How Much Is Car Insurance in Pennsylvania?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 Understanding Pennsylvania’s Car Insurance Requirements

- 4 Average Car Insurance Costs in Pennsylvania

- 5 Factors That Affect Your Car Insurance Premium in PA

- 6 How to Save Money on Car Insurance in Pennsylvania

- 7 Pennsylvania-Specific Tips and Considerations

- 8 Final Thoughts: Finding the Right Balance

- 9 Frequently Asked Questions

Car insurance in Pennsylvania costs an average of $1,400 to $2,000 per year for full coverage, though rates vary widely based on location, driving history, and coverage choices. Understanding state requirements and shopping around can help you find affordable, reliable protection.

If you’re driving in the Keystone State, you’ve probably asked yourself: *How much is car insurance in Pennsylvania?* It’s a fair question—and one that doesn’t have a one-size-fits-all answer. Car insurance costs in PA depend on a mix of state regulations, personal factors, and where you live. But don’t worry—we’re here to break it all down so you can understand what you’re paying for and how to get the best deal.

Pennsylvania operates under a “choice” no-fault insurance system, which means you can choose between limited tort (lower premiums, restricted lawsuit rights) or full tort (higher premiums, full legal rights after an accident). This unique setup affects both your coverage options and your bottom line. On top of that, Pennsylvania has specific minimum coverage requirements that every driver must meet—but many opt for more robust protection to avoid financial risk.

Whether you’re a new driver in Harrisburg, a commuter in Pittsburgh, or a retiree cruising through the Poconos, knowing how car insurance works in PA—and what it really costs—can save you money and stress. In this guide, we’ll walk you through average rates, key factors that influence pricing, state-specific rules, and practical tips to lower your premium without sacrificing coverage.

Key Takeaways

- Average annual premiums: Full coverage in Pennsylvania averages $1,600–$2,000, while minimum liability coverage costs around $600–$900 per year.

- State requirements: PA mandates minimum liability coverage of 15/30/5 (bodily injury and property damage), plus optional add-ons like first-party benefits.

- Location matters: Urban areas like Philadelphia and Pittsburgh have higher rates due to traffic density and theft rates compared to rural counties.

- Driver profile impacts cost: Age, credit score, driving record, and vehicle type significantly influence your premium—young drivers and those with accidents pay more.

- Shop around annually: Comparing quotes from at least three insurers can save hundreds; companies like State Farm, Geico, and Erie often offer competitive PA rates.

- Discounts add up: Safe driver, multi-policy, good student, and low-mileage discounts can reduce your bill by 10–30%.

- Consider usage-based programs: Telematics programs like Progressive’s Snapshot or Allstate’s Drivewise reward safe driving with lower premiums.

📑 Table of Contents

Understanding Pennsylvania’s Car Insurance Requirements

Before diving into costs, it’s essential to know what Pennsylvania law requires from drivers. Unlike some states that use a pure no-fault system, Pennsylvania gives you a choice—but that choice comes with trade-offs.

Minimum Liability Coverage

Every driver in Pennsylvania must carry at least the following liability limits:

- $15,000 for bodily injury per person

- $30,000 for bodily injury per accident

- $5,000 for property damage

This is often written as 15/30/5. These amounts cover damages you cause to others if you’re at fault in an accident. However, they do not cover your own injuries or vehicle repairs—that’s where additional coverage comes in.

First-Party Benefits (FPB)

Pennsylvania also requires drivers to carry First-Party Benefits, which pay for your medical expenses regardless of who caused the crash. The minimum FPB is $5,000, but you can increase this up to $100,000 or more. This coverage includes:

- Medical expenses

- Lost wages (up to 80% of income, max $2,500/month)

- Funeral costs

- Replacement services (like childcare or housekeeping)

Because PA is a no-fault state, your own insurance pays these benefits first—even if the other driver was at fault.

Tort Option: Limited vs. Full

Here’s where Pennsylvania stands out: you must choose between limited tort and full tort when buying insurance.

- Limited tort: Costs less but restricts your right to sue for pain and suffering unless the injury is severe (e.g., death, disfigurement, permanent loss).

- Full tort: Costs more (typically 10–25% higher) but preserves your right to sue for non-economic damages after an accident.

Most Pennsylvanians choose limited tort to save money—but if you value legal flexibility, full tort may be worth the extra cost.

Uninsured/Underinsured Motorist Coverage (UM/UIM)

While not mandatory, UM/UIM coverage is highly recommended. It protects you if you’re hit by a driver with no insurance or insufficient coverage. Given that nearly 12% of Pennsylvania drivers are uninsured (above the national average), this add-on can be a financial lifesaver.

Average Car Insurance Costs in Pennsylvania

So, how much is car insurance in Pennsylvania, really? Let’s look at real-world averages based on recent data from sources like the National Association of Insurance Commissioners (NAIC), Quadrant Information Services, and consumer surveys.

Statewide Averages

For a typical 35-year-old driver with a clean record and full coverage (liability, collision, comprehensive), the average annual premium in Pennsylvania is approximately $1,750. That breaks down to about $146 per month.

Visual guide about How Much Is Car Insurance in Pennsylvania?

Image source: carinsurance.org

If you only carry the state minimum (15/30/5 liability + $5,000 FPB), your annual cost drops to around $750, or $62 per month. However, this minimal coverage leaves significant gaps in protection.

Cost by Age and Gender

Young drivers pay significantly more. A 17-year-old male in Pennsylvania might pay over $4,000 annually for full coverage, while a 17-year-old female pays slightly less—around $3,600. Rates begin to drop steadily after age 25.

For seniors (65+), premiums stabilize but may rise again due to age-related risk factors. A 70-year-old driver with a clean record might pay around $1,500 per year for full coverage.

Cost by Location

Where you live in Pennsylvania has a major impact on your rate. Urban areas with high traffic, crime, and accident rates see higher premiums.

- Philadelphia: Average full coverage = $2,200/year

- Pittsburgh: Average full coverage = $1,900/year

- Allentown: Average full coverage = $1,800/year

- State College: Average full coverage = $1,400/year

- Rural counties (e.g., Potter, Cameron): Average full coverage = $1,200/year

Even within cities, ZIP codes matter. A driver in Northeast Philly might pay 20% more than someone in the suburbs of Montgomery County.

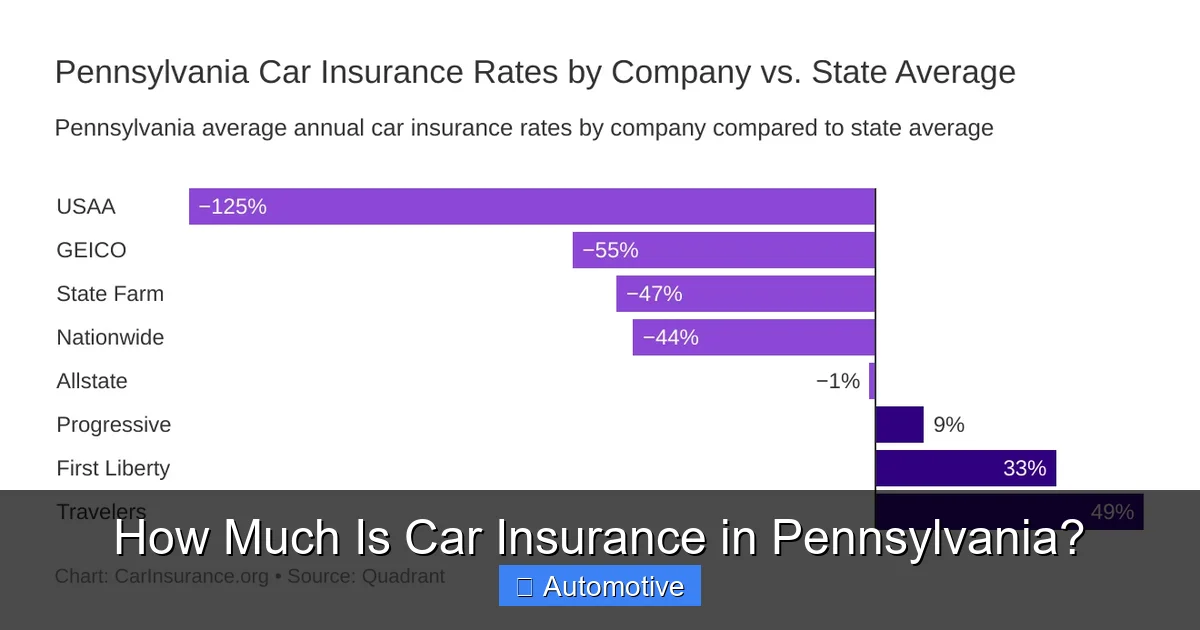

Cost by Insurance Company

Not all insurers charge the same—even for identical coverage. Here are average annual full-coverage premiums from top providers in PA:

- Erie Insurance: $1,300

- State Farm: $1,500

- Geico: $1,600

- Progressive: $1,700

- Allstate: $1,850

- Nationwide: $1,750

Erie consistently ranks as one of the most affordable options in Pennsylvania, especially for safe drivers and those with bundled policies.

Factors That Affect Your Car Insurance Premium in PA

Your car insurance rate isn’t random—it’s calculated using a complex algorithm that weighs dozens of variables. Understanding these factors can help you control your costs.

Driving Record

Your history behind the wheel is one of the biggest determinants of your rate. A clean record = lower premiums. But accidents, tickets, and DUIs can spike your cost significantly.

Visual guide about How Much Is Car Insurance in Pennsylvania?

Image source: general.com

- A single at-fault accident can increase your premium by 20–50%.

- A speeding ticket might add $100–$300 per year.

- A DUI conviction can double your rate—or lead to non-renewal.

Example: A driver with a clean record pays $1,600/year. After a fender bender, their rate jumps to $2,200. After a DUI? It could exceed $3,500.

Credit Score

Pennsylvania allows insurers to use credit-based insurance scores to set rates—and it makes a big difference. Drivers with excellent credit (750+) often pay 20–30% less than those with poor credit (below 600).

Why? Studies show a correlation between credit history and claim frequency. Insurers see lower-risk drivers as more financially responsible.

Tip: Check your credit report annually and dispute errors. Even improving your score by 50 points can lower your premium.

Vehicle Type

The car you drive affects your rate. Sports cars, luxury vehicles, and models with high theft rates cost more to insure.

- Safe, affordable sedans (e.g., Honda Accord, Toyota Camry): Lower premiums

- SUVs and minivans (e.g., Honda CR-V, Toyota Sienna): Moderate rates

- Luxury and performance vehicles (e.g., BMW, Mercedes, Mustang): Higher premiums due to repair costs and theft risk

Newer cars may cost more to insure due to higher replacement value, but they often qualify for safety discounts (e.g., automatic emergency braking, lane departure warnings).

Annual Mileage

The more you drive, the higher your risk of an accident. Insurers ask for your annual mileage—and low-mileage drivers (under 7,500 miles/year) often qualify for discounts.

If you work from home or use public transit, be sure to report accurate mileage. Some insurers offer “low-mileage” or “pleasure-use” discounts that can save you 5–15%.

Coverage Level and Deductibles

Higher coverage limits and lower deductibles mean higher premiums. For example:

- Choosing a $500 deductible instead of $1,000 can increase your collision/comprehensive premium by 15–25%.

- Increasing liability limits from 15/30/5 to 100/300/100 can add $200–$400 per year but offers far better protection.

Balance affordability with risk. If you have significant assets, higher liability limits are wise to protect against lawsuits.

How to Save Money on Car Insurance in Pennsylvania

The good news? There are many ways to reduce your car insurance bill without cutting essential coverage.

Shop Around Every Year

Insurance companies change their pricing models frequently. A provider that was cheap last year might not be this year. Get quotes from at least three insurers annually.

Visual guide about How Much Is Car Insurance in Pennsylvania?

Image source: americaninsurance.com

Use online comparison tools or work with an independent agent who represents multiple companies. Don’t forget regional insurers like Erie or Donegal—they often offer better rates than national brands in PA.

Bundle Your Policies

Most insurers offer a multi-policy discount (typically 10–25%) if you bundle auto with home, renters, or umbrella insurance. For example, bundling a $1,600 auto policy with a $1,000 home policy could save you $400/year.

Maintain a Clean Driving Record

Safe driving isn’t just smart—it’s profitable. Many insurers offer accident forgiveness or safe driver discounts after three to five claim-free years.

Some companies also offer defensive driving course discounts (usually 5–10%) for completing an approved course. Pennsylvania allows this for drivers 55 and older, but some insurers extend it to all ages.

Take Advantage of Discounts

Ask your insurer about every discount you might qualify for. Common ones in PA include:

- Good student discount: For full-time students with a B average or higher

- Military discount: For active-duty, veterans, and family members

- Low-mileage discount: For driving under 7,500 miles/year

- Anti-theft device discount: For vehicles with alarms or tracking systems

- Paperless billing & auto-pay discount: Often 5–10% for going digital

Stacking multiple discounts can reduce your premium by 20% or more.

Consider Usage-Based Insurance

Telematics programs like Progressive’s Snapshot, Allstate’s Drivewise, or State Farm’s Drive Safe & Save monitor your driving habits via a mobile app or plug-in device.

If you drive safely—avoiding hard braking, speeding, and late-night trips—you can earn discounts of 10–30%. Some programs even offer immediate savings just for signing up.

Example: A Pittsburgh driver saved $320/year after six months in Snapshot by maintaining smooth, consistent driving.

Raise Your Deductible (Carefully)

Increasing your collision and comprehensive deductible from $500 to $1,000 can save you $100–$200 per year. But only do this if you have enough savings to cover the higher out-of-pocket cost if you file a claim.

Tip: Set aside the annual savings in a dedicated “car repair fund” so you’re prepared.

Pennsylvania-Specific Tips and Considerations

Beyond general savings strategies, Pennsylvania drivers should keep a few state-specific factors in mind.

No-Fault System Nuances

Because PA is a no-fault state, your own insurance covers your medical bills first—even if the other driver caused the crash. This can speed up claims but also means your insurer may pursue reimbursement from the at-fault party (subrogation).

If you choose limited tort, remember: you can still sue for economic damages (medical bills, lost wages) but not for pain and suffering unless your injury meets the state’s “serious injury” threshold.

High Uninsured Motorist Risk

With over 1 in 10 Pennsylvania drivers uninsured, adding UM/UIM coverage is smart. A typical UM/UIM policy with 100/300 limits adds $100–$200 per year but can pay for medical bills, lost wages, and pain and suffering if you’re hit by an uninsured driver.

Winter Driving and Weather Risks

Pennsylvania winters bring snow, ice, and increased accident risk. While you can’t control the weather, you can:

- Install winter tires (some insurers offer discounts)

- Park in a garage to reduce comprehensive claims (e.g., hail, falling trees)

- Use remote start to warm up your car safely (reduces risk of theft or carbon monoxide issues)

Comprehensive coverage is especially valuable in PA due to weather-related damage and animal collisions (deer are a major hazard in rural areas).

Teen Drivers and Family Policies

Adding a teen to your policy can be expensive—but there are ways to soften the blow:

- Keep them on your policy (cheaper than a separate one)

- Enroll them in a driver’s ed course (many insurers offer discounts)

- Choose a safe, used car (avoid sports models)

- Encourage good grades for the good student discount

Some insurers also offer “distracted driving prevention” apps that monitor phone use while driving—another potential discount.

Final Thoughts: Finding the Right Balance

So, how much is car insurance in Pennsylvania? The answer depends on your unique situation—but now you have the tools to find a fair price and the right coverage.

Remember, the cheapest policy isn’t always the best. Minimum coverage might save you money upfront but could leave you vulnerable to massive out-of-pocket costs after an accident. Aim for a balance: enough liability to protect your assets, adequate medical coverage, and optional add-ons like UM/UIM and comprehensive.

And don’t forget to revisit your policy annually. Life changes—new job, new car, improved credit—can all affect your rate. A quick check-in could save you hundreds.

By understanding Pennsylvania’s insurance landscape, comparing quotes, and taking advantage of discounts, you can drive confidently—and affordably—on the roads of the Keystone State.

Frequently Asked Questions

What is the minimum car insurance required in Pennsylvania?

Pennsylvania requires drivers to carry at least 15/30/5 liability coverage ($15,000 per person, $30,000 per accident for bodily injury, and $5,000 for property damage) plus $5,000 in First-Party Benefits for medical expenses.

Is car insurance expensive in Pennsylvania?

Car insurance in Pennsylvania is moderately priced compared to other states. Full coverage averages $1,600–$2,000 per year, which is close to the national average, though urban areas like Philadelphia have higher rates.

Can I choose not to have full tort in Pennsylvania?

Yes. Pennsylvania allows drivers to choose between limited tort (lower cost, restricted lawsuit rights) and full tort (higher cost, full legal rights). Most drivers select limited tort to save money.

Does credit score affect car insurance rates in PA?

Yes. Pennsylvania permits insurers to use credit-based insurance scores, and drivers with poor credit often pay 20–30% more than those with excellent credit.

How can I lower my car insurance premium in Pennsylvania?

Shop around annually, bundle policies, maintain a clean driving record, take advantage of discounts, consider usage-based programs, and raise your deductible if you can afford the out-of-pocket cost.

Do I need uninsured motorist coverage in Pennsylvania?

It’s not required, but highly recommended. With over 12% of PA drivers uninsured, UM coverage protects you if you’re hit by someone without insurance.