How Much Is Car Insurance in Massachusetts?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance in Massachusetts?

- 4 What Does Car Insurance in Massachusetts Cover?

- 5 Factors That Affect Car Insurance Rates in Massachusetts

- 6 Average Car Insurance Costs by City in Massachusetts

- 7 How to Save Money on Car Insurance in Massachusetts

- 8 Filing a Claim in Massachusetts: What to Expect

- 9 Conclusion: Finding the Right Car Insurance in Massachusetts

- 10 Frequently Asked Questions

Car insurance in Massachusetts typically costs between $1,200 and $1,800 per year for full coverage, though rates vary based on location, driving history, and vehicle type. Understanding state requirements and shopping around can help you find the best deal.

Key Takeaways

- Average annual cost: Full coverage car insurance in Massachusetts averages $1,500 per year, while minimum coverage costs around $600.

- State requirements: Massachusetts mandates liability, personal injury protection (PIP), and uninsured motorist coverage.

- Factors affecting rates: Your age, driving record, ZIP code, credit score, and vehicle model all influence your premium.

- Safe driver discounts: Clean records and defensive driving courses can lower your rates significantly.

- Shop around: Comparing quotes from at least three insurers can save you hundreds annually.

- Usage-based programs: Telematics programs like Snapshot or Drive Safe & Save offer discounts for safe driving habits.

- Urban vs. rural: Drivers in Boston or Worcester pay more than those in smaller towns due to higher traffic and theft rates.

📑 Table of Contents

- How Much Is Car Insurance in Massachusetts?

- What Does Car Insurance in Massachusetts Cover?

- Factors That Affect Car Insurance Rates in Massachusetts

- Average Car Insurance Costs by City in Massachusetts

- How to Save Money on Car Insurance in Massachusetts

- Filing a Claim in Massachusetts: What to Expect

- Conclusion: Finding the Right Car Insurance in Massachusetts

How Much Is Car Insurance in Massachusetts?

If you’re a driver in Massachusetts, you’re probably wondering: “How much is car insurance in Massachusetts?” It’s a fair question—after all, auto insurance isn’t just a legal requirement; it’s a financial necessity that protects you, your passengers, and your vehicle on the road. The good news? Massachusetts offers some of the most comprehensive insurance protections in the U.S., including no-fault coverage and strong personal injury protection (PIP). But with great protection comes a price tag—and understanding that cost is the first step to making smart, budget-friendly decisions.

On average, Massachusetts drivers pay between $1,200 and $1,800 per year for full coverage car insurance. That’s about $100 to $150 per month. For minimum coverage—just enough to meet state law—you might pay closer to $500 to $700 annually, or roughly $40 to $60 a month. These numbers aren’t set in stone, though. Your actual rate depends on a mix of personal factors, from where you live to how you drive. And while Massachusetts is known for having slightly lower-than-average insurance rates compared to states like Michigan or Florida, it’s still important to shop around and understand what you’re paying for.

What Does Car Insurance in Massachusetts Cover?

Visual guide about How Much Is Car Insurance in Massachusetts?

Image source: carinsurance.org

Before diving into costs, it’s essential to know what your policy actually includes. Massachusetts has a “no-fault” insurance system, which means your own insurance pays for your medical expenses and lost wages after an accident—regardless of who caused it. This system is designed to reduce lawsuits and get claims settled faster, but it also means your policy must include certain mandatory coverages.

Mandatory Coverage Requirements

In Massachusetts, every driver must carry the following minimum coverages:

- Bodily Injury Liability: $20,000 per person / $40,000 per accident. This covers medical expenses for others if you’re at fault in an accident.

- Property Damage Liability: $5,000 per accident. This pays for damage you cause to another person’s vehicle or property.

- Personal Injury Protection (PIP): $8,000 per person. This covers your medical bills, lost wages, and other expenses, no matter who’s at fault.

- Uninsured Motorist Bodily Injury: $20,000 per person / $40,000 per accident. This protects you if you’re hit by a driver with no insurance.

These are the bare minimums. While they meet legal requirements, they may not be enough to fully protect you in a serious accident. That’s why most financial advisors recommend higher liability limits and additional coverage like collision and comprehensive.

Optional Coverage Add-Ons

Beyond the basics, you can customize your policy with optional coverages that provide extra peace of mind:

- Collision Coverage: Pays to repair or replace your car if it’s damaged in a crash, regardless of fault.

- Comprehensive Coverage: Covers non-collision incidents like theft, vandalism, fire, or weather damage.

- Gap Insurance: Useful if you’re leasing or financing a car. It covers the difference between what you owe and the car’s actual cash value if it’s totaled.

- Rental Reimbursement: Pays for a rental car while your vehicle is being repaired after a covered claim.

- Towing and Labor: Covers the cost of towing and roadside assistance.

Adding these options will increase your premium, but they can save you thousands in out-of-pocket expenses down the road. For example, a comprehensive claim for a stolen catalytic converter—a common issue in urban areas—could cost $2,000 or more without coverage.

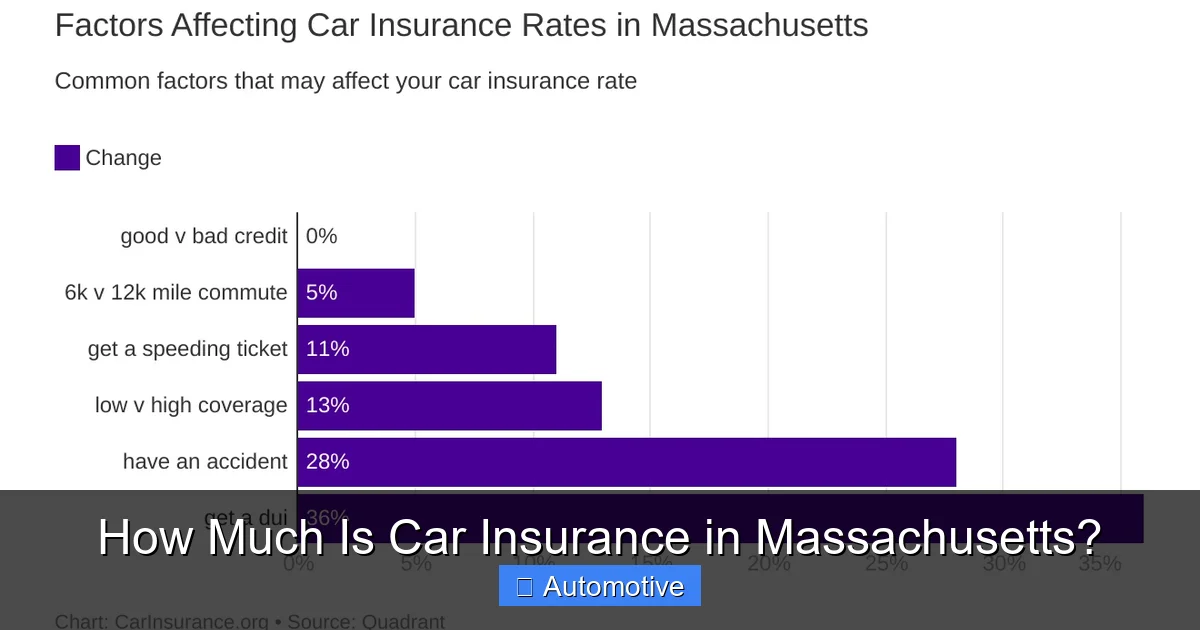

Factors That Affect Car Insurance Rates in Massachusetts

Visual guide about How Much Is Car Insurance in Massachusetts?

Image source: carinsurance.org

Now that you know what’s covered, let’s talk about what determines how much you’ll pay. Insurance companies use a complex formula to calculate your premium, weighing dozens of factors. Some you can control, others you can’t—but understanding them helps you make smarter choices.

Location: Where You Live Matters

Your ZIP code is one of the biggest predictors of your insurance cost. Urban areas like Boston, Worcester, and Springfield tend to have higher rates due to:

- Higher traffic density and accident rates

- Increased risk of theft and vandalism

- More pedestrians and cyclists, raising liability risks

For example, a driver in downtown Boston might pay $1,800 a year for full coverage, while someone in a rural town like Amherst or Pittsfield might pay closer to $1,200. Even within the same city, rates can vary by neighborhood. Areas with higher crime rates or frequent accidents will see steeper premiums.

Age and Driving Experience

Young drivers, especially those under 25, face the highest insurance rates. This is because statistics show that inexperienced drivers are more likely to be involved in accidents. A 19-year-old male in Massachusetts might pay over $3,000 a year for full coverage, while a 35-year-old with a clean record could pay half that.

On the flip side, older drivers (65+) may see rates rise again due to slower reaction times and increased health risks. However, many insurers offer discounts for mature drivers who complete defensive driving courses.

Driving Record and Claims History

Your driving history is a major factor. A clean record with no accidents or violations can qualify you for significant discounts. But even one speeding ticket can increase your premium by 10–20%. A DUI or at-fault accident? That could double your rate.

For example, a driver with a recent at-fault accident might see their annual premium jump from $1,500 to $2,200. Similarly, multiple claims—even for small incidents—can label you a “high-risk” driver, making it harder to find affordable coverage.

Credit Score

In Massachusetts, insurers can use your credit-based insurance score to help determine your rate. While the state limits how much weight credit has, studies show that drivers with poor credit pay significantly more. A person with a credit score below 600 might pay $400 more per year than someone with a score above 750.

Improving your credit—by paying bills on time, reducing debt, and checking for errors on your report—can lead to lower insurance costs over time.

Vehicle Type and Usage

The car you drive affects your premium. High-performance vehicles, luxury cars, and models with high theft rates (like certain SUVs) cost more to insure. For instance, insuring a Toyota Camry will be cheaper than insuring a BMW X5 or a Ford Mustang.

How you use your car also matters. If you commute 50 miles a day, you’ll likely pay more than someone who drives 10 miles for errands. Business use, ride-sharing (like Uber or Lyft), or using your car for deliveries can also increase your rate.

Coverage Level and Deductibles

The more coverage you buy, the higher your premium. Full coverage (liability + collision + comprehensive) costs more than minimum liability alone. But higher coverage limits and lower deductibles also mean higher costs.

For example:

- A $500 deductible on collision coverage might cost $1,500/year.

- Raising the deductible to $1,000 could drop the premium to $1,300/year—saving $200 annually.

Choosing a higher deductible lowers your monthly payment but means you’ll pay more out of pocket if you file a claim. It’s a trade-off between upfront savings and financial risk.

Average Car Insurance Costs by City in Massachusetts

Visual guide about How Much Is Car Insurance in Massachusetts?

Image source: gouldinsurance.com

Let’s look at how rates vary across the state. While statewide averages are helpful, your actual cost depends heavily on where you live.

Boston and Surrounding Areas

As the largest city in Massachusetts, Boston has the highest insurance rates in the state. The combination of heavy traffic, high population density, and frequent accidents drives up premiums. On average, Boston drivers pay:

- Full coverage: $1,700–$2,000 per year

- Minimum coverage: $700–$900 per year

Neighboring cities like Cambridge, Somerville, and Quincy have similar rates due to their urban environments and proximity to Boston.

Worcester and Central Massachusetts

Worcester, the second-largest city, also sees elevated rates, though not as high as Boston. Expect to pay:

- Full coverage: $1,500–$1,700 per year

- Minimum coverage: $600–$750 per year

Smaller towns in the region, like Fitchburg or Leominster, offer slightly lower premiums due to less traffic and lower crime rates.

Western Massachusetts (Springfield, Amherst, Pittsfield)

Western Massachusetts tends to be more affordable. Cities like Springfield have moderate rates, while college towns like Amherst (home to UMass) see slightly higher costs due to young drivers. Rural areas like Pittsfield offer the lowest premiums in the state:

- Full coverage: $1,200–$1,400 per year

- Minimum coverage: $500–$600 per year

Southeastern Massachusetts (Fall River, New Bedford, Cape Cod)

This region offers a mix of urban and coastal living. Fall River and New Bedford have higher rates due to older infrastructure and higher accident rates. Cape Cod towns like Hyannis or Provincetown are more expensive in summer due to tourism and increased traffic, but quieter in winter.

Average costs:

- Full coverage: $1,400–$1,600 per year

- Minimum coverage: $550–$700 per year

How to Save Money on Car Insurance in Massachusetts

Nobody likes overpaying for insurance. The good news? There are plenty of ways to reduce your premium without sacrificing coverage.

Shop Around and Compare Quotes

One of the most effective ways to save is by comparing quotes from multiple insurers. Rates can vary by hundreds of dollars between companies for the same coverage. Use online comparison tools or work with an independent agent to get quotes from:

- GEICO

- State Farm

- Progressive

- Liberty Mutual

- MAPFRE (a popular choice in Massachusetts)

Don’t just look at the price—check customer service ratings, claims satisfaction, and available discounts.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Common ones include:

- Safe Driver Discount: For drivers with no accidents or violations in the past 3–5 years.

- Multi-Policy Discount: Save 10–25% by bundling auto and home or renters insurance.

- Good Student Discount: Full-time students with a B average or higher may qualify.

- Defensive Driving Course: Completing an approved course can reduce your rate by 5–10%.

- Low Mileage Discount: If you drive fewer than 7,500 miles per year.

- Anti-Theft Device Discount: Vehicles with alarms, tracking systems, or VIN etching may qualify.

Ask your insurer about all available discounts—you might be missing out on savings.

Consider Usage-Based Insurance

Telematics programs like Progressive’s Snapshot, State Farm’s Drive Safe & Save, or Allstate’s Drivewise monitor your driving habits through a mobile app or plug-in device. If you drive safely—avoiding hard braking, speeding, and late-night driving—you could earn discounts of 10–30%.

These programs are especially helpful for young drivers or those with less-than-perfect records. Just remember: your driving is being tracked, so honesty is key.

Raise Your Deductible

As mentioned earlier, increasing your deductible from $500 to $1,000 can save you $100–$200 per year. Just make sure you have enough savings to cover the higher out-of-pocket cost if you need to file a claim.

Maintain a Good Credit Score

Since credit affects your rate, work on improving your score. Pay bills on time, keep credit card balances low, and check your credit report annually for errors.

Review Your Policy Annually

Life changes—and so should your insurance. If you’ve moved, gotten married, paid off your car, or started working from home, your needs may have changed. Review your policy each year to ensure you’re not over-insured or under-insured.

Filing a Claim in Massachusetts: What to Expect

Even with the best coverage, accidents happen. Knowing how to file a claim can reduce stress and help you get back on the road faster.

Steps to Take After an Accident

1. Ensure Safety: Move to a safe location if possible and call 911 if there are injuries.

2. Exchange Information: Get the other driver’s name, contact info, license plate, and insurance details.

3. Document the Scene: Take photos of damage, skid marks, and road conditions.

4. Report the Accident: In Massachusetts, you must report any accident with injuries or over $1,000 in damage to the RMV within 10 days.

5. Contact Your Insurer: File a claim as soon as possible. Most companies have 24/7 claims lines.

No-Fault Claims Process

Because Massachusetts is a no-fault state, your own PIP coverage pays for your medical bills first—up to $8,000. If your injuries exceed that amount or meet the “serious injury” threshold (like broken bones or permanent disability), you may sue the at-fault driver for additional damages.

Your insurer will investigate the claim, assess damage, and coordinate repairs. Most claims are resolved within 30 days, but complex cases may take longer.

Conclusion: Finding the Right Car Insurance in Massachusetts

So, how much is car insurance in Massachusetts? On average, expect to pay $1,500 per year for full coverage and $600 for minimum coverage. But your actual cost depends on your location, driving history, vehicle, and coverage choices.

The key to getting the best rate is understanding your options and shopping smart. Compare quotes, take advantage of discounts, and consider usage-based programs. Don’t just go with the first offer—your wallet (and peace of mind) will thank you.

Remember, the cheapest policy isn’t always the best. Make sure you have enough coverage to protect your assets and financial future. And if you’re ever unsure, talk to a licensed insurance agent who can help you navigate the complexities of Massachusetts auto insurance.

With the right policy, you can drive confidently—knowing you’re protected, no matter what the road brings.

Frequently Asked Questions

What is the minimum car insurance required in Massachusetts?

In Massachusetts, drivers must carry at least $20,000 in bodily injury liability per person, $40,000 per accident, $5,000 in property damage liability, $8,000 in personal injury protection (PIP), and uninsured motorist coverage matching the liability limits.

Why is car insurance so expensive in Boston?

Boston has high traffic density, frequent accidents, and elevated theft and vandalism rates, all of which drive up insurance costs. Urban areas also have more pedestrians and cyclists, increasing liability risks.

Can I get car insurance with a bad driving record in Massachusetts?

Yes, but it will cost more. High-risk drivers can still get coverage through standard insurers or state-assigned risk pools, though premiums will be significantly higher due to increased risk.

Do I need full coverage car insurance in Massachusetts?

Full coverage isn’t legally required, but it’s highly recommended if you own a newer or financed vehicle. It protects you from costly repairs and theft, offering greater financial security.

How can I lower my car insurance premium in Massachusetts?

You can save by shopping around, raising your deductible, maintaining a clean driving record, taking defensive driving courses, bundling policies, and using telematics programs to earn safe driving discounts.

Does Massachusetts use credit scores to determine insurance rates?

Yes, Massachusetts allows insurers to use credit-based insurance scores as a rating factor, though the impact is limited by state regulations. Drivers with higher credit scores typically pay lower premiums.