What Is a Deductible in Car Insurance?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is a Deductible in Car Insurance?

- 4 How Does a Car Insurance Deductible Work?

- 5 Types of Car Insurance Deductibles

- 6 How Deductibles Affect Your Insurance Premiums

- 7 When Does the Deductible Apply?

- 8 How to Choose the Right Deductible for You

- 9 Common Misconceptions About Car Insurance Deductibles

- 10 Tips for Managing Your Deductible

- 11 Conclusion

- 12 Frequently Asked Questions

A deductible in car insurance is the amount you pay out of pocket before your insurer covers the rest of a claim. Choosing the right deductible affects your premiums and out-of-pocket costs during a claim.

Key Takeaways

- Definition: A deductible is the portion of a claim you pay before insurance kicks in, common in collision and comprehensive coverage.

- Types of Deductibles: Most are fixed dollar amounts (e.g., $500), but some policies use percentage-based deductibles, especially for older vehicles.

- Impact on Premiums: Higher deductibles lower your monthly premium, while lower deductibles mean higher premiums but less to pay when filing a claim.

- When It Applies: Deductibles apply only to certain coverages—typically collision and comprehensive—not liability or medical payments.

- Choosing Wisely: Pick a deductible you can comfortably afford to pay in case of an accident, balancing savings and financial safety.

- State Rules Vary: Some states have regulations on minimum or maximum deductible amounts, so check local laws.

- Claims Process: You pay the deductible directly to the repair shop or insurer, depending on the claim type and provider.

📑 Table of Contents

- What Is a Deductible in Car Insurance?

- How Does a Car Insurance Deductible Work?

- Types of Car Insurance Deductibles

- How Deductibles Affect Your Insurance Premiums

- When Does the Deductible Apply?

- How to Choose the Right Deductible for You

- Common Misconceptions About Car Insurance Deductibles

- Tips for Managing Your Deductible

- Conclusion

What Is a Deductible in Car Insurance?

When you’re shopping for car insurance or reviewing your current policy, you’ve probably come across the term “deductible.” But what does it really mean? In simple terms, a deductible in car insurance is the amount of money you agree to pay out of your own pocket before your insurance company steps in to cover the rest of a claim. Think of it as your share of the cost when something goes wrong—like a fender bender, a cracked windshield, or damage from a fallen tree.

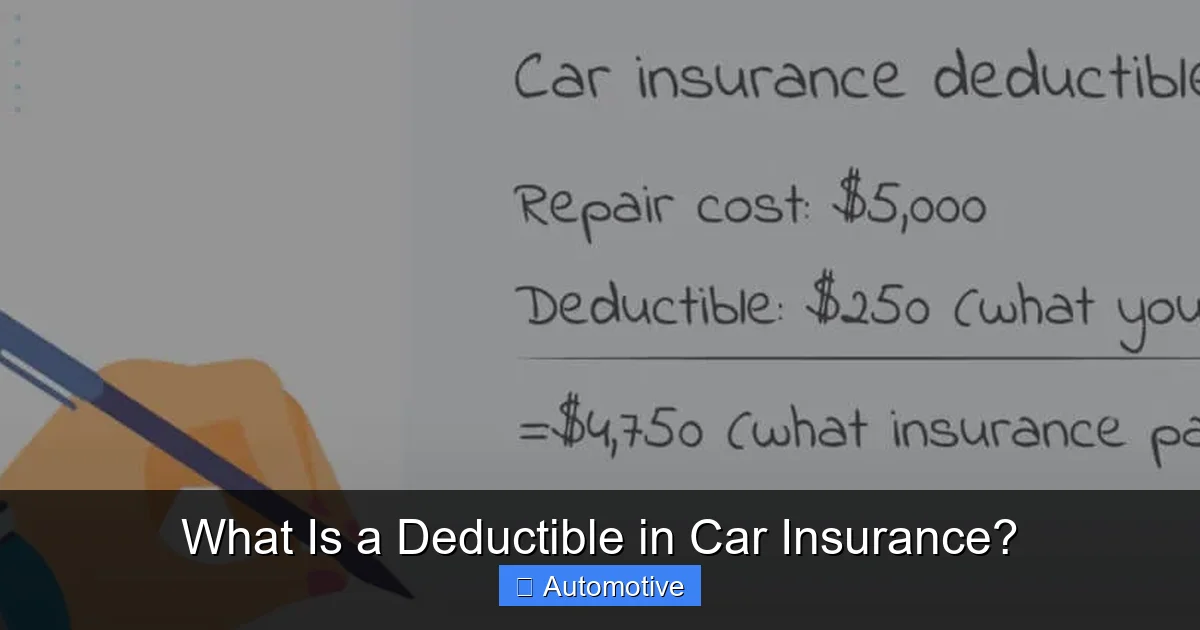

For example, if you have a $500 deductible and your car sustains $2,000 in damage from an accident, you’ll pay the first $500, and your insurer will cover the remaining $1,500. This system helps keep insurance premiums more affordable for everyone by sharing the financial responsibility between you and the insurance company. Without deductibles, insurers would have to charge much higher premiums to cover every small claim.

Understanding your deductible is crucial because it directly affects how much you’ll pay both monthly and in the event of a claim. It’s one of the most important decisions you’ll make when choosing or updating your car insurance policy. Whether you’re a new driver or have been behind the wheel for decades, knowing how deductibles work can save you money and reduce stress when you need your insurance the most.

How Does a Car Insurance Deductible Work?

Visual guide about What Is a Deductible in Car Insurance?

Image source: bjak.my

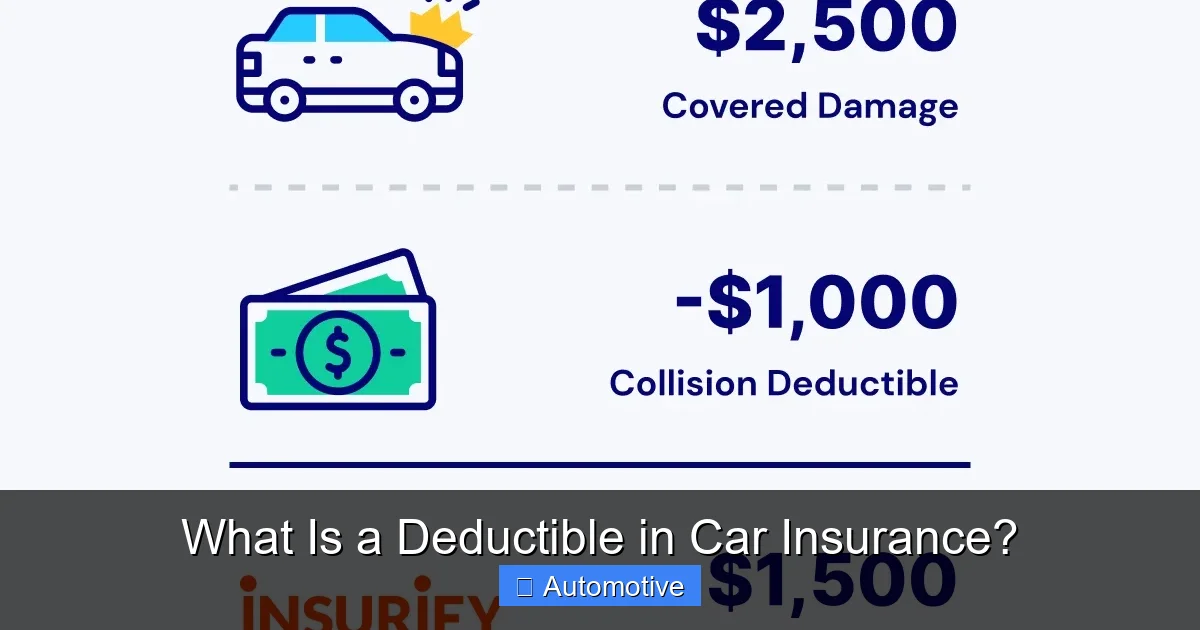

Let’s break it down with a real-life scenario. Imagine you’re driving home on a rainy evening and accidentally rear-end another car at a stoplight. Your car’s front bumper is damaged, and the repair estimate comes in at $1,800. If you have a $500 deductible on your collision coverage, you’ll pay $500, and your insurance company will pay the remaining $1,300. That $500 is your responsibility—no matter what.

But here’s the key: the deductible only applies when you file a claim under certain types of coverage. Most commonly, deductibles are tied to collision and comprehensive coverage. Collision covers damage from accidents with other vehicles or objects, while comprehensive covers non-collision events like theft, vandalism, fire, or weather damage. So if your car is stolen or hit by a hailstorm, your deductible will apply when you make a claim.

On the other hand, if you’re at fault in an accident and the other driver’s car is damaged, your liability coverage pays for their repairs—and there’s no deductible involved. Liability insurance covers damage or injuries you cause to others, not your own vehicle. That’s why deductibles don’t apply to liability, medical payments, or uninsured motorist coverage.

It’s also important to know that not all claims require you to pay a deductible. For instance, some insurers waive the deductible if the other driver is clearly at fault and their insurance covers your damages. Additionally, glass repair or replacement (like a cracked windshield) may be covered with no deductible under certain policies—especially if you have full glass coverage.

Who Pays the Deductible?

When a claim is filed, the deductible is typically paid directly to the repair shop. After your insurer approves the claim, they’ll issue a check to the repair facility for the amount minus your deductible. You then pay the shop the deductible amount, either upfront or when you pick up your car. Some insurers may allow you to pay the deductible in installments or even roll it into a financing plan, but this varies by company.

In some cases, especially with smaller claims, your insurer might send you a check for the full repair amount, and you’re responsible for paying the shop—including the deductible portion. Always clarify how the payment process works with your insurance agent or company to avoid surprises.

Does the Deductible Apply Every Time?

Yes—each time you file a claim under a coverage that includes a deductible, you’ll pay it. So if you have two separate incidents in one year—say, a collision in March and a hailstorm in July—you’ll pay the deductible twice. This is why it’s important to consider how often you might need to use your insurance and whether a high deductible makes sense for your lifestyle.

Types of Car Insurance Deductibles

Visual guide about What Is a Deductible in Car Insurance?

Image source: a.storyblok.com

Not all deductibles are created equal. While most car insurance deductibles are fixed dollar amounts, there are a few different types you might encounter, depending on your policy and insurer.

Fixed Dollar Deductibles

This is the most common type. You choose a set amount—like $250, $500, or $1,000—and that’s what you pay each time you file a claim. These are straightforward and easy to understand. For example, a $500 deductible means you pay $500 no matter how large the claim is (as long as it’s above $500).

Fixed deductibles are typically used for collision and comprehensive coverage. They give you predictable out-of-pocket costs and are ideal for most drivers.

Percentage-Based Deductibles

Less common, but still used—especially for older vehicles—percentage-based deductibles are calculated as a percentage of the car’s actual cash value (ACV). For instance, if your car is worth $10,000 and you have a 10% deductible, you’d pay $1,000 out of pocket for a claim.

This type is rare in standard auto policies but may appear in specialty or classic car insurance. It’s more common in homeowners or renters insurance, so don’t be surprised if you don’t see it on your car policy.

No Deductible Options

Some insurers offer policies with no deductible, especially for specific types of claims. For example, many companies now offer full glass coverage with no deductible for windshield repairs or replacements. This is a great perk, especially in areas with lots of road debris or extreme weather.

Additionally, some high-end or luxury car insurance plans may include zero-deductible options for certain coverages as part of a premium package. While these plans often come with higher monthly premiums, they can provide peace of mind for drivers who want minimal out-of-pocket costs.

Disappearing Deductibles

A newer trend in the insurance world is the “disappearing deductible.” With this feature, your deductible decreases over time as long as you remain accident-free. For example, your $500 deductible might drop to $250 after one year with no claims, and to $0 after three years. If you do file a claim, the deductible resets to the original amount.

This is a great incentive for safe driving and can save you money in the long run. Not all insurers offer this, so ask your agent if it’s available.

How Deductibles Affect Your Insurance Premiums

Visual guide about What Is a Deductible in Car Insurance?

Image source: images.contentstack.io

One of the biggest factors in determining your car insurance premium is your deductible amount. In general, the higher your deductible, the lower your monthly premium. Why? Because you’re taking on more financial risk, the insurer takes on less—and they reward you with lower rates.

Let’s look at an example. Suppose you’re comparing two policies with identical coverage except for the deductible:

– Policy A: $250 deductible → $120 per month

– Policy B: $1,000 deductible → $90 per month

Over a year, Policy A costs $1,440, while Policy B costs $1,080—a savings of $360. That’s a significant difference. But remember: if you file a claim, you’ll pay $750 more out of pocket with Policy B.

So the trade-off is clear: lower premiums now vs. higher costs later. The right choice depends on your budget, driving habits, and how much risk you’re comfortable taking on.

Who Should Choose a High Deductible?

A high deductible (like $1,000) makes sense if:

– You have a clean driving record and rarely file claims.

– You have enough savings to cover the deductible in an emergency.

– You drive an older car with lower repair costs.

– You’re looking to reduce your monthly expenses.

For example, a retiree who drives infrequently and has a paid-off, 10-year-old sedan might benefit from a high deductible. Their risk of accidents is low, and they can save hundreds per year on premiums.

Who Should Choose a Low Deductible?

A low deductible (like $250 or $500) is better if:

– You drive frequently or in high-traffic areas.

– You have a newer or more expensive vehicle.

– You don’t have much savings to cover unexpected costs.

– You prefer predictable out-of-pocket expenses.

A young professional with a new SUV and a tight budget might opt for a lower deductible to avoid large, unexpected bills after an accident.

Balancing Risk and Savings

The key is to find a balance. Use this simple rule of thumb: choose a deductible you could pay comfortably within 30 days if needed. If a $1,000 deductible would force you to use a credit card or borrow money, it’s probably too high.

Also, consider your car’s value. If your car is only worth $3,000, paying a $1,000 deductible for a $2,500 repair claim means you’re covering 40% of the cost. In such cases, a lower deductible might make more sense.

When Does the Deductible Apply?

Not every claim triggers your deductible. It’s important to know exactly when you’ll be on the hook for that out-of-pocket amount.

Collision and Comprehensive Claims

These are the two main coverages where deductibles apply. Whether you hit a deer, back into a pole, or your car is stolen, you’ll pay your deductible when filing a claim under these sections.

For example:

– You skid on ice and damage your front end → collision claim → deductible applies.

– A tree branch falls on your roof during a storm → comprehensive claim → deductible applies.

Liability, Medical Payments, and Uninsured Motorist Coverage

These coverages do not have deductibles. If you’re at fault in an accident and the other driver’s car is damaged, your liability coverage pays for it—no deductible. Similarly, if you or your passengers are injured, medical payments or PIP (personal injury protection) coverage kicks in without requiring you to pay first.

Uninsured motorist coverage also typically has no deductible. If you’re hit by a driver with no insurance, your policy covers your damages directly.

Glass and Windshield Repairs

Many insurers now offer full glass coverage with no deductible. This means if your windshield cracks from a flying rock, you can get it repaired or replaced at no cost. However, this is optional and may increase your premium slightly.

If you don’t have this add-on, a standard comprehensive deductible will apply to glass claims.

Rental Reimbursement and Towing

These are additional coverages that usually don’t involve deductibles. If your car is in the shop after an accident, rental reimbursement pays for a temporary vehicle—no deductible. Same with roadside assistance or towing services.

How to Choose the Right Deductible for You

Picking the right deductible isn’t just about saving money—it’s about managing risk. Here’s a step-by-step guide to help you decide.

Step 1: Assess Your Financial Situation

Ask yourself: How much can I afford to pay out of pocket if I have an accident? If you have $1,000 in savings set aside for emergencies, a $1,000 deductible might be manageable. But if your savings are low, a $500 or $250 deductible could be safer.

Step 2: Consider Your Driving Habits

Do you commute daily in heavy traffic? Do you drive long distances for work? High-mileage drivers face more risk and may benefit from a lower deductible. On the other hand, if you only drive occasionally—like on weekends—you might be able to handle a higher deductible.

Step 3: Evaluate Your Vehicle’s Value

If your car is worth $20,000, a $1,000 deductible is 5% of its value—reasonable. But if your car is only worth $5,000, that same deductible is 20%, which might be too high. In such cases, a lower deductible or even dropping collision/comprehensive coverage altogether might make sense.

Step 4: Compare Quotes

Get quotes from multiple insurers with different deductible amounts. Use online comparison tools or work with an independent agent. Look at the total annual cost—premiums plus potential out-of-pocket expenses—to see which option offers the best value.

Step 5: Review Annually

Your needs change over time. A deductible that made sense when you bought your car might not be right after a few years. Review your policy each year during renewal and adjust your deductible if your financial situation or driving habits have changed.

Common Misconceptions About Car Insurance Deductibles

There’s a lot of confusion around deductibles. Let’s clear up some of the most common myths.

Myth 1: “I Pay the Deductible to the Insurance Company”

Not necessarily. In most cases, you pay the deductible directly to the repair shop. The insurer pays the shop the rest. Only in rare cases—like when the insurer sends you a check—do you handle the full amount and then pay the shop.

Myth 2: “All Claims Require a Deductible”

False. Only claims under collision and comprehensive coverage typically involve deductibles. Liability, medical payments, and uninsured motorist claims do not.

Myth 3: “A Higher Deductible Always Saves Money”

Not always. While higher deductibles lower premiums, they increase your financial risk. If you file multiple claims, the savings could be wiped out by out-of-pocket costs. It’s about balance, not just cutting costs.

Myth 4: “I Can Change My Deductible After Filing a Claim”

Generally, no. Deductibles are set when you purchase or renew your policy. You can’t lower it after an accident to reduce your payment. However, you can adjust it during your next renewal period.

Myth 5: “Deductibles Apply to Rental Cars”

Only if you’re using your personal policy to cover a rental. In that case, the same deductibles apply. But if you buy insurance from the rental company, their rules—and deductibles—may differ.

Tips for Managing Your Deductible

Here are some practical tips to help you get the most out of your deductible choice:

- Build an emergency fund: Aim to save at least your deductible amount in a dedicated savings account. This ensures you’re prepared if an accident happens.

- Use disappearing deductible programs: If available, enroll in programs that reduce your deductible over time for safe driving.

- Bundle policies: Some insurers offer discounts if you bundle auto and home insurance, which can offset the cost of a lower deductible.

- Consider usage-based insurance: Programs that track your driving habits may offer discounts that make lower deductibles more affordable.

- Ask about deductible waivers: Some policies waive the deductible if the other driver is uninsured or if you’re not at fault.

Conclusion

Understanding what a deductible in car insurance is—and how it affects your coverage—is essential for making smart financial decisions. It’s not just a number on your policy; it’s a key part of your risk management strategy. By choosing the right deductible, you can save money on premiums while ensuring you’re protected when you need it most.

Remember, there’s no one-size-fits-all answer. The best deductible for you depends on your budget, driving habits, vehicle value, and comfort with risk. Take the time to evaluate your options, compare quotes, and review your policy regularly. With the right approach, you can strike the perfect balance between affordability and protection on the road.

Frequently Asked Questions

What happens if my claim is less than my deductible?

If your repair costs are less than your deductible, your insurance won’t pay anything, and you’ll cover the full amount yourself. For example, a $300 repair with a $500 deductible means no claim payout.

Can I change my deductible after an accident?

No, you generally can’t change your deductible after filing a claim. However, you can adjust it when you renew your policy, usually once per year.

Do deductibles apply to rental cars?

Only if you’re using your personal auto insurance to cover the rental. In that case, your normal deductibles apply. Rental company insurance has its own terms.

Is it better to have a high or low deductible?

It depends on your situation. A high deductible lowers premiums but increases out-of-pocket costs. A low deductible does the opposite. Choose based on your budget and risk tolerance.

Are there any coverages with no deductible?

Yes. Liability, medical payments, uninsured motorist, and some glass repairs often have no deductible. Check your policy for details.

What if I can’t afford to pay my deductible?

Talk to your insurer or repair shop. Some offer payment plans or financing. You can also use a credit card or personal loan, but be mindful of interest rates.