What State Does Not Require Car Insurance?

Only one U.S. state—Virginia—does not legally require drivers to carry traditional car insurance, but it’s not a free pass. Instead, Virginia offers an alternative through a $500 uninsured motor vehicle fee and proof of financial responsibility. Drivers must still meet strict liability requirements or face serious penalties.

Key Takeaways

- Virginia is the only state that does not require traditional car insurance: Drivers can opt out by paying a $500 uninsured motor vehicle fee and showing proof of financial responsibility.

- Financial responsibility is still mandatory: Even without insurance, drivers must be able to cover damages in an at-fault accident, typically through bonds, cash deposits, or self-insurance.

- Penalties for non-compliance are severe: Driving without meeting Virginia’s requirements can lead to license suspension, fines, and vehicle registration revocation.

- Most states require liability insurance: All other 49 states mandate minimum liability coverage to legally operate a vehicle on public roads.

- Self-insurance is an option in some states: High-net-worth individuals or fleet owners may qualify to self-insure, but this requires significant assets and state approval.

- Choosing to go uninsured is risky: Without insurance, you’re personally liable for all damages, medical bills, and legal fees after an accident.

- Alternatives like pay-per-mile or non-owner policies exist: These can offer flexible, low-cost coverage for drivers who don’t need full-time insurance.

📑 Table of Contents

What State Does Not Require Car Insurance?

When it comes to driving in the United States, car insurance is a legal necessity—almost everywhere. In fact, 49 out of 50 states require drivers to carry at least a minimum amount of liability insurance to legally operate a vehicle. This insurance helps cover damages or injuries you might cause to others in an accident. But what about the one state that stands out from the rest? That state is Virginia, and it’s the only place in the country where you can legally drive without traditional car insurance—if you follow specific rules.

Now, before you start planning a road trip to Virginia to cancel your policy, it’s important to understand what “not requiring car insurance” really means. Virginia doesn’t give drivers a free pass to drive uninsured with no consequences. Instead, it offers an alternative path: paying a fee and proving you can cover potential damages out of pocket. This system is designed to ensure financial responsibility, even if you don’t have an insurance policy. So while Virginia may not mandate insurance, it still holds drivers accountable for their actions on the road.

In this article, we’ll explore how Virginia’s unique approach works, what the alternatives are, and why most experts still recommend carrying insurance—even if it’s not legally required. We’ll also look at how other states handle financial responsibility, the risks of driving uninsured, and smart ways to save on coverage without breaking the law. Whether you’re a Virginia resident or just curious about auto insurance laws, this guide will give you the full picture.

Understanding Financial Responsibility Laws

Visual guide about What State Does Not Require Car Insurance?

Image source: hughesandcoleman.com

Before diving into Virginia’s exception, it’s helpful to understand the broader concept of financial responsibility laws. These laws exist in every state and are designed to ensure that drivers can pay for damages they cause in an accident. In most states, the way to meet this requirement is by purchasing liability car insurance. This type of insurance covers bodily injury and property damage that you may cause to others. For example, if you rear-end another car and the driver needs medical treatment, your liability insurance would help cover those costs.

But insurance isn’t the only way to meet financial responsibility. Some states allow alternatives like posting a bond, depositing cash with the state, or qualifying for self-insurance—especially for large fleets or high-net-worth individuals. These options are rare and often come with strict requirements, but they prove that the goal isn’t necessarily to force everyone into an insurance policy. The real goal is accountability. The state wants to know that if you cause an accident, someone will pay the bills—whether it’s an insurance company or you personally.

Virginia takes this idea a step further by making insurance optional, as long as you pay a fee and prove you can cover potential claims. This approach reflects a belief in personal responsibility over mandatory coverage. However, it also shifts the risk entirely onto the driver. If you cause a serious accident and don’t have insurance, you could be on the hook for tens or even hundreds of thousands of dollars in damages. That’s why, even in Virginia, most drivers still choose to buy insurance—it’s simply the safer and more practical option.

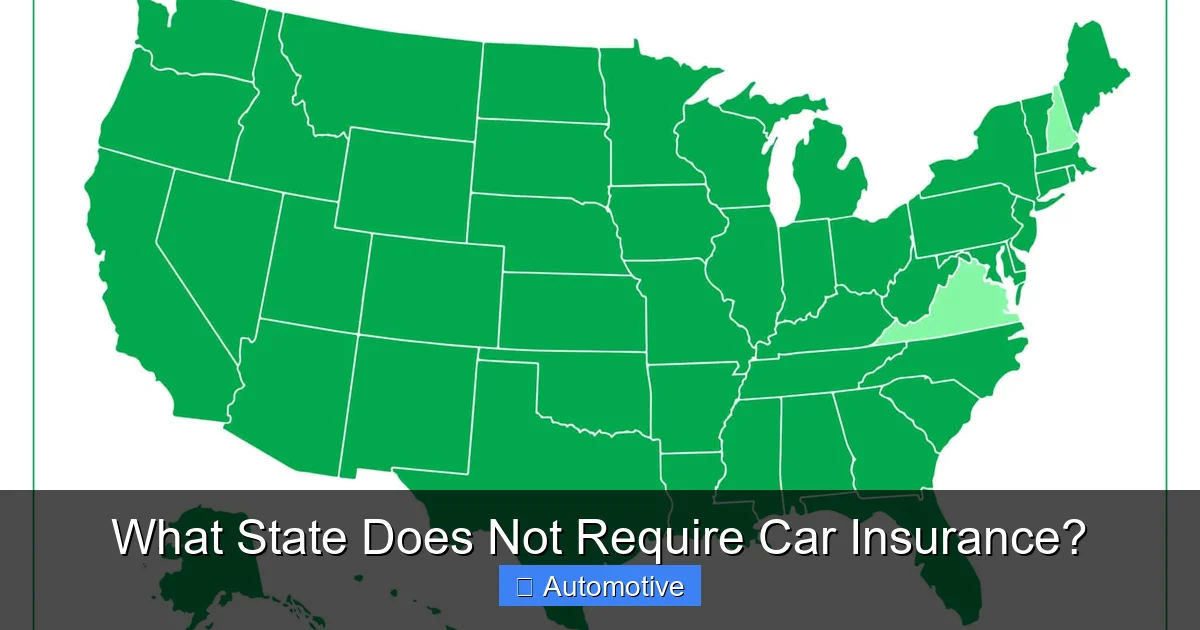

Virginia: The Only State Without a Mandatory Insurance Law

Visual guide about What State Does Not Require Car Insurance?

Image source: carinsurancecomparison.com

Virginia is the only state in the U.S. that does not require drivers to carry traditional car insurance. This unique policy has been in place since 1975, when the state legislature passed a law allowing drivers to opt out of insurance if they met certain conditions. Instead of buying a policy, drivers can pay a $500 uninsured motor vehicle (UMV) fee to the Virginia Department of Motor Vehicles (DMV) each year. This fee is not insurance—it doesn’t cover any damages or injuries. It simply allows you to legally register and drive a vehicle without a policy.

But here’s the catch: paying the fee doesn’t absolve you of financial responsibility. You must still prove that you can cover damages if you cause an accident. This usually means showing proof of sufficient assets—like savings, investments, or property—that could be used to pay claims. The DMV may require documentation such as bank statements or asset valuations. If you can’t prove financial stability, you won’t be allowed to register your vehicle without insurance.

It’s also important to note that the $500 fee applies per vehicle. So if you own two cars, you’d need to pay $1,000 annually to go uninsured. And if you cause an accident, the other party can still sue you for damages. Without insurance, you’d have to pay out of pocket—or risk losing your assets in a lawsuit. That’s why, despite the legal option, over 90% of Virginia drivers still choose to carry insurance. It’s simply too risky to go without.

How the Virginia UMV Fee Works

The uninsured motor vehicle fee is paid directly to the Virginia DMV when you register your vehicle. You’ll see it listed as an option during the registration process, alongside the standard insurance requirement. If you select the UMV fee, you’ll be asked to sign a statement acknowledging that you understand the risks of driving without insurance. You’ll also need to provide proof of financial responsibility, which the DMV reviews before approving your registration.

The fee is non-refundable and must be paid every year when you renew your registration. If you decide later that you want to switch to insurance, you can do so at any time—just provide proof of coverage to the DMV. However, if you stop paying the fee or fail to maintain financial responsibility, your registration can be suspended, and you could face additional penalties.

Who Should Consider the UMV Option?

The UMV fee is generally only practical for a small group of people: those with significant assets who are confident they can cover any potential claims. For example, a wealthy individual with multiple properties and substantial savings might feel comfortable going uninsured. But for the average driver, the risk far outweighs the $500 savings. A single at-fault accident could result in damages far exceeding that amount—especially if someone is seriously injured.

Additionally, some drivers may mistakenly think the UMV fee protects them from lawsuits. It doesn’t. If you cause an accident, the injured party can still take legal action against you. Without insurance, you’ll have no legal defense or financial backup. That’s why financial advisors and insurance experts almost universally recommend carrying coverage, even in Virginia.

Penalties for Non-Compliance in Virginia

Visual guide about What State Does Not Require Car Insurance?

Image source: d2tez01fe91909.cloudfront.net

While Virginia allows drivers to go without insurance, failing to meet the state’s requirements can lead to serious consequences. If you choose the UMV fee but can’t prove financial responsibility, your vehicle registration will be denied or revoked. Driving with a suspended registration is illegal and can result in fines, court appearances, and even impoundment of your vehicle.

If you’re caught driving without insurance and without paying the UMV fee, the penalties are even harsher. First-time offenders may face a fine of up to $500, a 30-day license suspension, and a requirement to file an SR-22 form (proof of future insurance) for three years. Repeat offenses can lead to higher fines, longer suspensions, and mandatory jail time in extreme cases.

These penalties are designed to discourage drivers from flouting the rules. Even though insurance isn’t mandatory, the state still expects accountability. And if you cause an accident while uninsured and unable to pay damages, the legal and financial fallout can be devastating.

Real-Life Example: The Cost of Going Uninsured

Imagine you’re driving in Virginia and choose to pay the $500 UMV fee instead of buying insurance. A few months later, you run a red light and collide with another vehicle. The other driver suffers a broken leg and needs surgery, totaling $75,000 in medical bills. Their car is totaled, adding another $25,000 in property damage.

Without insurance, you’re personally responsible for all $100,000 in damages. If you don’t have the assets to cover it, the other party can sue you. If the court rules in their favor, your wages could be garnished, or your assets seized. In contrast, a basic liability policy with $100,000 in coverage would have handled these costs automatically—protecting your finances and your future.

How Other States Handle Car Insurance Requirements

While Virginia is the only state without a mandatory insurance law, every other state requires drivers to carry at least minimum liability coverage. These requirements vary by state but typically include:

– Bodily Injury Liability: Covers medical expenses for others if you’re at fault.

– Property Damage Liability: Covers damage to another person’s vehicle or property.

For example, California requires drivers to carry at least $15,000 in bodily injury coverage per person, $30,000 per accident, and $5,000 in property damage coverage. New York has higher minimums: $25,000/$50,000 for bodily injury and $10,000 for property damage. These minimums are often referred to as “25/50/10” or similar formats.

Some states also require additional coverage, such as uninsured motorist protection or personal injury protection (PIP). These help cover your own medical expenses or protect you if you’re hit by an uninsured driver.

States with Alternative Financial Responsibility Options

A few states offer alternatives to traditional insurance, though they’re rarely used. For example:

– **New Hampshire** technically doesn’t require insurance, but only if you can prove financial responsibility. In practice, almost all drivers buy insurance because proving financial responsibility is difficult and risky.

– **Mississippi** allows self-insurance for individuals with a net worth over $1 million, but the process is complex and requires state approval.

– **Alaska** permits cash deposits or bonds as proof of financial responsibility, but again, this is uncommon.

These options are typically reserved for wealthy individuals or large companies with fleets. For the average driver, purchasing insurance remains the simplest and safest way to comply with the law.

The Risks of Driving Without Insurance

Even in states where it’s technically legal to go without insurance, doing so is incredibly risky. Here are some of the biggest dangers:

– **Personal Financial Liability:** If you cause an accident, you’re responsible for all damages. Medical bills, vehicle repairs, and legal fees can quickly add up to tens or hundreds of thousands of dollars.

– **Lawsuits:** Injured parties can sue you for damages beyond what insurance would cover. Without a policy, you have no legal defense team or financial backing.

– **License and Registration Suspension:** Most states will suspend your driving privileges if you’re caught without insurance or proof of financial responsibility.

– **Higher Future Premiums:** If you later decide to buy insurance, insurers may charge you higher rates due to your lapse in coverage.

– **Difficulty Renting Cars or Getting Loans:** Many rental car companies and lenders require proof of insurance. Going uninsured can limit your options.

Tips for Staying Protected Without Breaking the Bank

If you’re looking to save on car insurance, there are smarter ways than going uninsured:

– **Shop Around:** Compare quotes from multiple insurers to find the best rate.

– **Raise Your Deductible:** A higher deductible lowers your premium, but make sure you can afford to pay it if you file a claim.

– **Take Advantage of Discounts:** Many insurers offer discounts for safe driving, good grades (for students), bundling policies, or installing safety features.

– **Consider Usage-Based Insurance:** Programs like Progressive’s Snapshot or Allstate’s Drivewise track your driving habits and reward safe behavior with lower rates.

– **Look into Non-Owner Policies:** If you don’t own a car but drive occasionally, a non-owner policy provides liability coverage at a lower cost.

Conclusion

So, what state does not require car insurance? The answer is Virginia—but with a big asterisk. While Virginia allows drivers to opt out of traditional insurance by paying a $500 fee and proving financial responsibility, this option is far from risk-free. The vast majority of drivers still choose to carry coverage because the potential costs of an accident far outweigh the savings.

Every other state requires some form of liability insurance, and for good reason: it protects drivers, passengers, and other road users. Even in states with alternative options, like self-insurance or cash deposits, the barriers are high and the risks are real.

Ultimately, car insurance isn’t just about following the law—it’s about protecting your financial future. A single accident can lead to devastating consequences if you’re not prepared. Whether you live in Virginia or anywhere else in the U.S., carrying adequate insurance is one of the smartest decisions you can make as a driver.

So before you consider going uninsured, weigh the risks carefully. Talk to an insurance agent, review your assets, and think about what you’d do if you caused a serious accident. In most cases, the peace of mind that comes with a good insurance policy is worth every penny.

Frequently Asked Questions

Is it legal to drive without car insurance in any state?

Yes, but only in Virginia—and even there, you must pay a $500 uninsured motor vehicle fee and prove financial responsibility. All other states require at least minimum liability insurance to legally drive.

What happens if I drive without insurance in Virginia?

If you don’t pay the UMV fee or can’t prove financial responsibility, your vehicle registration can be suspended. If you’re caught driving illegally, you may face fines, license suspension, and legal liability for any damages you cause.

Can I sue someone who caused an accident but has no insurance?

Yes, you can sue an uninsured driver for damages. However, collecting payment may be difficult if they lack assets or income. That’s why uninsured motorist coverage is important—it protects you in these situations.

Are there any other states that don’t require car insurance?

No. Virginia is the only state without a mandatory insurance law. New Hampshire technically doesn’t require it, but drivers must still prove financial responsibility, which is rarely done without insurance.

What is the $500 UMV fee in Virginia?

The uninsured motor vehicle fee is a yearly payment to the Virginia DMV that allows you to register a vehicle without insurance. It does not provide any coverage—it only permits legal registration if you can prove financial responsibility.

Is it smart to go uninsured to save money?

Generally, no. The potential costs of an at-fault accident far exceed the savings from avoiding insurance. Most financial experts recommend carrying at least minimum liability coverage to protect your assets and future.