

So, do you need gap insurance on a used car? The answer isn’t one-size-fits-all.

If you have a long loan term, made a small down payment, or are driving a car that depreciates quickly, gap insurance can be a smart financial move. It protects you from owing money on a car you no longer have—a situation that can happen even with used vehicles.

On the other hand, if you have significant equity, a short loan term, or a car that holds its value well, you may not need it.

The key is to assess your personal risk. Ask yourself:

– How much do I owe vs. how much is the car worth?

– Could I afford to pay the gap if the car is totaled?

– Am I comfortable with that risk?

If the answer to the second question is “no,” gap insurance is probably worth the cost.

At the end of the day, it’s about peace of mind. For a few hundred dollars, you can protect yourself from a potentially devastating financial hit. And in the world of car ownership, that kind of protection is priceless.

Frequently Asked Questions

Is gap insurance required for used cars?

No, gap insurance is not required by law for used cars. However, some lenders may require it if you have a long loan term or made a small down payment.

Can I buy gap insurance after purchasing a used car?

It depends. Some insurers and lenders allow you to add gap coverage later, but it’s often more expensive and may not be available if the car is too old or has high mileage.

Does gap insurance cover theft?

Yes, gap insurance typically covers theft if your car is declared a total loss by your insurance company. It works the same way as coverage for accidents.

Can I cancel gap insurance early?

Many policies allow cancellation if you pay off your loan early. Check your contract terms, as some may charge a fee or require proof of payoff.

Does gap insurance cover my deductible?

Standard gap insurance usually does not cover your deductible, but some enhanced policies (like Return to Invoice) may include it. Always verify what’s covered.

Is gap insurance worth it for a 10-year-old used car?

It’s less likely to be worth it for very old cars, especially if they have high mileage and low value. The risk of owing more than the car is worth is lower, and gap policies may not even be available.