Does Gap Insurance Help You Get a New Car

Gap insurance doesn’t directly help you buy a new car, but it can prevent financial loss if your current vehicle is totaled or stolen. By covering the difference between what you owe and the car’s actual value, it protects your credit and frees up resources for your next purchase.

Key Takeaways

- Gap insurance covers the “gap” between your car’s depreciated value and your loan balance. This is crucial if your vehicle is totaled or stolen and your auto insurance payout falls short.

- It does not directly fund a new car purchase. Instead, it prevents you from owing money on a car you no longer have, reducing financial stress.

- Gap insurance is most beneficial for new cars, long-term loans, or low down payments. These scenarios increase the risk of being “upside-down” on your loan.

- You typically need comprehensive and collision coverage to qualify for gap insurance. Most providers require full coverage on the vehicle.

- Gap insurance can be purchased from dealerships, banks, or third-party insurers. Compare options to find the best price and terms.

- If your loan balance is covered, you may receive a small refund. Some policies return a portion of the gap amount to help with your next vehicle.

- Once your loan balance drops below the car’s value, gap insurance becomes unnecessary. Reassess your need for it annually.

📑 Table of Contents

- Does Gap Insurance Help You Get a New Car?

- What Is Gap Insurance and How Does It Work?

- Does Gap Insurance Help You Get a New Car?

- When Is Gap Insurance Worth It?

- When Is Gap Insurance Not Worth It?

- How to Get Gap Insurance

- Tips for Using Gap Insurance Wisely

- Real-Life Example: How Gap Insurance Helped Sarah

- Conclusion

Does Gap Insurance Help You Get a New Car?

So, you’ve just totaled your car in an accident—or worse, it’s been stolen. You’re already stressed about the situation, but then you remember: you still owe $18,000 on your loan, and your auto insurance company only pays out $14,000 because that’s what your car was worth. That leaves you $4,000 in the hole. Ouch.

This is where gap insurance comes in. It’s not a magic ticket to a brand-new ride, but it can be a financial lifesaver when you’re facing a total loss. While gap insurance doesn’t directly help you get a new car, it removes a major financial obstacle that could otherwise delay or derail your next purchase.

In this article, we’ll break down exactly what gap insurance does, when it’s worth it, and how it indirectly supports your ability to move forward—financially and logistically—after a loss. Whether you’re leasing, financing, or just curious about protecting your investment, understanding gap insurance is a smart move.

What Is Gap Insurance and How Does It Work?

Visual guide about Does Gap Insurance Help You Get a New Car

Image source: bankrate.com

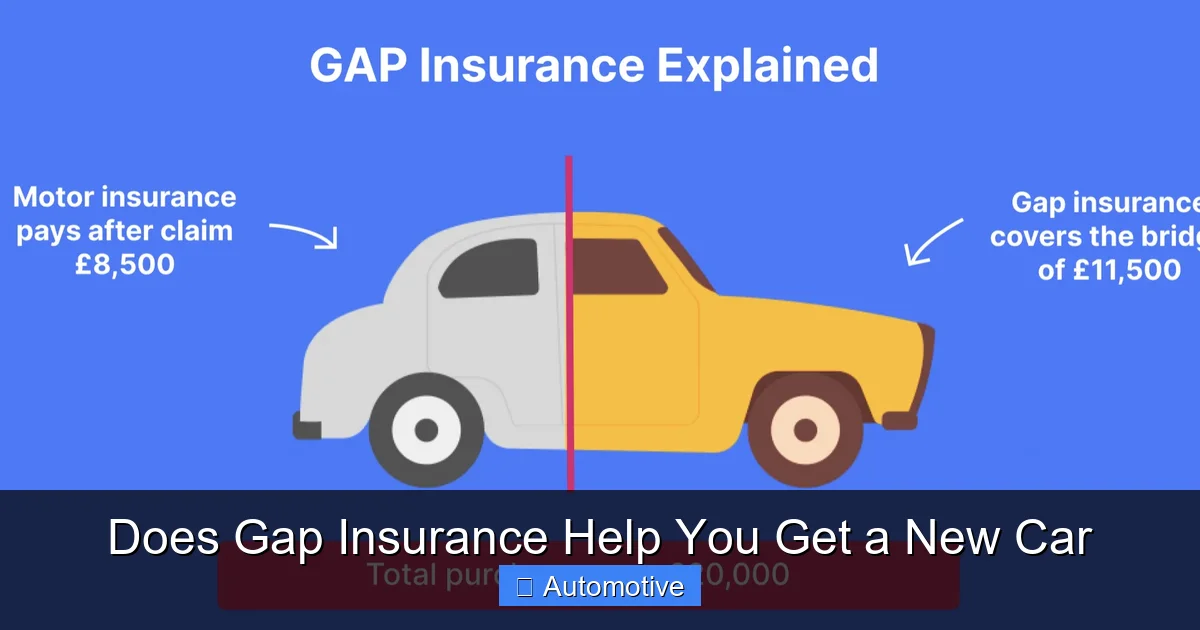

Let’s start with the basics. Gap insurance—short for “guaranteed asset protection” insurance—is a type of coverage designed to protect borrowers when their vehicle is declared a total loss due to an accident, theft, or natural disaster.

Here’s how it works: When you buy a new car, it starts losing value the moment you drive it off the lot. In fact, most new cars depreciate by 20% to 30% in the first year alone. Meanwhile, your loan balance decreases much more slowly, especially if you have a long-term loan (like 60 or 72 months) or made a small down payment.

This creates a “gap” between what your car is worth (its actual cash value) and what you still owe on the loan. If your car is totaled, your standard auto insurance will only pay the car’s current market value—not the full loan amount. That’s where gap insurance steps in.

Example: The $4,000 Gap

Imagine you bought a new SUV for $30,000 with a $3,000 down payment and a 60-month loan. After two years, you’ve paid down the loan to $22,000. But due to depreciation, the car is now worth only $18,000.

If the car is totaled in an accident, your auto insurer will pay $18,000. But you still owe $22,000. That leaves a $4,000 gap.

Without gap insurance, you’d have to pay that $4,000 out of pocket—even though you no longer have the car. With gap insurance, that $4,000 is covered. You walk away debt-free.

When Does Gap Insurance Pay Out?

Gap insurance only kicks in under specific conditions:

- Your vehicle is declared a total loss by your auto insurer (usually when repair costs exceed 70–80% of the car’s value).

- The loss is due to an accident, theft, vandalism, or natural disaster covered under your comprehensive or collision policy.

- You have an active loan or lease on the vehicle.

- You’ve maintained your regular auto insurance coverage (most gap policies require full coverage).

It’s important to note that gap insurance does not cover mechanical breakdowns, routine wear and tear, or missed payments. It’s strictly for total loss scenarios.

Does Gap Insurance Help You Get a New Car?

Visual guide about Does Gap Insurance Help You Get a New Car

Image source: caradviser.co.uk

Now, back to the big question: Does gap insurance help you get a new car?

The short answer: Not directly. But it can make the process of getting your next vehicle much smoother—and far less stressful.

Let’s break this down.

It Removes Financial Liability

The biggest way gap insurance helps is by eliminating the risk of owing money on a car you no longer have. If you’re stuck paying off a loan for a totaled vehicle, that debt can eat into your budget, reduce your credit score, and make it harder to qualify for a new auto loan.

By covering the gap, gap insurance ensures you’re not left with a financial burden. This means you can focus on shopping for your next car instead of scrambling to pay off old debt.

It Protects Your Credit Score

Defaulting on a car loan—even after a total loss—can seriously damage your credit. If you can’t pay the remaining balance, the lender may send the debt to collections, which shows up on your credit report and lowers your score.

A lower credit score can lead to higher interest rates on future loans, making your next car more expensive. Gap insurance helps you avoid this domino effect by ensuring the loan is fully satisfied.

It Frees Up Cash for a Down Payment

Let’s say your gap insurance pays off the remaining $4,000 on your loan. Some policies also offer a small refund—say, $1,000—to help with your next purchase. While this isn’t guaranteed, it’s a nice bonus that can go toward a down payment on a new vehicle.

Even without a refund, not having to pay out of pocket means you can save that money for your next car. Instead of draining your savings to cover a gap, you can use those funds to get a better deal on your next ride.

It Reduces Stress and Speeds Up the Process

Dealing with a totaled car is already stressful. Adding financial uncertainty makes it worse. Gap insurance gives you peace of mind, knowing you won’t be stuck with a big bill.

This emotional relief can help you make smarter, faster decisions about your next car. You’re not rushed into a bad deal because you’re desperate to get out of debt. Instead, you can take your time, shop around, and find a vehicle that fits your budget and needs.

When Is Gap Insurance Worth It?

Visual guide about Does Gap Insurance Help You Get a New Car

Image source: cdn.ramseysolutions.net

Gap insurance isn’t for everyone. It’s most valuable in certain situations. Here’s when it makes the most sense to consider it.

You Bought a New Car

New cars depreciate fast. In the first year, they can lose 20% or more of their value. If you’re financing a new vehicle, especially with a long loan term, you’re likely to be upside-down (owing more than the car is worth) for several years.

For example, a $35,000 new car might be worth only $28,000 after one year. If you owe $32,000, you’re already $4,000 underwater. Gap insurance protects you during this vulnerable period.

You Made a Small or No Down Payment

The less you put down, the longer it takes to build equity in your car. If you financed 100% of the purchase price, you start with zero equity. Even after a year of payments, you might still owe more than the car is worth.

A small down payment increases your risk of being upside-down, making gap insurance a smart safeguard.

You Have a Long Loan Term (60+ Months)

Longer loans mean slower equity buildup. With a 72- or 84-month loan, you’re paying mostly interest in the early years. This means your loan balance decreases slowly while your car’s value drops quickly.

For instance, on a 72-month loan, you might still owe 70% of the original amount after three years—while the car is worth only 50%. That’s a big gap.

You Leased Your Vehicle

Leased cars also depreciate rapidly, and lease agreements often require gap coverage. If your lease doesn’t include it, adding gap insurance can protect you from owing thousands if the car is totaled.

Some leasing companies include gap coverage in the lease price, so check your contract before buying extra.

You Drive a High-Depreciation Vehicle

Certain cars lose value faster than others. Luxury vehicles, electric cars, and models with high mileage or poor reliability ratings tend to depreciate quickly.

If you’re driving a car known for rapid depreciation, gap insurance offers extra protection.

When Is Gap Insurance Not Worth It?

Gap insurance isn’t always necessary. Here are situations where you might skip it.

You Have a Short Loan Term (36 or 48 Months)

With a shorter loan, you build equity faster. You’re less likely to be upside-down, especially if you made a decent down payment.

For example, on a 36-month loan with a $5,000 down payment, you might owe less than the car is worth after just one year.

You Made a Large Down Payment

If you put 20% or more down, you start with significant equity. This reduces the risk of owing more than the car is worth.

A $7,000 down payment on a $35,000 car means you only finance $28,000. Even with depreciation, you’re less likely to be underwater.

Your Car Is Older or Has High Mileage

Used cars depreciate more slowly than new ones. If you bought a 3-year-old car with 40,000 miles, it’s already taken the biggest depreciation hit.

In this case, your loan balance is more likely to stay below the car’s value, making gap insurance less necessary.

You’re Close to Paying Off Your Loan

Once your loan balance drops below the car’s market value, you’re no longer upside-down. At that point, gap insurance offers little benefit.

Check your loan balance and car value annually. If you’re no longer in the gap, you can cancel the coverage.

How to Get Gap Insurance

If you decide gap insurance is right for you, here’s how to get it.

Buy It from the Dealership

Many car dealers offer gap insurance at the time of purchase. It’s convenient, but often more expensive than other options.

Dealership gap insurance can cost $500 to $1,000 or more, rolled into your loan. While it’s easy to add, it increases your monthly payment and total interest.

Get It from Your Bank or Credit Union

If you financed your car through a bank or credit union, ask if they offer gap insurance. These policies are often cheaper than dealer options and can be added to your existing loan.

Purchase from a Third-Party Insurer

Some insurance companies sell standalone gap insurance. You can buy it separately from your auto policy.

Third-party gap insurance is usually the most affordable option. Compare quotes from multiple providers to find the best deal.

Check If You Already Have It

Some auto insurance policies include gap coverage, especially for leased vehicles. Review your policy or call your insurer to confirm.

Also, some credit cards offer gap protection if you used the card to finance part of the purchase. Check your card benefits.

Tips for Using Gap Insurance Wisely

To get the most out of gap insurance, follow these tips.

Read the Fine Print

Not all gap policies are the same. Some cover only the loan balance, while others include a refund or rental car reimbursement.

Make sure you understand what’s covered, any exclusions, and how to file a claim.

Keep Your Auto Insurance Active

Most gap policies require you to maintain comprehensive and collision coverage. If you let your auto insurance lapse, your gap insurance may be void.

File Your Claim Promptly

If your car is totaled, contact your gap insurer as soon as your auto claim is settled. Delays can complicate the process.

Reassess Annually

As your loan balance decreases and your car ages, your need for gap insurance changes. Review your situation each year and cancel the policy if it’s no longer needed.

Don’t Double Up

You don’t need multiple gap policies. If you already have coverage through your lease or auto insurer, don’t buy another one.

Real-Life Example: How Gap Insurance Helped Sarah

Let’s look at a real-world scenario.

Sarah bought a new sedan for $28,000 with a $2,000 down payment and a 60-month loan. After 18 months, she was in a minor accident. The repair estimate came in at $20,000—more than 75% of the car’s value. Her insurer declared it a total loss.

At that point, Sarah owed $23,500 on her loan. Her auto insurance paid $19,000 based on the car’s current value. That left a $4,500 gap.

Luckily, Sarah had purchased gap insurance from her credit union for $400. The gap insurer covered the $4,500, and even gave her a $500 refund to help with her next car.

Without gap insurance, Sarah would have had to pay $4,500 out of pocket. Instead, she used the $500 refund as part of her down payment on a new hybrid. She also avoided damage to her credit and financial stress.

Gap insurance didn’t buy her a new car—but it made getting one possible.

Conclusion

So, does gap insurance help you get a new car? Not directly. But it plays a crucial role in protecting your finances after a total loss, which in turn makes it easier to move forward and purchase your next vehicle.

By covering the difference between your loan balance and your car’s value, gap insurance prevents you from owing money on a car you no longer have. It protects your credit, reduces stress, and can even free up cash for a down payment.

It’s most valuable for new cars, long-term loans, small down payments, and high-depreciation vehicles. But if you have a short loan, large down payment, or older car, it may not be necessary.

The key is to assess your risk, compare options, and make an informed decision. Gap insurance isn’t a requirement, but for many drivers, it’s a smart investment in peace of mind.

When disaster strikes, you’ll be glad you had it.

Frequently Asked Questions

Does gap insurance pay for a new car?

No, gap insurance does not pay for a new car. It only covers the difference between your loan balance and your car’s actual cash value if it’s totaled or stolen. It helps you avoid debt, but doesn’t fund your next purchase.

Can I buy gap insurance after I purchase my car?

Yes, in most cases. You can usually buy gap insurance within 30 to 60 days of your car purchase, depending on the provider. Some lenders or insurers may allow later enrollment, but it’s best to act quickly.

Is gap insurance required?

No, gap insurance is not legally required. However, some leasing companies or lenders may require it, especially for long-term loans or low down payments. Always check your loan or lease agreement.

Does gap insurance cover theft?

Yes, most gap insurance policies cover theft if your comprehensive auto insurance also covers it. If your car is stolen and not recovered, gap insurance can cover the loan gap after your insurer pays the car’s value.

Can I cancel gap insurance?

Yes, you can usually cancel gap insurance once your loan balance drops below your car’s value. Contact your provider to cancel and possibly receive a refund for unused coverage.

Does gap insurance cover mechanical failures?

No, gap insurance only covers total losses due to accidents, theft, or natural disasters. It does not cover mechanical breakdowns, maintenance issues, or wear and tear.