Do You Need a Down Payment to Buy a Car

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Is a Down Payment?

- 4 Can You Buy a Car with No Down Payment?

- 5 Pros and Cons of Making a Down Payment

- 6 How Your Credit Score Affects Down Payment Needs

- 7 Alternatives to Cash Down Payments

- 8 Tips for Deciding Whether to Put Money Down

- 9 Final Thoughts: Is a Down Payment Right for You?

- 10 Frequently Asked Questions

You don’t always need a down payment to buy a car, but skipping one comes with trade-offs. While some lenders offer 100% financing, putting money down can lower your monthly payments, reduce interest costs, and improve loan approval odds—especially if you have less-than-perfect credit.

[FEATURED_IMAGE_PLACEOLDER]

Buying a car is one of the biggest financial decisions most people make—right after purchasing a home. And when it comes to financing that purchase, one of the first questions that pops into your mind is: *Do you need a down payment to buy a car?* The short answer? Not always. But just because you *can* skip the down payment doesn’t mean you *should*.

The truth is, the need for a down payment depends on several factors—your credit score, the type of car you’re buying, the lender’s requirements, and your personal financial goals. Some dealerships and lenders proudly advertise “$0 down” financing, making it seem like you can drive off the lot without spending a dime upfront. And while that’s technically possible, it’s important to understand what you’re really signing up for. Skipping a down payment might get you into a car faster, but it could also lead to higher monthly payments, more interest over the life of the loan, and the risk of owing more than the car is worth—a situation known as being “upside down” on your loan.

So, before you sign on the dotted line, let’s break down everything you need to know about down payments, why they matter, and how to decide what’s best for your situation. Whether you’re a first-time buyer, rebuilding credit, or just trying to stretch your budget, this guide will help you make a smart, informed decision.

Key Takeaways

- A down payment isn’t legally required: Many lenders offer zero-down auto loans, especially for buyers with good credit.

- It reduces your loan amount: Putting money down lowers the total you borrow, which means smaller monthly payments and less interest over time.

- It can improve loan terms: A larger down payment may help you qualify for lower interest rates and better financing deals.

- It helps avoid being “upside down”: Cars depreciate fast—starting with equity protects you from owing more than the car is worth.

- Trade-ins count as down payments: Trading in your current vehicle can reduce or eliminate the need for cash upfront.

- Special programs exist for low-income buyers: Some nonprofits and government-backed loans offer low- or no-down-payment options.

- Weigh the pros and cons: While skipping a down payment preserves cash, it often leads to higher long-term costs.

📑 Table of Contents

What Is a Down Payment?

A down payment is an upfront cash payment made at the time of purchase that reduces the total amount you need to finance. Think of it as your initial investment in the vehicle. For example, if you’re buying a $25,000 car and put down $5,000, you only need to borrow $20,000. That $5,000 comes out of your pocket—or from a trade-in—and lowers your loan balance right from the start.

Down payments are common in many big purchases, like homes and cars, because they reduce the lender’s risk. When you put money down, you have more “skin in the game,” which makes lenders more confident you’ll keep up with payments. This is especially important in the auto industry, where cars lose value quickly—often 20% or more in the first year alone.

But here’s the thing: unlike buying a house, where a down payment is often expected (and sometimes required), car loans are more flexible. Many lenders offer financing with little or no money down, especially if you have strong credit. However, just because it’s available doesn’t mean it’s the best move for your wallet.

How Much Should You Put Down?

There’s no one-size-fits-all answer, but financial experts often recommend putting down at least 10% to 20% of the car’s purchase price. On a $25,000 vehicle, that’s $2,500 to $5,000. This range helps you avoid being upside down on your loan and keeps your monthly payments manageable.

For used cars, the recommendation might be even higher—some advisors suggest 20% or more—because older vehicles depreciate faster and may come with higher interest rates. If you’re buying a luxury or high-end model, a larger down payment can also help offset the steep depreciation that kicks in the moment you drive off the lot.

That said, your ideal down payment amount depends on your budget, credit score, and loan terms. If you’re tight on cash but have excellent credit, you might get away with a smaller down payment and still secure a low interest rate. On the other hand, if your credit needs work, a bigger down payment can help compensate and improve your chances of approval.

Can You Buy a Car with No Down Payment?

Visual guide about Do You Need a Down Payment to Buy a Car

Image source: investopedia.com

Yes—you absolutely can buy a car with no down payment. In fact, it’s more common than you might think. Many dealerships and lenders promote “$0 down” financing as a way to attract buyers, especially during sales events or for new models. These offers are often targeted at people with good to excellent credit, but some programs are available for those with fair or even poor credit.

So how does it work? Instead of paying cash upfront, you finance the entire purchase price of the car—plus taxes, fees, and sometimes even extras like extended warranties or gap insurance. This means your loan amount is higher, your monthly payments are larger, and you’ll pay more in interest over time.

For example, let’s say you buy a $22,000 car with no down payment and finance it over 60 months at a 5% interest rate. Your monthly payment would be around $415. But if you put down $4,000, your loan drops to $18,000, and your monthly payment falls to about $337. Over the life of the loan, you’d save nearly $2,300 in interest just by putting that $4,000 down.

Who Offers No-Down-Payment Loans?

Several types of lenders offer no-down-payment auto loans:

– **Dealership financing:** Many manufacturers’ captive finance arms (like Toyota Financial Services or Ford Credit) run promotional programs with $0 down, especially for new cars.

– **Credit unions:** Some credit unions offer low- or no-down-payment loans to members, particularly if you have a strong relationship with the institution.

– **Online lenders:** Companies like LightStream or Capital One Auto Finance may offer no-down options for qualified borrowers.

– **Subprime lenders:** If your credit is poor, some lenders specialize in high-risk loans with no down payment—but be prepared for high interest rates and strict terms.

While these options can be lifesavers in a pinch, it’s crucial to read the fine print. No-down-payment loans often come with longer loan terms (72 or 84 months), which can trap you in debt for years. And if the car depreciates faster than you pay it off, you could end up owing more than it’s worth—making it hard to sell or trade in later.

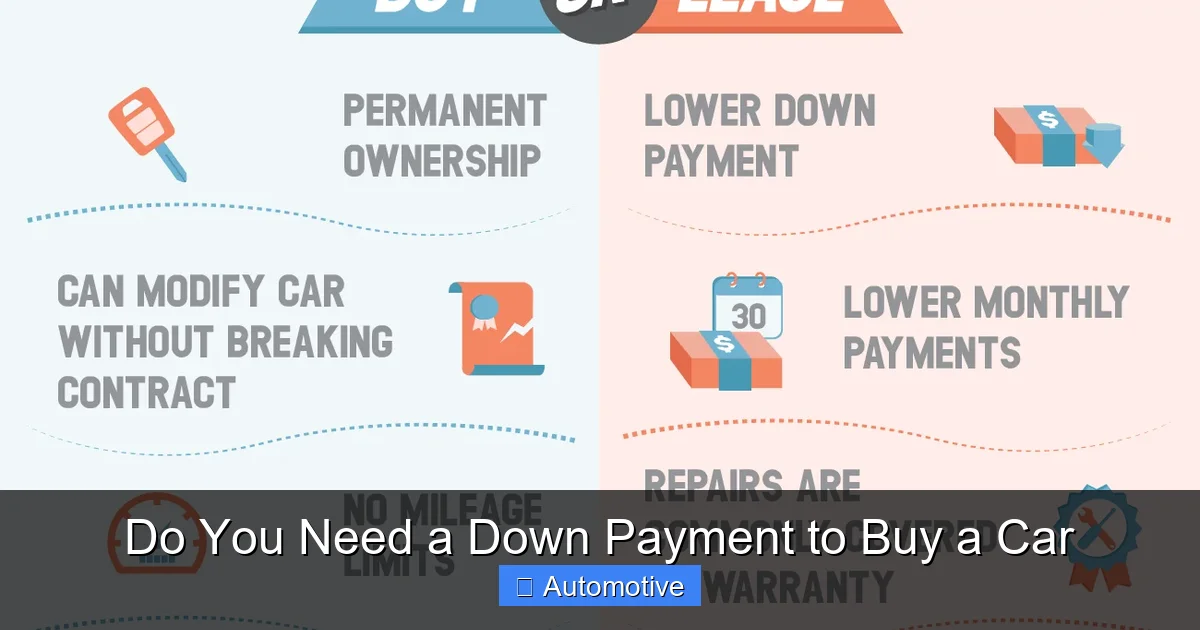

Pros and Cons of Making a Down Payment

Visual guide about Do You Need a Down Payment to Buy a Car

Image source: carpaymentcalculator.net

Like most financial decisions, putting money down on a car comes with both advantages and drawbacks. Let’s look at the key pros and cons so you can decide what’s right for you.

Advantages of a Down Payment

– **Lower monthly payments:** The more you put down, the less you have to borrow, which directly reduces your monthly obligation. This frees up cash for other expenses or savings.

– **Less interest paid:** A smaller loan amount means less interest accrues over time. Even a modest down payment can save you hundreds or thousands of dollars.

– **Better loan approval odds:** Lenders see a down payment as a sign of financial responsibility. If your credit isn’t perfect, a larger down payment can help you qualify for a loan you might otherwise be denied.

– **Lower risk of being upside down:** Cars lose value quickly. Starting with equity means you’re less likely to owe more than the car is worth, which is crucial if you plan to sell or trade it in the future.

– **Access to better rates:** Some lenders offer lower interest rates to buyers who put down 10% or more, especially on used cars.

Disadvantages of a Down Payment

– **Ties up cash:** Money used for a down payment isn’t available for emergencies, investments, or other needs. If you’re living paycheck to paycheck, draining your savings could leave you vulnerable.

– **Opportunity cost:** That $5,000 could potentially grow if invested elsewhere. However, the guaranteed savings from lower interest often outweigh potential investment gains.

– **Not always necessary:** If you have excellent credit and a stable income, you might secure a great rate even with little or no down payment.

The key is balance. If you can afford to put money down without jeopardizing your emergency fund or other financial goals, it’s usually a smart move. But if doing so would leave you cash-strapped, a smaller down payment—or even none at all—might be the better short-term choice.

How Your Credit Score Affects Down Payment Needs

Visual guide about Do You Need a Down Payment to Buy a Car

Image source: everyhome.com

Your credit score plays a huge role in whether you need a down payment—and how much. Lenders use your credit history to assess risk: the higher your score, the more confident they are that you’ll repay the loan.

If you have **excellent credit** (typically 720 or higher), you’ll likely qualify for the best interest rates and may not need a large down payment—or any at all. Many lenders offer competitive terms to high-credit borrowers, including 0% APR financing on new cars.

With **good credit** (660–719), you’ll still have solid options, but you might need a small down payment (5%–10%) to secure the best rates, especially on used vehicles.

If your credit is **fair or poor** (below 660), lenders may require a larger down payment—sometimes 10% to 20% or more—to offset the higher risk. In some cases, you might not qualify for financing at all without a significant down payment or a co-signer.

Improving Your Credit Before Buying

If your score isn’t where you want it, consider taking a few months to improve it before applying for a car loan. Simple steps like paying down credit card balances, disputing errors on your credit report, and avoiding new credit applications can boost your score. Even a 50-point increase could save you thousands in interest over the life of your loan.

And remember: a higher credit score doesn’t just reduce your need for a down payment—it also opens the door to better loan terms, lower rates, and more negotiating power at the dealership.

Alternatives to Cash Down Payments

Not everyone has thousands of dollars sitting in a savings account. The good news? You don’t always need cash to make a down payment. Here are some common alternatives:

Trade-In Your Current Vehicle

One of the most popular ways to reduce or eliminate a down payment is by trading in your current car. The dealership will appraise your vehicle and apply its value toward the purchase of your new one. For example, if your trade-in is worth $8,000 and the new car costs $25,000, you only need to finance $17,000—effectively giving you an $8,000 down payment.

Just be sure to research your car’s value beforehand using tools like Kelley Blue Book or Edmunds. Dealerships may offer less than market value, so knowing your car’s worth helps you negotiate a fair deal.

Use a Gift or Loan from Family

Some buyers receive financial help from family members. While this can be a great way to boost your down payment, make sure everyone understands the terms—especially if it’s a loan, not a gift. Putting it in writing can prevent misunderstandings later.

Tap into Retirement Savings (Carefully)

In rare cases, you might consider borrowing from a 401(k) or withdrawing from a Roth IRA (if you’ve held it for at least five years). However, this comes with risks—like penalties, taxes, and lost investment growth—so it’s usually a last resort.

Look into Special Programs

Certain nonprofits, military organizations, and government-assisted programs offer low- or no-down-payment auto loans for qualifying individuals. For example, the USDA offers vehicle loans for rural residents, and some charities provide cars to low-income families. These programs often have strict eligibility requirements but can be lifesavers for those in need.

Tips for Deciding Whether to Put Money Down

Still unsure? Here are some practical tips to help you decide:

– **Calculate the total cost:** Use an auto loan calculator to compare scenarios with and without a down payment. Look at monthly payments, total interest, and loan term.

– **Assess your cash flow:** Can you comfortably afford a larger monthly payment if you skip the down payment? Or would a smaller payment give you more financial breathing room?

– **Consider your timeline:** If you plan to keep the car for 10+ years, being upside down early might not matter as much. But if you trade cars every 3–5 years, starting with equity is wise.

– **Shop around:** Get pre-approved from multiple lenders (banks, credit unions, online lenders) before visiting the dealership. This gives you leverage and helps you spot the best deal.

– **Negotiate the price first:** Always negotiate the car’s purchase price before discussing financing or down payments. A lower price means you’ll need to borrow less, regardless of your down payment.

Remember, the goal isn’t just to get into a car—it’s to do so in a way that supports your long-term financial health.

Final Thoughts: Is a Down Payment Right for You?

So, do you need a down payment to buy a car? The answer is: it depends. While it’s not a strict requirement, making a down payment—whether in cash, trade-in value, or a combination—offers significant financial benefits. It lowers your loan amount, reduces interest costs, improves your loan terms, and helps you avoid the pitfalls of negative equity.

That said, life happens. If you’re facing an emergency, starting a new job, or simply don’t have the savings yet, a no-down-payment loan might be your best option. Just be sure to understand the trade-offs and plan accordingly.

The most important thing is to go into the car-buying process informed and prepared. Know your credit score, set a realistic budget, and compare financing options from multiple sources. Whether you put $500 or $5,000 down, the right decision is the one that aligns with your financial goals and keeps you on solid ground—both on the road and in your bank account.

Frequently Asked Questions

Do you legally need a down payment to buy a car?

No, there’s no law requiring a down payment to purchase a car. Many lenders offer 100% financing, especially for buyers with good credit. However, skipping a down payment may result in higher monthly payments and more interest over time.

What happens if I don’t make a down payment?

Without a down payment, you’ll finance the full purchase price plus fees and taxes. This increases your loan amount, monthly payments, and total interest paid. You’re also more likely to owe more than the car is worth, especially in the first few years.

Can I use my trade-in as a down payment?

Yes! Trading in your current vehicle counts as a down payment. The dealership will appraise your car and apply its value toward the new purchase, reducing the amount you need to finance.

Is it better to put more money down on a car?

Generally, yes—putting more down lowers your loan balance, reduces interest costs, and helps you avoid being upside down. But don’t drain your emergency fund; aim for a balance that keeps you financially secure.

What if I have bad credit? Do I need a bigger down payment?

Lenders often require a larger down payment (10%–20% or more) for buyers with poor credit to offset the higher risk. A bigger down payment can also improve your chances of loan approval and secure better terms.

Are there programs that help with down payments?

Yes, some nonprofits, military organizations, and government-backed loans offer assistance or low-down-payment options for qualifying individuals, especially those with low income or special circumstances.